English

English

Industrial services M&A activity remained vigorous in the third quarter of 2018 as industry leaders consolidate market segments, chasing service offering diversification and expanded geographical presence. Private equity firms are seen active on both sides of the transaction; exiting positions to realize favorable returns in the strong M&A market and pursuing new platform investments and add-on acquisitions. Share price performance remains relatively flat over the third quarter, accompanied by constant last-12-month EBITDA margins and trading multiples; however, industry growth remains optimistic as end markets such as manufacturing, construction, and oil and gas continue to benefit from positive industry dynamics. Additionally, continuous technological advances have forced a greater emphasis on process improvement and industrial automation, which will ultimately provide more opportunity for companies providing industrial services.

Key Takeaways

- Continued strong overall industrial services M&A activity

- Revenue growth across all segments exhibits strong industry dynamics

- Internet of Things (IoT) movement driving significant growth in the transportation and logistics segment

- Rising commercial construction activity surging demand for facility support services

- Cross-border M&A activity continued to surge as large, public corporations seek to diversify by expanding geographic presence

- Valuation multiples remain steady

- Continued low cost of capital and high capital availability

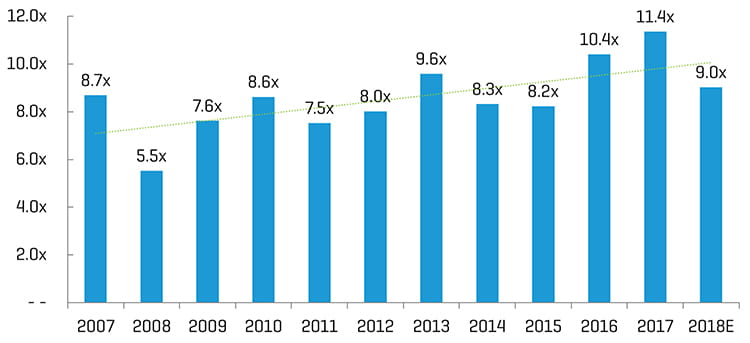

Historical Enterprise Value / EBITDA Multiples[1]

(1) Multiples above 20x are excluded from the mean/median calculation; data represents the overall median of all nine subsegment benchmarks presented in this report

Industry Statistics

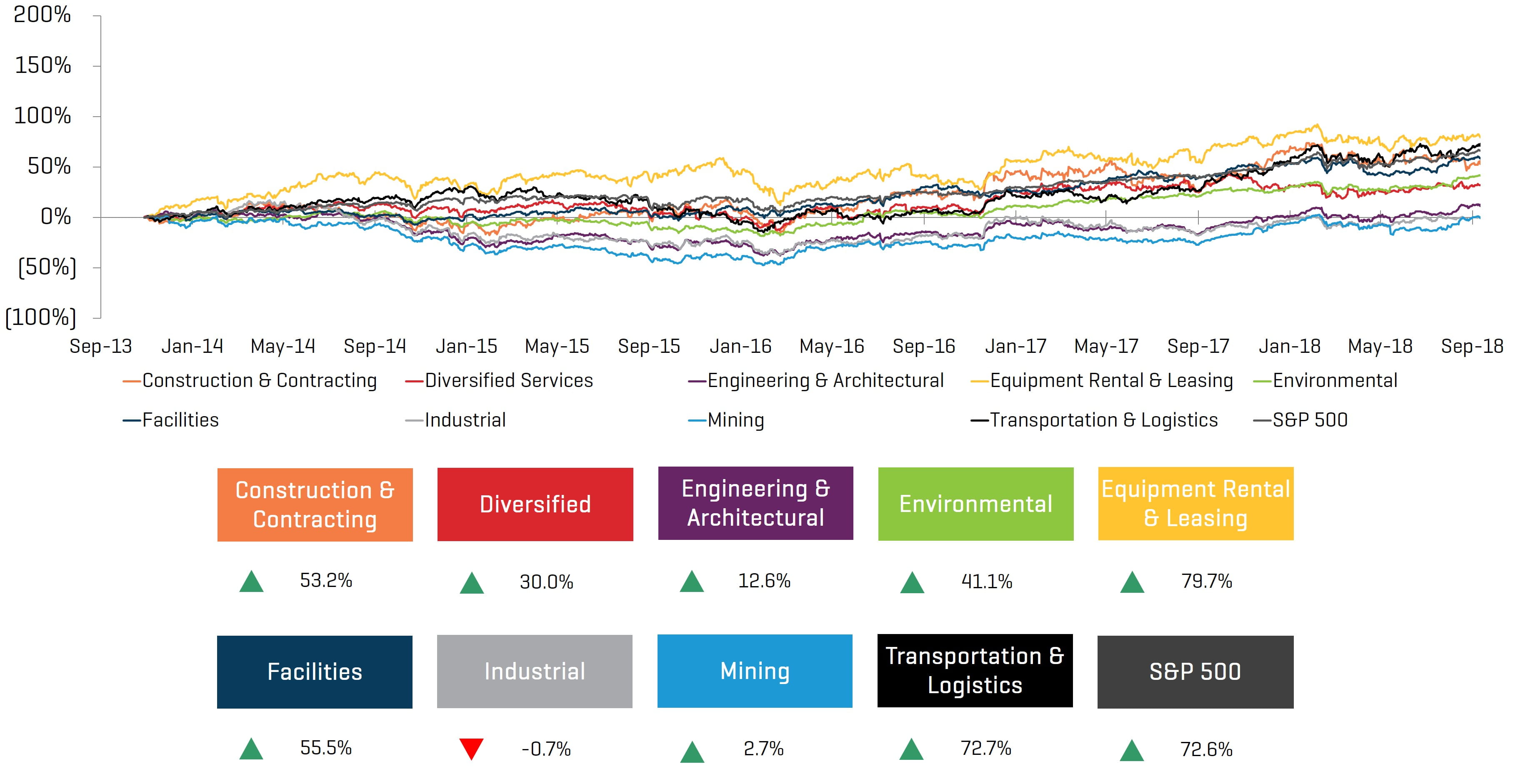

5-Year Historical Share Price Performance

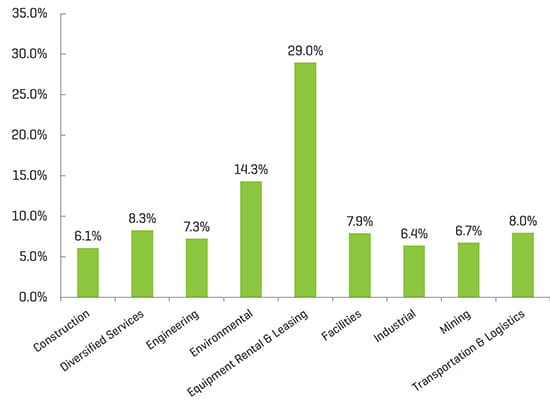

LTM EBITDA Margin

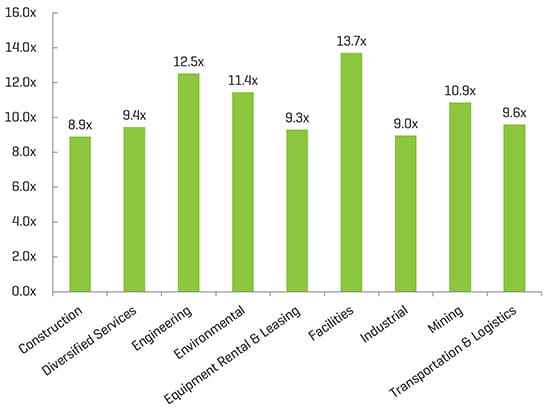

Enterprise Value / LTM EBITDA[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Note: Median from public comp sets featured in report

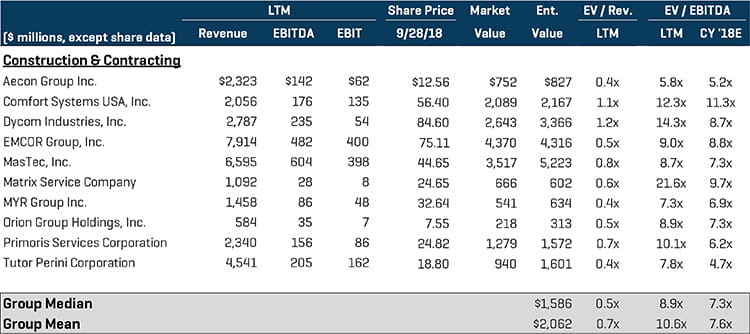

Construction & Contracting Services

Transaction activity in the construction and contracting services segment remained strong in the third quarter, driven by large corporations seeking geographical expansion and service offering diversification as the industry adapts to changes in technology and federal policy. Notable transactions include:

- Dunes Point Capital announced the acquisition of Foundation Building Materials’ (NYSE:FBM) Mechanical Insulation segment, a fabricator of commercial and industrial insulation products servicing through 67 locations across the United States and Canada, for $122.5 million

- MYR Group (NASDAQ:MYRG), an Illinois-based electrical contracting firm has announced its acquisition of The Huen Companies, a leading electrical construction firm with offices in Illinois, New Jersey and New York, for approximately $47.1 million

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

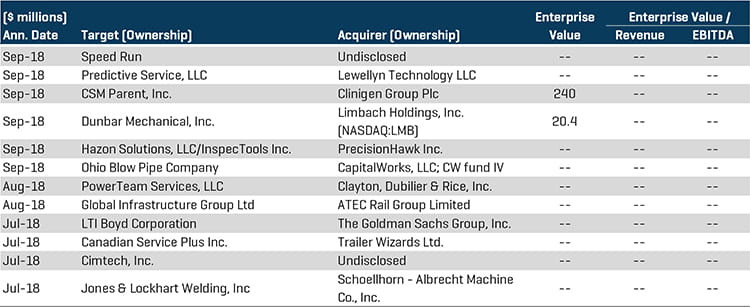

Select M&A Transactions

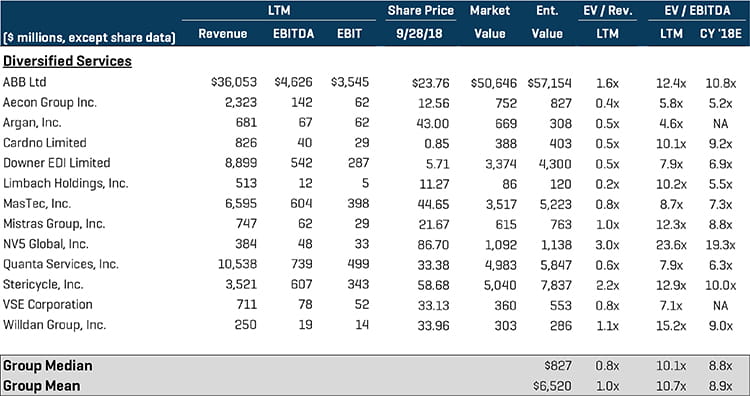

Diversified Services

The diversified services segment saw a mixture of large strategic acquisition activity as industry players pursue complimentary service offerings and capabilities, as well as private equity buyers diversifying industrials-oriented portfolios. Notable transactions include:

- Clayton, Dubilier & Rice, an American private equity firm, has announced that it will be acquiring PowerTeam Services, LLC, a North Carolina-based provider of maintenance, repair, upgrade and installation services for U.S. utility industries. PowerTeam serves a deep customer base of leading regulated utilities through its 42-location network with approximately 4,200 employees nationwide

- Limbach Holdings, Inc.’s (NASDAQ:LMB) acquisition of Ohio-based Dunbar Mechanical, Inc. for approximately $20.2 million will strengthen Limbach’s project management and contracting services. The two companies have direct side-by-side experience working in collaboration on one of the largest healthcare construction projects in the Toledo, OH, area

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

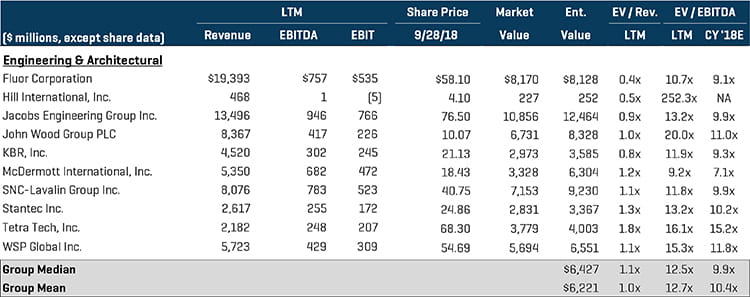

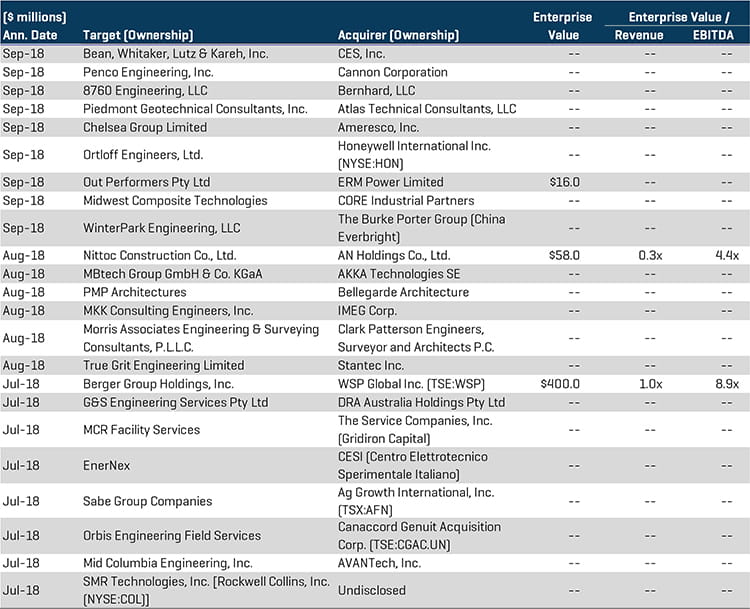

Engineering & Architectural Services

International strategic buyers headlined an active third quarter for the engineering and architectural services segment, as businesses anticipate that a continued uptick in construction and corporate investment in core business operations will fuel industry growth moving forward. Notable transactions include:

- CORE Industrial Partners, a private equity firm, announced its acquisition of Midwest Composite Technologies, Inc., a Wisconsin-based industrial components prototype engineer and manufacturer, for an undisclosed amount. CORE Industrial Partners notes its plans to build upon Midwest Composite Technologies’ automation capabilities to create a high-tech enabled engineering platform

- WSP Global, Inc. (TSE:WSP), a publicly listed Canadian global professional services entity, has agreed to acquire Berger Group Holdings, Inc., a privately held U.S.-based global construction engineering and professional services company, in a transaction valued at $400 million. The transaction will add 5,000 employees to WSP’s workforce, strengthening its U.S. footprint and expanding WSP’s international presence across Continental Europe, Latin America and the Middle East

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

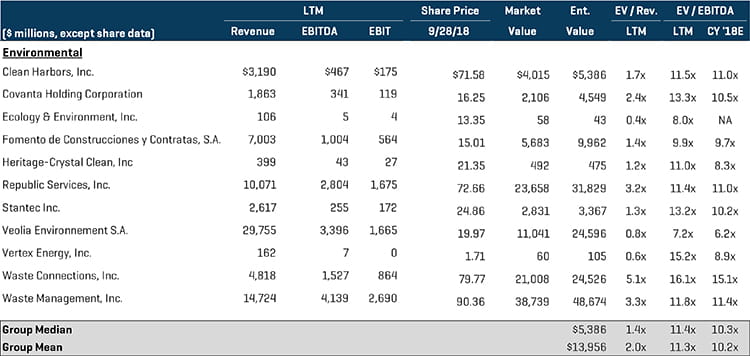

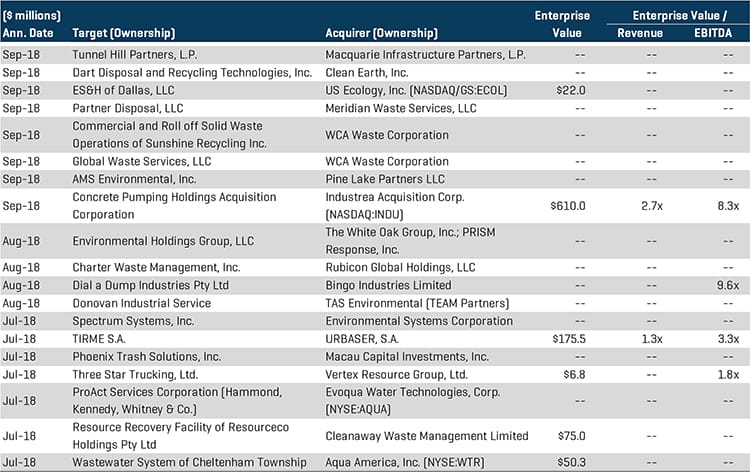

Environmental Services

The environmental services segment continued its robust M&A activity in the third quarter led by some of the largest strategic players, pointing towards a continuance of industry consolidation. The acquisitive nature of environmental services companies is indicative of broader industry growth, driven by changes in governmental regulation, technological advances and an increased emphasis on environmental sustainability initiatives. Notable transactions include:

- WCA Waste Corporation’s acquisition of Global Waste Services, LLC expands WCA’s sustainability initiatives, offering a strengthened range of recycling capabilities to its Houston, Texas area customers

- In a related transaction, WCA Waste Corporation acquired the commercial and roll-off solid waste operations of Sunshine Recycling, Inc., expanding the company’s national platform with the entrance into the state of Florida

- Macquarie Infrastructure Partners, a New York-based investment fund that operates within Macquarie Group, is in discussions to potentially acquire Tunnel Hill Partners, a New York-based non-hazardous solid waste handling company with operations across Northeastern U.S.

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

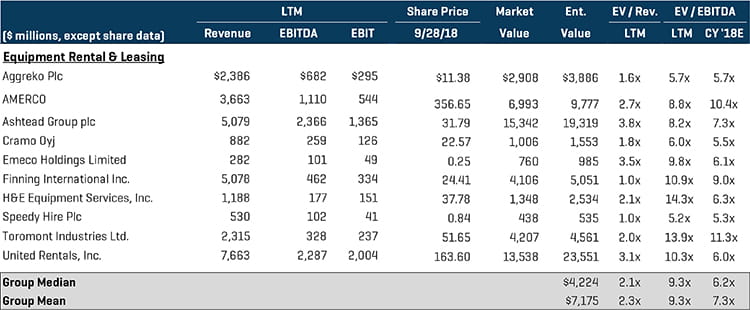

Equipment Rental & Leasing

The equipment rental and leasing segment experienced strong activity in the third quarter of 2018, led by a large public entity growing operations acquisitively and private equity firms conducting roll-up acquisition strategies through existing portfolio companies. Notable transactions include:

- United Rentals, Inc. (NYSE:URI) has agreed to acquire BlueLine Rental, a Texas-based equipment rental company, from Platinum Equity in a cash transaction worth $2.1 billion. BlueLine Rental is among the largest equipment rental companies in North America, serving over 50,000 construction and industrial customers across 114 locations with over 1,700 employees throughout the U.S. and Canada

- In a related transaction, United Rentals, Inc. announced it has entered into a definitive agreement to acquire BakerCorp International Holdings, Inc., a California-based containment, pumping, filtration and shoring equipment rental solutions company, in a deal valued at up to $715 million – the transaction strengthens United Rentals’ position in the market with the acquisition of key blue-chip customer relationships

- Tecum Equity Partners has made an investment in Tidewater Equipment Company, a Georgia-based dealer of forestry and related equipment, making the transaction the fourth platform investment for Tecum – Tidewater management notes that the investment makes for an ideal partnership, allowing for the company to pursue its next phase of growth

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

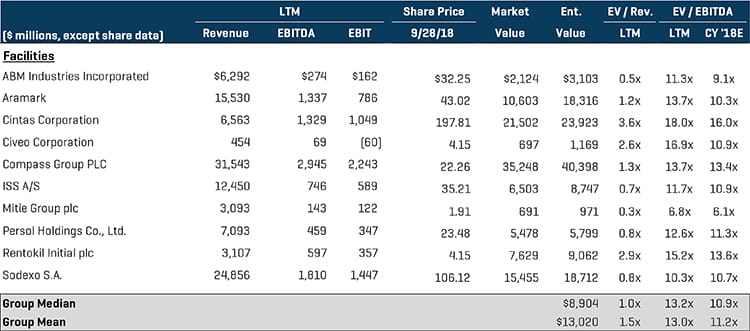

Facilities Services

The facilities services segment continues to see aggressive platform and add-on acquisition activity from financial sponsors, as well as ongoing consolidation from domestic and international strategic acquirers as positive dynamics in commercial construction generates growing demand for facility support services. Notable transaction details include:

- Gridiron Capital, a private equity firm, has acquired The Service Companies, Inc., a Florida-based diversified provider of managed services, staffing and specialty facility cleaning. Gridiron has since focused on expanding the company through an acquisitive growth approach via the add-on acquisition of MCR Facility Services, a leading provider of integrated facility solutions – following the acquisition of MCR, The Service Companies launched a new business unit, TSC Engineering, which will provide engineering services to the commercial facilities industry

- Lenmac Mechanical Services Ltd., an Ireland-based facilities and equipment servicing company, has been acquired by Designer Group, a global leader in facilities management solutions headquartered in Ireland, for an undisclosed amount. The acquisition will add to Designer Group’s more than 750 employees and expands its facilities management capabilities with the expertise and project-oriented experience of Lenmac

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

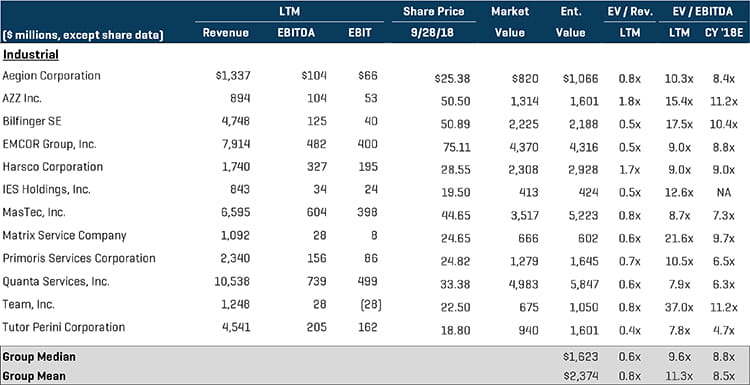

Industrial Services

Industrial services M&A activity continues to be very active from both strategic and financial buyers. Strategic buyers in this segment look to expand service offering and geographic coverage to serve as a “one-stop shop” for customers and private equity firms seek industrials portfolio diversification. Notable transactions include:

- Valmont Industries (NYSE:VMI), a manufacturer of industrial and irrigation products with a $3.1 billion market cap, agreed to acquire the assets of CSP Coatings Systems, a New Zealand-based steel coating service provider, for an undisclosed amount – Valmont Industries executives note that the transaction advances the company’s geographic expansion strategy by building upon its existing presence in New Zealand

- PumpMan Holdings, a New Jersey-based pump service and repair provider backed by Soundcore Capital Partners, acquired Southwest Waterworks Contractors, Inc. – the transaction grants PumpMan entry to the fast-growing Phoenix market

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

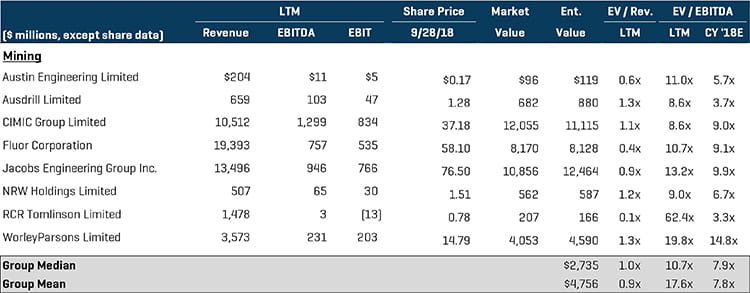

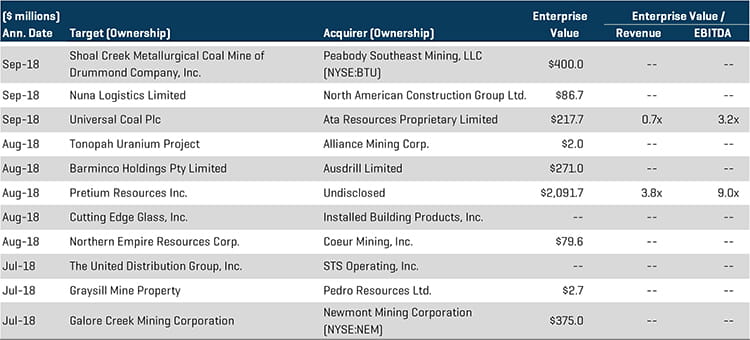

Mining Services

The mining services industry remains a competitive market where companies are fiercely competing to gain access to attractive geographical regions. Large mining industry players continue to utilize acquisitive strategies in place of greenfield exploration efforts to gain control of profitable mining projects. Notable transactions include:

- Peabody Southeast Mining, LLC, a subsidiary of Peabody Energy Corporation (NYSE:BTU) has entered into a definitive agreement to acquire the Shoal Creek metallurgical coal mine from Drummond Company, Inc, a private coal producer, in a deal valued at $400 million – Peabody management notes the transaction’s opportunity for significant value creation through enhanced logistical capabilities, expanded volumes and alignment of complimentary products for customers

- Newmont Mining Corporation (NYSE:NEM), a leading gold and copper producer with operations globally, has acquired a fifty percent interest in Galore Creek Mining Corporation, a diversified metal mining and exploration services company. Newmont will form a strategic partnership with Teck Resources Limited (TSX:TECK.B), a global natural resources producer that controls the remaining ownership interest in the company

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

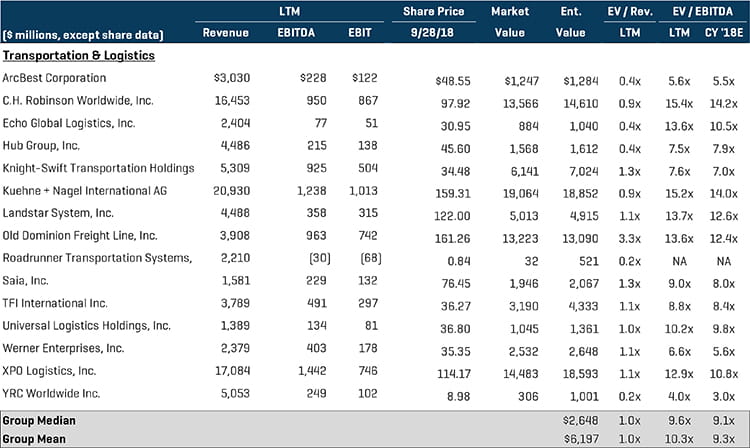

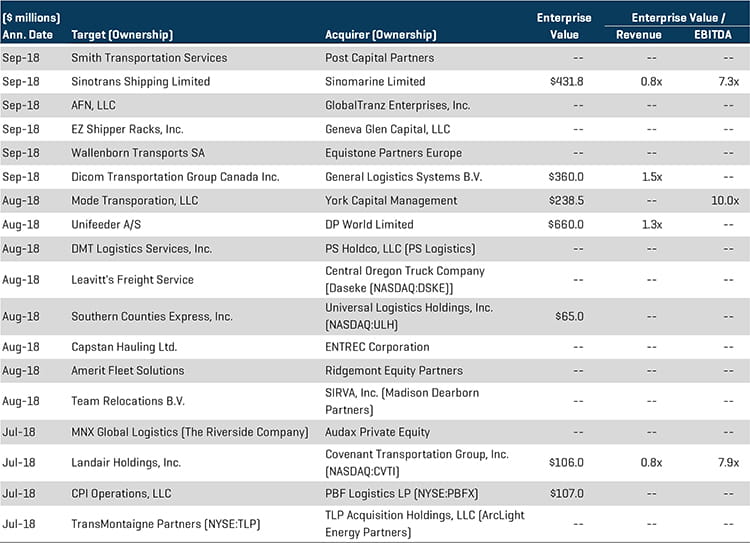

Transportation & Logistics

Transportation and logistics M&A activity in third quarter 2018 was driven by private equity firms pursuing attractive opportunities with cutting-edge logistics providers and large public strategic buyers aiming to expand service offerings through industry consolidation. Internet of Things (IoT) continues to be a driving force behind the segment’s activity as buyers pursue technology-enabled logistics platforms to outpace competition. Notable transactions include:

- York Capital Management, a New York City-based investment management firm, has entered into an agreement to acquire Mode Transportation, LLC, a Texas-based third-party logistics company previously owned by Hub Group, Inc. (NASDAQ:HUBG), in a transaction valued at $238.5 million

- Audax Private Equity acquired California-based, global provider of customized transportation and logistics services for high-value goods, MNX Global Logistics, from The Riverside Company for an undisclosed amount. MNX serves global leaders across diversified industries in over 190 countries with its preeminent logistics capabilities

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

All Sources for charts: S&P Capital IQ and Stout Research