English

English

1H 2018 Metal Prices and Demand Spur M&A Activity

Strength in metals prices (supported by Section 232 tariffs and other trade restrictions), solid end-market demand, and a robust M&A market have ignited transaction activity in the metals supply chain. Scrap processors, steel mills, and metal service centers in particular are taking advantage of robust market conditions to pursue both organic (e.g., restarts and expansions) and M&A growth opportunities. How long will the party last? In the near term, metals market conditions will be dictated by trade policy decisions, economic conditions in foreign industrialized regions, and domestic supply constraints (namely labor and freight).

Key Takeaways:

- North American metal suppliers have experienced a surge in M&A activity during the first half of 2018, led by scrap processors, steel mills and metal service centers

- With balance sheets bolstered by robust pricing and demand, strategic buyers have led the majority of transactions so far this year

- Overall valuations have moderated for the public companies in Stout’s proprietary metal supplier indices, as stronger earnings in 2018 have been met with relatively flat share price performance

- Domestic metal prices have generally benefited from trade protections and solid end-market demand, however, disparities prevail – steel, aluminum, copper and other metals industry participants face varying supply/demand and foreign trade dynamics

Metal Pricing

Domestic metal prices have generally benefitted from Section 232 tariffs and sanctions, while spreads among finished products and scrap grades continue to fluctuate with disparate foreign trade actions. During second-quarter earnings announcements, executives for publicly traded service centers that sell a wide variety of metals communicated expectations of stabilizing prices in the near term. However, carbon steel suppliers face supply/demand dynamics that can differ meaningfully from aluminum, copper, and specialty producers as well as scrap suppliers.

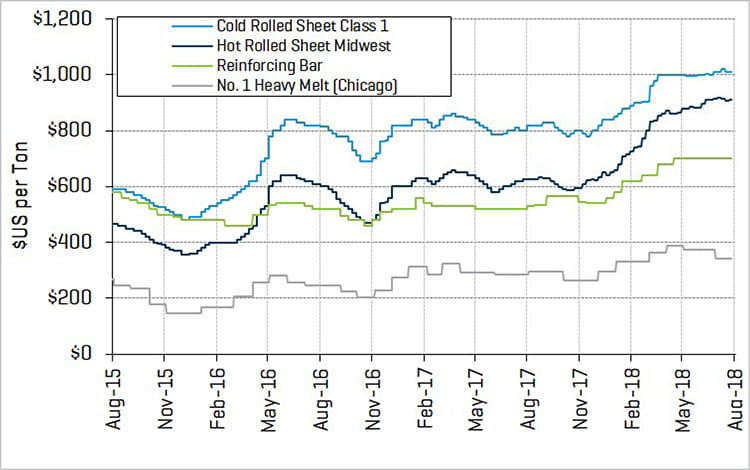

Steel Prices

Source: American Metal Market

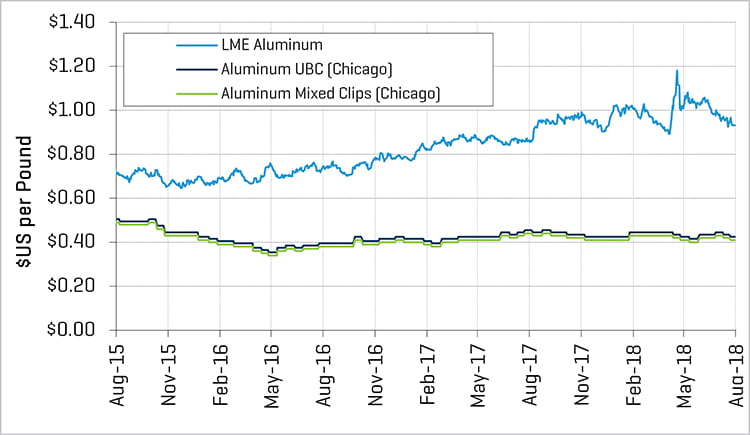

Aluminum Prices

Source: American Metal Market

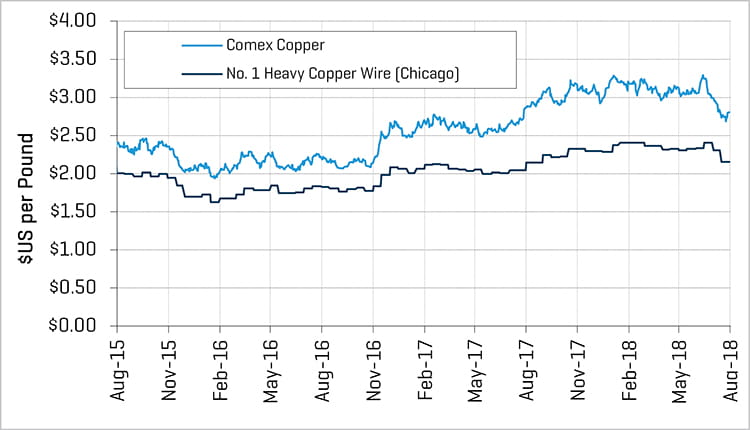

Copper Prices

Source: American Metal Market

PUBLIC COMPANY PERFORMANCE

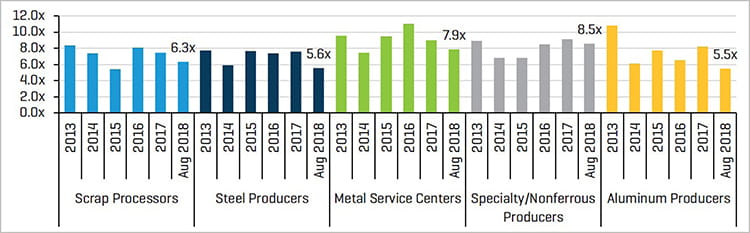

North American metal suppliers’ latest-12-month (LTM) EBITDA margins have benefited from recent global metals price increases and robust demand. Forward EBITDA multiples, however, retracted from previous year levels as valuations haven’t kept pace with EBITDA growth amid investor uncertainty around metals prices and foreign trade conditions.

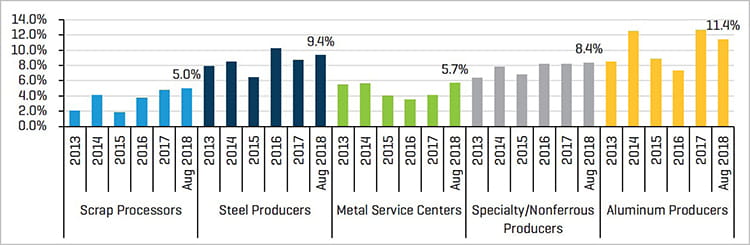

Public Companies: LTM EBITDA Margins

Source: Capital IQ and Stout Research

Public Companies: Forward EBITDA Multiples

Source: Capital IQ and Stout Research

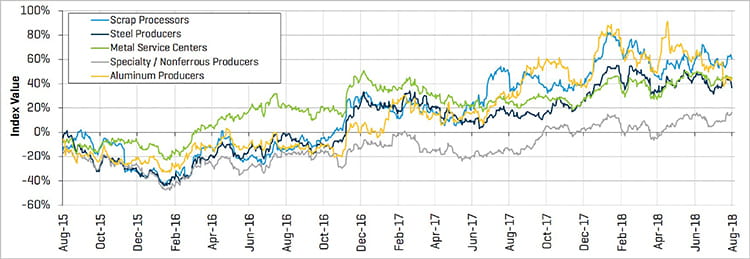

Public company share price performance within Stout’s proprietary metal supplier indices have generally fared well over the past three years, led by aluminum producers, scrap proccesors, metal service centers, and steel producers. Specialty/nonferrous producers' share prices have lagged other metals subsectors but have recovered and are slightly above 2015 levels.

Public Companies: Relative Share Price Performance

Source: Capital IQ and Stout Research

M&A ACTIVITY

M&A activity among metal suppliers has increased significantly in 2018 due to rising metals prices, strong demand and favorable M&A and financing markets. Numerous steel mills changed hands as some producers looked to exit North American positions, while consolidation continues in the metal service center sector. Notable transactions include:

- Commercial Metals Company (NYSE:CMC) announced the acquisition of several steel mill and fabrication assets from Gerdau S.A., providing CMC with an expanded footprint within the largest construction region in the U.S.

- Main Steel, LLC a portfolio company of Peak Rock Capital was acquired by Samuel, Son & Co. expanding their geographic and service capabilities

- Steel Dynamics, Inc. (Nasdaq:STLD) acquired Heartland Steel Processing from Companhia Siderúrgica Nacional (“CSN”), expanding Steel Dynamics’ annual flat roll steel shipping capacity to 8.4 million tons and total steel shipping capability to 12.4 million tons

- JSW Steel Limited acquired hot-rolled steel producer ACERO Junction Inc., the former Wheeling-Pittsburgh Steel mill in Mingo Junction, Ohio

- U.K.-based Liberty House Group closed on the acquisition of ArcelorMittal’s (ENXTAM:MT) idled wire rod mill in Georgetown, SC

- Ryerson Holding Corporation (NYSE:RYI) acquired Chicago-based metal service center Central Steel and Wire Company

- Metal One Corporation of Japan acquired Cargill’s domestic metal service center business

- Novelis Inc. recently announced the acquisition of Aleris Corporation after a deal with China’s Zhongwang fell apart

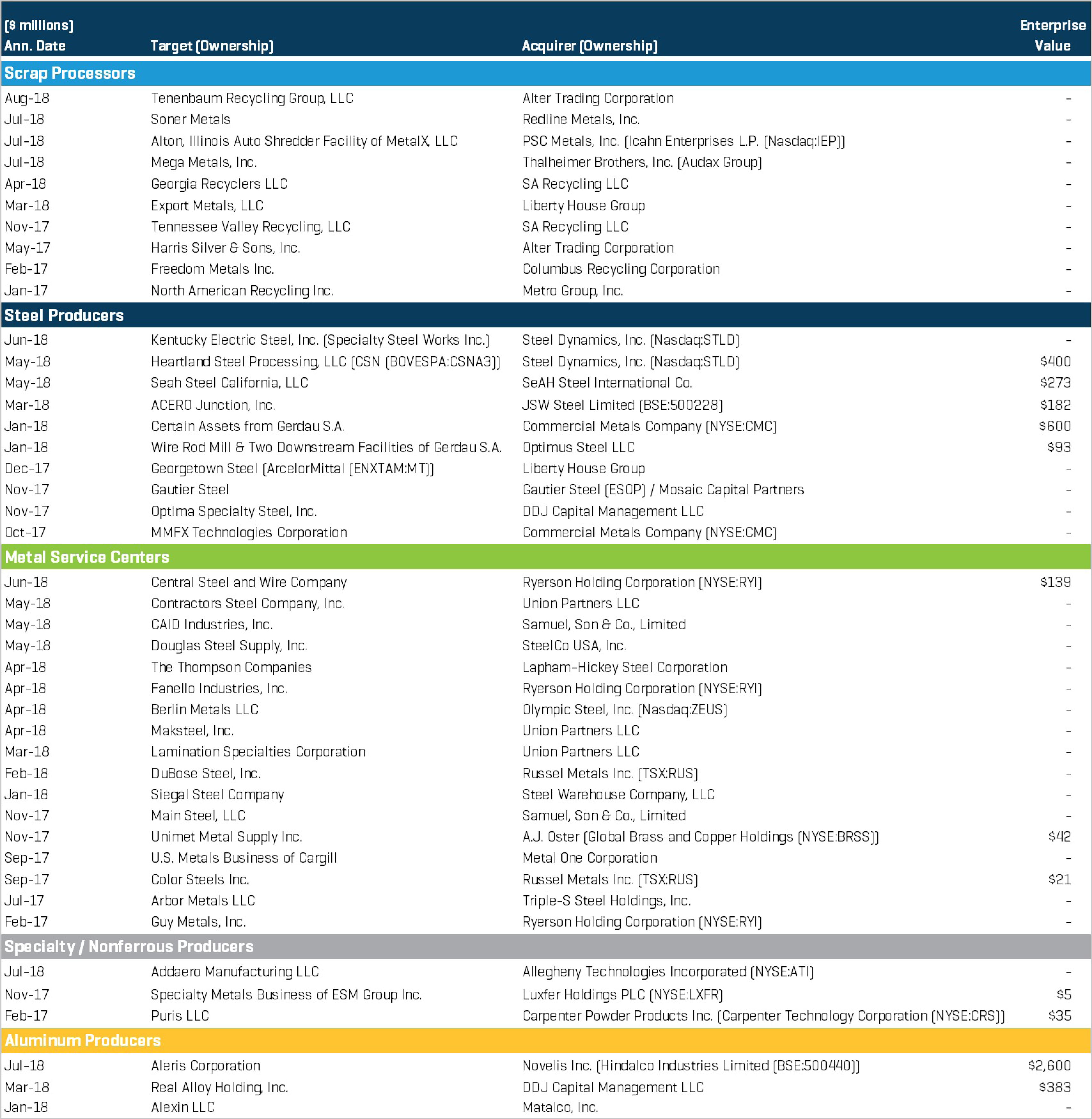

Select Recent Transactions: