English

English

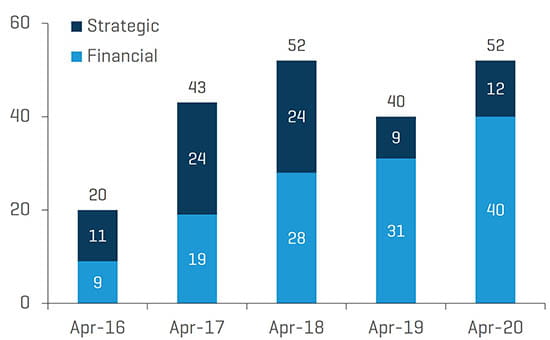

The first quarter of 2020 saw the highest number of announced North American metal forming transactions in the past eight years. Quarterly transaction volume increased 60% over the fourth quarter of 2019 and almost 80% over the same quarter last year. Private equity buyers continue to drive deal activity, accounting for approximately 75% of transactions announced in the first quarter. A closer look at the data, however, illustrates a significant slowdown as the impact of COVID-19 takes hold: Only seven transactions were announced in March and three in April. While there remains abundant private equity capital available to invest, both buyers and lenders are approaching new deals with caution. Sale processes that were prepared to launch have been put on hold while sellers assess the impact of COVID-19 on their businesses and travel restrictions impair buyer due diligence. The payroll protection program has provided liquidity for metal forming companies and allowed lenders to exercise patience, but an increase in special situation transactions is likely if company performance suffers for an extended period.

Key Takeaways:

- After a record start to the year, metal forming transaction volume declined significantly in March and April

- Financial buyers dominate metal forming transaction volume

- Abundant capital available from private equity and strategic buyers, but few new deals coming to market

- Uncertainty exists around availability of debt financing

- Special situations M&A activity is expected to increase

- Public company share prices and valuations suffered in the first quarter due to historic declines in the stock market

- Metal prices under pressure with automotive shutdowns and collapse in energy prices

Quarterly Metal Forming M&A Volume

Source: Stout Research

Stout Proprietary Metal Forming M&A Database Highlights

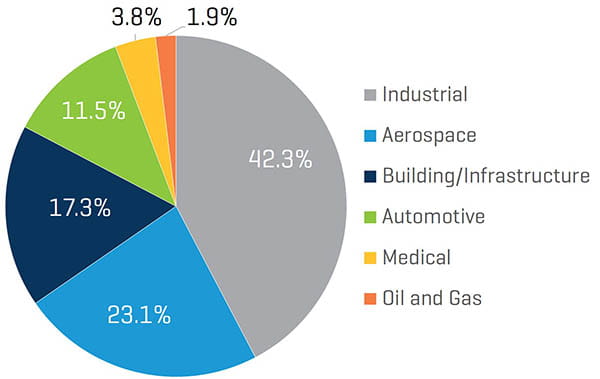

Financial buyers accounted for approximately three-fourths of metal forming transaction volume, roughly in line with the same period last year. The number of Aerospace transactions increased 100% over 2019 and represented almost a quarter of deals announced year-to-date. Industrials continue to constitute the bulk of transaction activity, increasing 38% year over year. Volumes in the remaining metal forming sectors were relatively flat versus the prior-year period.

Share of Transactions by Buyer Type (YTD through April)

Source: Stout Research

Year-to-Date Transaction Volume by Sector

Source: Stout Research

Notable transactions announced through April 2020 include:

- Stanley Black & Decker Inc.’s (NYSE:SWK) acquisition of Consolidated Aerospace Manufacturing, LLC from Tinicum L.P. for approximately $1.5 billion, or 4.0x 2019 revenue

- RTI Surgical Holdings, Inc.’s (Nasdaq: RTIX) announced divestiture of the Company’s OEM business to Montagu Private Equity LLP for a total consideration of $490 million

- Kymera International’s, a portfolio company of Palladium Equity Partners, LLC, acquisition of Reading Alloys from AMETEK, Inc. (NYSE:AME) for approximately $250 million, or 1.6x annual revenue

- Placements CMI Inc. (Marcel Dutil family), Fonds de solidarité FTQ and Caisse de dépôt et placement du Québec’s acquisition of the Canadian operations and certain assets in the United States and Overseas of Canam Group Inc. for C$840 million

- Bendix Commercial Vehicle Systems LLC’s announced acquisition of R. H. Sheppard Co., Inc. from WABCO Holdings Inc. (NYSE:WBC) for approximately $150 million

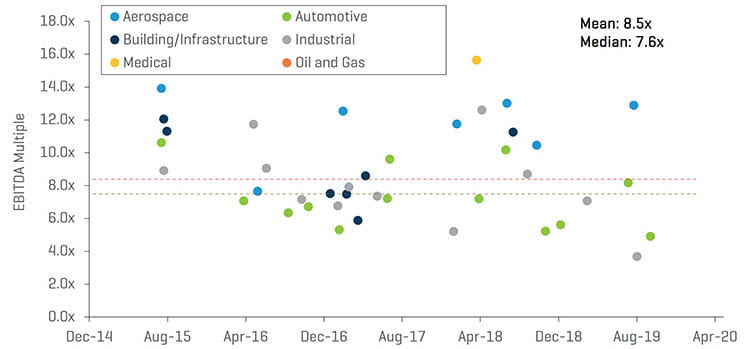

Announced metal forming transactions through April 2020 did not yield any new enterprise value-to-EBITDA (EV/EBITDA) multiples

Select Transaction EV/EBITDA Multiples

Source: Stout Research

Public Company Performance

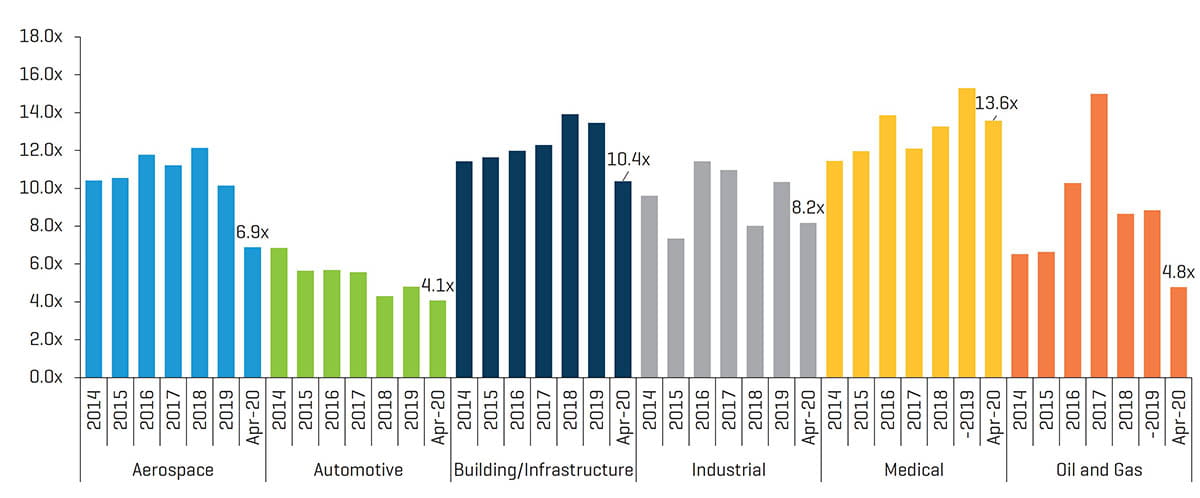

After a bull market that has lasted for over a decade, the U.S. stock market saw one of the worst quarterly declines in history as the COVID-19 crisis unfolded. For the first three months of 2020, the Dow was down approximately 23%, while the S&P 500 and Nasdaq were down 20% and 14%, respectively. Within the metal forming industry, EV/EBITDA multiples for all sectors were down in April as compared with the end of 2019.

Public Companies: Last-12-Month (LTM) EV/EBITDA Multiples (December 31, 2014 to April 30, 2020)

Source: S&P CapIQ

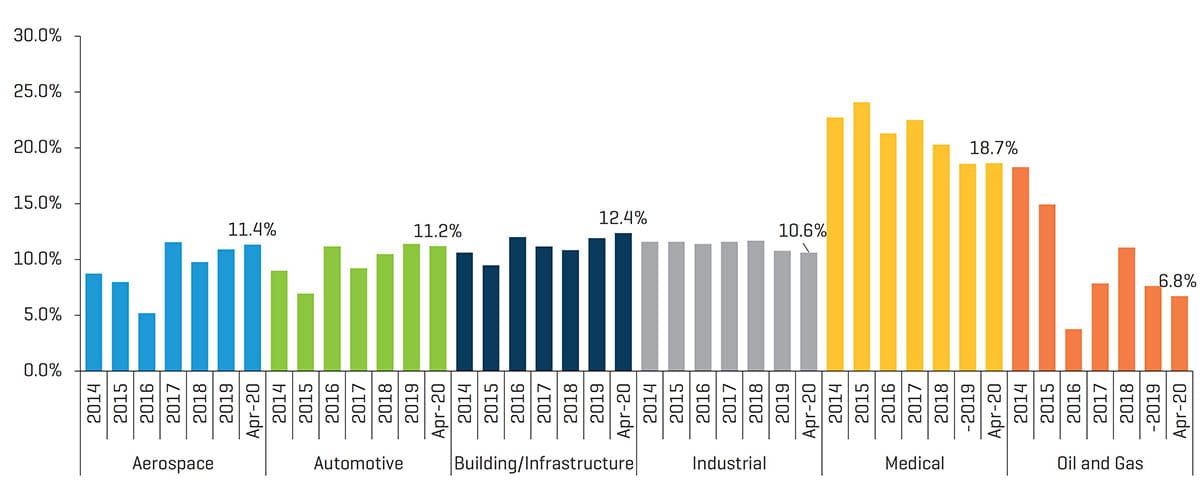

Public Companies: LTM EBITDA Margins (December 31, 2014 to April 30, 2020)

Source: S&P CapIQ

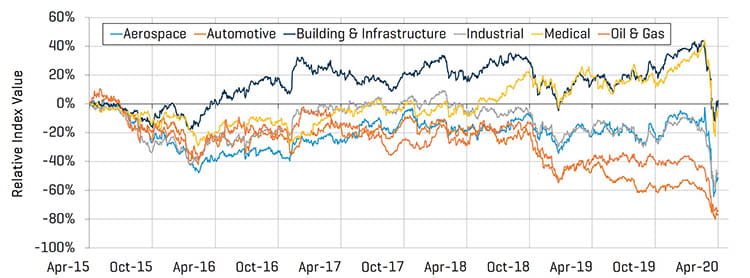

As expected, all metal forming indices have seen negative impacts from recent market volatility surrounding COVID-19; all sectors are trading at or below April 2015 levels. Despite the downward pressure caused by the broader market, the Medical, Building & Infrastructure, Industrial and Aerospace sectors have seen stable increases from the market rally beginning the last week of March.

Public Companies: Relative Share Price Performance (April 1, 2015 to April 30, 2020)

Source: S&P CapIQ

Metal Pricing

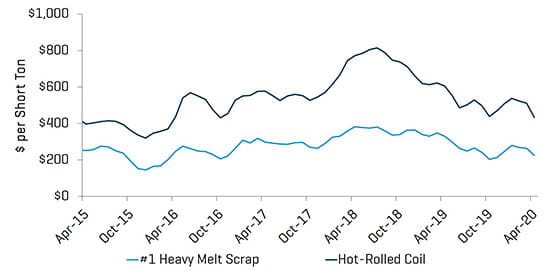

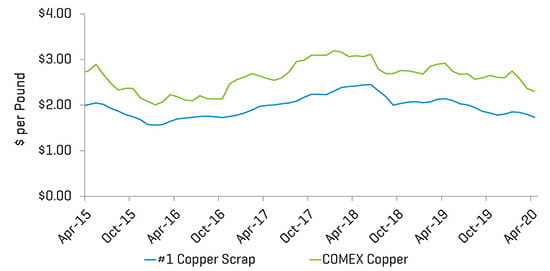

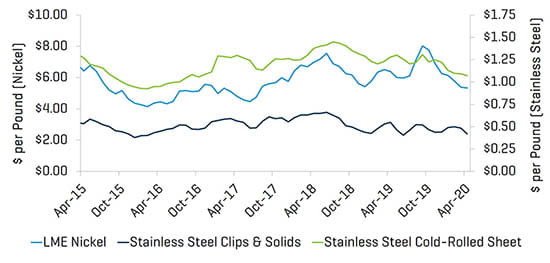

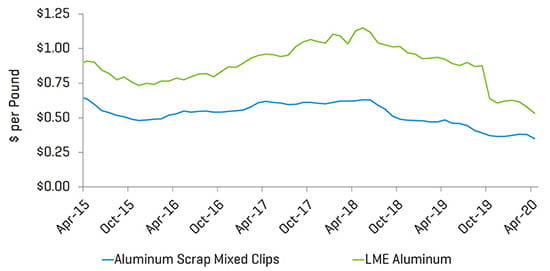

Domestic metals prices suffered in the first quarter from anticipated declines in automotive, commercial aerospace, building products and other industrial production. The collapse in energy prices and drilling activity have also taken a toll on finished metal and scrap prices, although ferrous scrap prices have rebounded in the second quarter as automotive and scrapyard shutdowns crimped supply.

Steel

Source: American Metal Market

Copper

Source: American Metal Market

Stainless Steel

Source: American Metal Market

Aluminum

Source: American Metal Market

This industry update analyzes Stout’s custom public company indices and proprietary M&A transaction database of North American metal forming transactions. Targeted companies include casting, extrusion, finishing, forging, machining, stamping, and various other processing and fabrication businesses across a wide range of end markets.