English

English

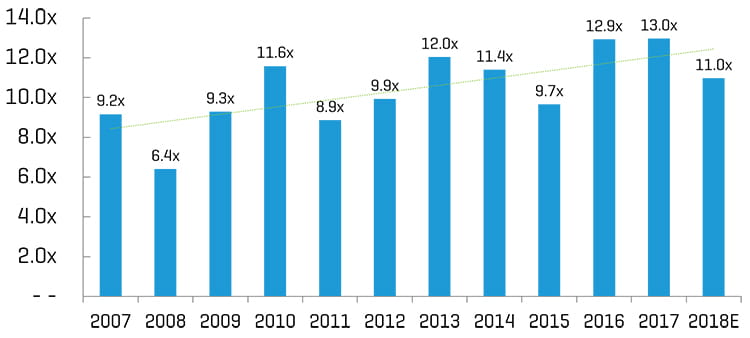

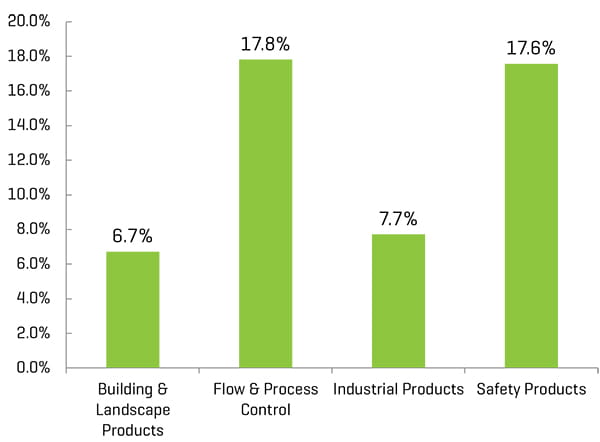

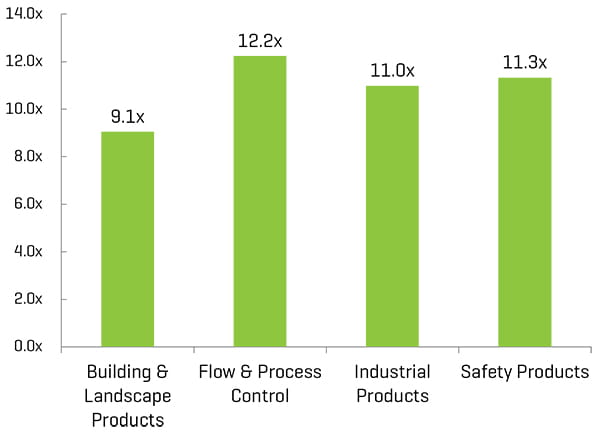

Industrial supply continued to produce solid M&A activity in the fourth quarter of 2018. Momentum has been driven by strategic acquirers vertically integrating across segments and private equity buyers pursuing new platform and add-on acquisitions. Our building and landscape products segment once again contained the most transaction activity of the group, with the flow and process control segment exhibiting the highest trading multiples. The industrial products segment continues to be an attractive area where buyers seek to grow through product offering diversification, while the safety products segment hosts a strong growth platform as industrial and commercial safety equipment and technology benefits from regulatory changes. Last-12-month EBITDA margins and EV / EBITDA multiples are lower than in the past two years, widely due to the market hosting volatile performance in the fourth quarter of 2018. Despite lower multiples, the industrial supply market continues to benefit from a strong economy; however, global trade and raw materials pricing for key building products components are areas that industry participants are closely watching. The industrial supply M&A market is expected to remain robust in 2019, driven by economic growth, a healthy job market, and an uptick in infrastructure investment.

Key Takeaways

- Notable transaction activity across all segments from both strategic and private equity buyers

- Robust private equity platform and add-on activity points toward a positive M&A market outlook

- Strategic buyers continue to pursue acquisitive growth strategies to gain a competitive edge through expanding product and service offerings and/or geographic coverage

- Significant roll-up activity is indicative of continued industry consolidation

- Strong M&A engagement domestically and internationally

Historical Enterprise Value / EBITDA Multiples ¹

Operating and Market Performance

LTM EBITDA Margin

Enterprise Value / LTM EBITDA ¹

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Median from public comp sets featured in report

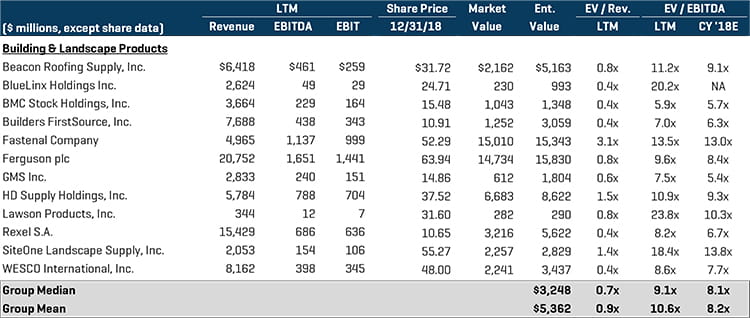

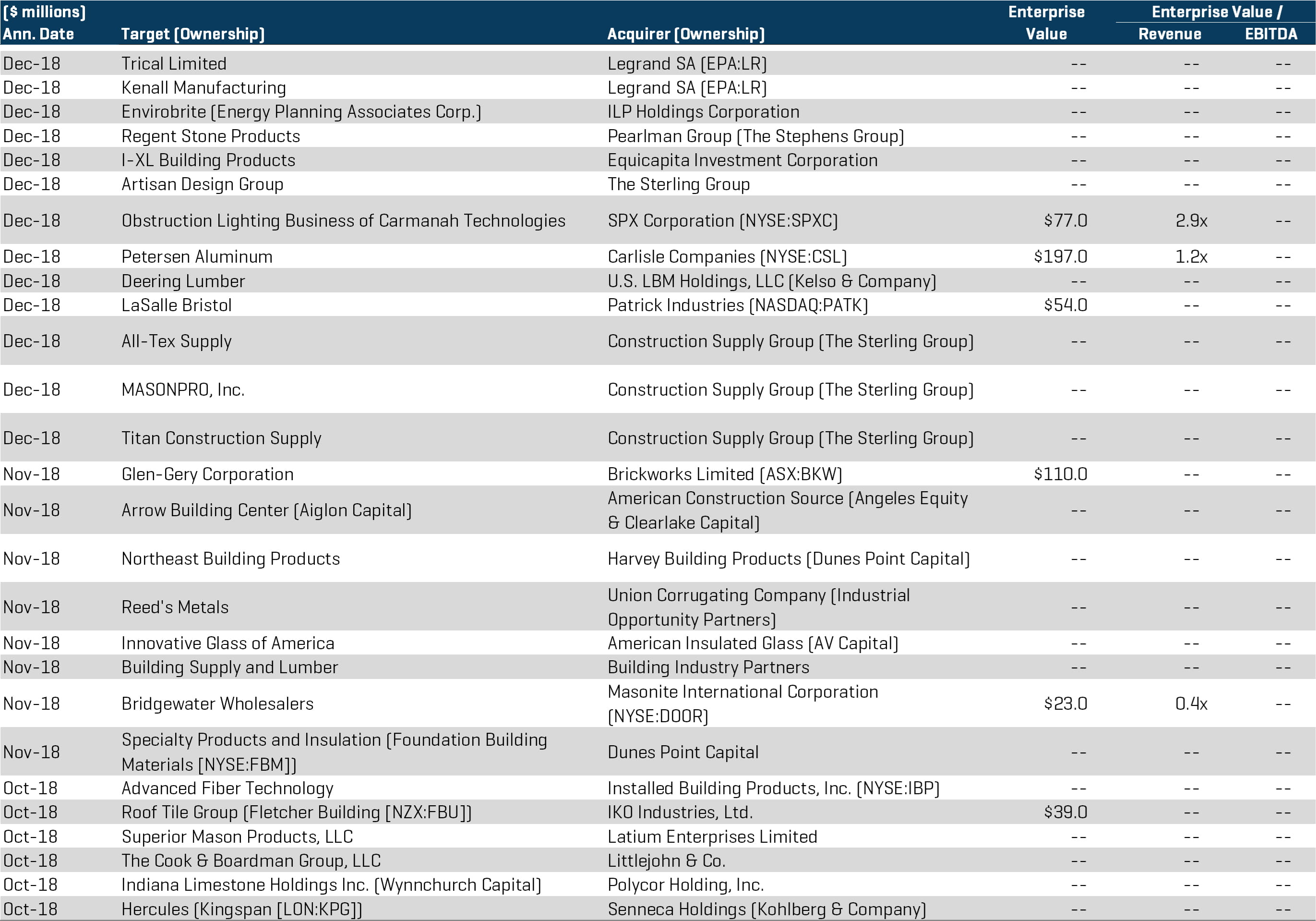

Building & Landscape Products

The building and landscape products segment benefited from significant roll-up activity by strategic buyers, pointing toward continued industry consolidation in 2019. Private equity firms were also seen active on both sides of the transaction; securing strong returns through portfolio exits and chasing attractive opportunities through platform acquisitions. While this segment contained the lowest multiples, in terms of EV / EBITDA, across the industrial supply spectrum, the segment contained the most transaction activity for the quarter, with notable transactions including:

- Carlisle Companies (NYSE:CSL), a global leader in building products through its Carlisle Construction Materials segment, announced its acquisition of Petersen Aluminum, a privately held manufacturer and supplier of metal roofing products, for approximately $197 million

- Construction Supply Group, a leading distributor of specialty construction materials and accessories, and a portfolio company of The Sterling Group, has conducted simultaneous roll-up acquisitions of All-Tex Supply, MASONPRO, Inc., and Titan Construction Supply. Over the past two years, Construction Supply Group has completed 13 acquisitions, forming the second-largest specialty construction supplies distributor in North America

Public Comparables ¹

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

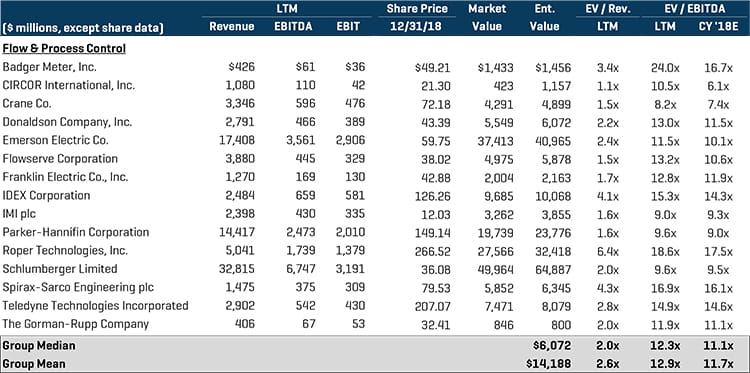

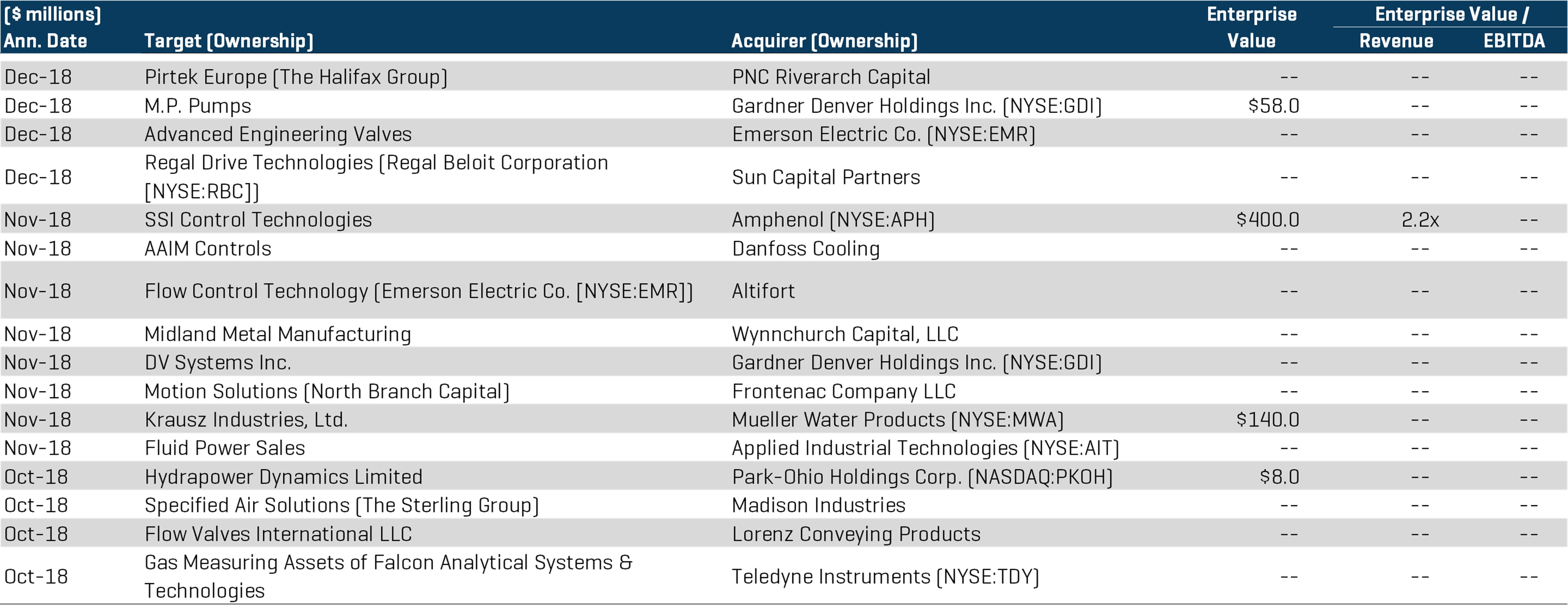

Flow & Process Control

The flow and process control segment again exhibited the highest trading multiples of the group in terms of EV / EBITDA and saw significant transaction activity in the fourth quarter coming predominantly from large public companies expanding into niche product and service offerings through an acquisitive approach. Private equity buyers also found attractive investment opportunities in private companies offering a unique business model to a fragmented industry. This segment’s notable transactions include:

- Gardner Denver Holdings Inc. (NYSE:GDI), a leading global provider of mission-critical flow control equipment, announced its acquisition of M.P. Pumps, a Fraser, MI-based manufacturer of industrial pumps and aftermarket parts for $58 million. The acquisition expands Gardner Denver’s offerings in its specialty industrial pump segment and allows for increased access to the market

- In a related transaction, Gardner Denver acquired DV Systems, an Ontario, Canada-based manufacturer and supplier of compressors. DV Systems will become a part of Gardner Denver’s Industrials segment

- Amphenol Corp. (NYSE:APH) has entered into a definitive agreement to acquire SSI Control Technologies (“SSI”), an innovative manufacturer of process control technologies for the automotive, HVAC and industrial, and material handling industries. The transaction is expected to close in early 2019 for a transaction value of approximately $400 million

Public Comparables ¹

<(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

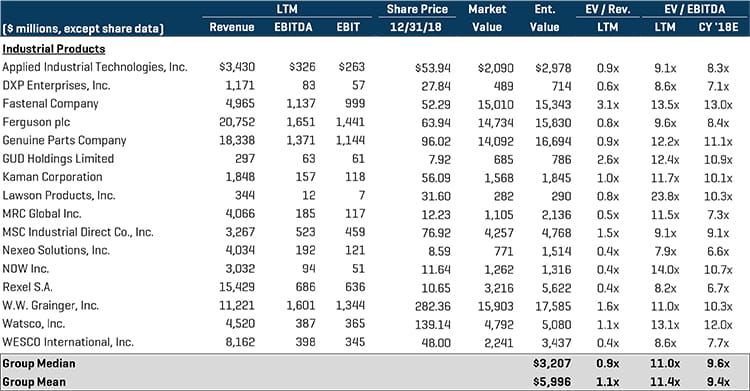

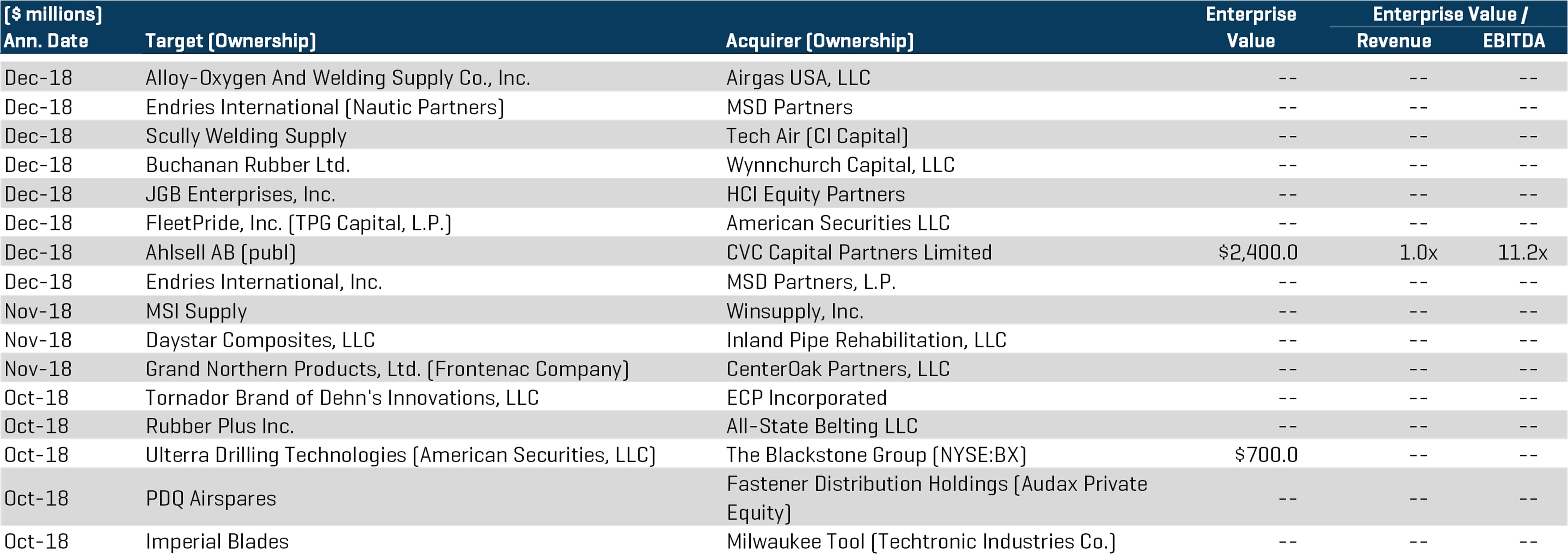

Industrial Products

The industrial products segment continues to benefit from strong transaction activity as private equity firms are seen actively pursuing unique investment opportunities and strategic buyers seek diversification in product offerings and capabilities. This segment has historically been an active area for private equity firms to grow existing platforms through add-on acquisitions. Notable transactions include:

- CVC Capital Partners, a leading global private equity firm, has agreed to acquire Ahlsell AB from Cinven and Goldman Sachs Capital Partners for $2.4 billion. Ahlsell is a distributor of construction products and machinery under the Nordic brand. A CVC spokesperson announced that it plans to use the company as a platform for organic growth and acquisitions

- The Blackstone Group (NYSE:BX) has entered into a definitive agreement to acquire a controlling majority interest in Ulterra Drilling Technologies, the largest independent supplier of tool bits predominantly to the oil and gas industry, in a transaction valued at $700 million

Public Comparables ¹

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

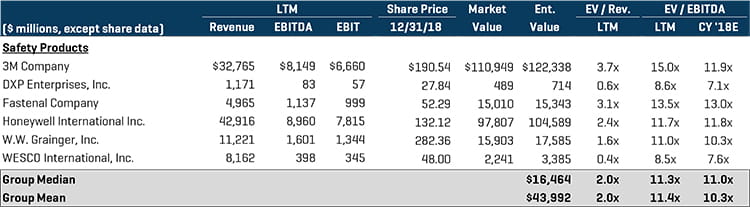

Safety Products

The safety products segment followed the flow and process control segment closely, exhibiting the second-highest trading multiples of the group. Transaction activity in the fourth quarter was driven predominantly by private equity players pursuing both platform and add-on acquisitions, as exhibited by Riverside’s simultaneous buy-and-build strategy detailed below. Notable transactions within this segment include:

- SureWerx, Inc., a portfolio company of The Riverside Company, has acquired the Jackson Safety and Wilson Safety Brands of Kimberly-Clark Professional. The acquisition includes part of Kimberly-Clark’s Industrial Personal Protective Equipment business and is part of an ongoing effort for Kimberly-Clark to streamline its global safety and scientific businesses by focusing on key product categories

- The add-on acquisition followed shortly after The Riverside Company acquired SureWerx, Inc. in November 2018 and marks a beginning to Riverside’s buy-and-build strategy with the portfolio company

- Audax Private Equity announced its acquisition of Colony Hardware Corporation, a leading distributor of safety products, tools, and other contractor supplies based in Orange, CT. Colony Hardware was previously a portfolio company of Tailwind Capital

Public Comparables ¹

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions