English

English

The S&P 500 gained just 1.3% during the third quarter of 2019, while the Healthcare Services and Life Sciences equities that we track in this report under-performed during the quarter, declining -3.2%. The S&P 500 is up 18.6% year to date through the third quarter of 2019, with the mean Stout Healthcare Universe stock price up 6.2% during the same period. As one might imagine, the three healthcare sectors to outperform the market year to date are: Healthcare Information Technology; Medical Devices and Supplies; and Diagnostics, Tool, and Reagents, the sectors without the direct reimbursement exposure. As we indicated in last quarter's report, the Democratic debates have stoked the flames of healthcare reform once again, which tends to hurt the healthcare service sectors disproportionally. There are also specific areas impacted by reimbursement changes or hospitals being disenfranchised by surgeries moving to the ambulatory setting, but we think a lot of the underperformance this year is sentiment-related and probably unjustified.

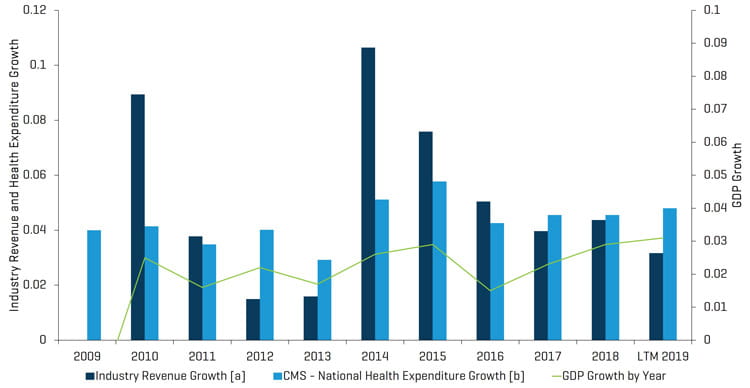

As shown in the table below, healthcare expenditures seem to be tracking in line with economic growth.

Historical Revenue Growth of Segments Monitored by Stout Vs. Annual Health Expenditures and GDP Growth

Notes:

[a] For each period, total revenue figures are derived from the sum of all comparable companies listed in the appendix (Healthcare Public Company Analysis).

[b] CMS tracks National Health Expenditure Accounts (NHEA), which are the official estimates of total health care spending in the United States annually.

Source: www.cms.gov, Historical and Projected NHEA tables.

M&A Market Update

M&A Market Key Takeaways:

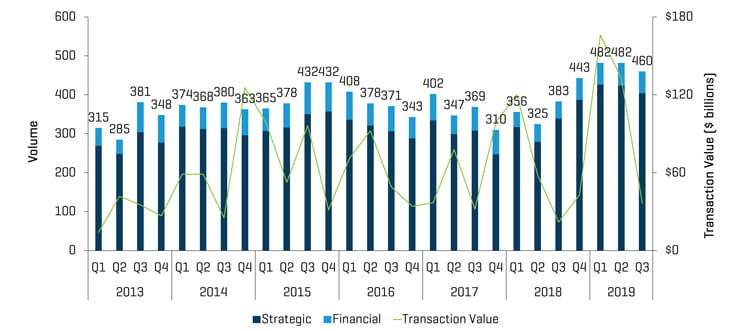

- A strong deal volume quarter with 460 transactions announced and/or closed, a significant increase from last year’s third quarter of 383 transactions but below the record highs of 482 in the each of the first two quarters of this year.

- Activity remains near historic highs and we would note that the number of deals announced in the healthcare sectors that we are tracking, came in at 126 versus 89 in the comparable year earlier quarter and near the historic high of 131 in 4Q’18.

- Overall transaction value in the third quarter of 2019 came in at nearly $37 billion compared to the previous year’s $22 billion, but we would note that the absence of mega mergers being either announced or closed in the period, such as some of the Big Pharma deals announced in prior periods, resulted in transaction value dropping from the $133 billion level seem in the second quarter of 2019.

- Stout Healthcare Universe last-12-month (LTM) 2019 revenue growth up 3.2% from the same LTM period in 2018.

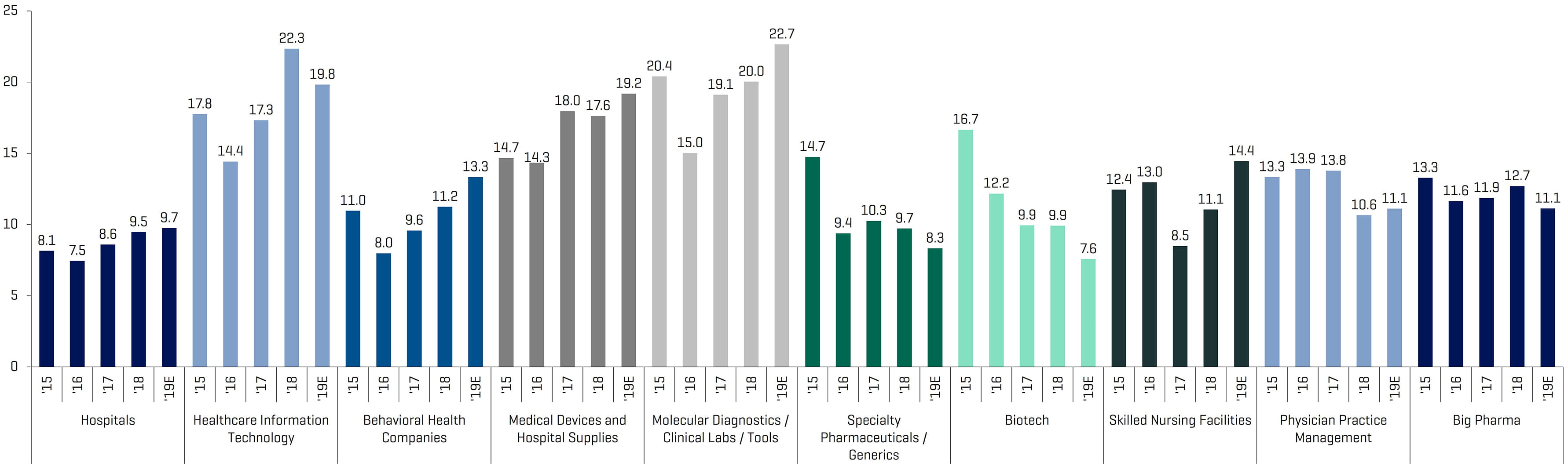

- EBITDA multiples continue to climb for Hospitals, Behavioral Health Companies, Medical Devices and Hospital Supplies, Molecular Diagnostics / Clinical Labs / Tools, and Skilled Nursing Facilities.

- We saw similar transaction volumes in each of the healthcare sectors that we track, but we would note that the Healthcare Information Technology and Skilled Nursing Facility Sectors experienced a significant increase in activity versus the comparable year earlier quarter, maybe for the same reasons.

- Changes in healthcare reimbursement models for services and an emphasis on value-based care (in addition to growth in risk contracting agreements) increasingly require data analytics and the need for consultants to establish how to price these contracts, and smaller operators may be finding it difficult to adapt or simply do not want to take that on. This is driving industry consolidation.

- At the same time, we are seeing growth in the Internet of Things and the need for connectivity and monitoring of many different types of medical devices and durable medical equipment whether it be heart monitors, vital signs monitor, biofeedback devices, sleep apnea devices, glucose monitoring devices, etc.

M&A Market Outlook

There were 126 deals announced in the third quarter of 2019 representing the most in the previous 14 quarters, which seems to support continued growth in activity.

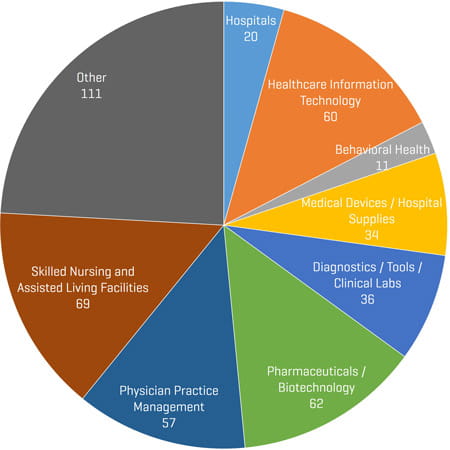

Skilled Nursing and Senior Housing continue to report high levels of activity. There were 69 Skilled Nursing/Senior Housing deals in the quarter versus 40 in the year earlier quarter.

Consolidation of the Physician Practice Management sector continued to be robust with 57 deals announced/closed, in line with 59 in the year earlier quarter. This is down from 72 deals in second quarter of 2019, but still a very healthy level. Interestingly, the activity in the quarter was expected with add-ons in Ophthalmology, Dermatology, Ortho/Spine/Sports Medicine, and Dental, but we also saw transactions in GI, Pain, Emergency Medicine, Anesthesia, and Pain Management, so it was pretty widespread as private equity is consolidating the industry and adopting themes across many different sub-specialties.

Medical device and supply transactions came in at 34 in the quarter and were down from 53 a year ago. We will have to see if this activity will pick up going forward or if strategic activity will subside. There were some notable deals announced and/or closed in the quarter, albeit smaller compared with some of the deals in previous quarters, such as Cantel Medical acquiring HuFriedy in the dental instrument space, Corindus Vascular Robotics being acquired by Siemens, Avedro being acquired by Glaukos, Collagen Matrix being acquired by Linden, and Aspen Surgical Products being acquired by Audax. We would note that post close of the quarter, 3M closed the acquisition of Acelity. We just did not see the usual level of tuck-ins either announced or closed by the big device manufacturers in the quarter.

Pharmaceuticals / Biotechnology realized a noticeable increase in deal flow - increasing to 62 in third quarter of 2019 compared with 53 the previous quarter and 52 in the third quarter of 2018. The deal value in this sector fell off precipitously, however, as there were no mega merger announcements or closings for deals like Abbvie-Allergan in the quarter. One transaction that caught our eye here was H. Lundbeck acquiring Alder BioPharmaceuticals, which is developing a drug for the preventative treatment of migraines. We would note that non-invasive neuromodulation device maker Cefaly Technology, has had compelling efficacy outcomes without the need for a systemic medication.

Diagnostics / Tools / Clinical Labs saw a sizable uptick in deal activity reaching 36 in third quarter of 2019 compared to 24 in the previous quarter and 26 a year ago. The most notable deal here was Exact Sciences acquiring Genomic Health.

Healthcare Information Technology saw 60 transactions in the quarter versus 36 a year ago and there are too many different sub-segments here to get granular in this report, whether it be artificial intelligence (AI) for practices, patient scheduling systems, cloud-based storage systems, electronic health records, billing systems, etc. This will continue to be an area with a high volume of activity.

Q2 2019 M&A Transactions: Volume and Value

Source: Source: S&P Capital IQ and Stout Industry Research

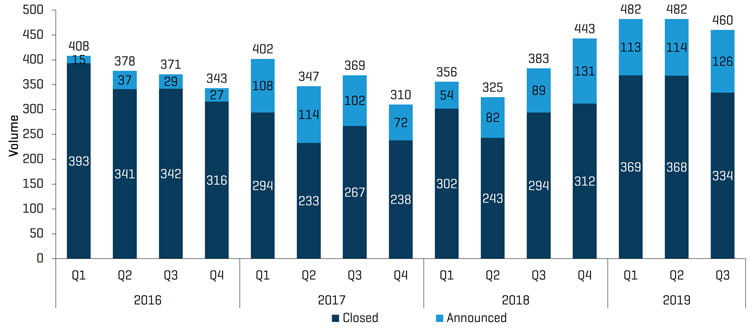

Historical M&A Transactions: Announced vs. Closed

Source: S&P Capital IQ and Stout Industry Research

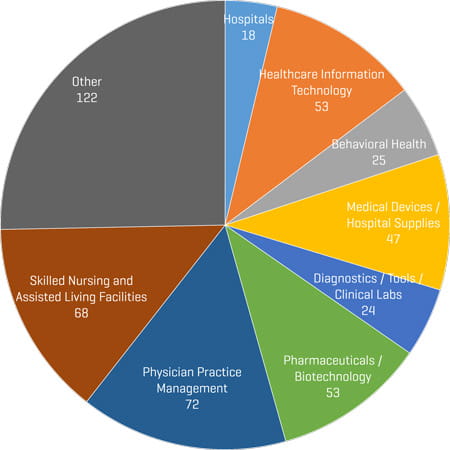

Q3 2019 M&A Transactions by Segment

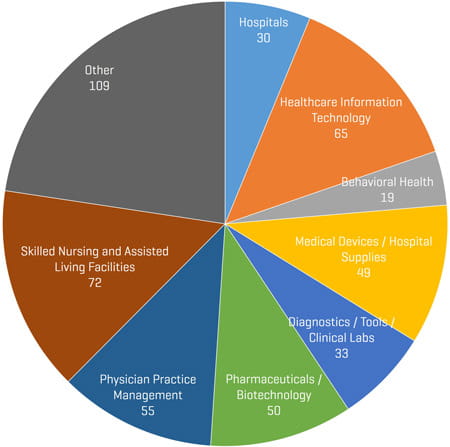

Q2 2019 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

Q1 2019 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

Public Comparable Companies: Historical and Forward EBITDA Multiples

*Click on chart image below to view larger.

Source: S&P Capital IQ; Multiples calculated from comparable companies universe that Stout tracks

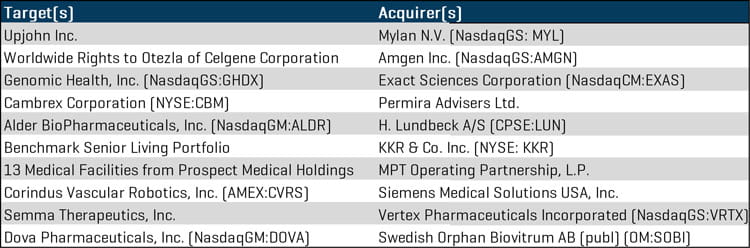

Notable Q3 2019 M&A Transactions

Mylan N.V. (NasdaqGS: MYL) announced its acquisition of Upjohn Inc., a manufacturer of biopharmaceutical drugs such as Lipitor and Zoloft, among others. The new combined company will generate roughly $20 billion a year in revenue.

Amgen Inc. (NasdaqGS: AMGN) announced an acquisition of the worldwide rights to Otezla from Celgene Corporation for $13.4 billion. The acquisition is contingent on the Bristol-Myers Squibb closing the pending merger with Celgene which is expected to close by the end of 2019.

Exact Sciences Corporation (NasdaqCM: EXAS) announced its acquisition of Genomic Health, Inc. (NasdaqGS: GHDX), which provides clinically actionable genomic information to personalize cancer treatment decisions for nearly $3 billion.

Permira Advisers announced its purchase of contract development and manufacturing company Cambrex Technologies (NYSE: CBM) at $60 per share at a 47% premium. The total deal value was about $2.6 billion.

H. Lundbeck A/S (CPSE: LUN) signed a definitive agreement to purchase Alder Biopharmaceuticals, Inc. (NasdaqGM: ALDR), a clinical-stage biopharmaceutical company for $2 billion.

Private equity giant KKR & Co. (NYSE: KKR) announced its investment in Benchmark’s portfolio of 48 medical properties for $1.85 billion.

Medical Properties Trust invested in Prospect Medical Holdings, Inc. via a sale-leaseback of the company’s real estate assets in California, Connecticut, and Pennsylvania, which included hospitals and various other facilities.

Siemens Medical Solutions USA, Inc. announced its acquisition of Corindus Vascular Robotics, Inc. (AMEX: CVRS), designer and manufacturer of robotic-assisted systems for use in interventional vascular procedures for $1.1 billion.

Vertex Pharmaceuticals Incorporated (NasdaqGS: VRTX) announced its plan to acquire Semma Therapeutics, Inc., a company focused on developing a cell therapy for Type 1 diabetes for $950 million.

Swedish Orphan Biovitrum (OM: SOBI) announced its acquisition of pharmaceutical company Dova Pharmaceuticals, Inc. (NasdaqGM: DOVA) for $927 million. The acquisition will enhance SOBI’s leading position in hematology and orphan diseases and improve its presence in the United States.

Cantel Medical Corporation (NYSE: CMD) announced its acquisition of dental instrument manufacturer Hu-Friedy Mfg. Co., LLC for $775 million. Cantel will combine Hu-Friedy with its dental division Crosstex.

Q3 2019 Largest M&A Transactions

Source: S&P Capital IQ

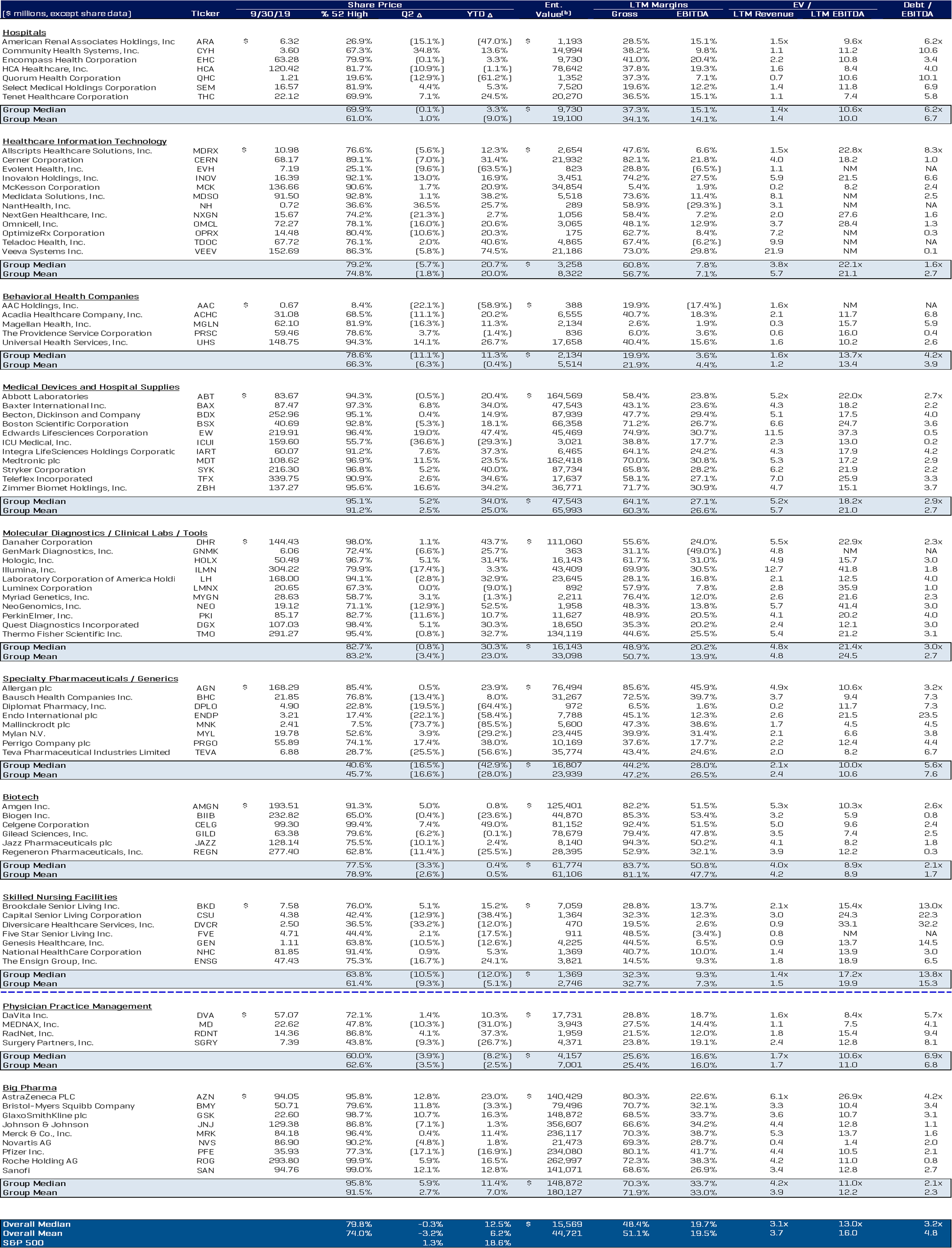

Healthcare Public Company Analysis

*Click on chart image below to view larger.

Source: S&P Capital IQ