English

English

Industrial supply has continued to produce solid M&A activity in the third quarter of 2018, with momentum being driven by strategic acquirers vertically integrating across segments and private equity buyers pursuing new platform and add-on acquisitions. Our building and landscape products segment continued to contain the most transaction activity of the group, with the flow and process control segment holding its position with the highest trading multiples. Last-12-month EBITDA margins and EV / EBITDA multiples remain consistent throughout 2018 across all four industry segments, as market trends continue to host a positive environment for industry participants. The continued robust M&A environment in the third quarter can be attributed, in part, to strong growth in global industrial manufacturing, driven by increased demand across core end markets. The U.S. economy continues to grow at a consistent rate, supporting growth in construction spending and a healthy job market, as evidenced by the rise in construction employment in the third quarter. Additionally, continued private equity buyer interest in the industrial supply segment points to a positive outlook as we move into the final quarter of 2018.

Key Takeaways

- Serial acquirers consolidating niche industry segments through vertical integration, enabling enhanced product capabilities and expansion of geographic presence

- Firm builder confidence and increased construction spending and employment exhibits robust transaction activity in the building, landscape and construction products segment[1]

- Robust public strategic buyer consolidation activity points toward favorable market trends

- Private equity interest in platform and add-on acquisitions and portfolio optimization

- High capital availability and continued low borrowing costs support a positive M&A environment

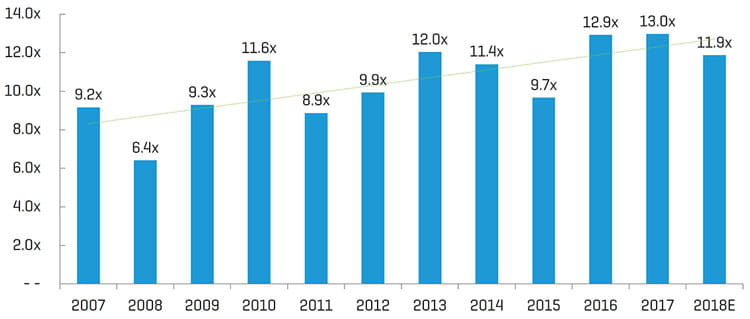

Historical Enterprise Value / EBITDA Multiples[2]

(1) Builder confidence reported through the National Association of Home Builders (NAHB) via the Wells Fargo Housing Market Index (HMI)

(2) Multiples above 20x are excluded from the mean/median calculation; data represents the overall median of all four sub-segment benchmarks presented in this report

Industry Statistics

5 –Year Historical Share Price Performance

Operating and Market Performance

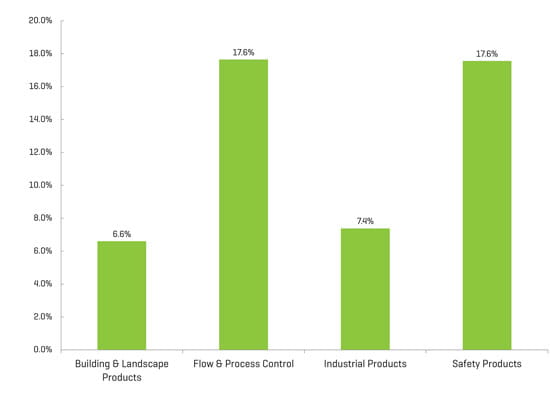

LTM EBITDA Margin

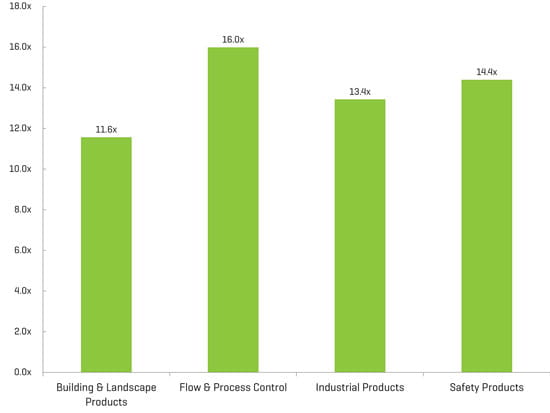

Enterprise Value / LTM EBITDA[1]

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Median from public comp sets featured in report

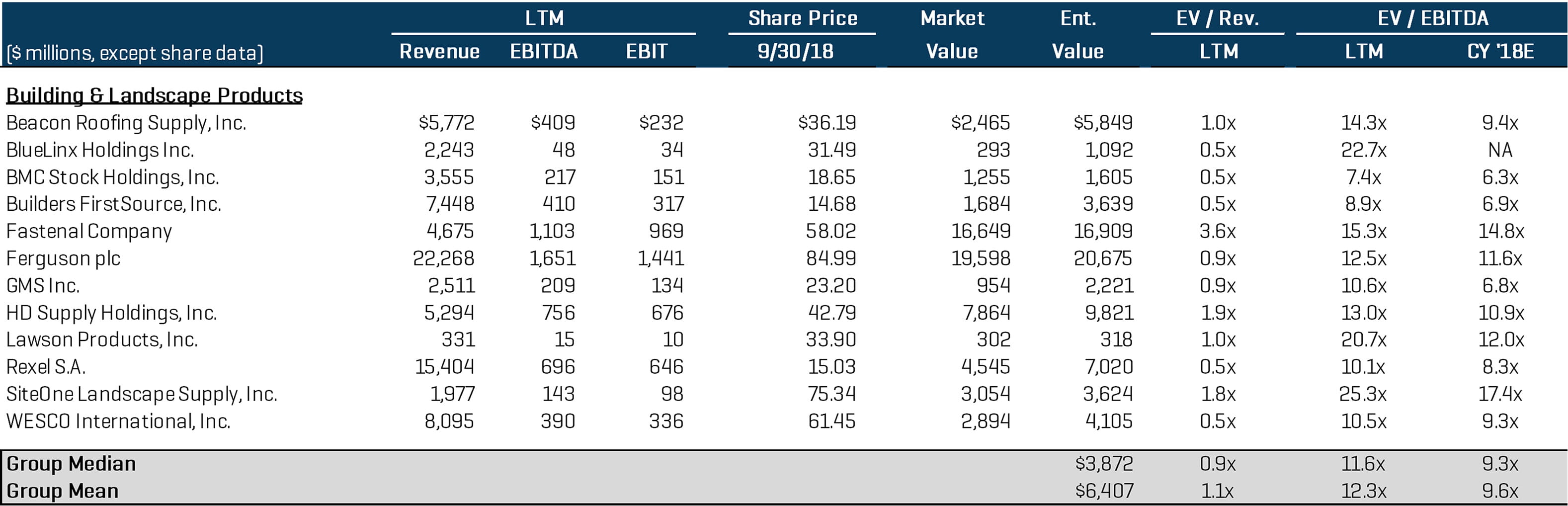

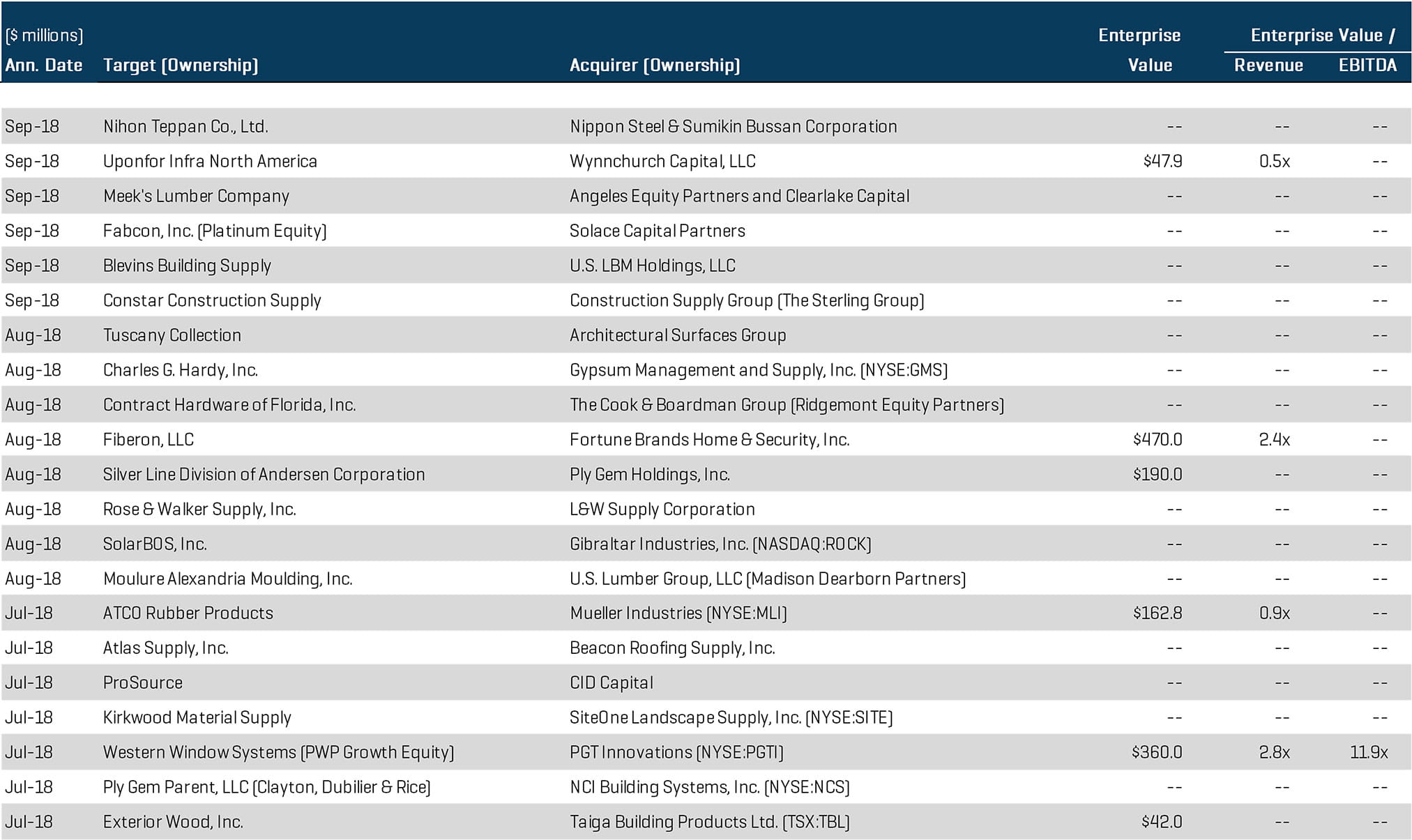

Building and Landscape Products

Backed by firm levels of commercial and residential builder confidence, as well as a rise in construction spending and employment, the building and landscape products segment flourished with strong M&A activity. The segment continues to be a favorable investment target for private equity buyers pursuing platform and add-on acquisitions, as well as a stage for significant activity from public strategic acquirers consolidating smaller players in the industry. This segment contained the most transaction activity for the quarter, with notable transactions including:

- PGT Innovations (NYSE:PGTI), a Florida-based manufacturer of residential windows and doors, agreed to acquire Western Window Systems, a building products and door systems manufacturer, from PWP Growth Equity, in a cash deal valued at $360 million. The transaction is expected to create a strategic platform for PGT Innovations to pursue critical Southwestern geographies

- NCI Building Systems, Inc. (NYSE:NCS) has entered into an agreement to acquire Ply Gem Parent, LLC, a North Carolina-based manufacturer of exterior building products, from private equity firm Clayton, Dubilier & Rice, for an undisclosed amount. The transaction is expected to close in the fourth quarter and the combined company will have a pro forma enterprise value of approximately $5.5 billion

- In a related transaction, Ply Gem Holdings, Inc. agreed to acquire the Silver Line vinyl window and patio door division of Andersen Corporation for approximately $190 million. The acquisition includes the portfolio of products sold under the Silver Line and American Craftsman brands, four manufacturing plants and the distribution and support services related to the division

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

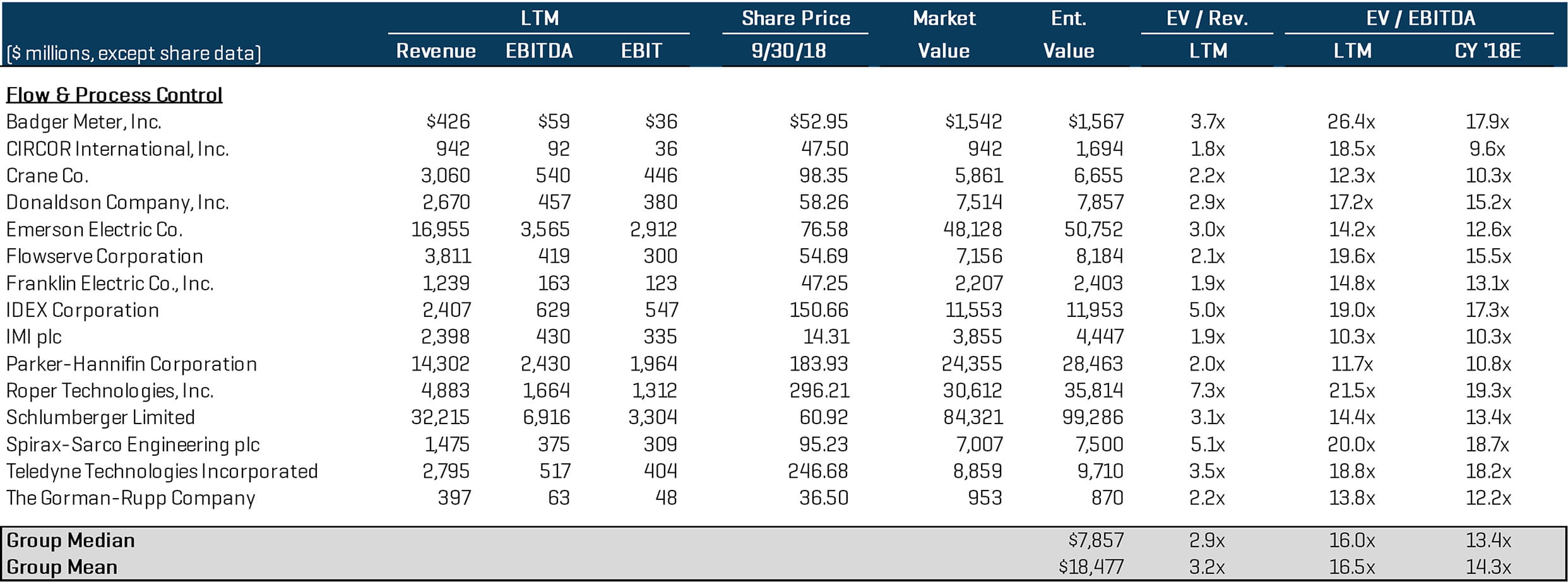

Flow & Process Control

The flow & process control segment again exhibited the highest trading multiples of the group in terms of EV / EBITDA and saw significant transaction activity in the third quarter coming from both publicly listed and private strategic buyers, as well as international entities. A series of private equity platform acquisitions were also completed. This segment’s notable transactions include:

- Baker Hughes (NYSE:BHGE), a GE company, announced an agreement to sell its Natural Gas Solutions (NGS) business, a provider of gas meters, pumps and other industrial flow products, to two separate entities: First Reserve Corporation, a private equity fund, and Pietro Fiorentini S.p.A., for a total aggregate value of $375 million

- Donaldson Company, Inc.’s (NYSE:DCI) acquisition of BOFA International Ltd., a United Kingdom-based designer, developer and manufacturer of fume extraction systems for a variety of industrial air filtration and flow applications, in a deal valued at $117.8 million – Donaldson Company will be combining the newly acquired BOFA International with its existing Industrial Filtration Solutions business that operates in the company’s Industrial Products segment

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

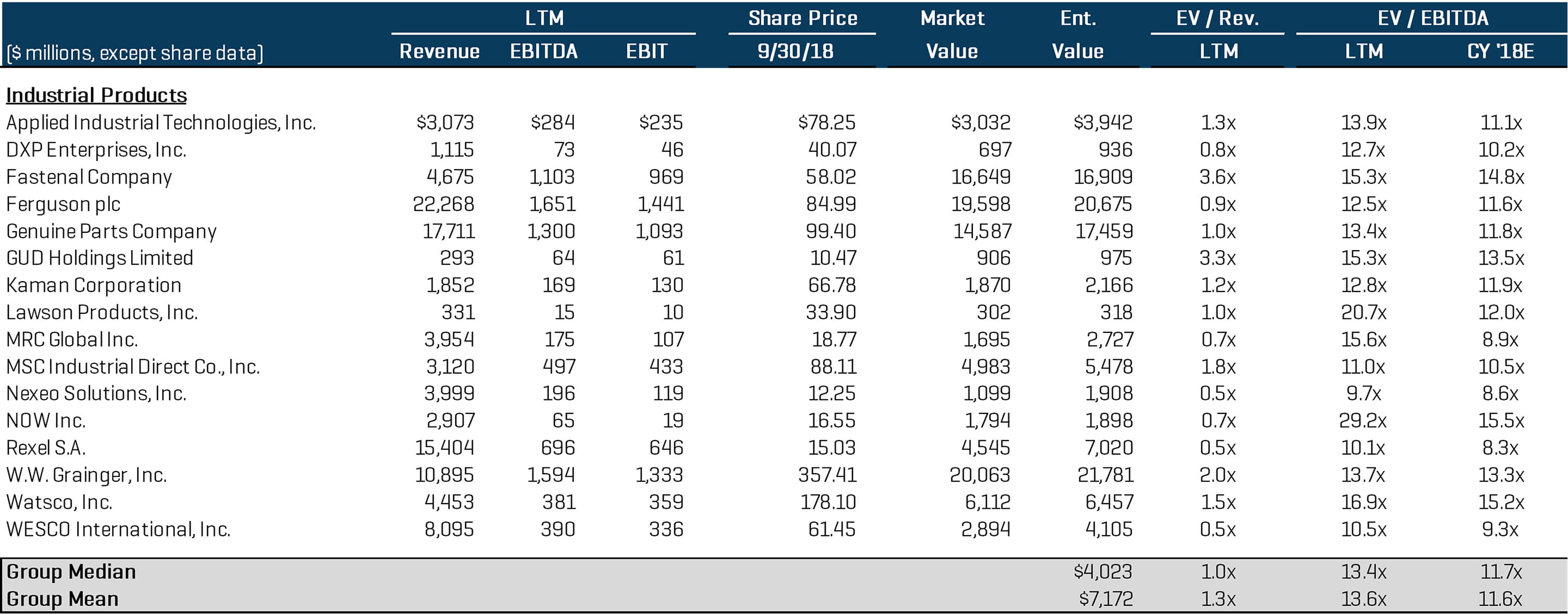

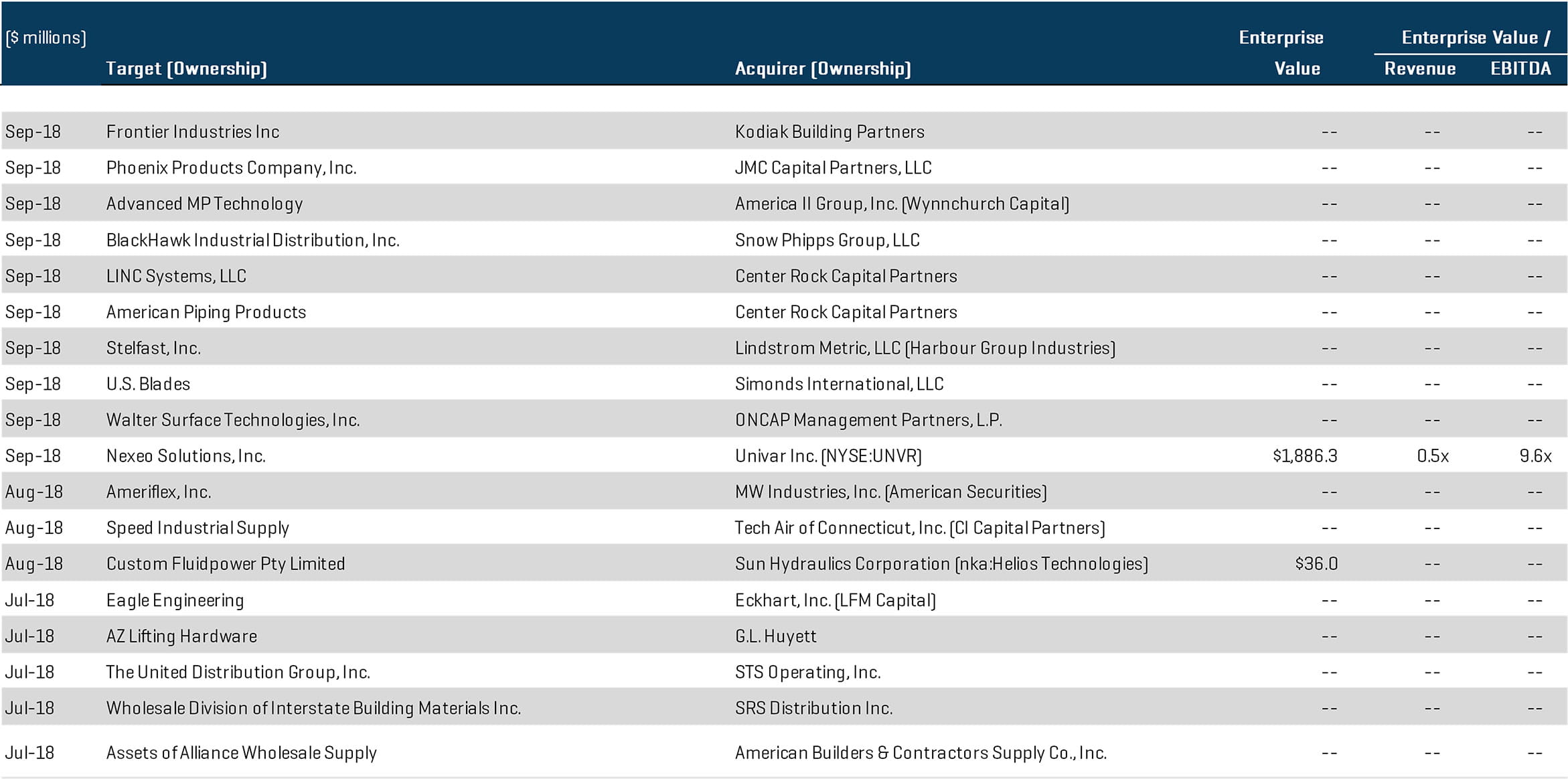

Industrial Products

The industrial products segment continued to generate substantial transaction activity in the third quarter, which has been driven by extensive overall growth in global industrial manufacturing, further increasing sales through industrial distribution channels. Activity in this segment came from a mixture of financial sponsors pursuing platform acquisitions and add-ons through portfolio companies, as well as large strategic buyers executing transactions to gain synergistic value. Notable transactions include:

- Univar, Inc. (NYSE:UNVR) has entered into a definitive agreement to acquire Nexeo Solutions (NASDAQ:NXEO), a leading global specialty chemicals and plastics distributor for industrial applications, in a deal valued at approximately $1.9 billion. Univar’s management notes that the transaction is expected to be accretive and to generate approximately $100 million of annual run rate cost savings synergies by the third year

- Center Rock Capital Partners, a Midwest-based private equity fund, invested in American Piping Products, a leading global distributor of steel pipes and valves, and LINC Systems, LLC, a North American distributor of fastener, packaging and MRO tools, in two separate transactions for an undisclosed amount

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

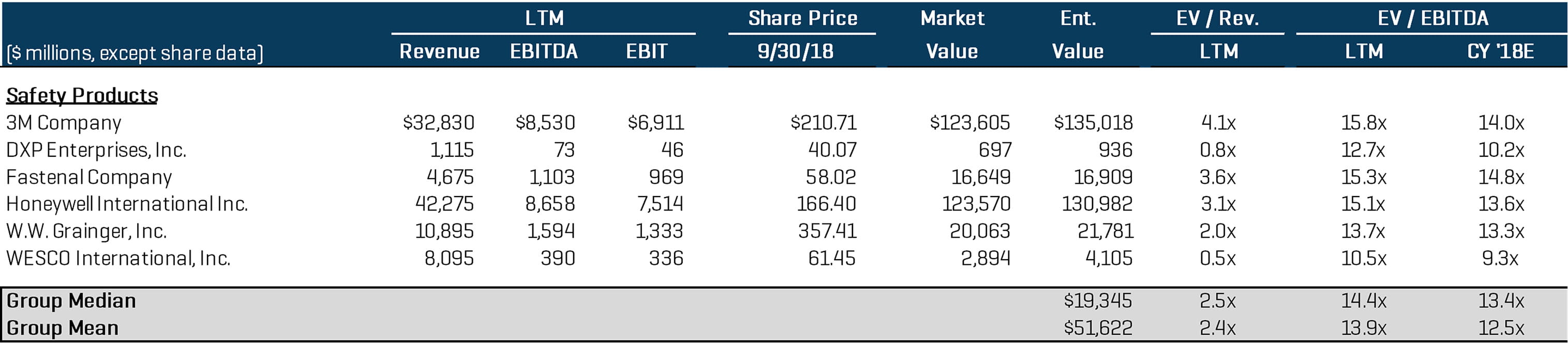

Safety Products

The safety products segment saw activity predominantly from strategic buyers looking to vertically integrate business operations and expand product offerings/capabilities, most notably, a serial acquirer pursuing an acquisitive growth approach. The safety products segment also experienced a number of private equity players pursuing attractive investment opportunities. Notable transactions within this segment include:

- Mallory Safety and Supply, Inc. announced its acquisition of Industrial Safety Supply Corporation, a California-based provider of technical safety products and services, for an undisclosed amount. The acquisition marks Mallory Safety and Supply’s 20th acquisition in the industrial safety products segment the last twelve months – the company notes its rationale has been to continue expanding upon its safety expertise, service and repair capabilities and build its geographical presence

- Core & Main LP, a Missouri-based water, sewer and fire protection products provider backed by Clayton, Dubilier & Rice, announced its acquisition of select assets of California-based DOT Sales Company for an undisclosed amount. The acquisition of DOT Sales Company’s Fontana, CA, facility adds to Core & Main’s 245 branch operation and enables the company to increase its exposure to Southern California

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

Operating and Market Performance