English

English

The engineering and construction (E&C) sector saw strong M&A activity in 2019, with both strategic and financial buyers continuing to be active. Activity was similar to that seen in 2018, both of which were below 2017, which was a record year for the sector. The total dollar value of transactions was down in 2019 compared with the prior two years.

Drivers for the continued activity include strategic buyers seeking diversification, financial buyers continuing to see value in the industry as compared to others, and the prevalence of both debt and equity available for transactions. Trading multiples for larger, more stable companies (such as engineering, CM/PM, inspection and maintenance) continued to be at or above historical ranges.

Of note in 2019 was the pressure seen on several larger industry players to shed under performing or non-core segments, some of which were very large trades, and focusing on higher margin, more stable project types. Technology, resiliency and regulatory-driven trends continued to impact the sector. A common theme seen across company types included labor pressures across all three levels: executive, project management, and field employees. We expect this trend to continue in 2020 and beyond.

As we enter the new year, market activity seems to be building and the first half of the year is expected to be strong. The latter half of 2020 could see impacts from the election, but overall M&A activity for the year should be similar to 2019 as the underlying fundamentals driving trades are expected to remain intact.

Key Takeaways

- Continued strong overall E&C M&A activity, with strategic and financial buyers seeking opportunities for growth and diversification

- Increased emphasis on resiliency, infrastructure improvement and technology adaptation in the industry

- Public equity starting the year at high levels with forward outlooks positive

Industry Statistics

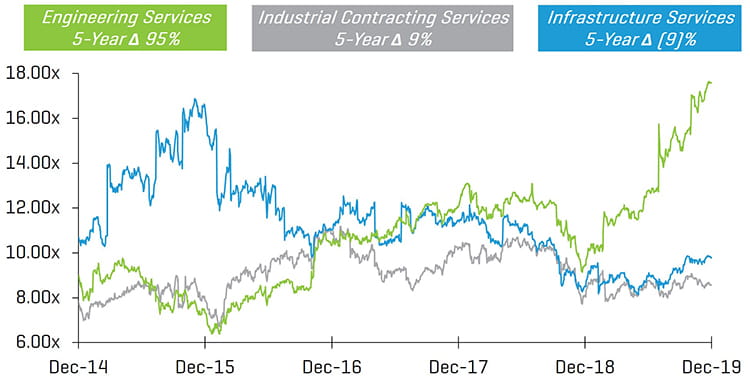

5-Year Historical Enterprise Value / LTM EBITDA Multiples

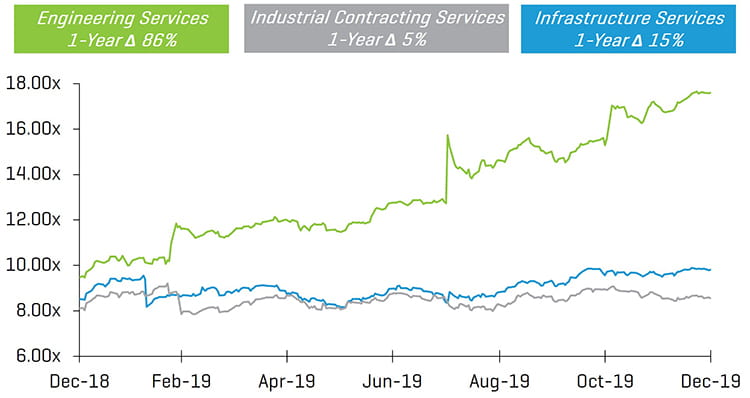

1-Year Historical Enterprise Value / LTM EBITDA Multiples

Public E&C Company Year-Over-Year Changes

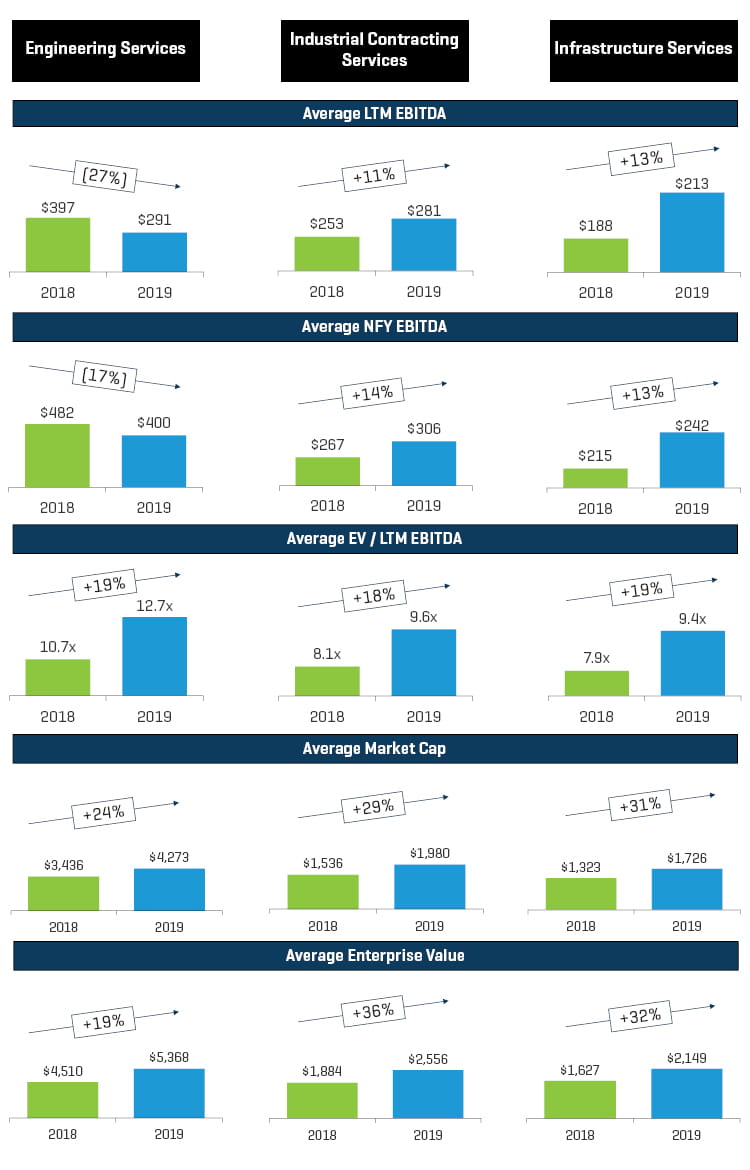

Several engineering firms faced project write-downs in 2019, impacting LTM and NFY EBITDA. The Industrial and Infrastructure services segments performed well and enter 2020 on a positive note. Interestingly, all three segments posted strong share price and enterprise value performance, despite project issues for several of the integrated engineering firms.

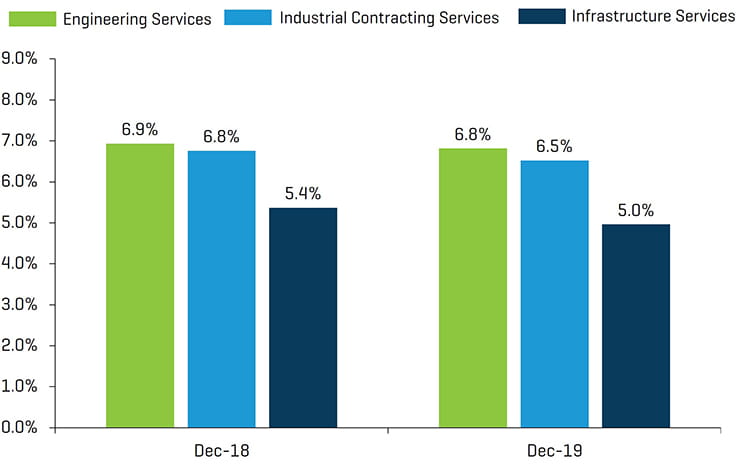

LTM EBITDA Margin

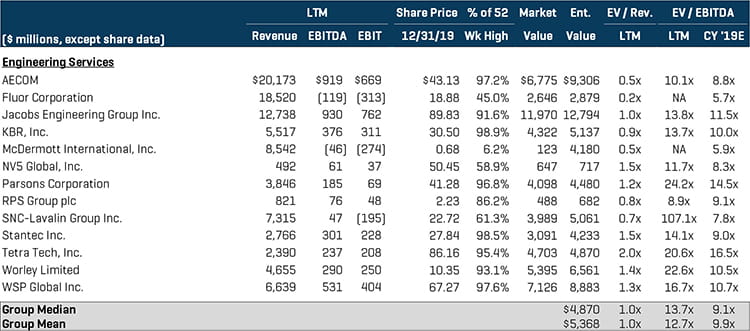

Engineering Services

This segment saw very strong public firm share price performance as well as continued strong M&A activity. Significant transactions include:

- NV5 (NYSE: NVEE) announced that it has acquired Quantum Spatial Inc., a leading provider of spatial analytics intelligence and enablement solutions including spatial data generation, integration, enablement, and analytics

- The Pritzker Organization acquired STV Group, Inc., a market leader in architectural, engineering, planning, environmental and construction management services

- American Securities LLC and Lindsay Goldberg acquired the Management Services of AECOM (NYSE: ACM). The business is a leading contractor to the U.S. federal government as well as other foreign governments

- Kohlberg & Company acquired EN Engineering, a leading provider of integrity management services

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions - Engineering Services

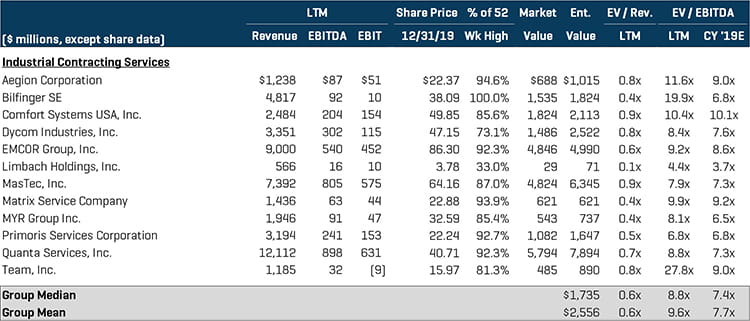

Industrial Contracting and Infrastructure Services

The Industrial Contracting and Infrastructure Services segments saw very strong M&A activity in 2019. Private equity buyers were attracted by firms with consistent, recurring revenues and strong specialty capabilities. Strategic buyers were active in acquiring infrastructure services firms in particular in order to diversify geographically and by end market type. Significant transactions include:

- Ventia Pty. Ltd. acquired the Australia and New Zealand operations of Ferrovial Services. The business provides infrastructure maintenance services to public and private entities.

- Harvest Partners acquired Yellowstone Landscape from CIVC. The company provides landscape management services to primarily commercial clients.

- J2 Acquisition Limited (a special purpose acquisition corp. or “SPAC”) acquired APi Group. APi is a conglomerate of over 30 companies in the industrial services, fire protection and steel fabrication sectors, among others.

- Sterling Construction Company, Inc. (NASDAQ: STRL) acquired Plateau Excavation, a southeast U.S.-based provider of large-scale infrastructure improvement services.

Industrial Contracting Services Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

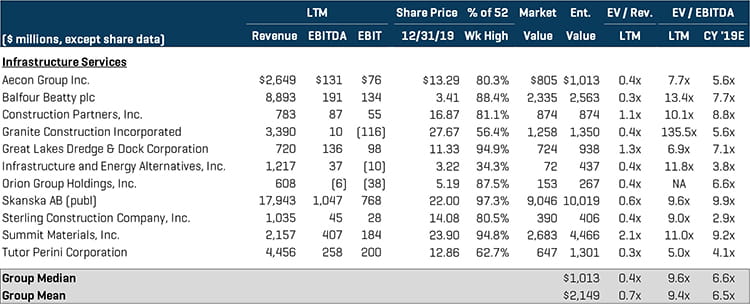

Infrastructure Services Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions - Industrial Contracting and Infrastructure Services

Industry Indexes for this report:

Engineering Services: ACM, FLR, J, KBR, MDRI.Q, NVEE, PSN, RPS, SNC, STN, TTEK, WOR, and WSP

Industrial Services: AEGN, GBF, FIX, DY, EME, LMB, MTZ, MTRX, MYRG, PRIM, PWR, and TISI

Infrastructure Services: ARE, BBY, ROAD, GVA, GLDD, IEA, ORN, SKA B, STRL, SUM, and TPC