English

English

The S&P 500 gained 8.5% during the fourth quarter of 2019, while the Healthcare Services and Life Sciences equities that we track in this report performed well during the quarter, increasing 12.5%. The S&P 500 was up 28.8% for 2019, with the mean Stout Healthcare Universe stock price up 19.2% during the same period.

Biotech (+24.8%), Molecular Diagnostics/Tools/Reagents (+31.1%), Medical Devices and Hospital Supplies (+27.9%), and Healthcare Information Technology (+22.5%) all had a strong showing. There are not enough public pure-play physician practice management companies to gauge that sectors performance, but we would note that UnitedHealth Group’s stock price was up 18.4% in 2019.

Specialty Pharmaceuticals and Skilled Nursing Facilities were the two sectors to report stock price declines in 2019, off 5.5% and 1.4%, respectively. This is no surprise with the opioid crisis-related lawsuit overhang, pressure from pharmacy benefit managers (PBMs), and competition impacting specialty pharma. Skilled Nursing has been hurt by the poor performance of a number of public companies that have not managed debt, mix, or reimbursement and cost management strategy well.

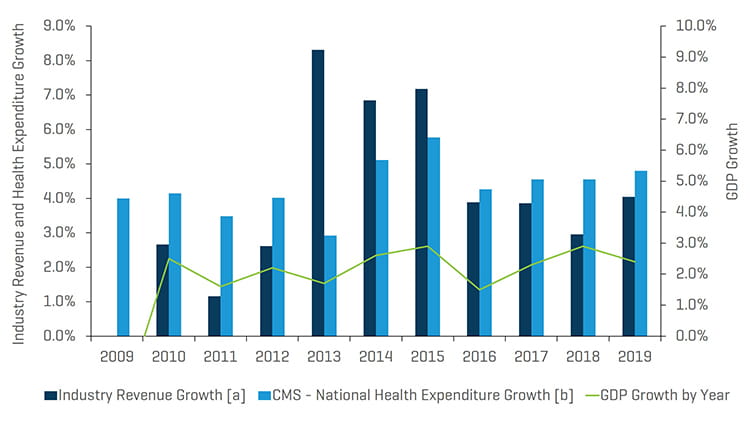

As shown in the chart below, Stout’s Healthcare Universe of companies saw revenue grow 4.4% in 2019, which was above with GDP growth.

Historical Revenue Growth of Segments Monitored by Stout Vs. Annual Health Expenditures and GDP Growth

Notes:

[a] For each period, total revenue figures are derived from the sum of all comparable companies listed in the appendix (Healthcare Public Company Analysis).

[b] CMS tracks National Health Expenditure Accounts (NHEA), which are the official estimates of total health care spending in the United States annually.

Source: www.cms.gov, Historical and Projected NHEA tables.

M&A Market Key Takeaways:

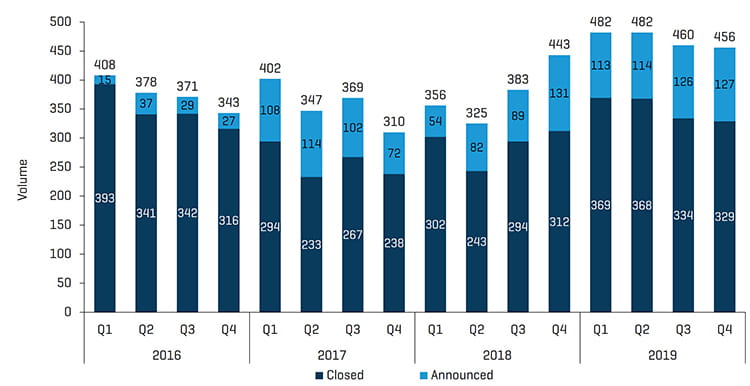

- M&A activity continues to be robust in healthcare. Transaction volume in the fourth quarter was 456 transactions announced and/or closed, a slight increase from the 2018 fourth-quarter volume of 443 transactions, but below the record highs of 482 in the each of the first two quarters of this year. Overall transaction value of deals announced and/or closed in the 2019 fourth quarter came in at more than $64 billion compared with the previous year’s $42 billion. But we would note that the absence of mega mergers being either announced or closed in the period, such as some of the big pharma deals announced and or closed in the first half of 2019, resulted in transaction value dropping from the $133 billion level seen in the second quarter of 2019. We would also mention that enterprise values are not reported for many private transactions, so total number of transactions is a more reliable metric. On the flip side, the largest transactions will generally involve a public buyer.

- We saw some interesting changes in where the activity occurred that we discuss below. Announced deals of 127 in the fourth quarter of 2019, versus 131 in the fourth quarter of 2018, was the second-highest level of activity in at least the last 16 quarters, and deals announced and/or closed (the two combined) in each quarter of 2019 exceeded the year earlier quarter. In the first three quarters of 2019, announced deals exceeded the respective year earlier quarter, so this implies that activity should hold at 2019 levels this year unless the elections or a sudden change in monetary policy impact seller behavior. There is also the possibility that sellers were racing to exit before the elections, in which case we suppose that announced deals post-election could fall off. A change in the political regime could also have an impact to the extent that it impacts interest rates, tax rates, or regulates healthcare or healthcare merger activity in other ways, such as Bernie Sanders’ Healthcare for All or Elizabeth Warren’s rhetoric about private equity debt obligations.

- The total of deals announced and closed in 2019 was 1,880, a 19.7% increase over 1,507 in 2018. Total transaction value of deals announced and/or closed was $400 billion in 2019, up 64.7% due to the large pharma mergers announced and/or closed in the first two quarters of the year.

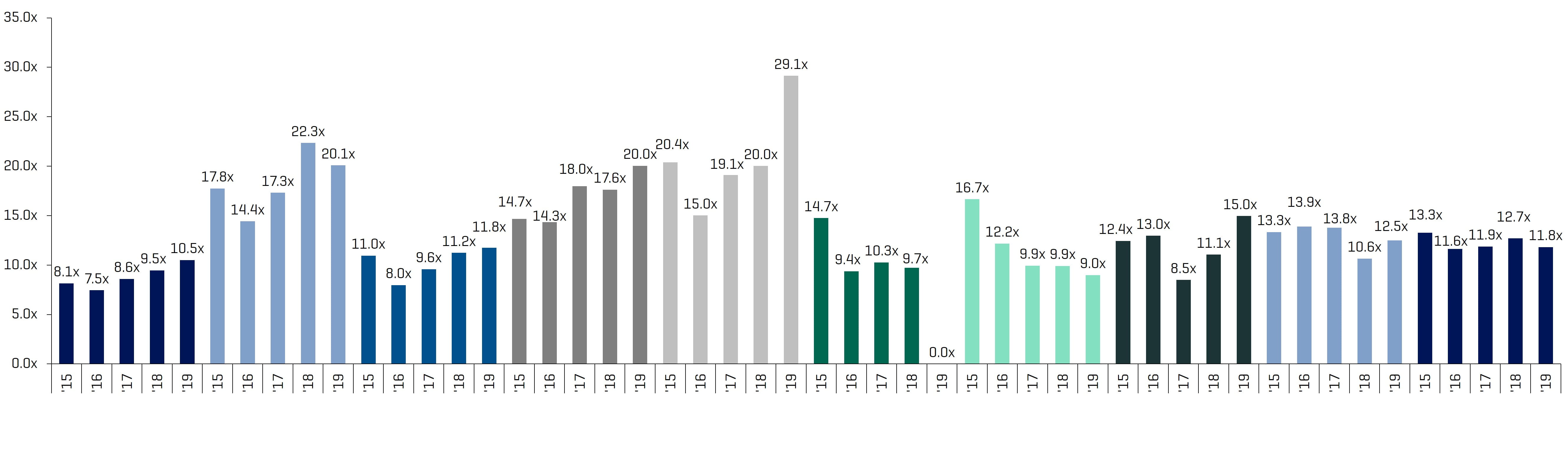

- Enterprise Value to EBITDA multiples for the publicly traded sectors in this report continued to climb in 2019 for Hospitals, Behavioral Health Companies, Molecular Diagnostics / Clinical Labs / Tools, Medical Device and Hospital Supplies and Skilled Nursing Facilities (see analysis in the tables below.)

Analysis of Healthcare Sub-Sector M&A Activity, Observations and Trends

United Optum seems to be making a run at taking over the healthcare world. One interesting trend that we have been observing in healthcare M&A has been United OptumRx’s acquisition of Specialty Pharma distributors Avella Specialty Pharmacy and Diplomat Pharmacy, presumably to lower their pharmaceutical costs and capture the drug margin. These Specialty Pharmacy distributors manage distribution of expensive drugs for patients with complex diseases. United also recently acquired Genoa Healthcare, a specialty pharmacy company that offers telepsychiatry services and medication management for behavioral health patients. That acquisition added 435 pharmacy locations to the insurer’s PBM OptumRx.

They have also been buying physician practices such as Davita Medical Group to build their physician network to increase their appeal to employer groups and once again to control costs and improve margin, hopefully while improving quality of care, as well.

United has also been focused on more value-based care arrangements (fee for performance as opposed to fee for service) with these contracts accounting for an estimated half of their volume.

Consolidation of the Physician Practice Management sector continued to be robust with 75 deals announced/closed in the fourth quarter, up from 60 in the year-earlier quarter. This is also up from 57 deals in the third quarter of 2019. FFL backed Eyecare Partners, one of the largest ophthalmology and optometry practices in the U.S., has been reportedly acquired for $2.2 billion by Partners Group and Ophthalmology continues to be a hot sector. Activity in PPM continues to be across the board with many add-ons in the quarter across many different sub-specialties, including dermatology, dental, fertility, urology, urgent care and other areas.

Pharmaceuticals / Biotechnology realized a noticeable increase in deal flow increasing to 77 in the fourth quarter of 2019 compared with 62 the fourth quarter of 2018 and 54 in the third quarter of 2019. Nine of the largest deals in fourth quarter were Pharma and Biotech deals, and these deals accounted for 70% of those deals with reported values. The largest deal in the quarter was International Flavors and Fragrances buying the Nutrition and Biosciences business of DuPont for $26.2 billion. Novartis also acquired the Medicines Company for $9.5 billion, while Roche, Sanofi, Astellas and Merck remain active buyers, as well. The acquisition activity has spread across therapeutic areas, including cardiovascular disease, oncology, rare diseases, diseases of the eye such as AMD, etc. Between the Trump Administration rhetoric about the cost of drugs being higher in the U.S. than neighboring countries or Democratic candidates pointing to the high cost of insulin and other medications, the pressure on the pharma industry will continue. Big Pharma still needs pipeline and will continue to acquire. On the Pharmaceutical Contract manufacturing side Enhanced Healthcare acquired Pharmaceutical Associates.

Skilled Nursing and Senior Housing continue to report high levels of activity. There were 54 Skilled Nursing/Senior Housing deals in the quarter versus 43 in the year-earlier quarter, but this was off from 69 in the third quarter of 2019. Nonetheless, we think that M&A activity in this sector will continue to come in above normalized levels given that valuations have increased in the private transactions and changes in reimbursement that make it more complex for smaller operators to compete and operate profitably.

Medical device and supply transactions came in at 26 in the quarter and were down from 39 a year ago. It does appear that M&A activity has slowed a bit here, and we did not see a lot of large deals in the fourth quarter. Cynosure was acquired by CD&R. There appears to be a limited number of compelling add-ons right now, with the exception of the OEM manufacturing side where we do expect to see continued consolidation, which seemed apparent from our recent conversations at the MD&M West Conference.

Diagnostics / Tools / Clinical Labs remained flat at 36 in the fourth quarter compared with 36 in the previous quarter and 35 a year ago. We think that Precision Medicine/personalized diagnostics will continue to drive significant growth in this sub-sector in the future as Artificial Intelligence and greater computing power and algorithms drive better matching of a patient’s genetic profile to the right targeted therapeutics.

Healthcare Information Technology saw 49 transactions in the quarter versus 55 a year ago and 60 in the prior quarter. We think that growth here will continue in areas like revenue cycle management, electronic medical records, coding and billing, patient scheduling, AI, cloud-based storage, asset management and tracking, and other areas with there being a perennial state of reimbursement and regulatory changes in healthcare.

Q4 2019 M&A Transactions: Volume and Value

Source: Source: S&P Capital IQ and Stout Industry Research

Historical M&A Transactions: Announced vs. Closed

Source: S&P Capital IQ and Stout Industry Research

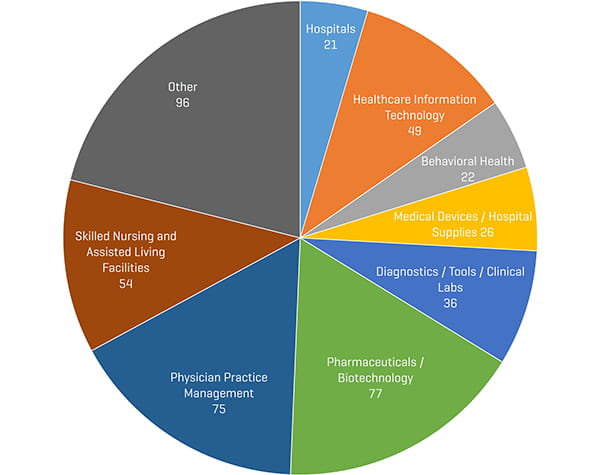

Q4 2019 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

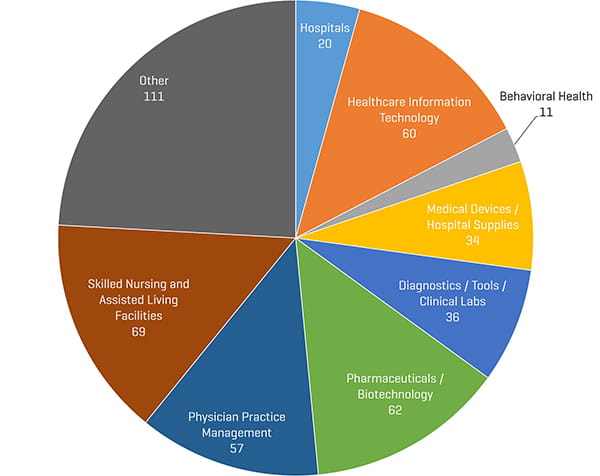

Q3 2019 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

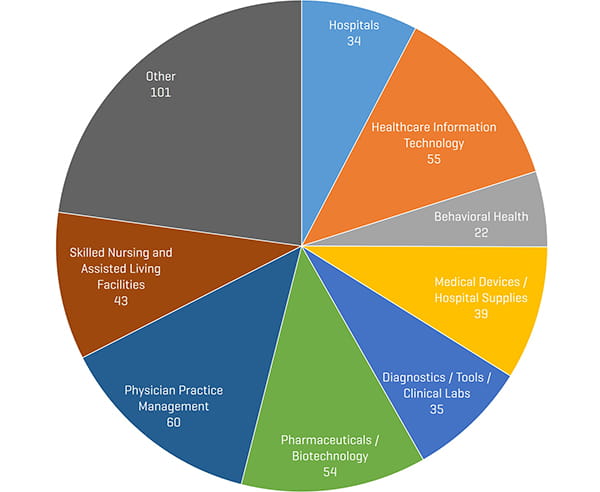

Q4 2018 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

Public Comparable Companies: Historical and Forward EBITDA Multiples

Source: S&P Capital IQ; Multiples calculated from comparable companies universe that Stout tracks

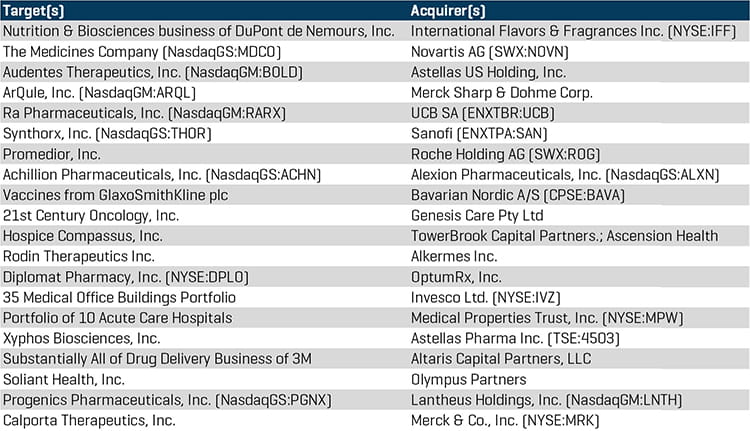

Notable Q4 2019 M&A Transactions

International Flavors & Fragrances Inc. (NYSE: IFF) announced its acquisition of Dupont de Nemours, Inc. Nutrition and Biosciences business. This acquisition was the biggest healthcare transaction of the quarter at $26.2 billion. DuPont will receive a cash payment of about $7 billion and the new entity will have about 4.0x EBITDA of debt, twice the average company in the S&P 500.

Novartis AG (SWX: NOVN) closed its acquisition of The Medicines Company (NasdaqGS: MDCO), maker of Inclisiran – a small RNA interference therapy being studied to evaluate its ability to lower low-density lipoprotein cholesterol.

Astellas Pharma Inc. announced its definitive agreement to acquire Audentes Therapeutics, Inc (NasdaqGM: Bold). The acquisition represents a key step in Astellas Focus Area approach as it is adding a fifth Primary Focus Area in Genetic Regulation.

Merck (NYSE: MRK) has announced its acquisition of ArQule, Inc. (Nasdaq: ARQL), a biopharmaceutical company focused on kinase inhibitor discovery and development for the treatment of patients with cancer and other diseases.

UCB SA (ENXTBR: UCB) has reached an agreement to acquire Ra Pharmaceuticals, Inc. (NasdaqGM: RARX). The acquisition will allow UCB to improve treatment options for people living with myasthenia gravis and other rare diseases.

Sanofi (ENXTPA: SAN) plans to bolster its immune-oncology pipeline through its acquisition of Synthorx, Inc. (NasdaqGS: THOR).

Roche Holding AG (SWX: ROG) has agreed to acquire Lexington, MA-based Promedior, a clinical-stage developer of therapies for fibrotic diseases, for up to $1.39 billion.

Alexion Pharmaceuticals, Inc. (NasdaqGS: ALXN) announced its acquisition of Achillion Pharmaceuticals, Inc. (NasdaqGS: ACHN) in an initial all – cash transaction for $6.30 per share and total transaction of up to $8.30 per share with potential additional contingent considerations.

Bavarian Nordic A/S (CPSE: BAVA) closed its acquisition of GlaxoSmithKline plc vaccines rabipur/rabavert and encepur travel. Bavarian Nordic believes the improved capacity utilization enabled by the integration of the vaccines into its production and fill-and-finish facilities will create future cost reductions.

Australia’s Genesis Care Pty Ltd. announced its acquisition of U.S. provider of radiation therapy and integrated cancer treatments, 21st Century Oncology. Cancer patients in communities across the U.S. are expected to benefit from increased access to high quality cancer care.

Q4 2019 Largest M&A Transactions

Source: S&P Capital IQ

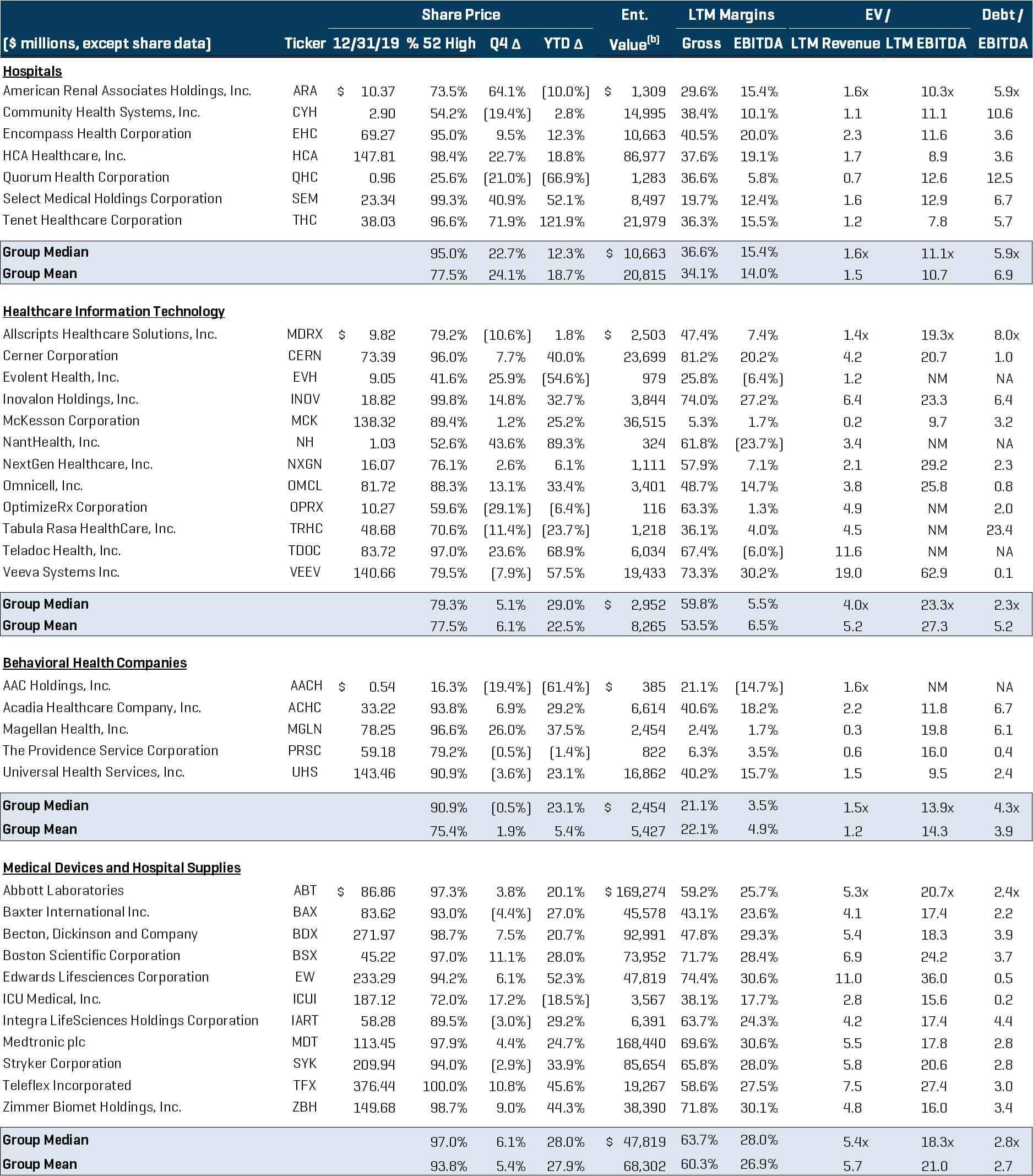

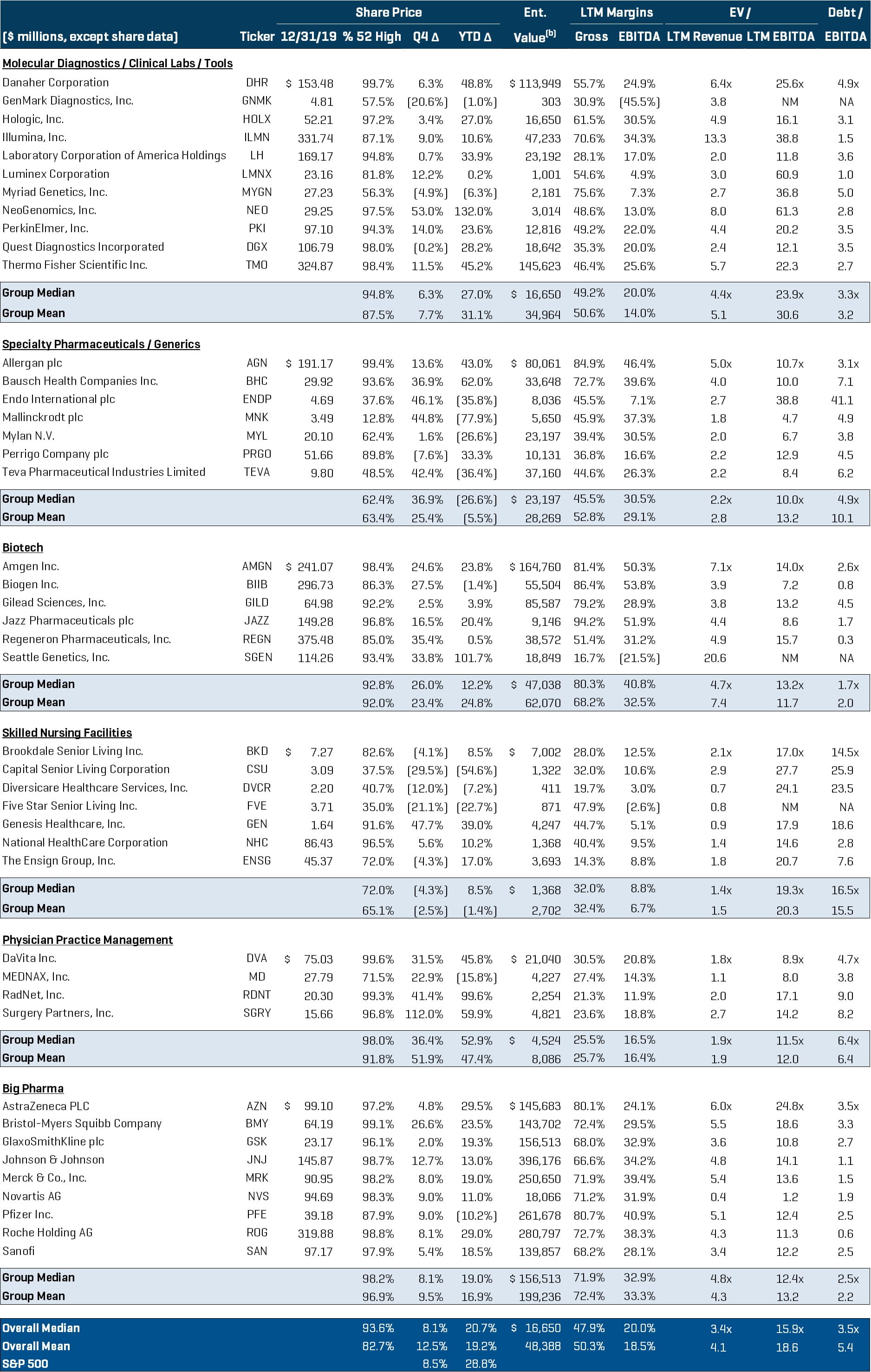

Healthcare Public Company Analysis