English

English

The industrial services industry ended the second half of 2019 with strong transaction volume domestically and internationally. Following an active first half, the public markets continued their upward rise during the last two quarters with most segments realizing positive returns. In conjunction with the public markets, trading multiples trended positively in the second half, with LTM EBITDA margins showing relative expansion across the board.

The continued technological advancement and development of various industrial equipment has led to more robust implementation, helping propel growth across the industrial services industry. Services surrounding evolving predictive maintenance and the Industrial Internet of Things (IIoT) are becoming more important for firms to adapt, as these advancements have allowed a higher level of connectivity and efficiency to make more-informed decisions as it relates to overall performance and service needs. Strategic buyers and private equity firms continue to seek attractive services-based commercial and industrial firms with competitive edges regarding service capabilities and expansive geographic coverage. Private equity continues to be active on both sides of transactions, putting capital to work in new platform and bolt-on investment opportunities. Large industry players are utilizing an acquisitive growth approach, as cross-border transaction activity remains prominent.

Geopolitical activity regarding trade tariffs and domestic infrastructure spending with the recent passing of the fiscal Transportation Funding Bill will be headlines to watch in 2020 with respect to expected performance in industrial services.

Key Takeaways

- Continued strong overall industrial services M&A activity, with international strength in certain segments

- Increased emphasis on sustainability and automation drive change across key industrial services segments as mechanized data collection, exchange, and analysis facilitate improvements in productivity and efficiency

- Public equity performance remains consistently robust following a strong first half of 2019

- Public Company valuation multiples are up from the 2018 three-year low but still down from 2017 highs

- Positive macroeconomic trends, despite pockets of turbulence regarding tariffs and political uncertainty

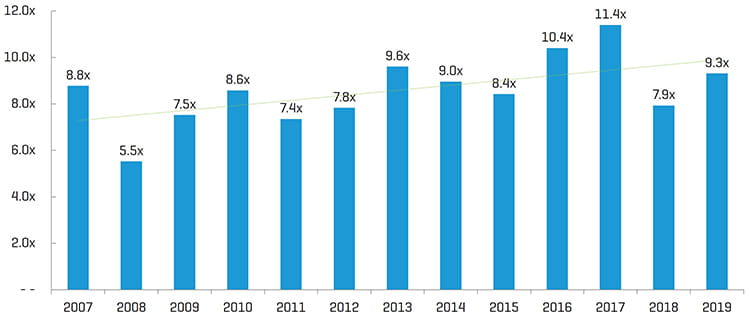

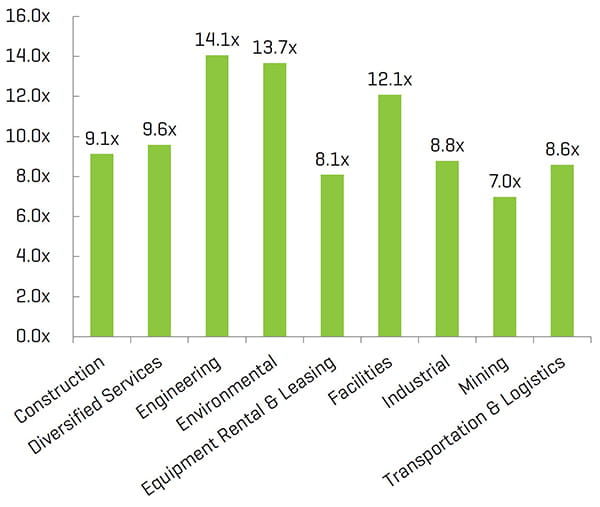

Historical Enterprise Value / EBITDA Multiples[1]

Industry Statistics

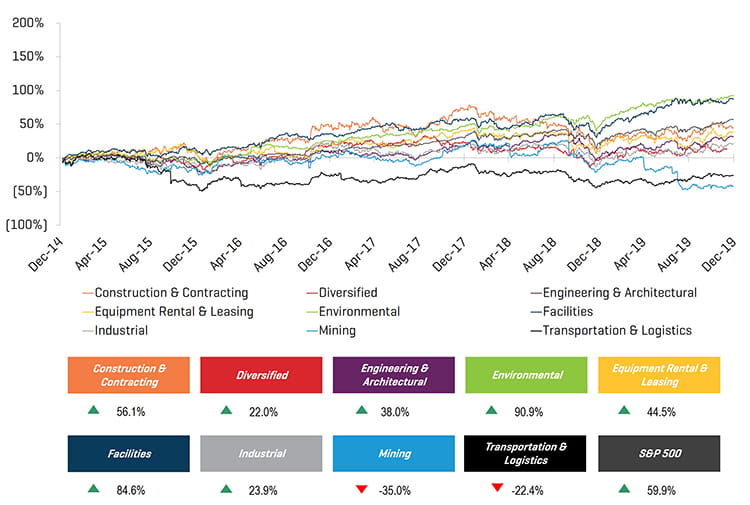

5-Year Historical Share Price Performance

Note: Public comp set has been updated to correspond with the Engineering & Construction Year in Review 2019 report.

Operating and Market Performance

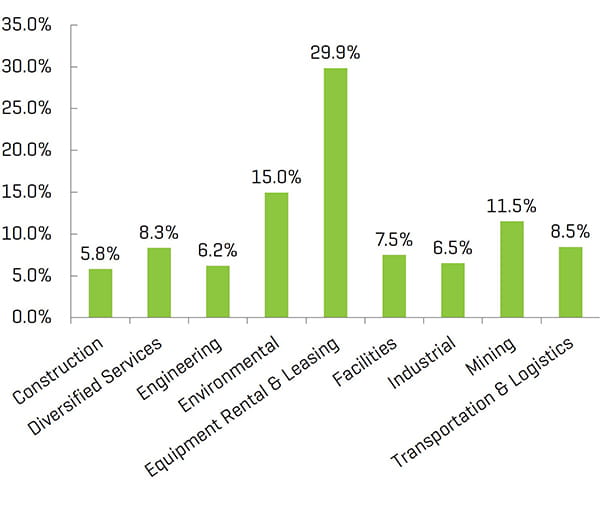

LTM EBITDA Margin

Enterprise Value / LTM EBITDA[1,2]

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Median from public comp sets featured in report

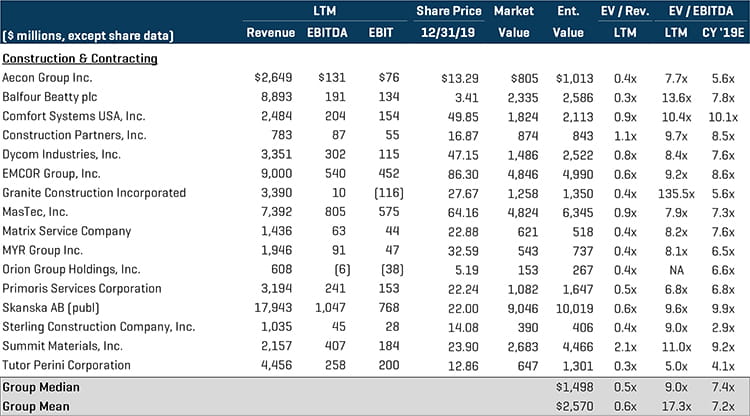

Construction & Contracting Services

The construction and contracting services segment continued to experience industry consolidation, as demonstrated by strategic and hybrid buyer roll-up activity. Private equity-backed buyers completed several transactions throughout the second half focused on expanding the scale and geographic reach of respective platform investments. As rapid changes in technology, automation, and federal policy continue, the infrastructure pipeline in North America remains strong as opportunities to construct sustainable buildings, optimizing energy efficiency and low carbon emissions have been driving service design. Notable transactions include [For more details see Stout's Engineering and Construction 2019 Year in Review report]:

- Plateau Excavation, Inc. was acquired by Sterling Construction Company, Inc. (NYSE:STRL) for approximately $399.1 million in August. Plateau is a full-service infrastructure site improvement contractor headquartered in Austell, GA

- Quanta Services, Inc. (NYSE:PWR) has agreed to acquire The Hallen Construction Company, Inc., a distribution contracting and construction services provider to the utilities sector, in a transaction valued at approximately $330.0 million

- Kirlin Design Build, a Maryland-based engineering and construction company for large, complex federal and private sector projects, was acquired by Blue Wolf Capital Partners, LLC

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

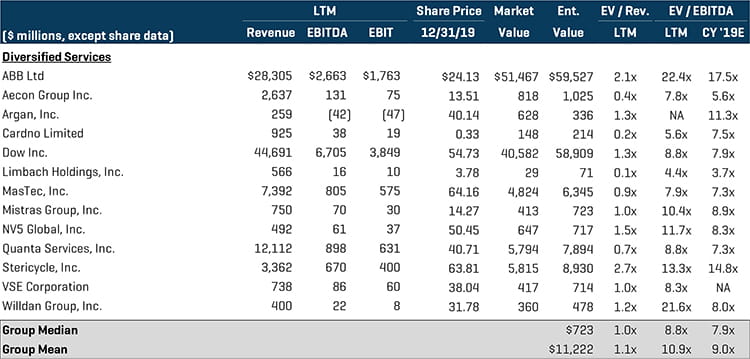

Diversified Services

The diversified services segment saw a mixture of large strategic acquisition activity as industry players pursue complimentary service offerings and capabilities, as well as private equity buyers diversifying industrials-oriented portfolios. Notable transactions include:

- Advanced Drainage Systems, Inc. (NYSE:WMS) announced that it has acquired Infiltrator Water Technologies, LLC, a leading provider of various onsite wastewater and water industry products, for approximately $1.1 billion

- J2 Acquisition Limited (LSE:JTWO) acquired APi Group, Inc., market-leading provider of commercial life safety solutions and industrial specialty services, for approximately $2.3 billion. With the closing of the transaction, J2 will be renamed to APi Group Corp.

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

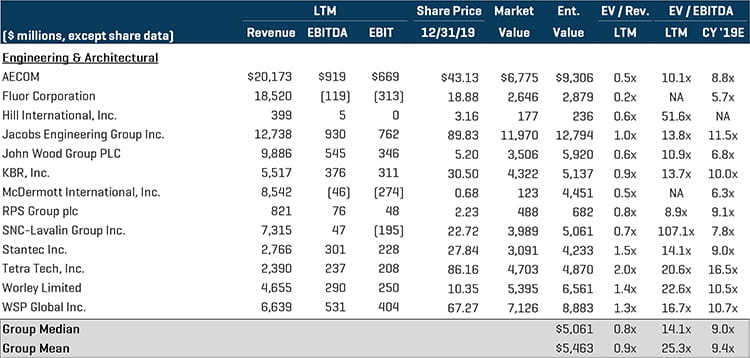

Engineering & Architectural Services

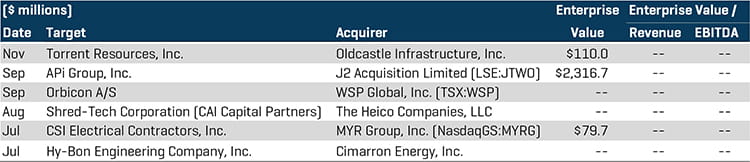

The engineering and architectural services segment continued to trade at the highest multiples in the group. Private equity buyers were active in the second half of 2019 executing platform and add-on acquisitions, in addition to exiting current investments. Notable transactions include [For more details see Stout's Engineering and Construction 2019 Year in Review report]:

- CSI Electrical Contractors, Inc., a leading provider of electrical design, engineering, and construction services to various industrial, residential, and commercial projects, has been acquired by MYR Group, Inc. (NasdaqGS:MYRG) for approximately $79.7 million. MYR Group was founded in 1891 and provides electrical construction services throughout North America

- Toshiba Corp. (TSE:6502) acquired the remaining 50.1% of Toshiba Plant Systems & Services Corp. (TSE:1983), an engineering constructor in the Asia-Pacific, for approximately $1.5 billion

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

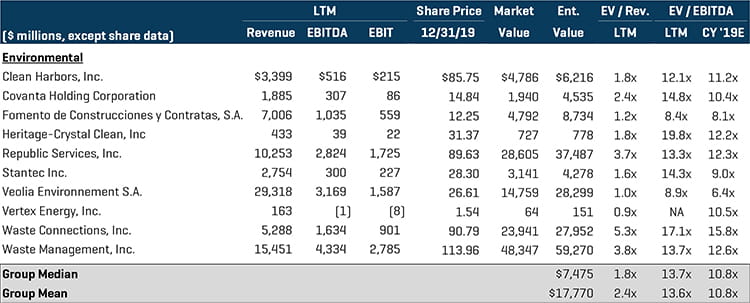

Environmental Services

The environmental services segment finished the second half with strong M&A volume, as private equity firms continue to seek out advantages with the changing of regulations and technology. Strategic buyers remain active in the space, consolidating regional players and expanding service offerings, in order to increase competitive competencies. Notable transactions include:

- WSP Global, Inc. (TSX:WSP), agreed to acquire Ecology & Environment, Inc., a portfolio company of Mill Road Capital Management, LLC, in a transaction valued at approximately $51.3 million. Ecology & Environment is an environmental consulting company, offering various development services such as feasibility studies, biological survey, and critical flaw assessments, among others

- Voith GmbH & Co. KGaA, a German multinational corporation serving the energy, oil & gas, raw materials, and transport & automotive markets, announced that it has acquired BTG Eclepens S.A., a process solutions provider for the pulp and paper industry, for approximately $353.2 million

- Golden Gate Capital announced it has sold Hillstone Environmental Partners, LLC to NGL Water Solutions Permian, LLC for approximately $600.0 million. Hillstone provides water management solutions for the oil and gas industry

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

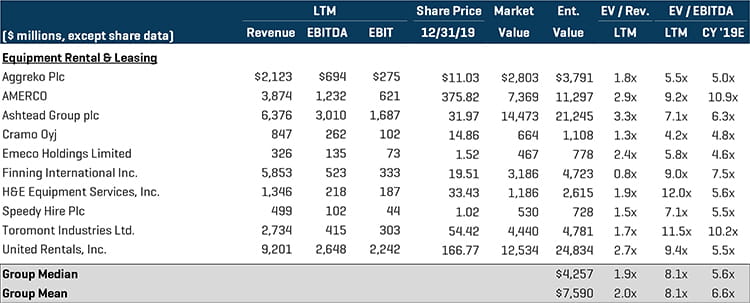

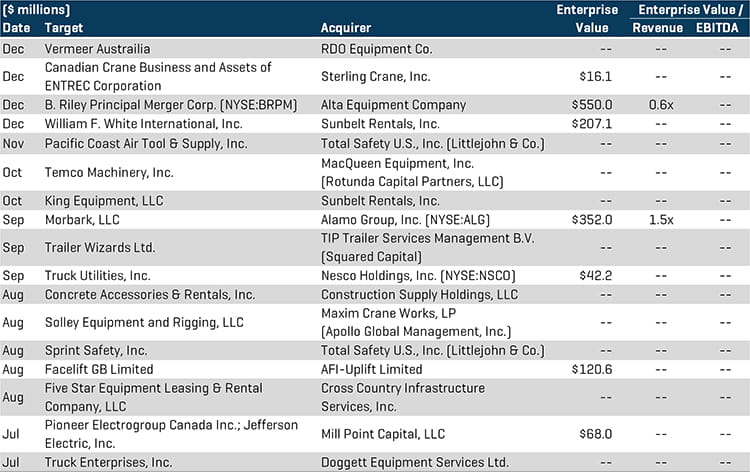

Equipment Rental & Leasing

The equipment rental and leasing segment continued to benefit from industry consolidation among large strategic serial acquirers pursuing roll-up acquisitions to expand geographic footprint, fleet size, and service capabilities. Private equity firms were also active in this segment. Notable transactions include:

- Morbark, LLC, a land-clearing and recycling solutions provider, was acquired by Alamo Group, Inc. (NYSE:ALG) for approximately $352.0 million. Alamo Group designs and manufactures agricultural and infrastructure maintenance equipment

- Sunbelt Rentals, Inc. announced that it has acquired William F. White International, Inc., a rental and service provider of theatrical production equipment headquartered in Ontario, for approximately $207.1 million

- Sunbelt Rentals, Inc. also announced that it has acquired King Equipment, LLC, a construction equipment lessor in Santa Fe Springs, CA

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

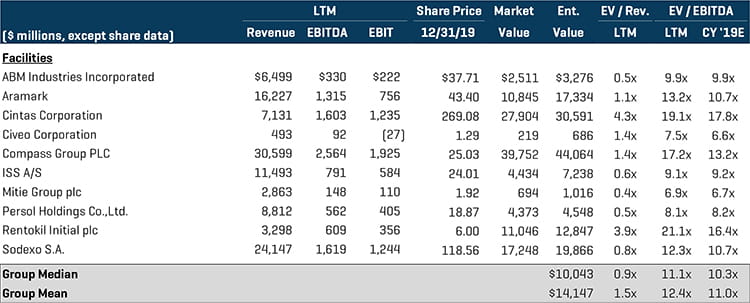

Facilities Services

The facilities services segment continued to see aggressive platform and add-on acquisition from private equity buyers, as an emphasis on regulatory compliance and an increasing demand for integrated facility management continues to propel market development. Notable transaction details include:

- Harsco Corp. (NYSE:HSC) has announced its acquisition of CEHI Acquisition Corp., an operating subsidiary of Compass Diversified Holdings, LLC (NYSE:CODI), for approximately $628.0 million. CEHI provides a range of facilities and environmental services and is headquartered in Westport, CT

- Nomor Holding AB, a Stockholm-based sanitation services provider, was acquired by ServiceMaster Global Holdings, Inc. (NYSE:SERV). The transaction closed in September and carried a transaction value of approximately $200.0 million

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

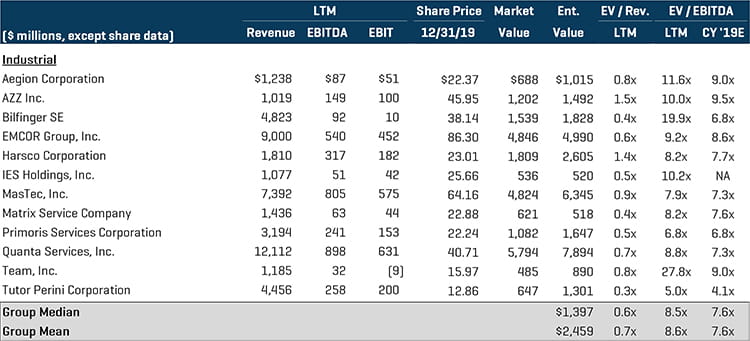

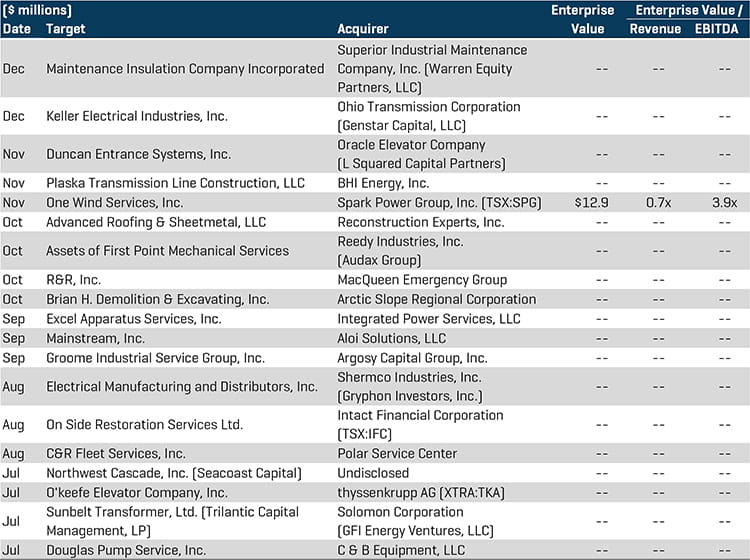

Industrial Services

The industrial services segment continues to be an attractive segment for both strategic and private equity buyers, given the abundance of targets throughout the space. Private equity add-on acquisition activity continued to lead industrial services’ strong deal volume in the second half as financial buyers seek to diversify portfolio company service capabilities through a roll-up strategy. Notable transactions include:

- Groome Industrial Service Group, Inc. was acquired by Argosy Capital Group, Inc., a private equity firm headquartered in greater Philadelphia. Groome offers nationwide specialty maintenance services, ranging from surface preparation to industrial cleaning and support

- Oracle Elevator Company, a portfolio company of L Squared Capital Partners, announced its acquisition of Duncan Entrance Systems, Inc., a provider of commercial automatic door installation and maintenance services

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

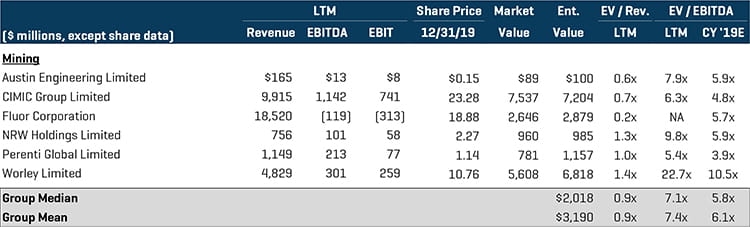

Mining Services

International M&A activity remained a key driver for continued consolidation in the mining services industry in the second half of 2019. Companies continue to be subject to intense competition, as access to attractive geographic locations and technological capabilities remain paramount to potential investors. Notable transactions include:

- Outotec Oyj (HLSE:OTE1V) has entered into a demerger plan and a combination agreement to acquire Metso Minerals Oy from Metso Corp. (HLSE:METSO). The agreement is still pending with a total transaction size of approximately $3.3 billion

- Keystone Capital, Inc., a private equity firm headquartered in Chicago, announced that it has acquired Lane Power & Energy Solutions, Inc., a project development company focused on the use of solution-mined caverns in salt formations for hydrocarbon and waste management projects

- NRW Holdings Limited (ASX:NWH), an Australian mining, construction, and maintenance service provider, has announced that it has acquired BGC Contracting Pty Ltd, an Australia-based contract miner, building constructor, and heavy road haulage service provider, for approximately $213.8 million

Public Comparables[1]

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Implies a 100% enterprise value

(3) Transaction status is pending

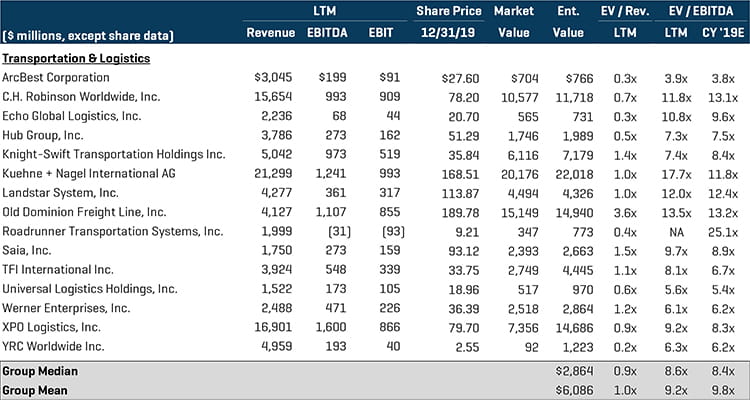

Transportation & Logistics

M&A activity in the transportation and logistics segment remained robust as strategic buyers continue to seek targets that will expand core competencies and geographic reach. Activity among private equity buyers in this segment remains dynamic, as there are many technologically advanced providers within the broader logistics industry looking to tap into new geographies and expand service offerings. Notable transactions include:

- Nova Cold Logistics, a portfolio company of Brookfield Business Partners, LP, has been acquired by Americold Realty Trust (NYSE:COLD) for approximately $253.7 million. Nova provides temperature-controlled logistics services and is headquartered in Canada

- Energy Transfer, LP (NYSE:ET), a leading provider of gas transportation and storage services, entered into a definitive agreement to acquire SemGroup Corp. (NYSE:SEMG) for approximately $1.4 billion. SemGroup provides transportation, storage, distribution, and other midstream services for producers and refiners of petroleum products

Public Comparables[1]

Select M&A Transactions