English

English

The industrial services industry closed out the fourth quarter of 2018 with strong transaction volume domestically and internationally. Continued industry consolidation, evolving customer and end-market expectations for service offerings, and a growing economy have been emblematic of vigorous M&A activity. Diversification in service capabilities and an expansive geographic presence continue to be differentiators, of which, large industry players are accessing by utilizing an acquisitive growth approach. Strategic buyers and private equity firms are continually seeking attractive services-based commercial and industrial firms with a competitive edge, either as platforms or bolt-on investments. Last-12-month (LTM) EBITDA margins remain consistent; however, trading multiples are lower across the board in correlation with general market volatility. Industry growth, however, remains optimistic as key end markets continue to benefit from positive industry dynamics. Additionally, digital transformation and technological commingling within the industrial services segment have forced a greater emphasis on process improvement and industrial automation, which will ultimately provide more opportunity for companies that deliver industrial services.

Key Takeaway

- Continued strong industrial services M&A activity

- Digital transformation and evolving customer expectations drive momentum in the transportation and logistics segment

- Renewed regulation and continued infrastructure investment reinforce increasing demand for facility support services

- Cross-border M&A activity continued to surge as large, public corporations seek to diversify by expanding geographic presence

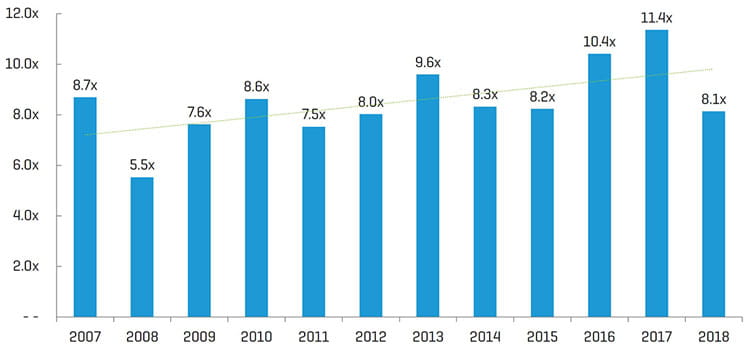

- Valuation multiples down from 2017 high

Historical Enterprise Value / EBITDA Multiples¹

(1) Multiples above 20x are excluded from the mean/median calculation; data represents the overall median of all nine sub-segment benchmarks presented in this report

Industry Statistics

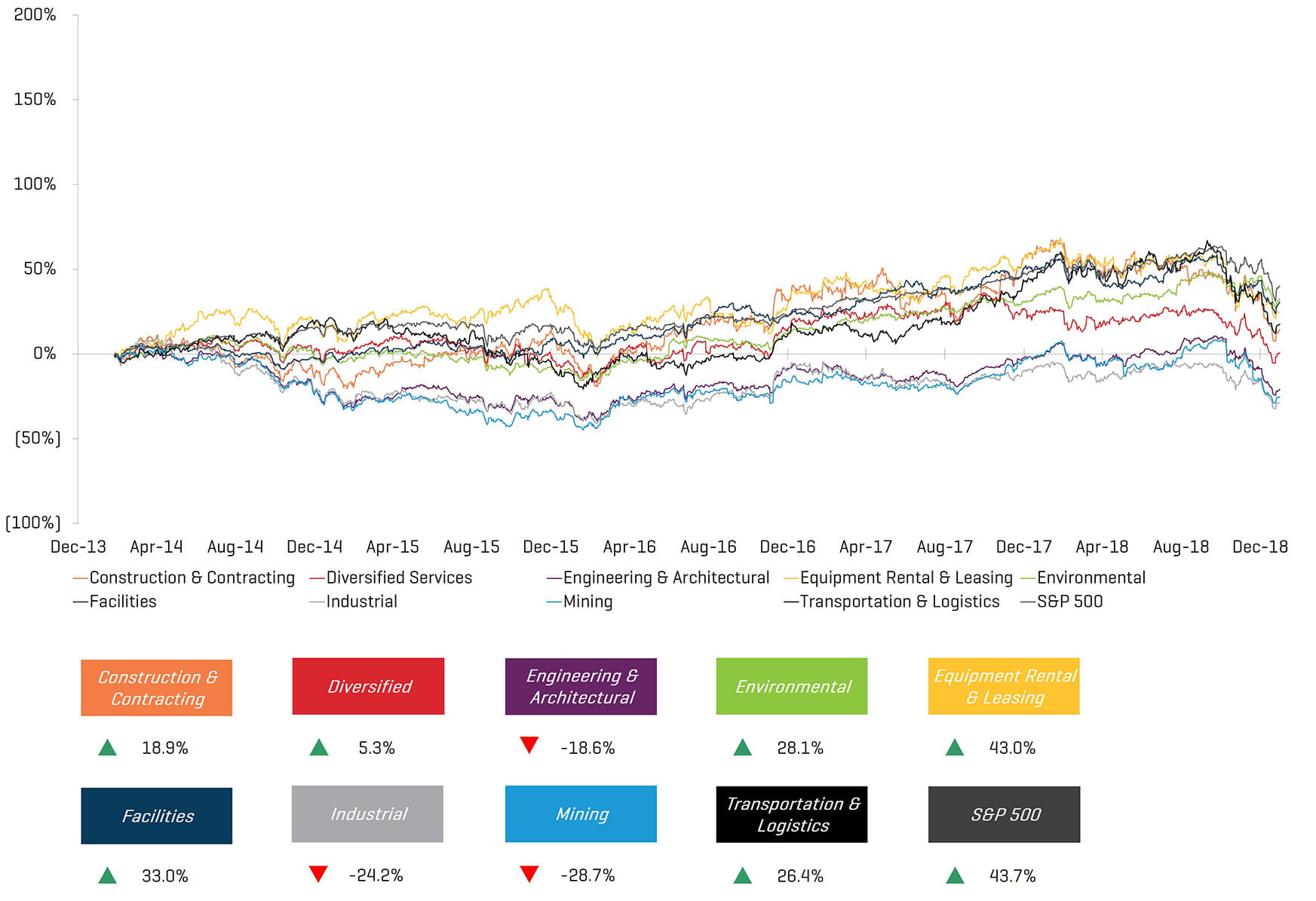

5-Year Historical Share Price Performance

Operating and Market Performance

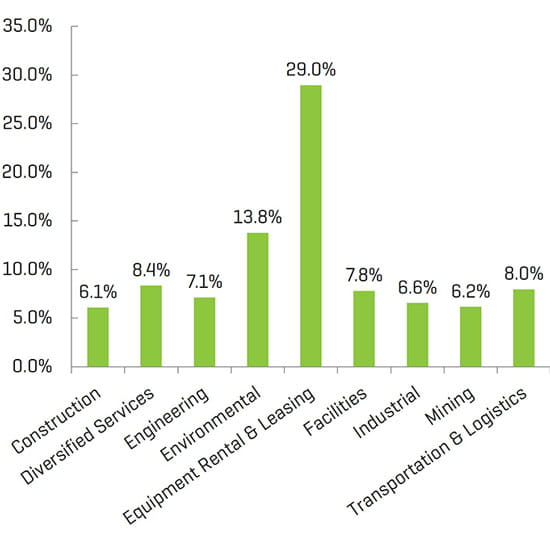

LTM EBITDA Margin

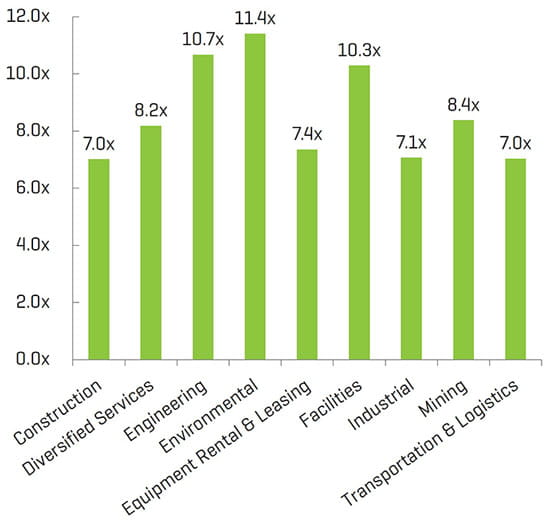

Enterprise Value / LTM EBITDA¹

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Median from public comp sets featured in report

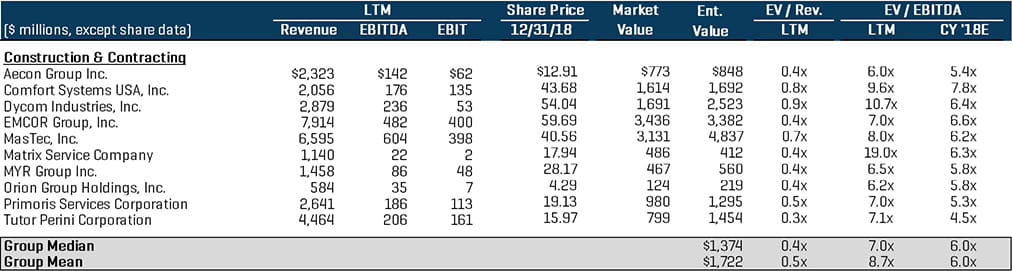

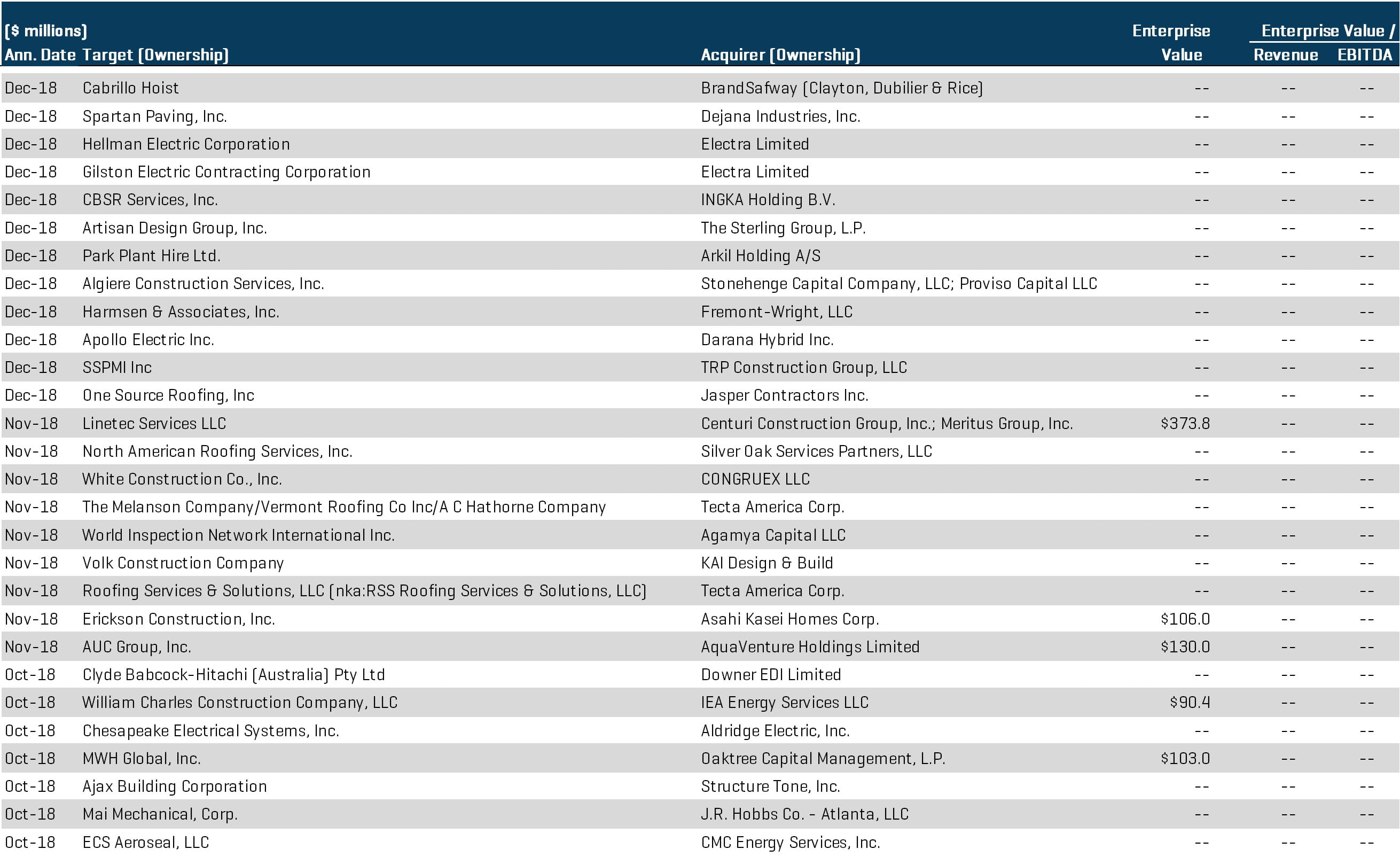

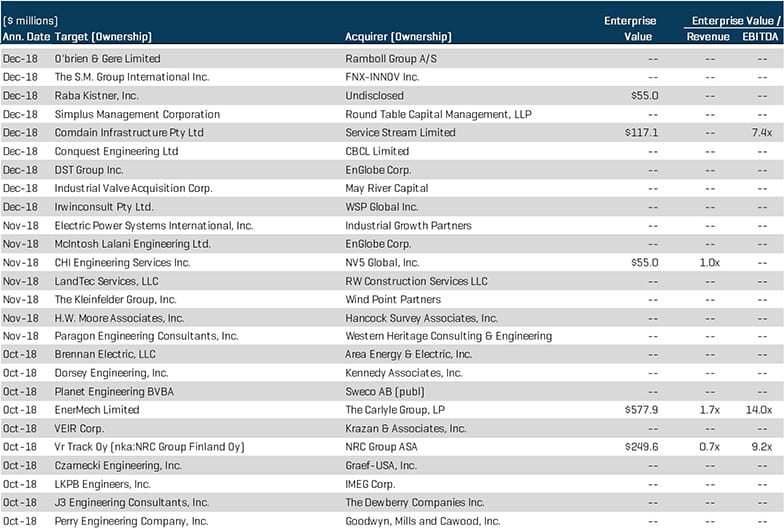

Construction & Contracting Services

Industry consolidation, as demonstrated by strategic buyer roll-up activity, remained constant in the fourth quarter as industry players seek to capitalize on increased construction and contracting activity in key metropolitan hubs. Continued private equity activity points toward steady M&A trends in 2019. Notable transactions include:

- Electra Limited (TLV:ELTR), a global construction services company headquartered in Israel, announced the acquisition of Hellman Electric Corp., a New York-based electrical construction contractor

- In a related transaction, Electra Ltd. acquired Gilston Electric Contracting Corp., a fully licensed electrical contracting company based in New York. The transaction, combined with the acquisition of Hellman Electric, broadens Electra’s electrical contracting services expertise and expands the company’s presence in North America

- Oaktree Capital Management, a leading global alternative investment manager, has acquired MWH Global, Inc., a worldwide provider of construction management services and design-build solutions in the water and wastewater infrastructure industry, for $103 million

Public Comparables¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

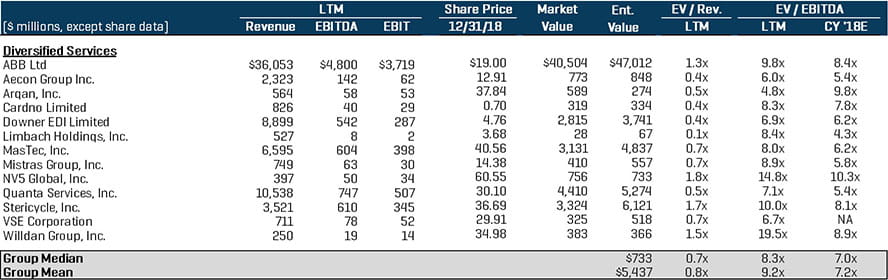

Diversified Services

The diversified services segment saw a mixture of large strategic acquisition activity as industry players pursue complimentary service offerings and capabilities, as well as private equity buyers diversifying industrials-oriented portfolios. Notable transactions include:

- DBM Global Inc. has agreed to acquire GrayWolf Industrial, a specialty industry maintenance, repair, and installation services provider, in a transaction valued at $135 million. The transaction fuels DBM’s acquisitive growth strategy and goal of becoming a $1 billion revenue-generating global industrial services company

- American Securities LLC, a leading U.S. private equity firm, announced the closing of its acquisition of CPM Holdings, Inc., a leading global supplier of engineered process equipment for diversified applications. CPM serves a global base of over 5,000 customers through its facilities in Europe, Asia, Latin America, and North America. Financial terms were not disclosed

Public Comparables¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

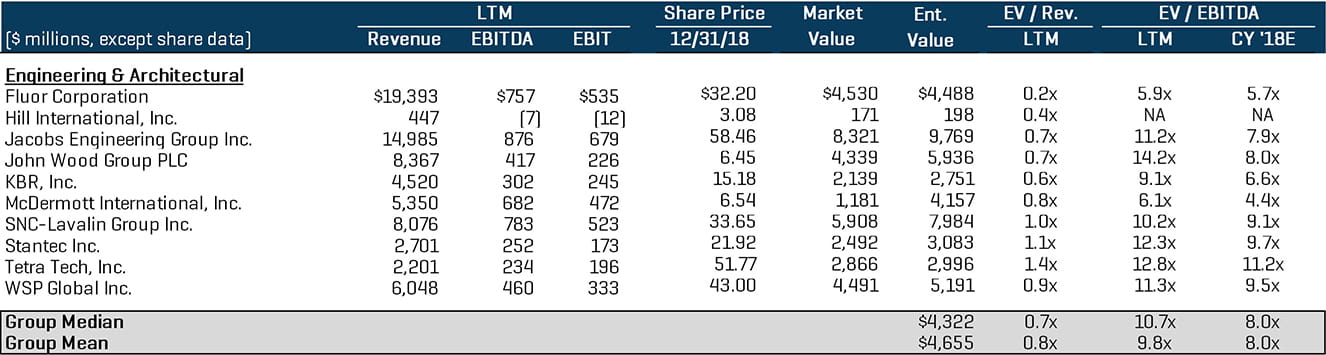

Engineering & Architectural Services

Private equity buyers were active in the fourth quarter executing platform and add-on acquisitions as a rise in construction and industrial production activity has increased the demand for engineering and contracting services. Continued infrastructure investment and corporate expenditures in core business operations will fuel industry growth moving forward. Notable transactions include:

- Wind Point Partners, a Chicago-based private equity firm, has acquired The Kleinfelder Group, a San Diego-based engineering and professional services company for an undisclosed amount. The partnership will be instrumental in restructuring The Kleinfelder Group’s capital structure and will fuel the path to the next stage of growth with the company’s management team remaining actively involved

- The Carlyle Group, LP (NASDAQ:CG), a global private equity and alternative asset management corporation, has entered into a definitive agreement to acquire Enermech Ltd. from Lime Rock Partners for $577.9 million

Public Comparables¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

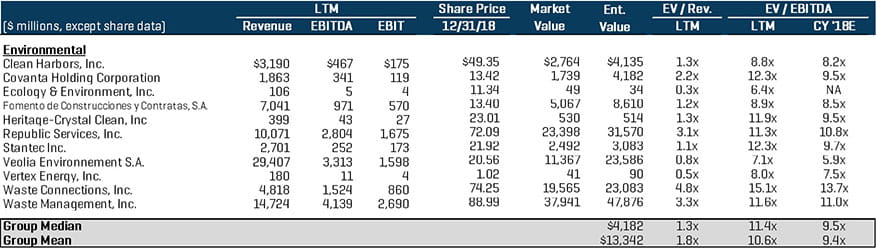

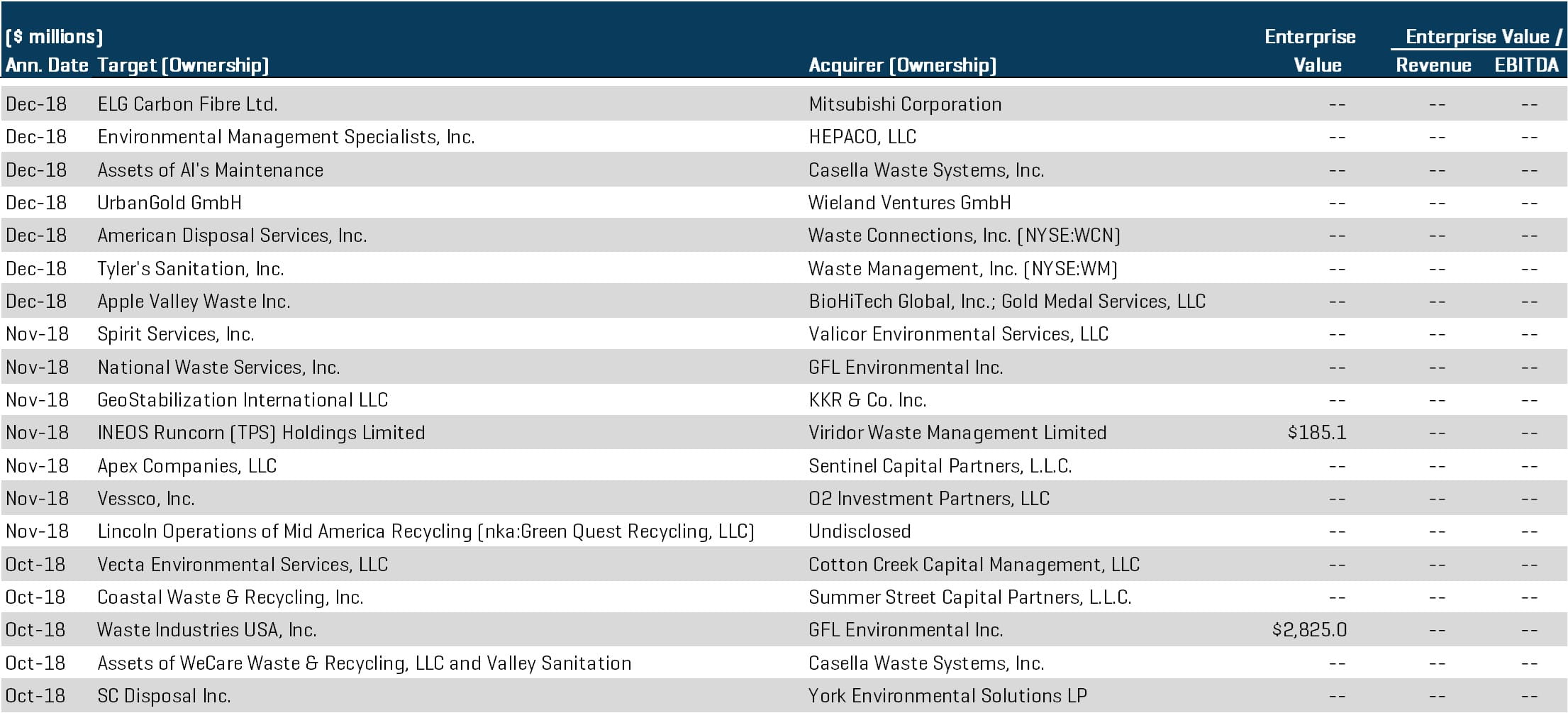

Environmental Services

The environmental services segment saw another quarter of strong M&A volume, led by large strategic players consolidating the industry and private equity firms chasing attractive platform opportunities. Changes in governmental regulation, technological advances, and an increased emphasis on environmental sustainability continue to drive activity in this segment. Notable transactions include:

- Waste Management, Inc.’s (NYSE:WM) acquisition of Tyler’s Sanitation, Inc., an Aiken, S.C.-based residential and commercial waste services provider, is emblematic of Waste Management’s initiative to strengthen regional presence through an acquisitive growth approach

- KKR & Co., Inc., an American multinational private equity firm, has agreed to acquire GeoStabilization International, a leading provider of geotechnical maintenance services, from CAI Capital Partners. The transaction, for an undisclosed amount, will be funded through KKR’s Americas XII Fund

- GFL Environmental Inc., has announced that it has entered into a definitive agreement to merge with Waste Industries USA, Inc. at a total enterprise value of $2.8 billion. The merger will create one of the largest privatelyowned environmental services providers in North America, with operations in nearly all Canadian provinces and in 10 states throughout the U.S.

Public Comparables¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

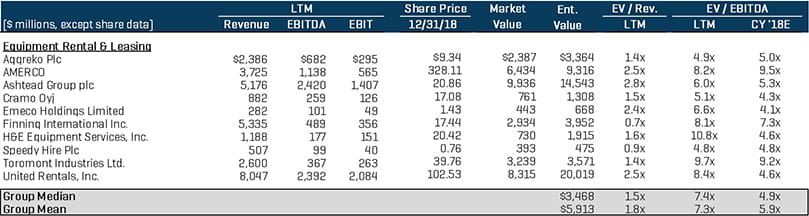

Equipment Rental & Leasing

The equipment rental and leasing segment continued to benefit from strong public strategic buyer activity in the fourth quarter. Private equity firms were also actively making add-on acquisitions and chasing attractive platform investments as a continued shift from equipment ownership to rental and leasing drives transaction volume and interest in the sector. Notable transactions include:

- Kadant Inc. (NYSE:KAI) announced that it has completed its acquisition of Syntron Material Handling Group, LLC, a leading provider of material handling equipment to a variety of process industries, from Levine Leichtman Capital Partners, in a transaction valued at approximately $179.0 million. The transaction grants Kadant access to new industries and extends the breadth of service offerings for the company

- United Rentals, Inc. (NYSE:URI) has acquired the assets of WesternOne Rentals & Sales LP (a subsidiary of WesternOne, Inc. [TSX:WEQ]) for approximately $91.8 million. The transaction builds upon United Rentals’ presence in Western Canada and expands the company’s regional service offering and fleet size

Public Comparables¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

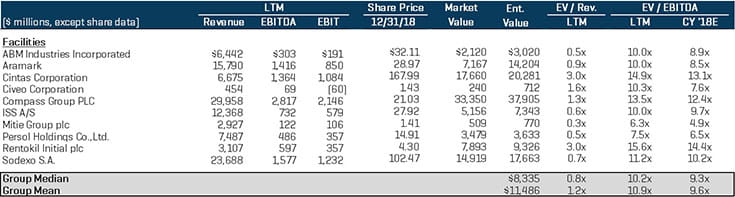

Facilities Services

The facilities services segment continues to see aggressive platform and add-on acquisition activity from financial sponsors, as well as ongoing consolidation from domestic and international strategic acquirers as an emphasis on regulatory compliance and an increasing demand for integrated facility management propels market development. Notable transaction details include:

- NCK Capital has entered into a definitive agreement to acquire Dallas-based City Wide Building Services, LLC, a full-service commercial building maintenance company servicing over 1,500 properties annually. City Wide was previously a portfolio company of Double R Partners

- Cushman & Wakefield (NYSE:CWK), a leading global real estate services firm, has agreed to acquire Quality Solutions, Inc., a premier facilities management firm specializing in on-demand facility maintenance and project management. The transaction will expand Cushman & Wakefield’s facilities management capabilities and geographic coverage across North America

Public Comparables¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

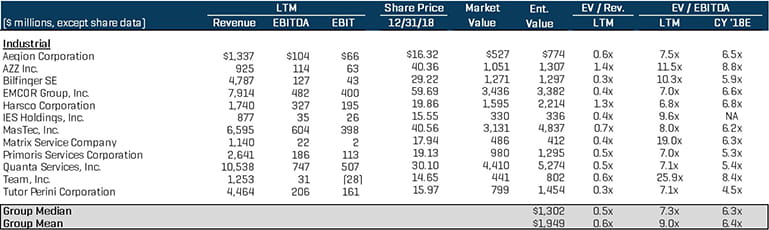

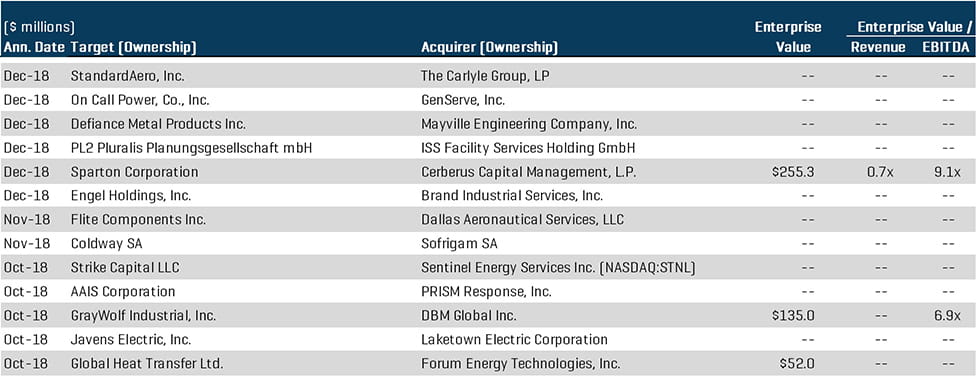

Industrial Services

Industrial services continues to be an attractive segment for private equity buyers making platform acquisitions. Strategic buyers in this segment look to create diversification through a “one-stop-shop” portfolio of service offerings and seek to maximize geographic coverage through an acquisitive approach. Notable transactions include:

- Cerberus Capital Management, L.P., a global leader in alternative investing, has announced that it has acquired Sparton Corporation (NYSE:SPA), a 119-year-old provider of concept development, industrial design, engineering, and field services to the medical, aerospace and defense, and industrial and commercial industries. The financial consideration of $18.50 per share, a 40% premium over the December 11, 2018, share price, equates to an approximate transaction value of $255.3 million

- Sentinel Energy Services, Inc. (NASDAQ:STNL) and Strike Capital, LLC have entered into a definitive merger agreement to form publicly traded Strike Inc. The combined entity will represent one of the largest facilities infrastructure, integrity, and industrial services providers across the U.S., with a total enterprise value estimated at approximately $854 million

Public Comparables¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

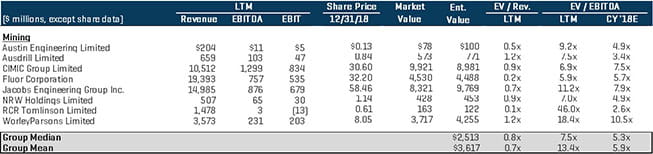

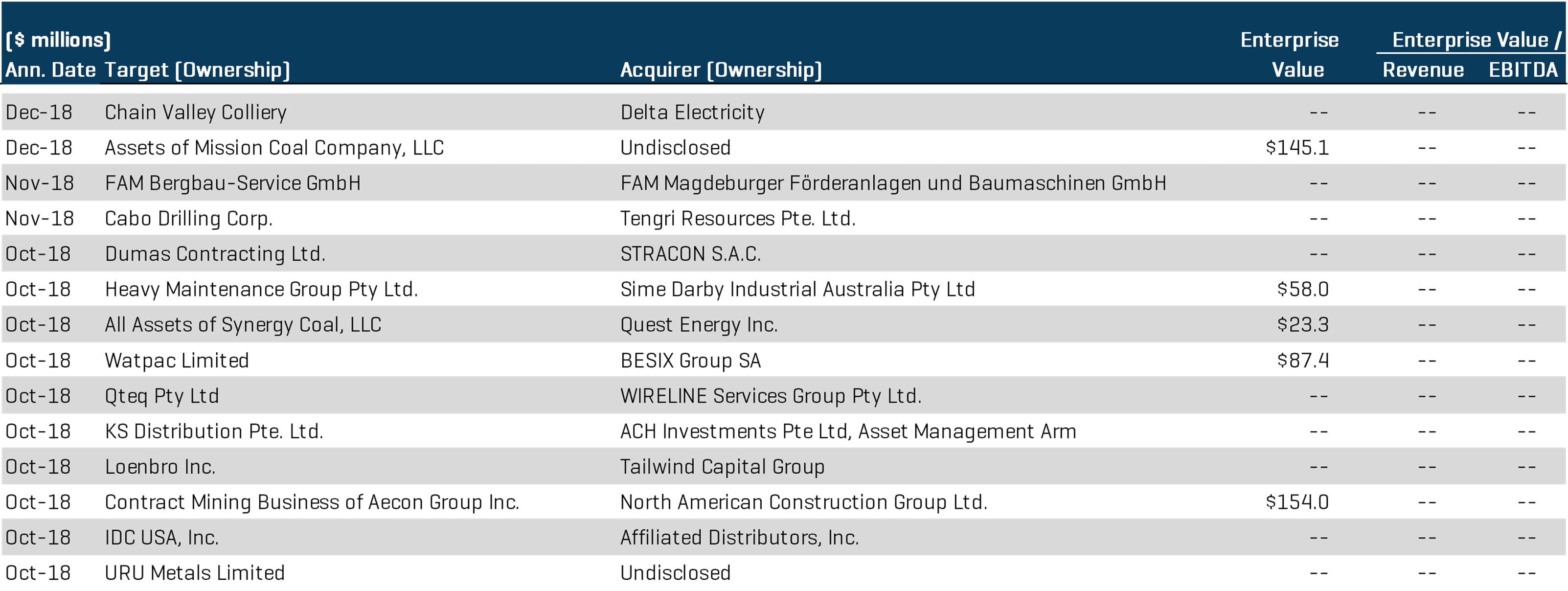

Mining Services

International M&A activity remained a key driver for continued consolidation in the mining services industry in the fourth quarter. The mining services industry continues to experience intense competition, pushing companies to gain a competitive edge by gaining access to attractive geographical regions and key projects. Notable transactions include:

- BESIX Group SA has announced the completion of a majority takeover offer for all remaining outstanding shares of Watpac Ltd., an Australian mining services contracting company. The transaction included the acquisition of the remaining 71.9% stake in Watpac at a valuation of approximately $87.4 million

- North American Construction Group has entered into an agreement to acquire the Contract Mining Business of Aecon Group Inc. in an all-cash transaction valued at approximately $154.0 million. Included in the purchase of the mining services business is earth-moving equipment, light construction assets, support equipment, and maintenance facilities

Public Comparables¹

Select M&A Transactions

(1) Multiples above 20x are excluded from the mean/median calculation

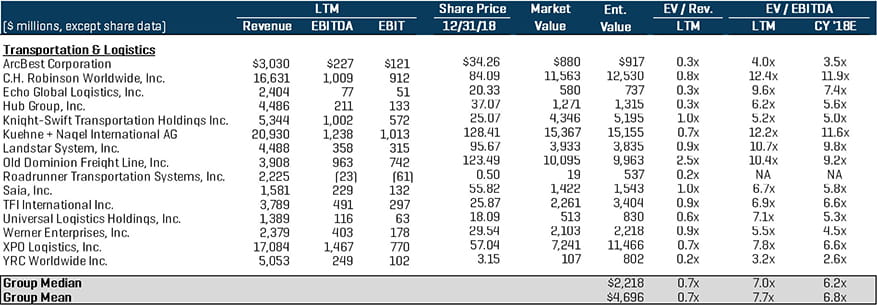

Transportation & Logistics

Transportation and logistics M&A activity in the fourth quarter of 2018 remained robust as digital transformation and positive end market dynamics, such as the evolution of the automotive aftermarket industry, propels transaction volume. Activity in the segment continues to be vigorous as private equity firms pursue attractive opportunities with cutting-edge logistics providers and large public strategic buyers tap into new geographies and aim to expand service offerings through enhanced technological innovation. Notable transactions include:

- Universal Logistics Holdings (NASDAQ:ULH), a leading provider of customized transportation and logistics solutions, announced its acquisition of Specialized Rail Service, Inc. (SRS) for approximately $12.3 million. The transaction includes the acquisition of SRS’ facilities in Clearfield, UT and Las Vegas, NV and expands upon the company’s service capabilities and geographic coverage

- CMA CGA S.A., the third-largest container shipping company in the world and headquartered in France, has announced that it has acquired CEVA Logistics (SWX:CEVA), a global third-party logistics services provider based in the Netherlands, in a transaction valued at approximately $2.95 billion

Public Comparables¹

Select M&A Transactions