English

English

Industrial supply continued to produce solid M&A activity in the second quarter of 2018. Momentum was driven by strategic acquirers vertically integrating across segments and private equity buyers pursuing new platform and add-on acquisitions. EV / EBITDA multiples continue to trade at levels consistent with 2017 and the first quarter of 2018 across all four industrial supply segments. The building and landscape products segment saw the most transaction activity of the group, including a private equity mega-deal and notable strategic acquirer activity. We note that the flow and process control segment continues to trade at the highest multiples, followed closely by our industrial and safety products segments. The continued robust M&A environment in the second quarter can be attributed, in part, to positive industry dynamics, as global industrial manufacturing remains prosperous. The U.S. economy continues to show vigorous activity, supporting growth in construction spending and a healthy job market. Additionally, financial sponsor acquisition activity, the requirement to deploy capital in new investments and build via acquisition through existing portfolio holdings, points to a positive outlook as we move into the third quarter.

Key Takeaways

- Strong levels of builder confidence and construction spending exhibited robust transaction activity in the building, landscape, and construction products segment1

- Private equity firms showed interest in platform and add-on acquisitions and portfolio optimization

- High capital availability and continued low borrowing costs supported a positive M&A environment

- Trading multiples among public companies remained strong, enabling accretive acquisitions at robust valuations

- There was active M&A engagement domestically and internationally

- Rising tides in global industrial manufacturing propelled M&A activity across segments

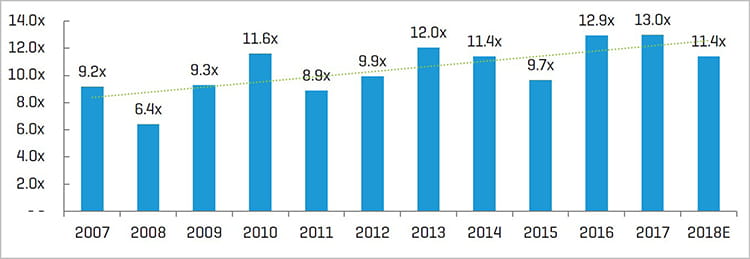

Historical Enterprise Value / EBITDA Multiples2

(1) Builder confidence reported through the National Association of Home Builders (NAHB) via the Wells Fargo Housing Market Index (HMI)

(2) Multiples above 20x are excluded from the mean/median calculation; data represents the overall median of all four sub-segment benchmarks presented in this report

Industry Statistics

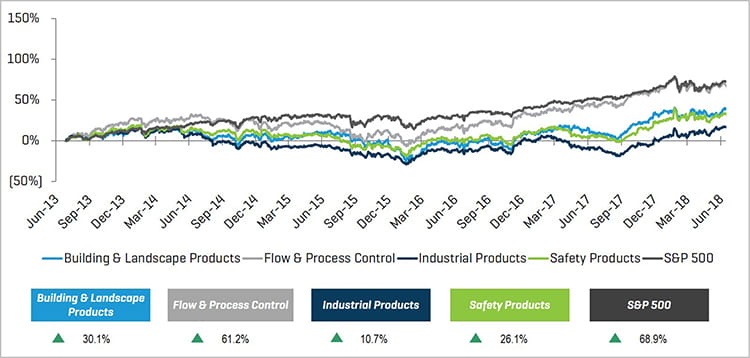

5 –Year Historical Share Price Performance

Operating and Market Performance

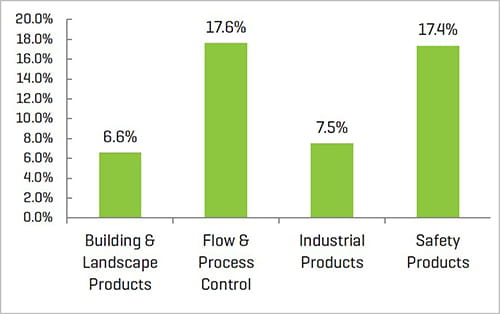

LTM EBITDA Margin

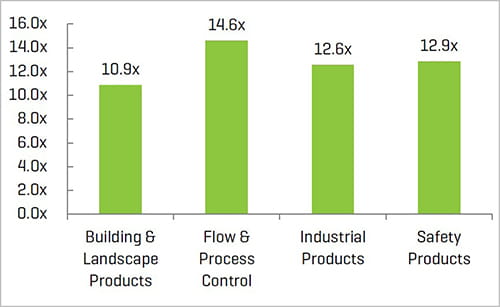

Enterprise Value / LTM EBITDA1

(1) Multiples above 20x are excluded from the mean/median calculation

Note: Median from public comp sets featured in report

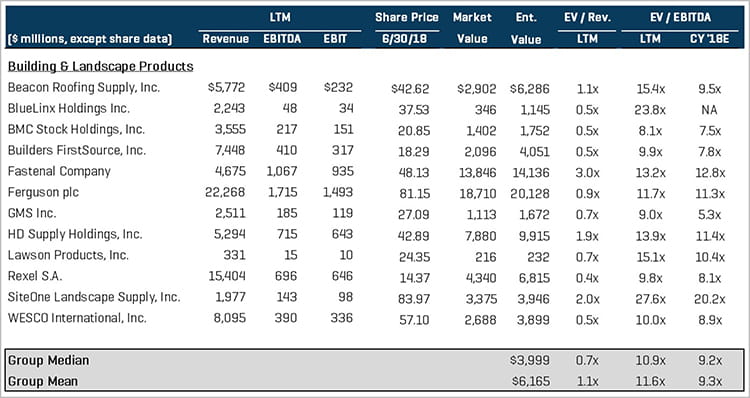

Building & Landscape Products

The building and landscape products segment flourished with strong M&A activity backed by solid residential and commercial builder confidence and a robust labor market. The segment saw a mix of private equity and strategic acquisition activity in the second quarter of 2018, including a financial sponsor mega-deal, and a number of publicly traded strategic acquirers looking to expand business activity operationally and geographically. This segment contained the most transaction activity for the quarter, with notable transactions including:

- Leonard Green & Partners (LGP), a private equity firm with over $23 billion in AUM, agreed to acquire U.S.-based building products manufacturer SRS Distribution Inc. from Berkshire Partners in a deal valued at more than $3 billion

- Gypsum Management & Supply’s (a subsidiary of GMS Inc. (NYSE:GMS)), acquisition of WSB Titan Inc., Canada’s largest independent building supplies dealer, for approximately $627 million. Management of GMS note strategic synergies through an expanded distribution network across the U.S. and Canada, further establishing GMS’ market-leading position in the wallboard and interior building products space

- Kohlberg & Company, a private equity firm, acquired Senneca Holdings, Inc., a leading North American manufacturer and distributor of doors and enclosures for commercial and industrial end markets, from Audax Private Equity for approximately $605 million

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

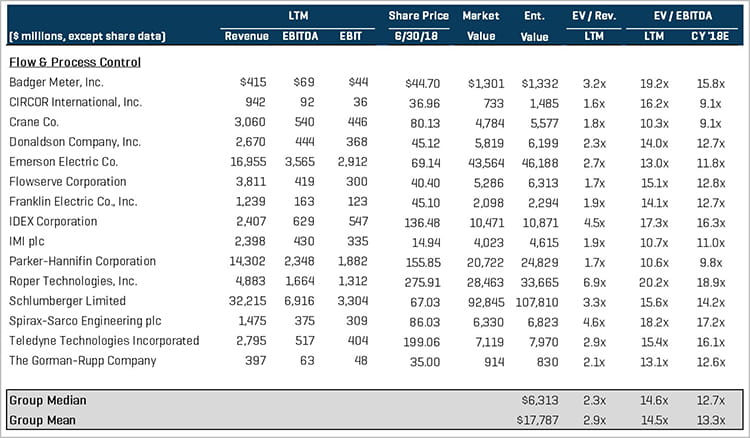

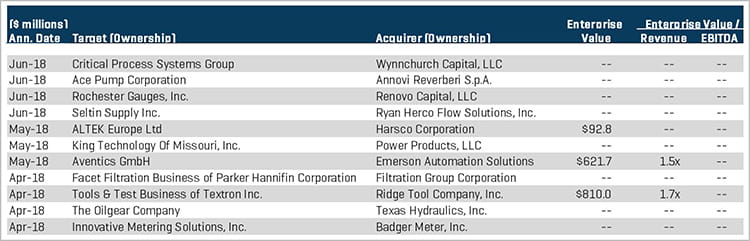

Flow & Process Control

The flow and process control segment again exhibited the highest trading multiples of the group in terms of EV / EBITDA and saw a majority of its acquisition activity from strategic acquirers (including several large public enterprises), with some private equity buyer involvement executing platform acquisitions. This segment’s notable transactions include:

- Ridge Tool Company, Inc., a subsidiary of Emerson Electric Co. (NYSE:EMR), announced it has entered into an agreement to acquire Tools & Test Business of Textron Inc., a manufacturer of utility tools and diagnostics instruments, for approximately $810 million – the deal includes all of the Textron Tools & Test businesses and brands; such as Greenlee, Greenlee Communications, Greenlee Utility, HD Electric, Klauke, Sherman+Reilly, and Endura

- Badger Meter Inc.’s (NYSE:BMI) acquisition of Innovative Metering Solutions, Inc., a distributor of residential and commercial water meters and metering systems, for an undisclosed amount. Following the acquisition, Innovative Metering Solutions began doing business as National Meter & Automation

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

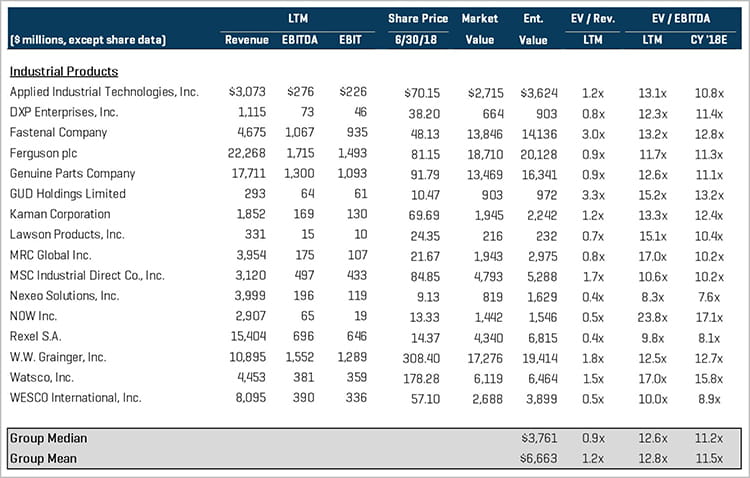

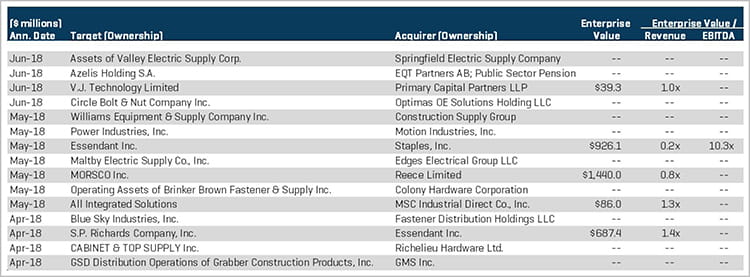

Industrial Products

The industrial products segment delivered substantial transaction activity in the second quarter, which has been driven by extensive overall growth in global industrial manufacturing. Rising tides in the industry have allowed for considerable M&A activity in this segment both internationally and domestically. Acquisitions in this segment came predominantly from larger strategic acquirers, pointing toward a theme of continued consolidation within the industry. Notable transactions include:

- Staples Inc. announced its initial proposal to acquire the shares of Essendant Inc. (Nasdaq:ESND), a leading distributor of workplace and industrial supplies, in an all cash consideration over $430 million – the initial proposal was revised by Staples, indicating it would be able to identify incremental value opportunities that would increase its revised offer significantly in excess of the original $11.50 per share, which is contingent on further discussions with Essendant

- In a related transaction, Essendant Inc. entered into a definitive merger agreement with S.P. Richards Company, Inc., a subsidiary of Genuine Parts Company (NYSE:GPC), in a Reverse Morris Trust transaction valued at approximately $690 million. The transaction came ahead of the Staples acquisition offer on Essendant

- Reece Limited (ASX:REH), an Australian plumbing products supplier entered into a binding agreement to acquire U.S.-based MORSCO Inc., a privately held distributor of plumbing, HVAC, and industrial piping products, from Advent International Corporation for approximately $1.4 billion – a rare type of Australian-American transaction that will enable Reece to increase market exposure to the Southern U.S. region

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

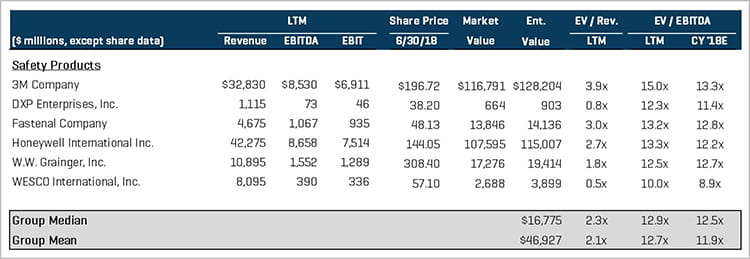

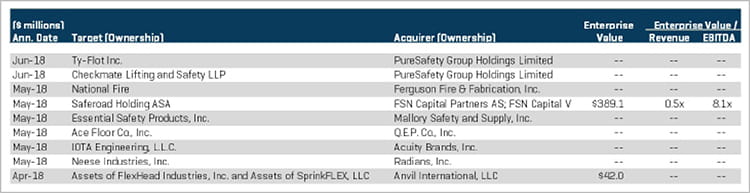

Safety Products

The safety products segment saw activity predominantly from strategic buyers looking to vertically integrate business operations and expand product offerings/capabilities, as well as a number of private equity players chasing attractive investment opportunities. Notable transactions within this segment include:

- Acuity Brands, Inc. (NYSE:AYI) announced its acquisition of IOTA Engineering, LLC, a manufacturer of highly engineered emergency lighting equipment for industrial and institutional applications, from Industrial Growth Partners, a private equity firm – Acuity Brands management noted that IOTA will directly support the smart building and lighting solutions strategy of Acuity, providing strategic synergies and product line expansion

- Mallory Safety and Supply, Inc. acquiring Essential Safety Products, Inc. (ESP), a distributor of industrial and facility safety equipment, boosts the combined company’s Western U.S. presence and safety expertise

- Ferguson Fire & Fabrication, Inc., subsidiary of Ferguson Enterprises, Inc. and the nation’s largest independent provider of fire protection systems, acquired National Fire Products, LLC – the transaction strengthens Ferguson Fire & Fabrication’s capabilities via National Fire’s expertise in sprinkler applications

Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

All Sources for charts: S&P Capital IQ and Stout Research