English

English

In the first quarter, industrial supply experienced significant roll-up and consolidation activity driven by both strategic and private equity buyers looking to diversify into new geographic regions and expanding product and service offerings. Despite industrial supply’s robust momentum heading into the second quarter, COVID-19 materially impacted the industry, causing M&A volumes to plummet as capital spending was put on pause.

Although LTM EBITDA margins were slightly down across the board as compared to last year for industrial supply participants, overall valuations are expected to slightly increase year-over-year, given the industry’s largely “essential” status particularly in feeding similarly essential industrial service companies and key end markets such as construction and contracting, homebuilding, and infrastructure, among others.

Toward the end of the first half, and into the third quarter, we are seeing a rebound in industrial supply as the economy reopens with large projects re-starting or ramping up, new projects coming on-line, and the federal government continuing to respond in aiding investment resulting from the COVID-19 pandemic.

Key Takeaways

- Industrial supply, in general, outperformed many sectors of the economy during COVID-19

- First quarter strategic and private equity roll-up M&A activity indicates ripe asset pool for the second half

- Despite lagging operational performance, valuations are expected to remain stable

- Uncertain macroeconomic trends to continue with evolution of global pandemic and response from federal government

- “Essential” businesses which performed well during COVID-19 period will be even more sought after as clarity returns to the forecast period

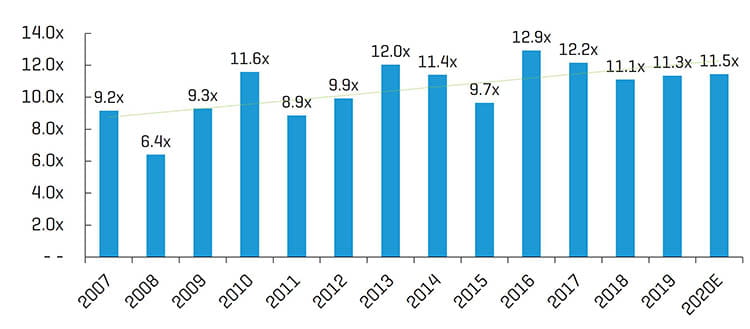

HISTORICAL ENTERPRISE VALUE / EBITDA MULTIPLES1

(1) Multiples above 20x are excluded from the mean/median calculation; data represents the overall median of all nine sub-segment benchmarks presented in this report

Industry Statistics

5 – YEAR HISTORICAL PRICE PERFORMANCE

Operating and Market Performance

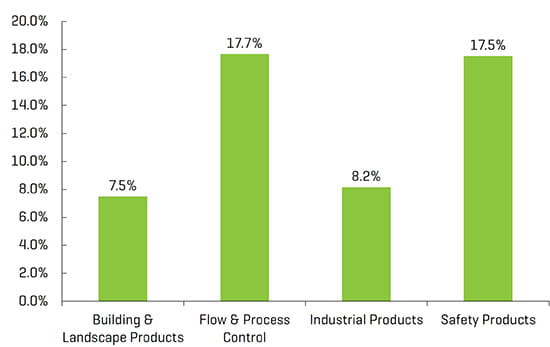

LTM EBITDA MARGIN

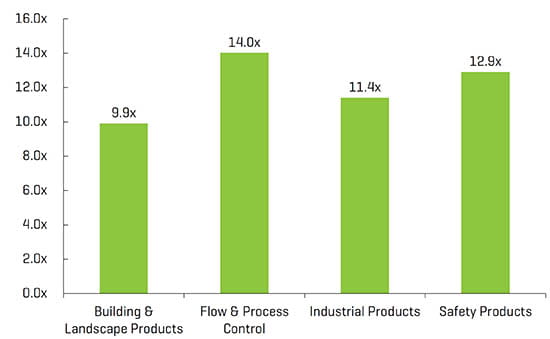

ENTERPRISE VALUE / LTM EBITDA1,2

(1) Multiples above 20x are excluded from the mean/median calculation

(2) Median from public comp sets featured in report

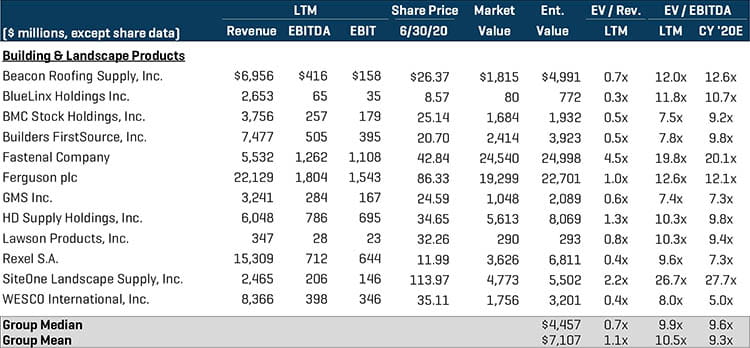

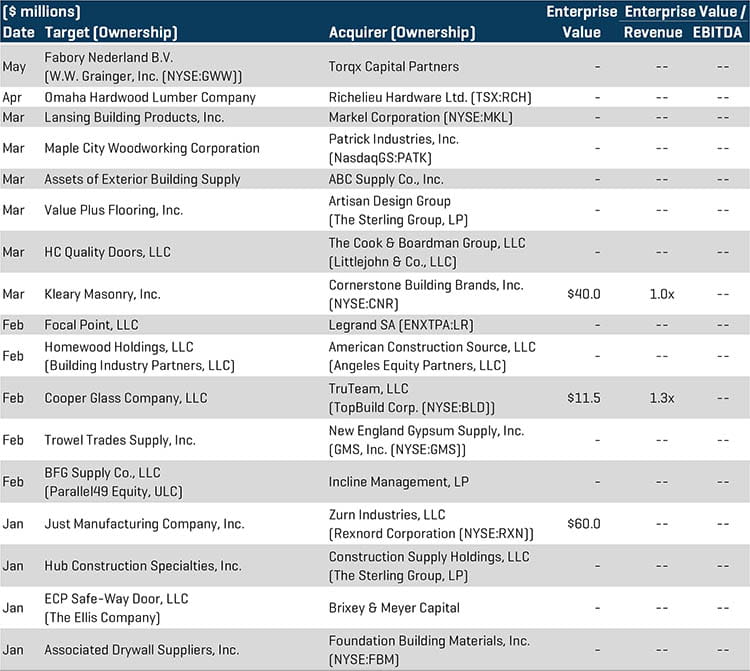

Building & Landscape Products

The building and landscape products segment continued to be the most active segment in terms of M&A activity as evidenced by continued industry consolidation driven by strategic and hybrid buyers. The segment’s M&A activity is largely driven by acquirers pursuing differentiated assets in an environment with many potential targets. With the current state of digital transformation varying widely across all aspects of the building & landscape industry’s value chain, many of the segment’s participants will continue to expand and innovate their product and service offerings in order to stay ahead of the curve. Notable transactions include:

- Just Manufacturing Company, Inc. was acquired by Zurn Industries, LLC, a subsidiary of Rexnord Corp, (NYSE:RXN), for approximately $60.0 million in January. Just Manufacturing manufactures and supplies stainless steel plumbing fixtures for heavy and light commercial projects. This acquisition partners two market leaders in the commercial and industrial stainless-steel sink market, allowing the combined entity, which will continue to operate as a subsidiary of Rexnord, to deliver a more robust lineup of finished plumbing content to new and existing buildings.

- Cornerstone Building Brands, Inc. (NYSE:CNR), a designer and manufacturer of external building products, has acquired Kleary Masonry, Inc. for approximately $40.0 million. Kleary provides stone veneer solutions and is headquartered in California. This acquisition for Cornerstone expands the company’s value-added, turnkey stone veneer solutions, enabling the building products provider to capitalize on one of the fastest-growing segments within the residential cladding market.

PUBLIC COMPARABLES1

(1) Multiples above 20x are excluded from the mean/median calculation

SELECT M&A TRANSACTIONS

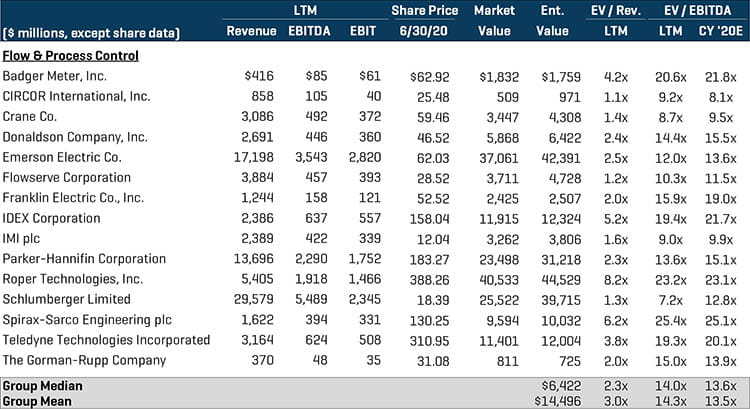

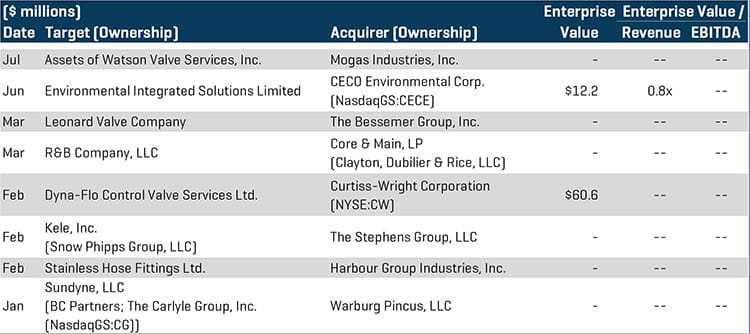

Flow & Process Control

The flow and process control segment finished the first half trading at the highest overall multiple among its industrial supply peers. Despite the diminished M&A volume during the second quarter, private equity buyers continued to find attractive investment opportunities within the highly fragmented industry. With renewed light cast upon the topic of highly sustainable and health-conscious flow and process practices, strategic and hybrid buyers will look to refine their future growth initiatives as a result of COVID-19. Notable transactions include:

- Curtiss-Wright Corporation (NYSE:CW), a designer and manufacturer of engineered products for the aerospace and defense industry, has acquired Dyna-Flo Control Valve Services Ltd. for approximately $60.5 million. Dyna-Flo manufactures and supplies linear and rotary control valves, actuators, and pressure control systems for various end markets. Curtiss-Wright’s investment is expected to be accretive to the company’s 2020 adjusted diluted earnings per share and will yield significant opportunities for growth within the company’s diverse industrial valve portfolio.

- Sundyne, LLC, a supplier of industrial pumps and compressors, has been acquired by Warburg Pincus, LLC. Warburg, a private equity firm based in New York, will look to implement its resources and expertise in the energy and industrials industries and build upon Sundyne’s highly regarded and reliable reputation in the mission critical flow control equipment market.

PUBLIC COMPARABLES1

(1) Multiples above 20x are excluded from the mean/median calculation

SELECT M&A TRANSACTIONS

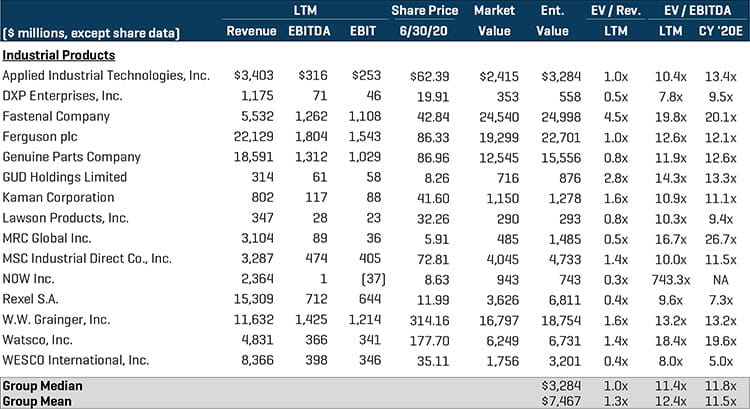

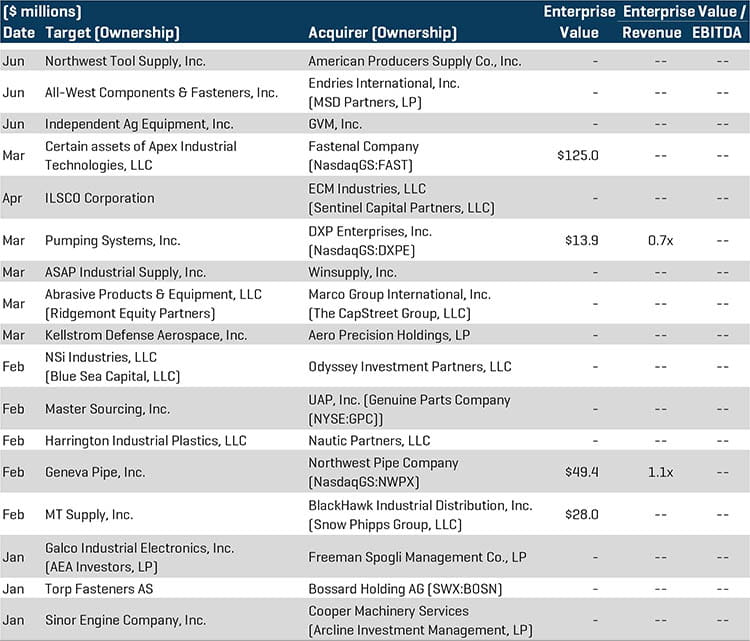

Industrial Products

The industrial products segment continued to trade at a double-digit multiple despite having single-digit LTM EBITDA margins. The segment continued to exhibit strong M&A activity, given the circumstances surrounding the pandemic, as both strategic and private equity buyers pursued unique investment opportunities. As optimism around infrastructure spending post-COVID continues to mount as part of one or more stimulus packages, industrial product suppliers will remain of high interest to various types of potential investors. Notable transactions include:

- Certain Assets of Apex Industrial Technologies, Inc., including Apex’s industrial supply distribution business, has been acquired by Fastenal Company (NasdaqGS:FAST) for approximately $125.0 million. Fastenal, a wholesale distributor of industrial and construction supplies, will look to expand upon the entities’ established relationship within the industrial and commercial supply chains and offer more than 105,000 product dispensing and leased devices across 25 countries.

- Northwest Pipe Company (NasdaqGS:NWPX), a manufacturer and supplier of engineered steel pipe systems, has acquired Geneva Pipe, Inc. for approximately $49.4 million. Geneva Pipe, founded in 1956, provides concrete pipes and precast products. This transaction for Northwest marks the company’s largest acquisition to date and provides Northwest a significant boost in the precast concrete products category given Geneva’s expertise in storm drains, manholes, and catch basins.

PUBLIC COMPARABLES1

(1) Multiples above 20x are excluded from the mean/median calculation

SELECT M&A TRANSACTIONS

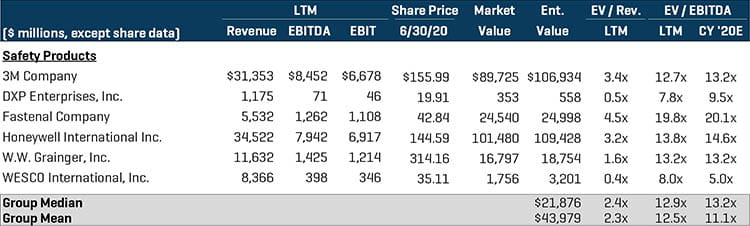

Safety Products

The safety products segment finished the first half trading at the second-highest overall multiple among its industrial supply peers due in large part to the “essential” nature of the segment’s products and relatively steady demand throughout the second quarter. Although M&A activity within the safety products segment was down year-over-year, the segment is poised for renewed interest in the second half as a result of its out-performance during COVID-19. Notable transactions include:

- Gruppo Sicura S.r.l., an Italian manufacturer and supplier of fire protection products, has been acquired by Argos Wityu Partners S.A., a private equity firm based in Paris, for approximately $59.1 million. The private equity firm will look to expand Gruppo Sicura’s established reputation in the safety products market by partnering with the company’s highly motivated and experienced management team with defined strategic goals.

- Carlson Private Capital Partners, a private equity firm based in Minnesota, acquired Street Smart Rental, Inc., a distributor of traffic control and safety products serving various traffic control companies, government agencies, and general contractors. Carlson looks to build upon Street Smart’s established business model, and the investment will enable the private equity firm to expand into new regions, while bolstering the technology and service capabilities of the firm’s overall portfolio.

PUBLIC COMPARABLES1

(1) Multiples above 20x are excluded from the mean/median calculation

SELECT M&A TRANSACTIONS