English

English

Through the first half of 2019, the industrial supply sector continued to experience a significant amount of M&A activity driven by both strategic and private equity buyers. Strategic acquirers drove vertical integration across various sub-segments in addition to expanding geographic footprint while enhancing product offerings.

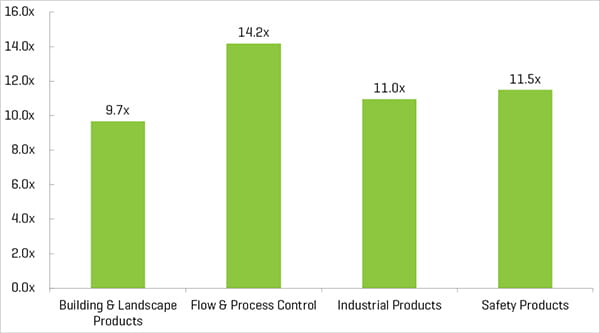

Private equity buyers continue to pursue new platform and add-on acquisitions to diversify portfolios and inorganically grow existing portfolio investments. The flow and process control segment continued to boast the highest trading multiples, with the building and landscape products segment being the most active from a M&A volume standpoint. The industrial products segment followed the flow and process control segment with the second-highest trading multiples of the industry, with the safety products segment showing strength as a multitude of private equity buyers conducted acquisitions within this space.

Two of the primary metrics which are closely monitored by participants of this industry include the Industrial Production index and raw materials pricing. The Industrial Production index, a measurement of the level of output from the mining, manufacturing, electric, and gas industries, is projected to rise over the coming year. Furthermore, raw material prices have seen volatility over the past several quarters, a trend that may continue throughout 2019, especially given the global business climate where tariffs and trade barriers are becoming more prevalent.

In the second half of 2019, we anticipate the industrial supply M&A market will remain robust, driven by consolidation, economic growth, and an uptick in infrastructure investment especially in North America where key infrastructure requires upgrade or replacement in the coming decade.

Key Takeaways

- Notable transaction activity from both strategic and private equity buyers, domestically and internationally

- Robust private equity platform and add-on activity points toward a positive M&A market outlook as capital is continually deployed amid a record overhang

- Strategic buyers continue to pursue acquisitive growth strategies to gain a competitive edge through expanding product and service offerings and/or geographic coverage

- Significant roll-up activity is indicative of continued industry consolidation

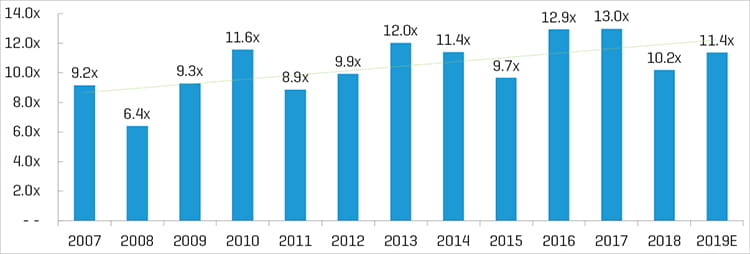

Historical Enterprise Value / EBITDA Multiples1,2

(1) FRED Industrial Production Index

(2) Multiples above 20x are excluded from the mean/median calculation; data represents the overall median of all four sub-segment benchmarks presented in this report

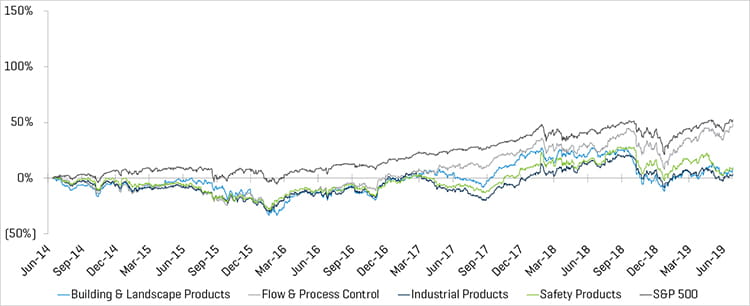

5-Year Historical Share Price Performance

Operating and Market Performance

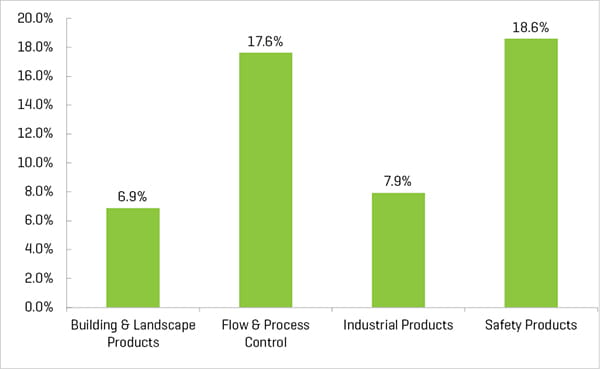

LTM EBITDA Margin

Enterprise Value / LTM EBITDA1

(1) Multiples above 20x are excluded from the mean/median calculation

Note: Median from public comp sets featured in report

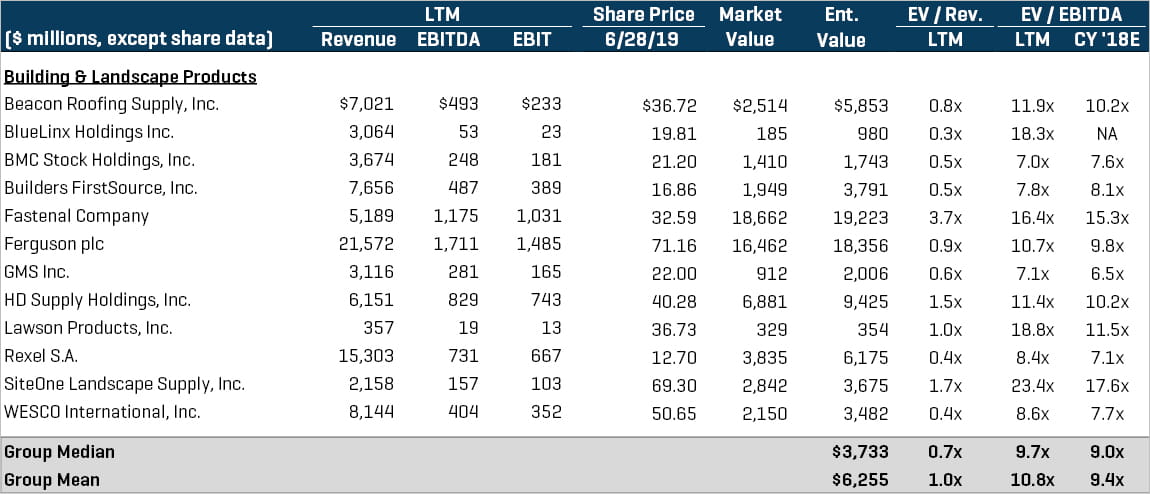

Building & Landscape Products

Significant consolidation activity by strategic buyers within the building and landscape products segment magnified the number of transactions within this sector, signaling a continued trend similar to that experienced in previous quarters. Private equity firms were also highly active in this sector as they continued to pursue platform and add-on acquisitions. Among the other segments across the industrial supply spectrum, the building and landscape products segment witnessed the greatest number of transaction activity for the first half of 2019, with notable transactions including:

- Louisiana-Pacific Corporation (NYSE:LPX), a global leader in manufacturing engineered wood building products, announced its acquisition of Prefinished Staining Products, a private distributor of factory finished exterior siding products. This acquisition serves as a complementary product offering allowing Louisiana-Pacific Corp. to expand its top line growth

- Construction Supply Group, a leading distributor of specialty construction materials and accessories, and a portfolio company of The Sterling Group, has conducted simultaneous roll-up acquisitions of Best Materials, Advantage Construction Supply, and Spec-West Concrete Systems. Over the span of two years, Construction Supply Group has completed 16 acquisitions, allowing the company to grow into the second-largest distributor of specialty construction materials throughout North America

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

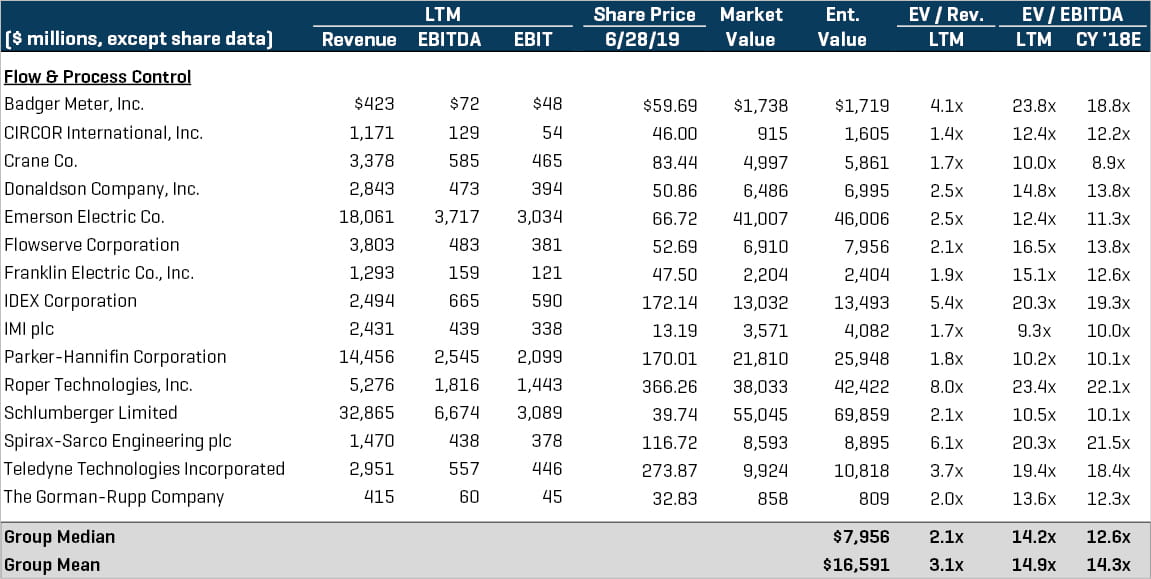

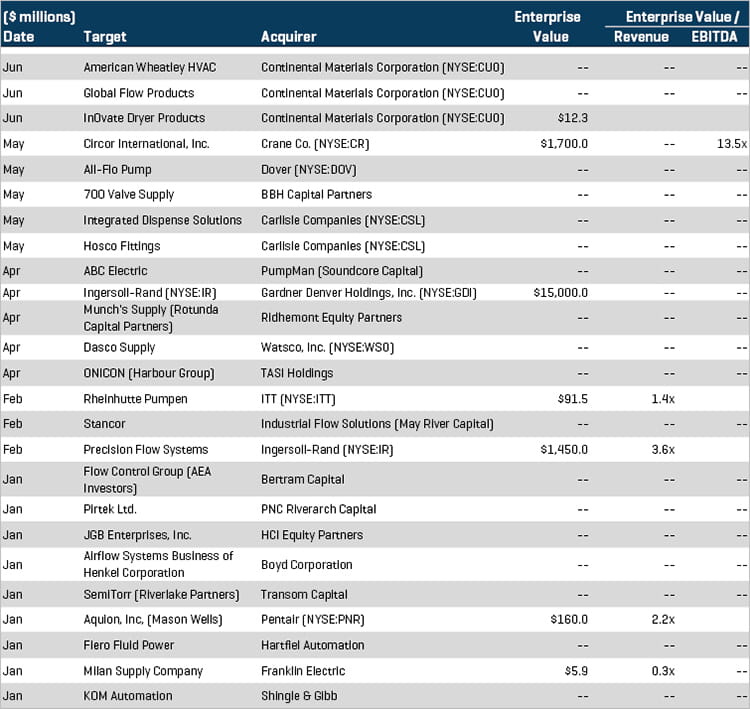

Flow & Process Control

Following the trend of previous quarters, the flow and process control segment produced the highest trading multiples with regard to EV / EBITDA. The segment also experienced strong M&A activity from large public companies looking to acquire smaller, predominantly private companies in an effort to expand product and service offerings. Private equity has invested in and supported growth of private companies which possessed unique business models within a fragmented industry. Notable transactions in the flow and process segment include:

- Crane Co. (NYSE:CR), a diversified manufacturer of highly engineered products for a diverse range of end markets, announced its acquisition of Circor International, Inc. for approximately $1.7 billion. The acquisition allows Crane to grow within the oil & gas space through the diversification of its flow control product offering

- Gardner Denver Holdings Inc. (NYSE:GDI), a leading global provider of mission-critical flow control equipment, announced its merger with Ingersoll-Rand (NYSE:IR) in a transaction valued at approximately $15 billion. The deal will make the combined entity a global leader in flow creation and industrial technologies

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

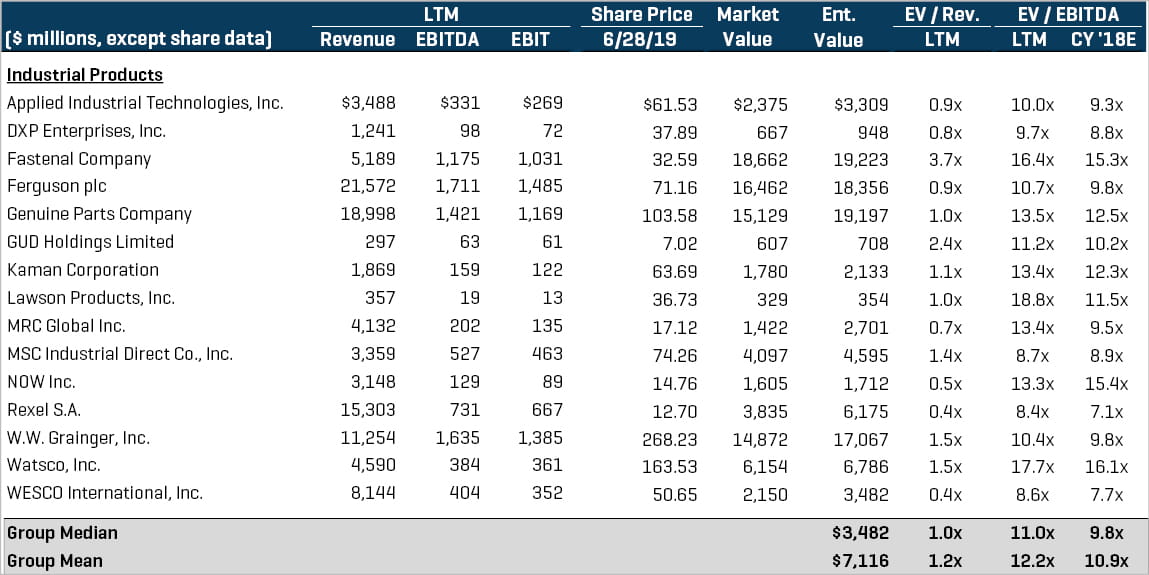

Industrial Products

The industrial products segment continues to exhibit strong M&A activity. Add-on acquisitions made by private equity buyers looking to grow existing platforms have historically made this a very active segment, with notable transactions from the first half of 2019 including:

- Littlejohn & Co., a leading global private equity firm focused on the middle market space has agreed to acquire the Distribution Segment of Kaman (NYSE:KAMN) for $700 million. Kaman’s Distribution Segment is a leading distributor of more than 6 million items within the industrials space and will serve as a strong platform for Littlejohn

- Lincoln Electric (NASDAQ:LECO), a global manufacturer of welding products and systems has entered into a definitive agreement to acquire Kaynak Teknigi Sanayi ve Ticaret A.S., a manufacturer and supplier of welding wires and equipment. The transaction allows Lincoln Electric to grow its geographic footprint allowing it to rise as a global leader within the welding systems space

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

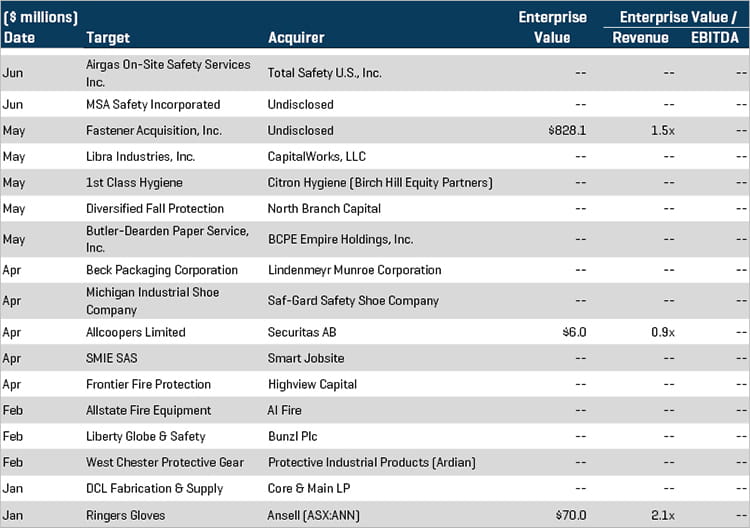

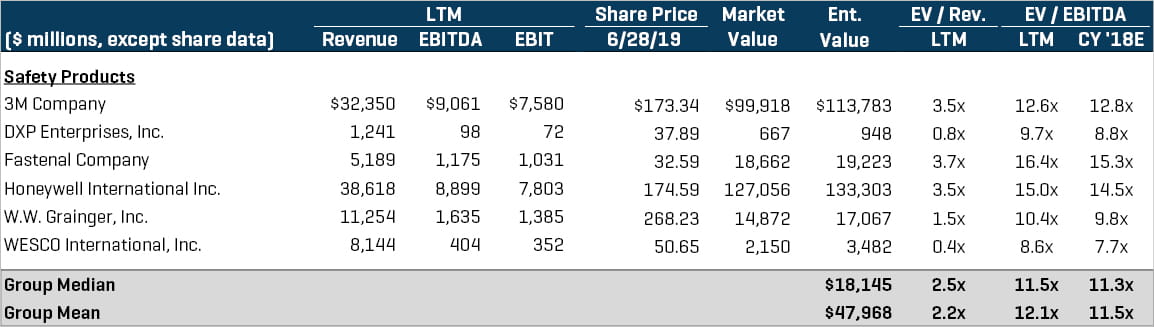

Safety Products

Private equity activity drove M&A volume in the safety products segment during the first half of 2019. Notable transactions within this segment include:

- CapitalWorks, LLC, a private equity firm focused on middle market companies primarily within the manufacturing and business services sector, has acquired Libra Industries, Inc., a recycler and supplier of safety products. The acquisition allows CapitalWorks to expand its portfolio of manufacturing companies while simultaneously providing the firm with a greater outlet of end market users

- Ansell (ASX:ANN), a leading manufacturer of industrial and medical safety equipment has entered into a definitive agreement to acquire Ringers Gloves for $70 million. The acquisition provides Ansell the opportunity to grow globally and penetrate new markets

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions