English

English

Metal forming M&A activity in 2019 almost kept pace with 2018’s record volumes with private equity firms driving over half of announced transactions. While public company valuations and margins generally remained strong through the end of the year, the ultimate economic impact of the Covid-19 virus outbreak and resulting equity market sell-off is still unknown.

Key Takeaways:

- Outside of the broad Industrial sector, the Aerospace sector was particularly active with 19% of announced transactions in 2019

- Transactions involving private equity sellers and buyers accounted for over half of all transactions announced in 2019

- Public company margins and valuations fared well in 2019, but have come under pressure as a result of the recent equity market turmoil

- The runup in steel and aluminum ahead of the 2018 Section 232 tariffs reversed course in 2019 and market participants are expecting less volatility in 2020

Stout Proprietary Metal Forming M&A Database Highlights

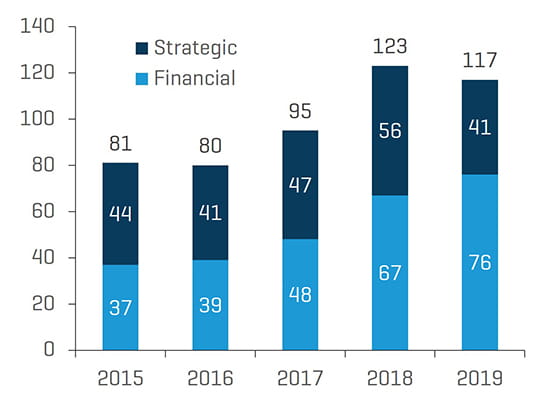

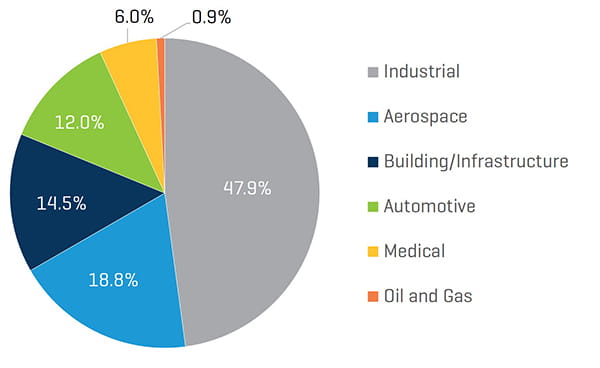

Metal forming M&A activity finished strong in 2019, nearly matching record volumes in 2018. Financial buyers represented almost two-thirds of transaction volume. Outside of the broad Industrial sector, Aerospace and Building/Infrastructure companies accounted for a third of transactions last year.

Share of Transactions by Buyer Type

Source: Stout Research

Year-to Date Transaction Volume by Sector

Source: Stout Research

Notable transactions announced in the fourth quarter of 2019 include:

- Martinrea International, Inc.’s acquisition of Metalsa S.A. de C.V.’s automotive structural components operations

- KKR & Co., Inc.’s acquisition of Novaria Holdings, LLC from Rosewood Private Investments and Tailwind Advisors

- Pella Corporation’s acquisition of Custom Window Systems, Inc. from Nautic Partners, LLC

- Kaman Aerospace Group, Inc.’s acquisition of Bal Seal Engineering, Inc.

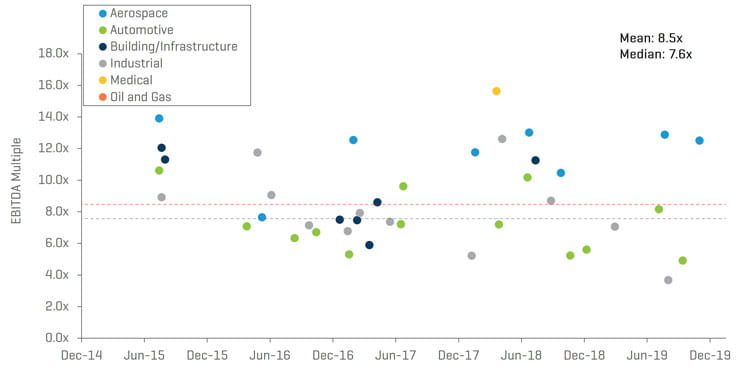

Select Transaction EV/EBITDA Multiples

Source: Stout Research

Public Company Performance

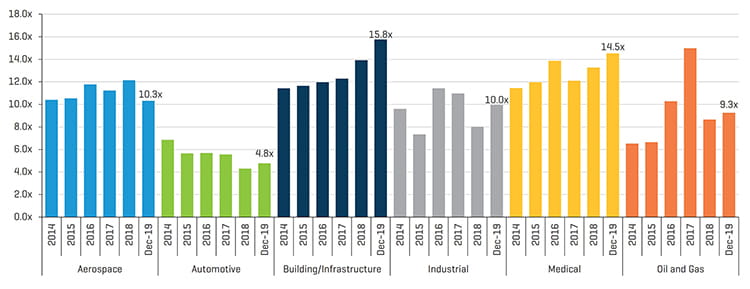

Valuations and margins for publicly traded metal forming companies fared well during 2019. The Building/Infrastructure sector had the highest relative average forward EV/EBITDA multiple at year-end while Automotive had the lowest. Valuations have since contracted alongside the market sell-off associated with the Covid-19 virus outbreak. It remains to be seen what impact the virus will have on metal forming company earnings over the coming quarters.

Public Companies: Forward EV/EBITDA Multiples (December 31, 2014 to December 31, 2019)

Source: S&P CapIQ

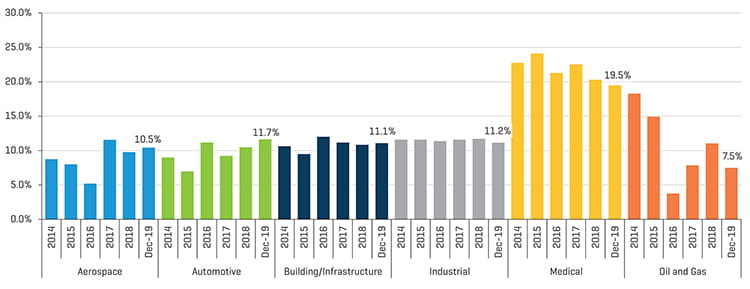

Public Companies: Latest-Twelve Months (“LTM”) EBITDA Margins (December 31, 2014 to December 31, 2019)

Source: S&P CapIQ

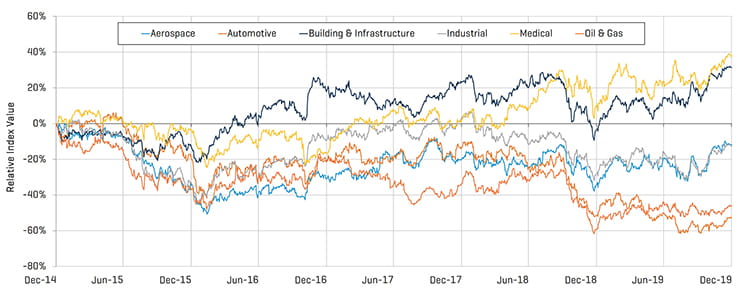

Fueled by strong performance in the broader equity markets last year, share prices in the Building/Infrastructure and Medical sectors continued to outperform other metal forming sectors. However, all indices have been negatively impacted by recent market volatility surrounding Covid-19.

Public Companies: Relative Share Price Performance (December 31, 2014 to December 31, 2019)

Source: S&P CapIQ

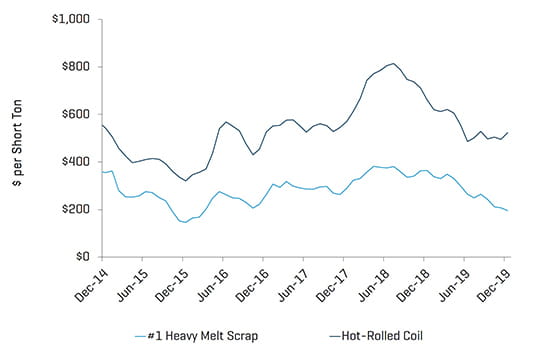

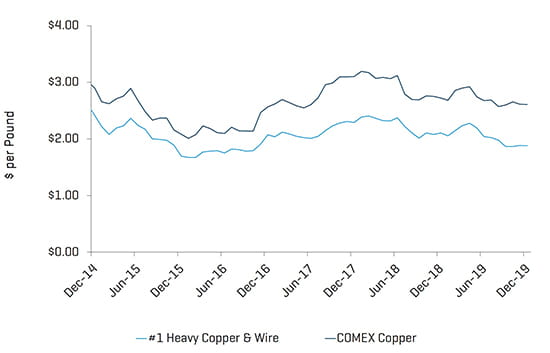

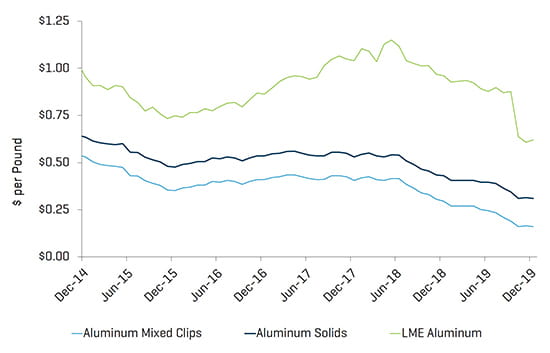

Metal Pricing

Domestic finished steel and aluminum prices retreated from 2018 highs driven by Section 232 tariffs. Meanwhile, spreads between hot-rolled steel coil and scrap widened in the second half of the year, suggesting there could be some downward pressure on steel prices in 2020. Overall, market participants are anticipating a more stable metals pricing environment in 2020 absent the volatility caused by Section 232 tariffs over the past two years.

Steel

Source: American Metal Market

Copper

Source: American Metal Market

Stainless Steel

Source: American Metal Market

Aluminum

Source: American Metal Market

This industry update analyzes Stout’s custom public company indices and proprietary M&A transaction database of North American metal forming transactions. Targeted companies include casting, extrusion, finishing, forging, machining, stamping, and various other processing and fabrication businesses across a wide range of end markets.