English

English

In the second half, industrial supply continued to experience a significant amount of M&A activity driven by both strategic and private equity buyers. Strategic acquirers have been a catalyst for M&A momentum given the need to horizontally integrate into new product offerings and geographic regions. The building and landscape products segment experienced various roll-up transactions, including French building products manufacturer Compagnie de Saint-Gobain S.A.’s proposed bid to expand its presence in the United States with the acquisition of Continental Building Products, Inc. (NYSE:CBPX), while private equity buyers continue to actively pursue new platform and add-on acquisitions to diversify portfolios and grow existing investment capabilities.

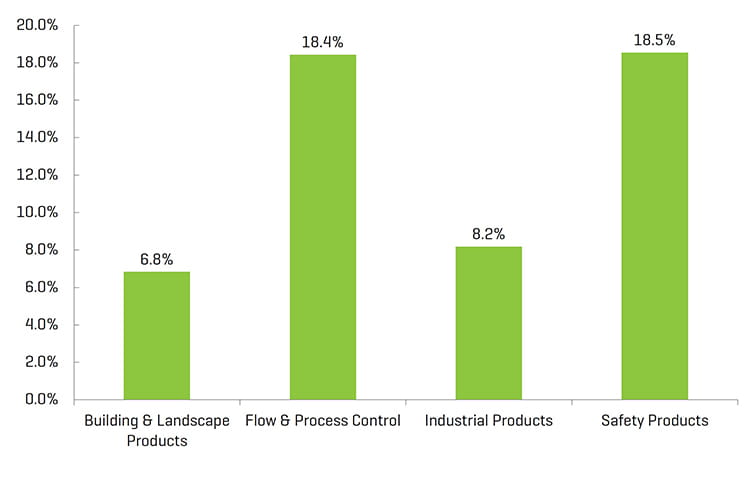

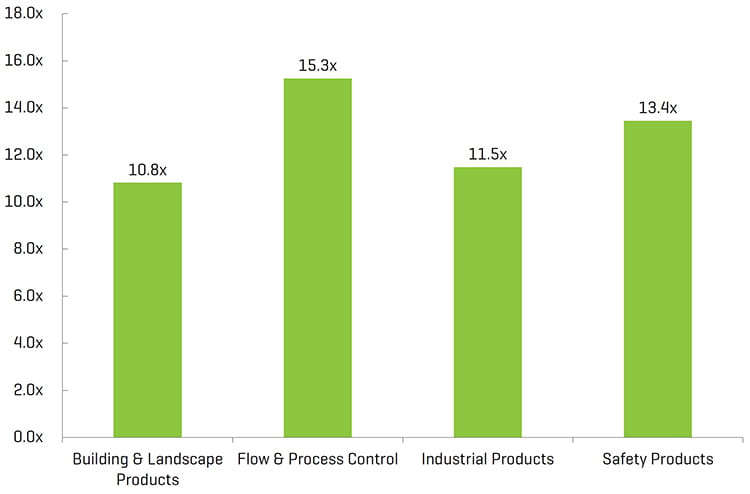

The flow and process control segment continued to boast the highest trading multiples, while the building and landscape products segment was the most active from a M&A volume standpoint. The safety products segment followed the flow and process control segment with the second highest trading multiples, and the industrial products segment showed strength as a multitude of private equity and strategic acquirers continue to be active on both sides of the transaction.

In 2020, we anticipate the industrial supply M&A market will remain robust, driven by continued interest from acquirers looking to act on opportunities to consolidate and diversify current portfolios. Additionally, the industrial supply industry should continue to see growth as a result of an uptick in infrastructure investment, in North American especially, as it relates to upgrading and replacing current structures.

Key Takeaways

- Notable transaction activity from both strategic and private equity buyers, domestically and internationally

- Robust private equity platform and add-on activity points towards a positive M&A market outlook as capital is continually deployed amidst a record overhang

- Strategic buyers continue to pursue acquisitive growth strategies to gain a competitive edge through expanding product and service offerings and/or geographic coverage

- Significant roll-up activity is indicative of continued industry consolidation

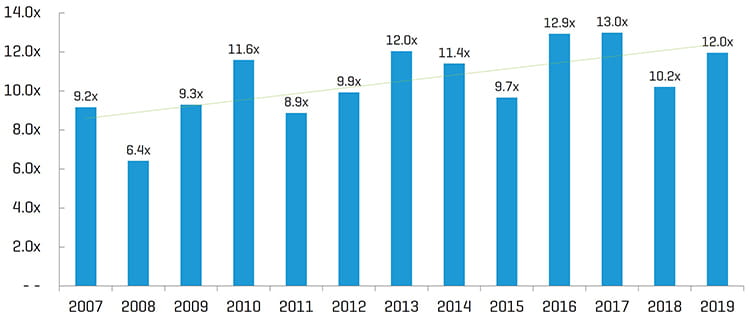

- Transaction multiples increased year over year and remain elevated on a historical basis

Historical Enterprise Value / EBITDA Multiples[1]

(1) Multiples above 20x are excluded from the mean/median calculation; data represents the overall median of all four sub-segment benchmarks presented in this report

Industry Statistics

5-Year Historical Share Price Performance

Operating and Market Performance

LTM EBITDA Margin

Enterprise Value / LTM EBITDA[1,2]

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Median from public comp sets featured in report

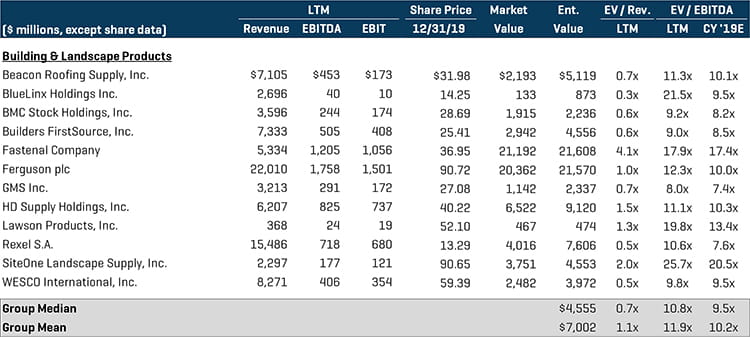

Building & Landscape Products

The building and landscape products segment benefited from significant roll-up activity by strategic buyers, pointing toward continued industry consolidation in 2020. Private equity firms were also highly active in this sector as they continued to pursue platform and add-on acquisitions. Although this segment contained the lowest EV / EBITDA multiples across the industrial supply spectrum, the segment experienced the most transaction activity in the second half. Notable transactions included:

- Compagnie de Saint-Gobain S.A. (ENXTPA:SGO), a leading global manufacturer of materials for building, transport, and infrastructure applications, acquired Continental Building Products, Inc. (NYSE:CBPX), a manufacturer of gypsum wallboard and complementary finishing products, for approximately $1.4 billion. The definitive agreement was announced in November, and the transaction closed during the first quarter of 2020

- The Blackstone Group, Inc. (NYSE:BX), a multinational private equity, alternative asset management, and financial services firm, has acquired the Europe distribution business of CRH plc (ISE:CRG) for approximately $1.9 billion. CRH manufactures and supplies a diverse range of building materials and products for use in construction, infrastructure, and housing projects, among others

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

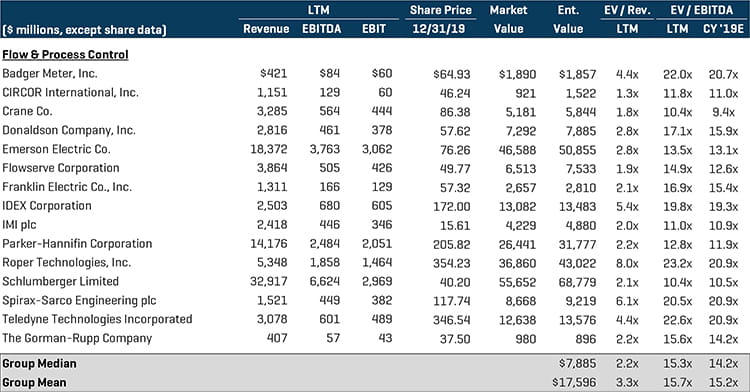

Flow & Process Control

Following the trend of previous periods, the flow and process control segment produced the highest EV / EBITDA trading multiples. The segment continued to experience strong M&A activity, following an active first half, from large public companies looking to expand product, service, and technology offerings as well as geographic coverage. Private equity continues to find attractive investment opportunities in private companies within a fragmented industry. Notable transactions included:

- Inflexion Private Equity Partners has announced an agreement to acquire Aspen Pumps Ltd., a manufacturer of condensate removal pumps and accessories for the HVAC industry, for approximately $271.9 million. The agreement is subject to customary closing procedures and is expected to close during the first quarter of 2020

- SPX Flow, Inc. (NYSE:FLOW), a leading rotating, actuating, and hydraulic technologies provider to the food and beverage, industrial, and energy end markets, announced it has reached an agreement to sell its power and energy businesses to Apollo Global Management, Inc. (NYSE:APO). The transaction is expected to close in the first half of 2020 and would value SPX’s power and energy businesses at approximately $475.0 million

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

(*) Transaction is currently pending

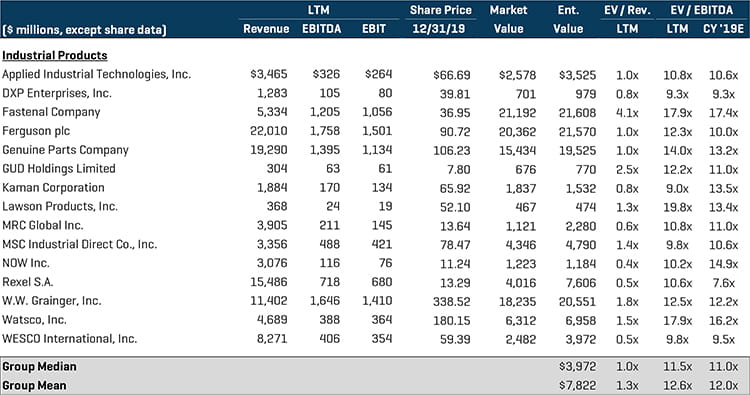

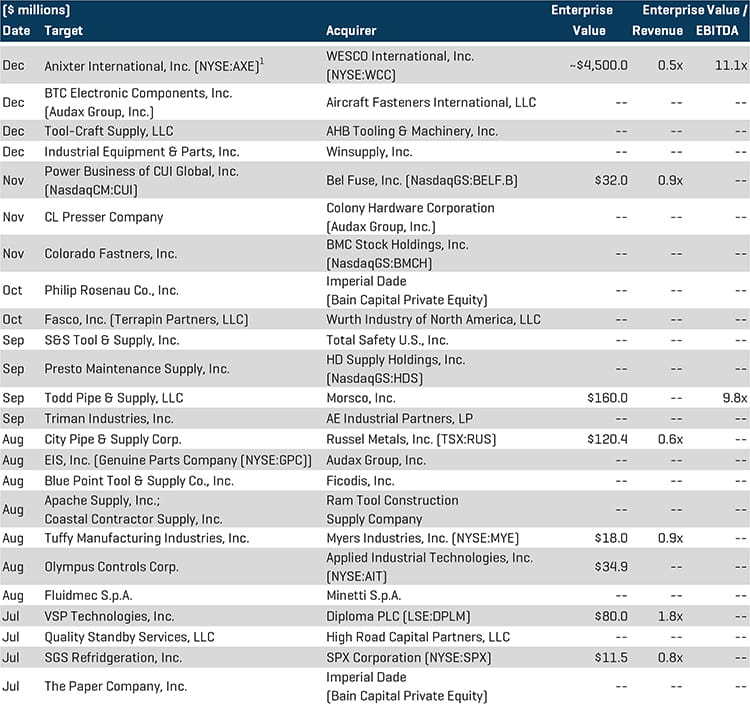

Industrial Products

The industrial products segment continues to exhibit strong M&A activity as private equity firms are seen actively pursuing unique investment opportunities. Consolidation by strategic and private equity buyers, product and volume synergies, diversification, and enhanced distribution networks has historically made this a very action segment. Notable transactions included:

- WESCO International, Inc. (NYSE:WCC), a global distributor of electrical and industrial equipment, has offered to acquire Anixter International, Inc. (NYSE:AXE) for approximately $4.5 billion. Anixter distributes enterprise cabling and utility power solutions, serving contractors, system integrators, architects, and engineers, among others

- City Pipe & Supply Corp., a market-leading distributor of pipes, valves, and fittings, has been acquired by Russel Metals, Inc. (TSX:RUS), a distributor of steel and metal products in North America, for approximately $120.4 million

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions

(1) Transaction is currently pending

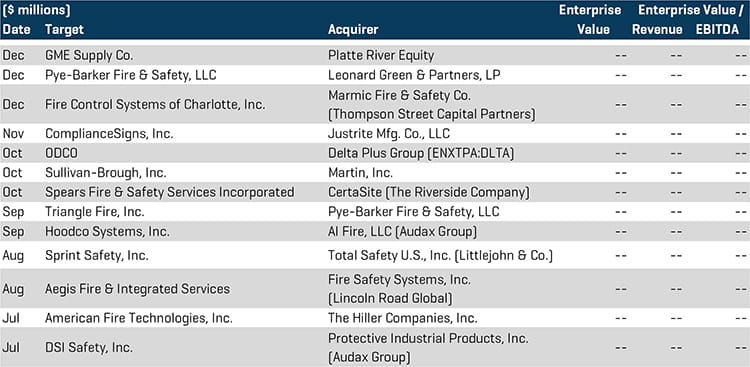

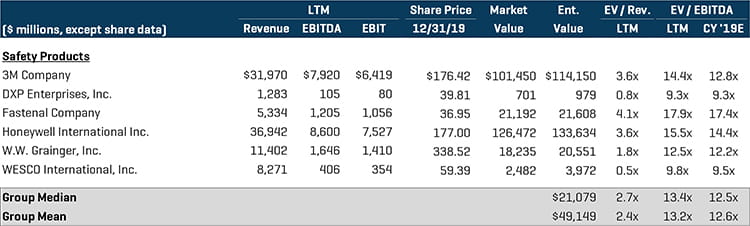

Safety Products

Safety products segment M&A activity was driven predominantly by private equity buyers looking to invest in both platform and add-on investments to increase geographic coverage during the second half. Notable transactions included:

- Sullivan-Brough, Inc., doing business as SafetyWear, has been acquired by Martin, Inc., a maintenance and repair solutions provider for the industrial and construction markets. This acquisition enables Martin to expand its E-catelog as well as penetrate new wearable safety product categories

- The Hiller Companies, Inc., a leading designer and supplier of fire protection products, has agreed to acquire American Fire Technologies, Inc. American Fire Technologies specializes in the integration of fire protection and detection management systems for the commercial, governmental, and utilities industries, among others

Public Comparables[1]

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions