English

English

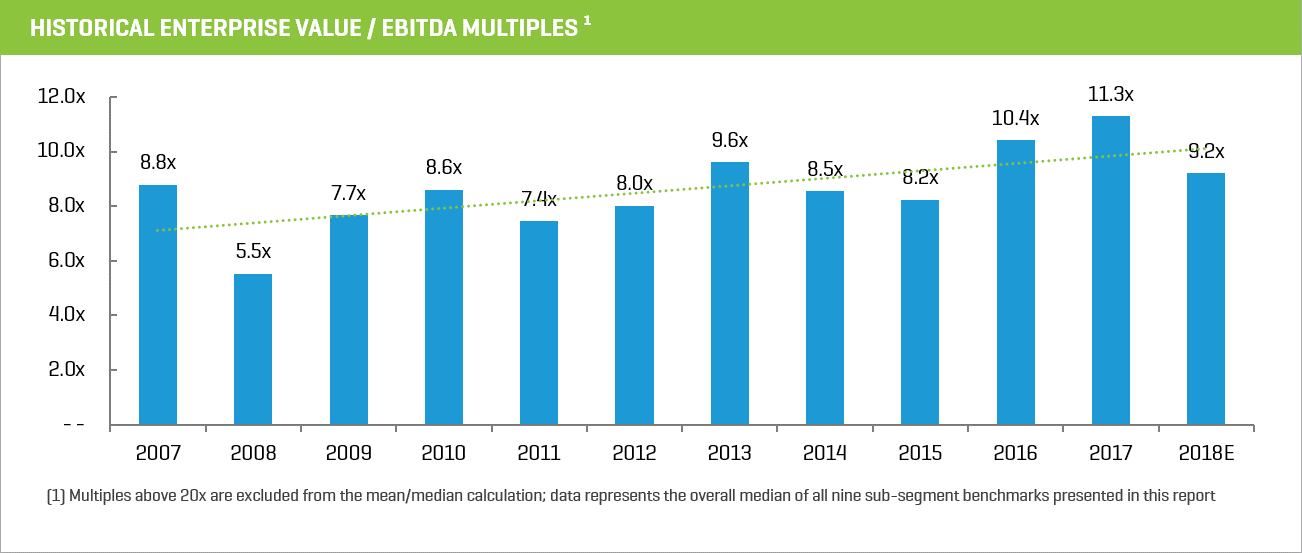

Historical EV / EBITDA multiples were at their highest level during 2017 at a median of 11.3x¹, primarily driven by resilient public equity markets, robust M&A activity, and abundant capital creating a competitive market. Strategic buyers dominated deal volume as they look to broaden service offering capabilities, grow market share, and expand geographical reach. Strategic buyers also look to increase earnings via scale and synergies, as they are pressured to create shareholder value in a mature and competitive industry. Private equity activity remained at historical levels and showed interest in select segments with the strongest compounded growth, such as Construction & Contracting and Diversified Industrials. As the economy continues to strengthen, construction and infrastructure spending initiatives will fuel organic growth and ignite further strategic M&A activity.

2017 Key Takeaways

- Continued strong overall industrial services M&A activity

- Two mega-mergers (Knight & Swift Transportation and McDermott & CBI) which have transformed their respective segments and resulted in vertically integrated leaders

- Valuation multiples reaching all-time highs

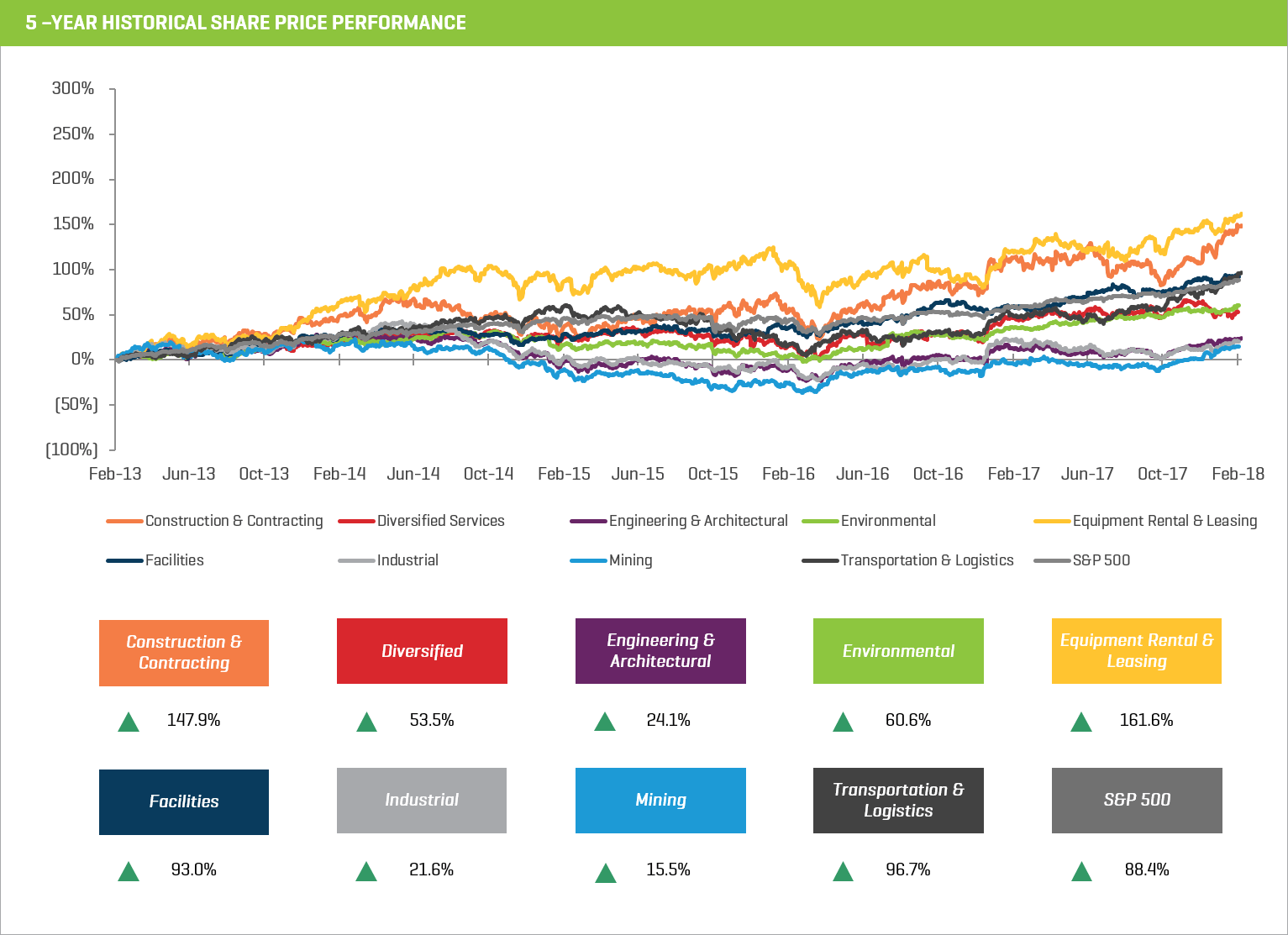

- Public equity performance positive, with four segments out-pacing the S&P 500

- Cross-border M&A activity surged

- Continued low cost of capital and high capital availability

- Key macroeconomic indicators seeing coordinated strength

Industry Statistics

Operating and Market Performance

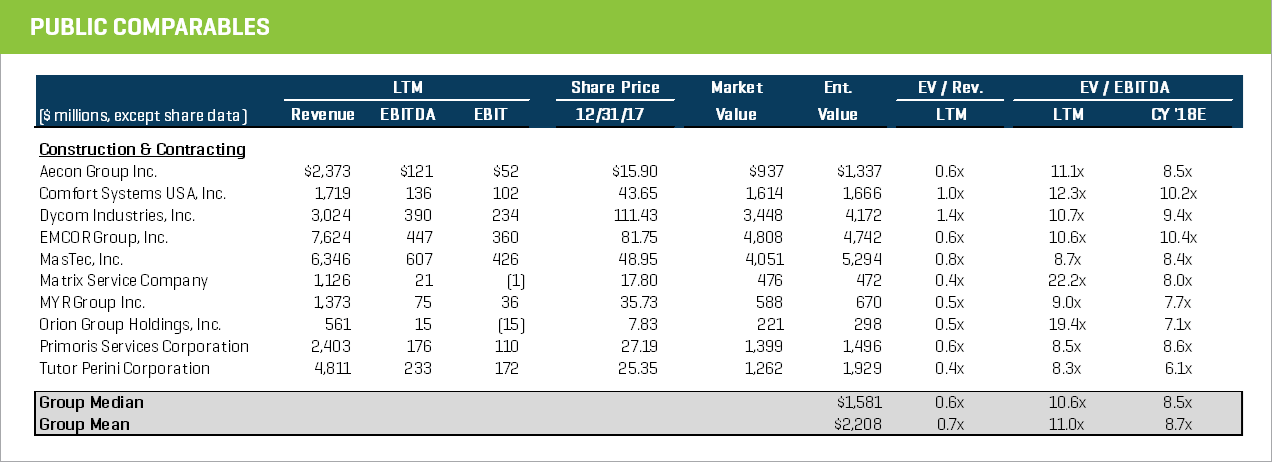

Construction & Contracting Services

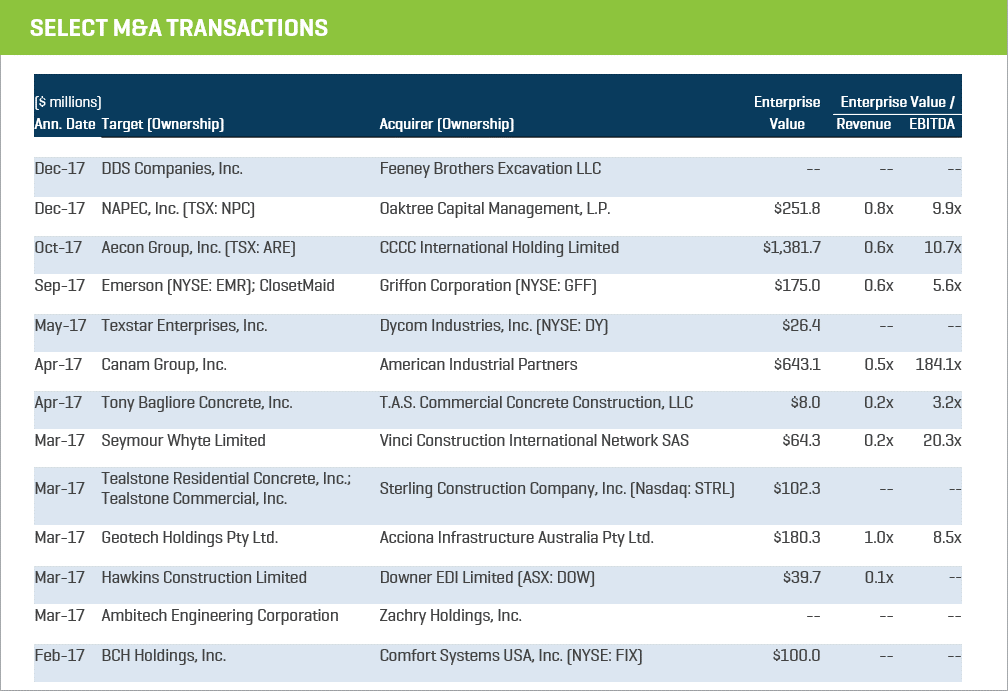

The construction segment saw a handful of cross-border, high-premium transactions with notable interest from both private equity and strategic buyers, including:

- American Industrial Partner’s acquisition of Canadian-based Canam Group, in a going private transaction representing a premium of 98.4%

- Oaktree Capital Management’s agreement to acquire Canadian-based NAPEC, representing a 35.4% premium

- CCCI’s agreement to acquire Canadian-based Aecon Group, representing a 42% premium

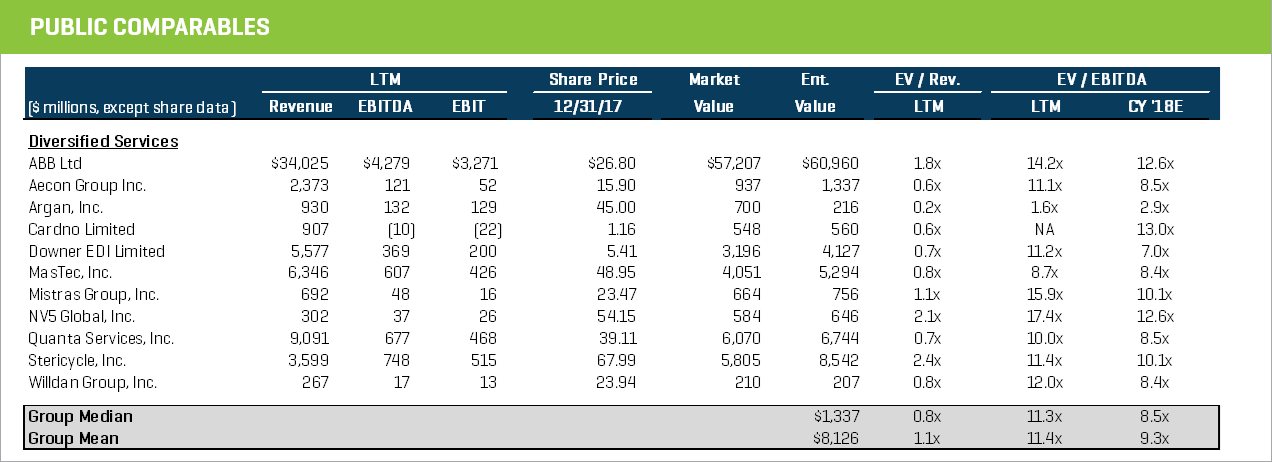

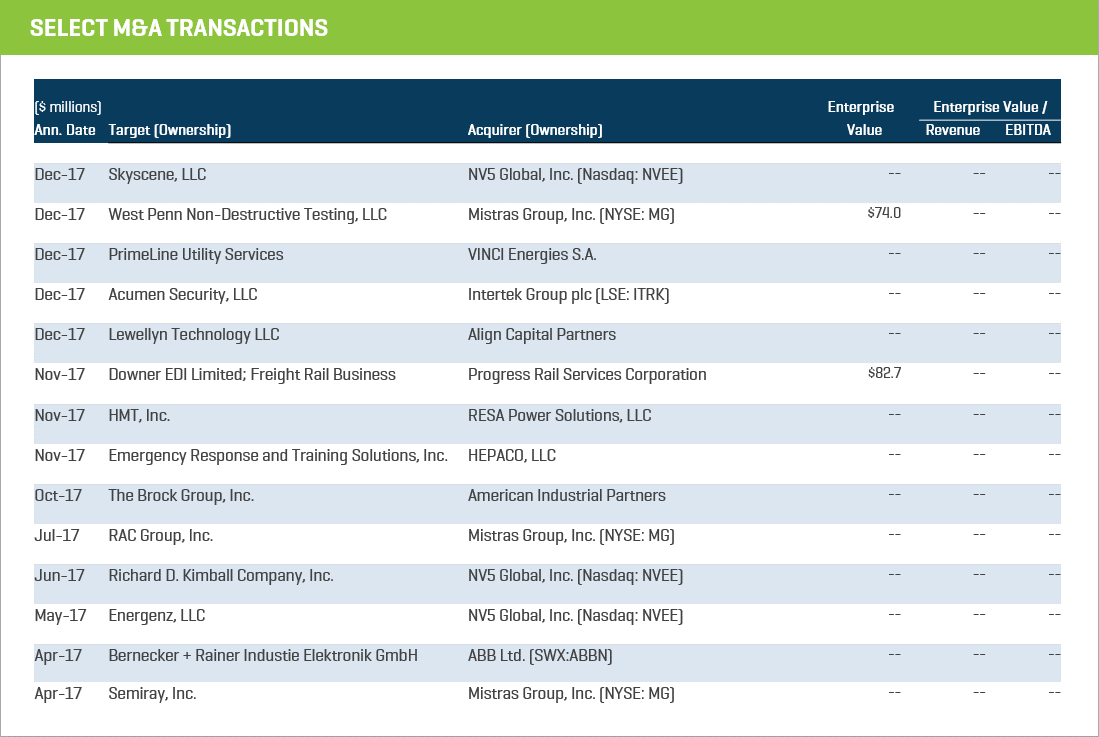

Diversified Services

Industrial conglomerates such as NV5 Global, VINCI, and ABB dominated M&A activity within the diversified industrials segment as they continue to consolidate the smaller players in the marketplace. The most notable transactions include:

- VINCI’s announced acquisition of U.S.-based PrimeLine Utility Services, representing its 30th external growth transaction in 2017

- American Industrial Partner’s acquisition of U.S.-based Brock Group, which significantly deleveraged the balance sheet and increased capital resources, allowing AIP to build upon Brock’s portfolio

- ABB’s acquisition of Austria-based Bernecker + Rainer, which valued the deal at almost $2 billion, according to a person familiar with the matter

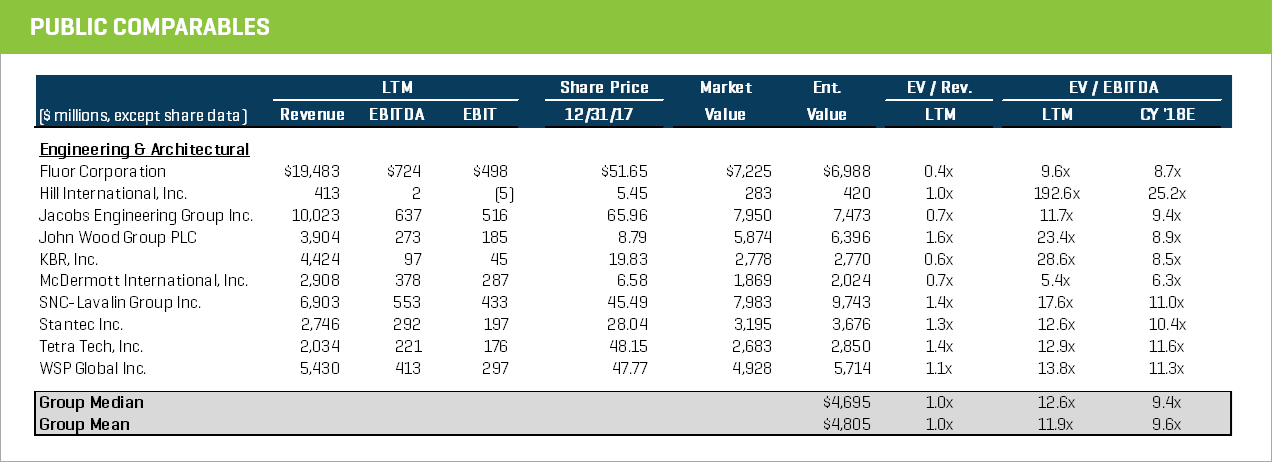

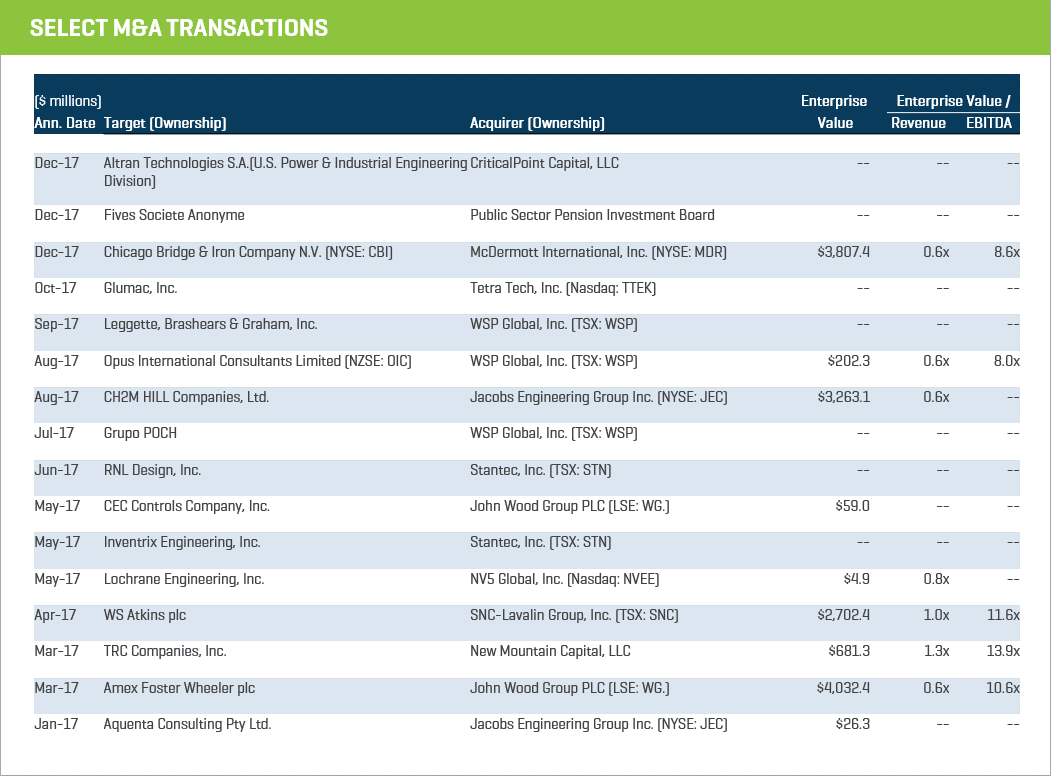

Engineering & Architectural Services

The engineering and architectural services segment contained the largest deals by size and traded second highest by group, in terms of EBITDA multiples. Acquisitions were primarily sought after due to realizable synergies which are expected to become accretive to earnings. The four largest deals include:

- John Wood Group’s acquisition of UK-based Amec Foster Wheeler, in an all-stock deal valuing the enterprise at approximately $4 billion

- McDermott and Chicago Bridge & Iron’s announced all-stock merger, which puts CBI’s enterprise value at approximately $3.8 billion and creates combined revenues of approximately $10 billion

- Jacobs Engineering Group’s acquisition of U.S.-based CH2M Hill Companies, in a cash and stock deal that values CH2M at approximately $3.2 billion

- SNC-Lavin Group’s acquisition of UK-based WS Atkins, in an all-cash deal that values Atkins at approximately $2.7 billion

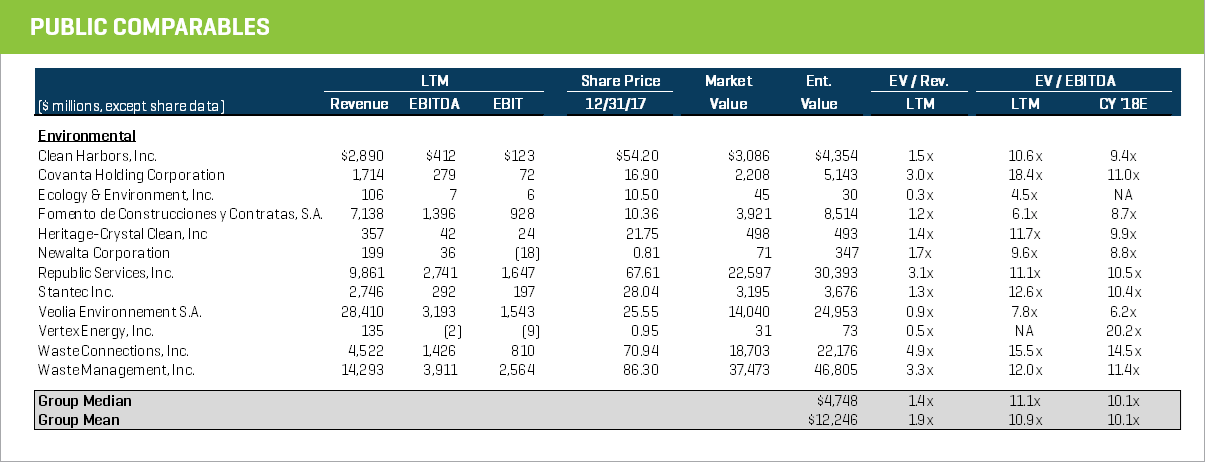

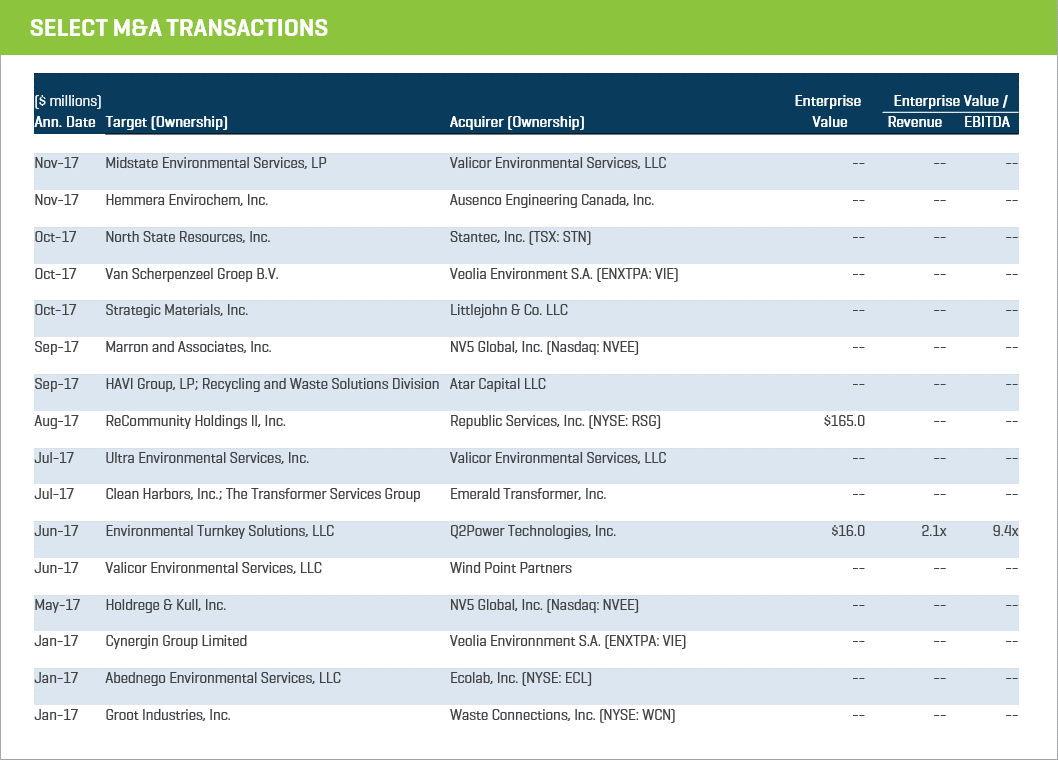

Environmental Services

The environmental services segment continues to expand as environmental standards and concerns push for stronger green initiatives. As a result, M&A activity is increasing and has had a primary focus towards broadening geographical and service offering capabilities. The most notable transactions include:

- Littlejohn & Co’s agreement to acquire U.S.-based Strategic Materials, as it looks to leverage its existing expertise in the broader industrials industry and capitalize on Strategic Materials’ 47 facilities that spread across North America

- Republic Services acquisition of U.S.-based ReCommunity Holdings II, which includes 26 recycling centers and will result in approximately 1.6 million tons of recycled commodities annually with combined operations

- Stantec’s acquisition of U.S.-based North State Resources, which significantly bolsters growth in its environmental service capabilities, particularly in regards to NEPA and CEQA compliance programs

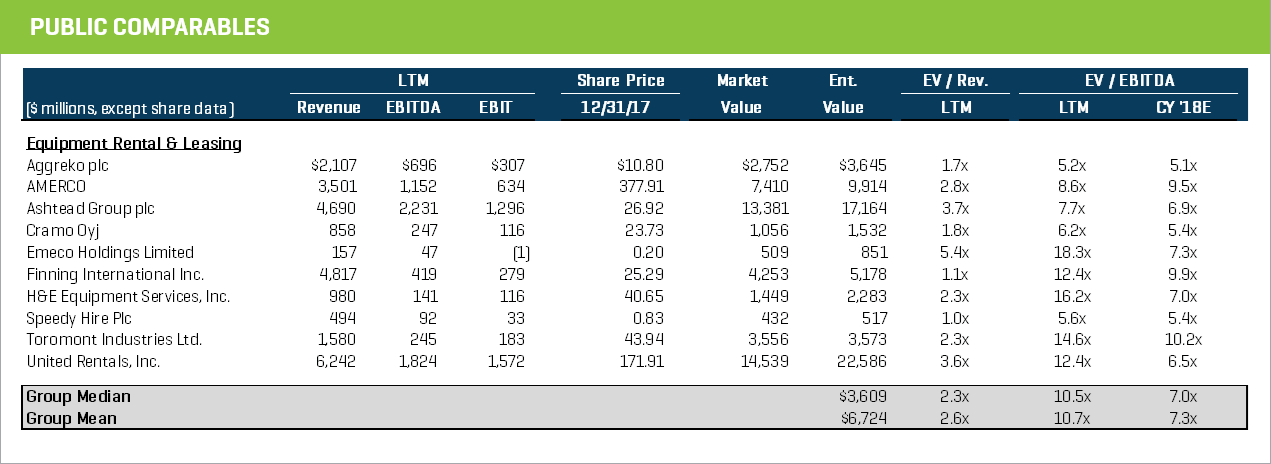

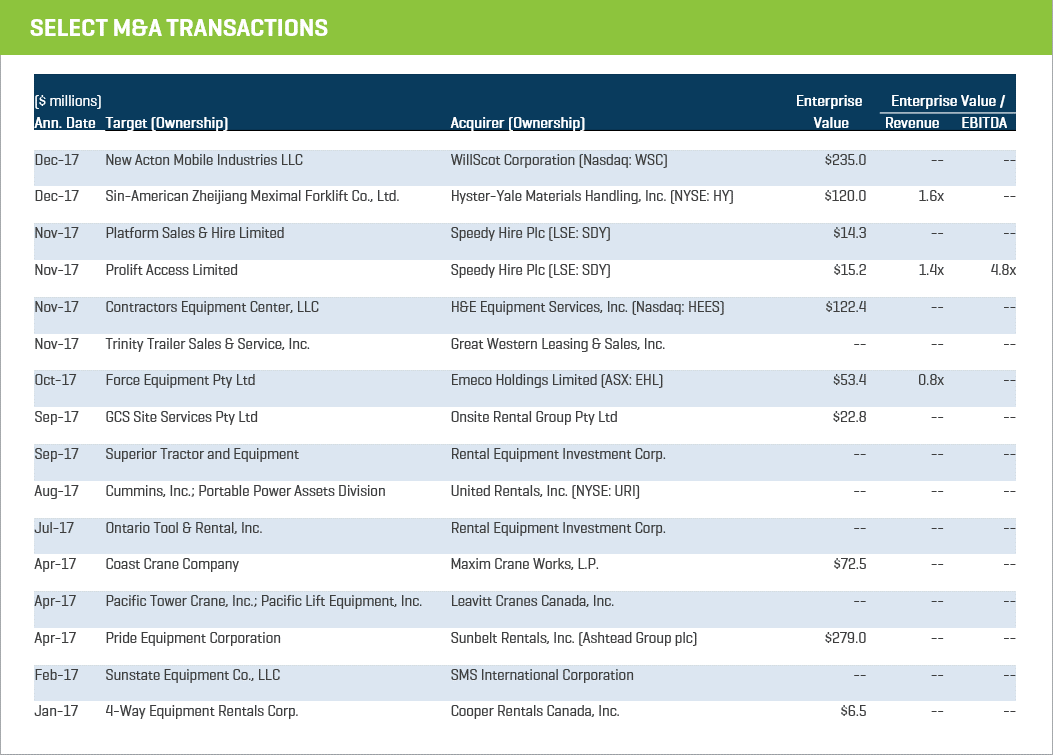

Equipment Rental & Leasing

The equipment rental and leasing segment saw a handful of strategic transactions that are meant to increase market share position and ensure they are staying competitive. The most notable

transactions include:

- H&E Equipment’s acquisition of U.S.-based Contractors Equipment Center, which will augment H&E’s capabilities and efficiencies of scale in the market areas and geographies CEC

currently serves - WillScot’s acquisition of U.S.-based New Action Mobile Industries, giving WillScot nearly 100,000 modular space and portable storage units serving approximately 35,000 customers from over 100 locations across North America

- Sunbelt Rentals’ acquisition of U.S.-based Pride Equipment Corporation, giving Sunbelt exposure to aerial equipment and brings significant cross-sell opportunities to an enlarged customer base

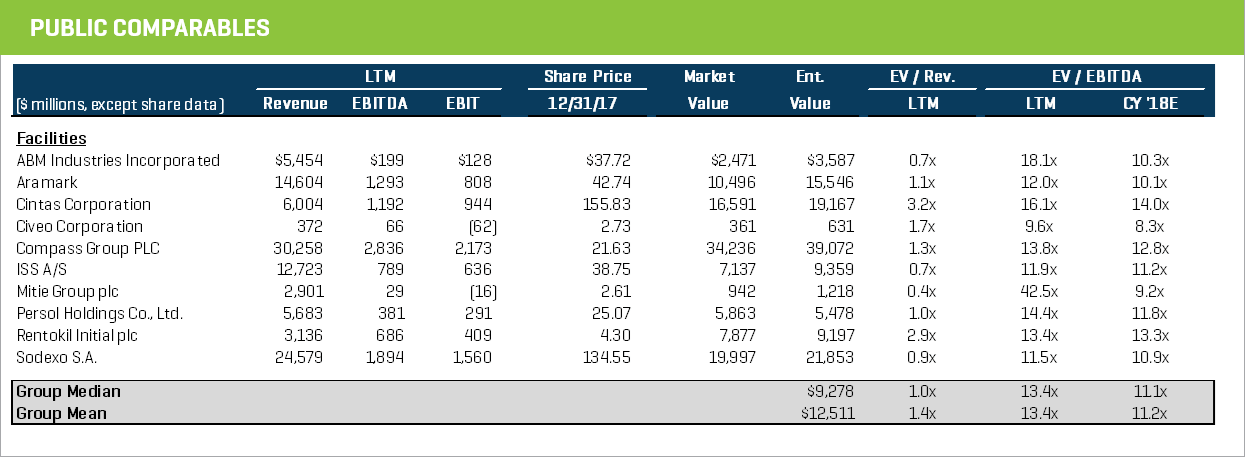

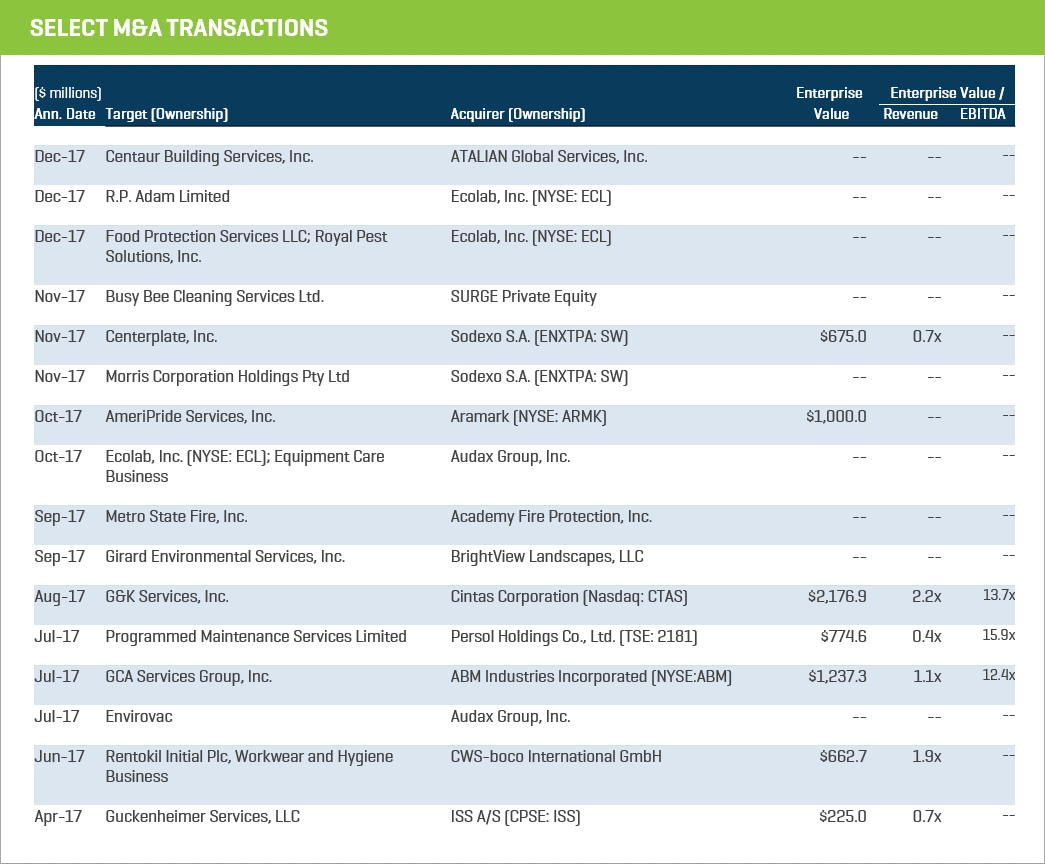

Facilities Services

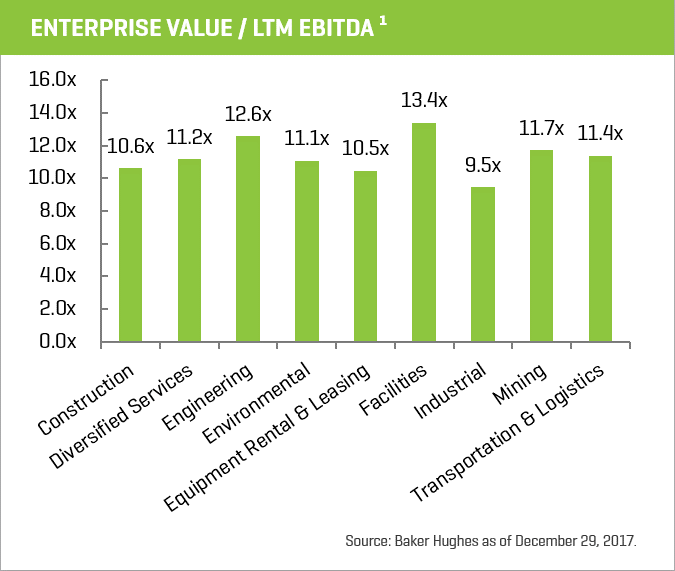

The facilities services segment traded at the highest EBITDA multiples out of all nine groups, in part, due to significant cost synergies anticipated to be realized post transaction by acquirers. Three notable transactions include:

- Aramark’s agreement to acquire U.S.-based AmeriPride, creating anticipated annual cost synergies of approximately $70 million

- Cintas’ acquisition of U.S.-based G&K Services, creating anticipated annual synergies between $130 and $140 million

- ABM’s acquisition of U.S.-based GCA Services, which is expected to produce cost synergies of approximately $20 to $30 million by the second full year of ownership

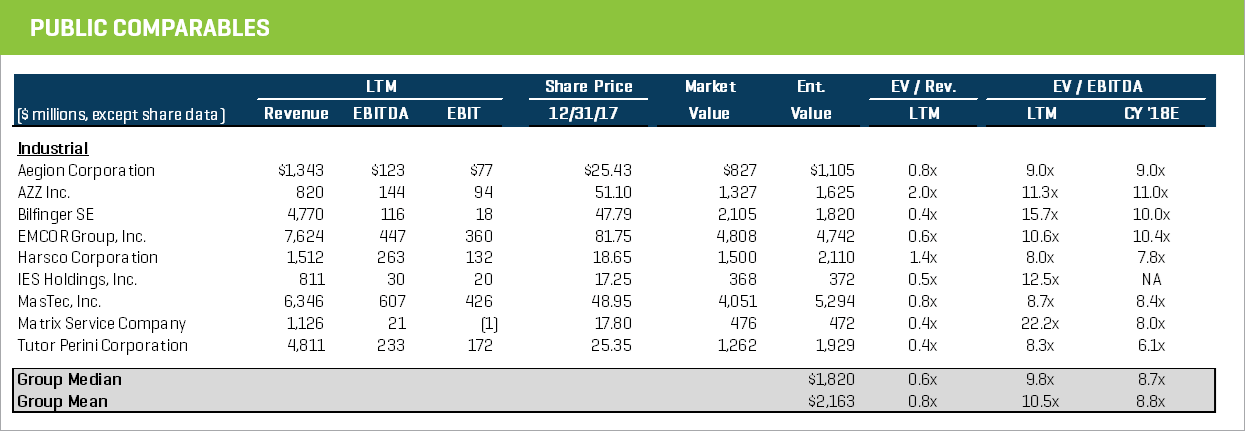

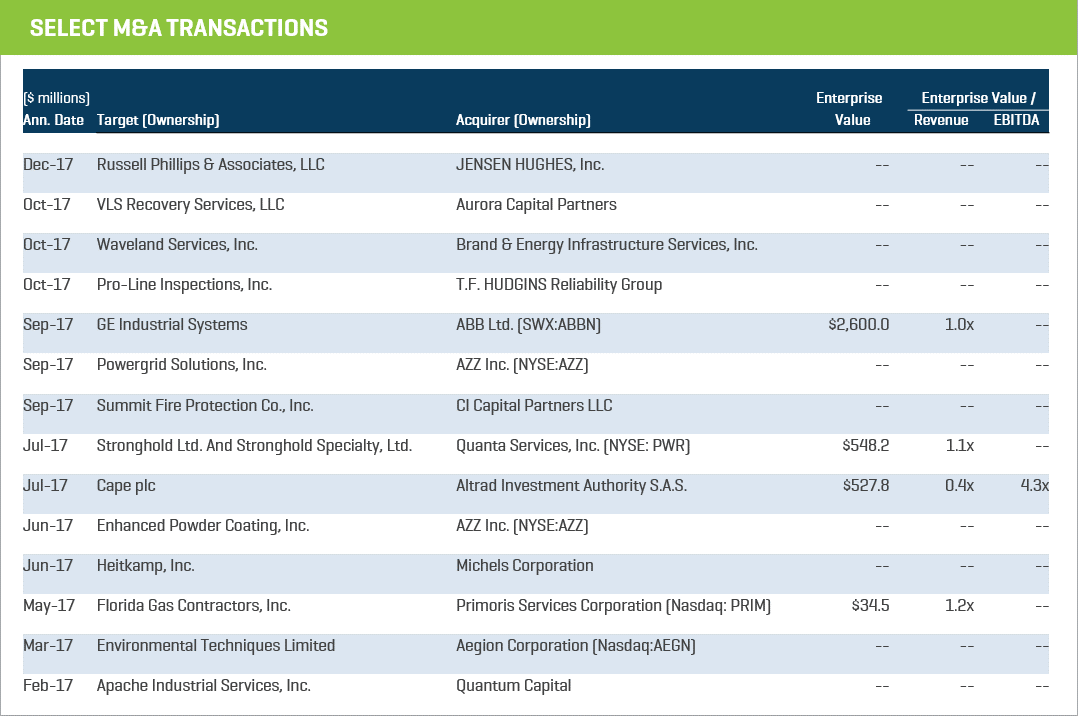

Industrial Services

Industrial services M&A activity was driven by large conglomerates and private equity interest. Strategic buyer activity was motivated by anticipated long-term benefits for both the target and the acquirer, due to complementary product mix and integration. Three notable transactions include:

- Altrad’s agreement to acquire UK-based Cape plc, creating both near and longer-term benefits for the combined entity, as geographical location and product mix is complemented

within the energy and natural resource sectors - ABB’s agreement to acquire U.S.-based GE Industrial Solutions, establishing a long-term strategic supply relationship for GE products and ABB products that GE currently sources

- Quanta Services’ acquisition of U.S.-based Stronghold, Ltd and Stronghold Specialty, Ltd., giving Quanta additional exposure to the Gulf Coast refinery and petrochemical market

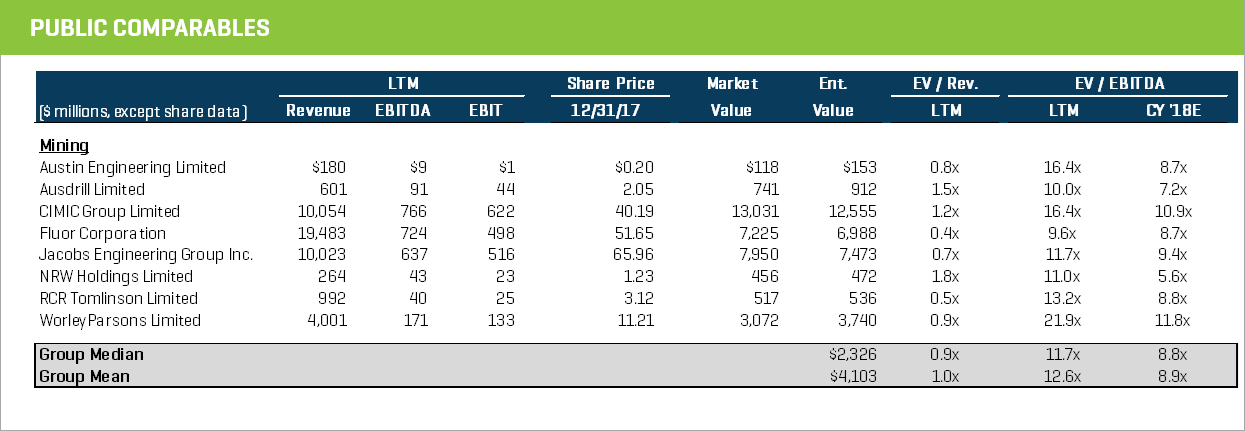

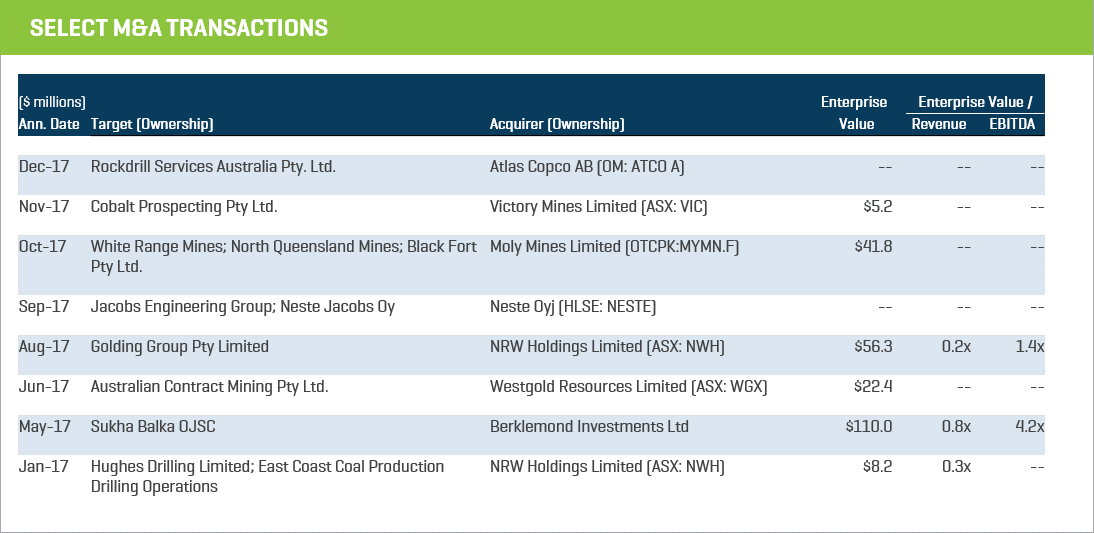

Mining Services

The mining services segment saw the most activity in Australia, and had two notable transactions from NRW Holdings, which is looking to expand its presence and service offerings into adjacent and complementary sectors. The two NRW transactions include:

- NRW’s acquisition of Australian-based Golding Group Pty Ltd, which expands its workforce to approximately 2,000 employees supporting more than 40 projects throughout Australia

- NRW’s acquisition of the east coast coal production and drilling operations of Hughes Drilling Limited, which is expected to add annual revenue of approximately $40 million AUD

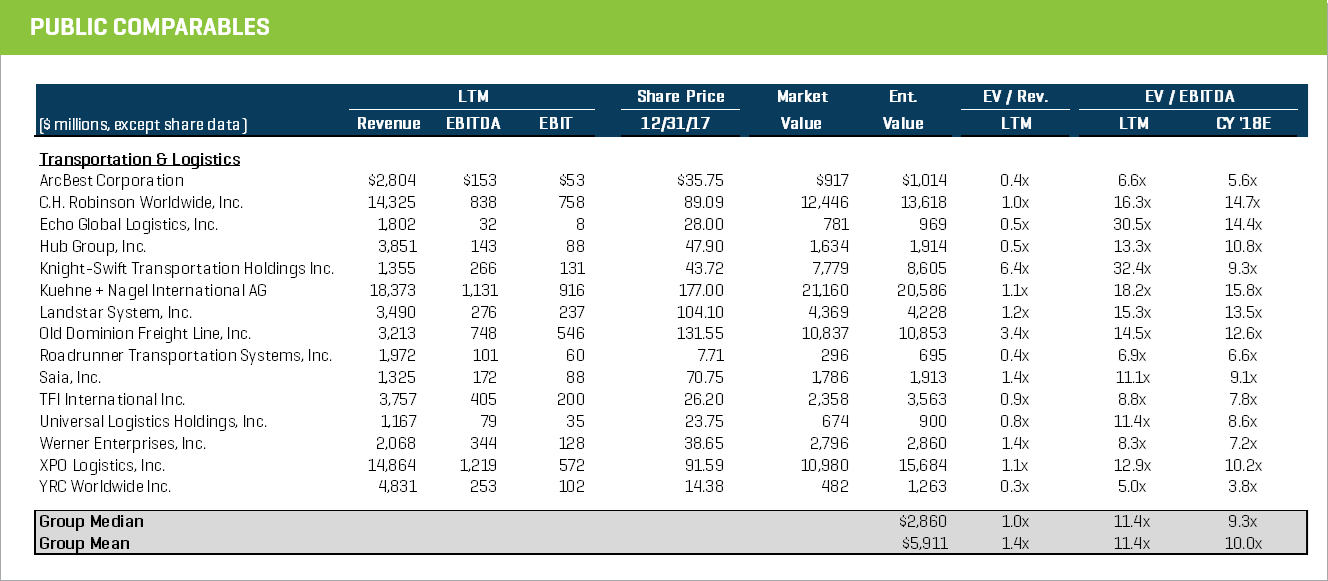

Transportation & Logistics

The transportation and logistics segment is experiencing a rapid change in how it operates and adapts to shorter delivery-time demands and higher e-commerce delivery volume. These changes

have resulted in a handful of transformative acquisitions which have already begun disrupting the industry. Three notable transactions include:

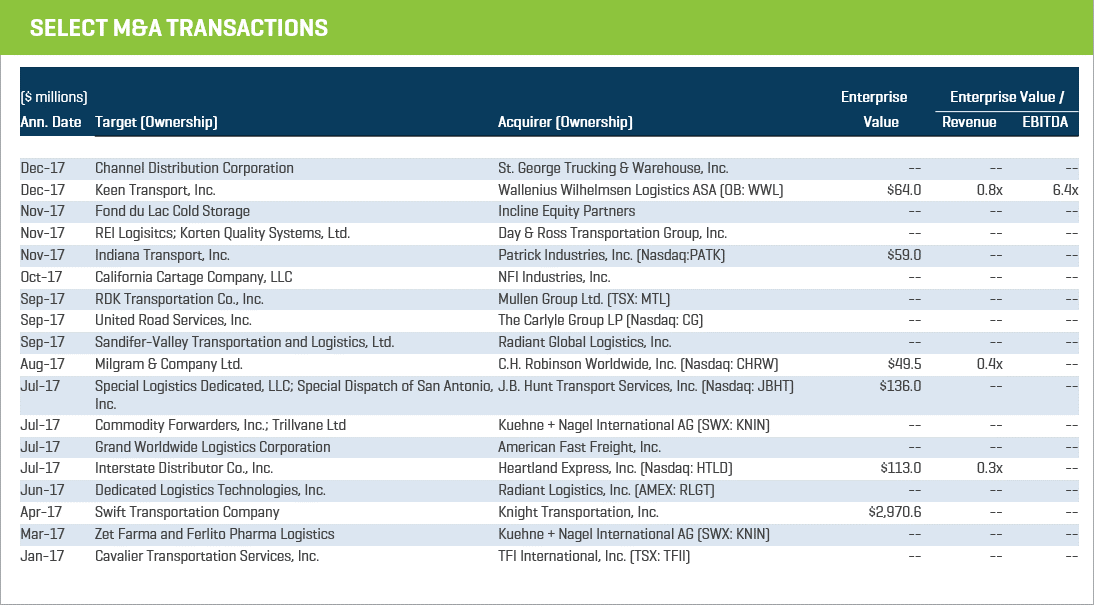

- The approximately $3 billion dollar merger of Knight Transportation and Swift Transportation, which allows the combined entity to act as a “one-stop” shop for truckload transportation and logistics services throughout North America

- J.B. Hunt Transport Services’ agreement to acquire U.S.-based Special Logistics Dedicated, which is expected to improve order fulfilment times and enhance J.B. Hunt’s e-commerce delivery capabilities

- Wallenius Wilhelmsen Logistics’ acquisition of U.S.-based Keen Transport, Inc., which provides value-added services to roughly 20 OEMs, and is expected to capitalize on improving fundamentals in mining and construction within the US

(1) Multiples above 20x are excluded from the mean/median calculation