English

English

Global markets were bullish in the first quarter of 2019, after declining in the fourth quarter of 2018. The first quarter marked not only a recovery for the overall market, but also for healthcare services and life sciences equities. Indeed, healthcare stocks mirrored the general market’s upward performance during the first three months of the year. Among the healthcare stocks that we track, the median price increase was 10.6% during the quarter, while the mean price increase was 11.3%. During the same period, the S&P 500 was up 12.9%, signaling a recovery off 2018 lows (a 14.3% decrease for the fourth quarter of 2018 and 7.0% decrease for the year).

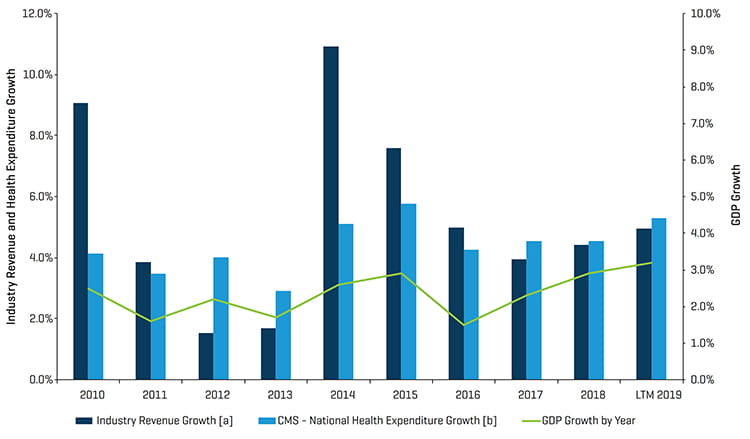

We believe that the fourth-quarter decline was driven by 1) lower corporate earnings forecasts (Apple, for example) and investors’ anticipation of lukewarm earnings reports; 2) rising interest rates and a related impact on the housing market and construction and mortgage activity, 3) weakness in the Chinese economy, and 4) lagging brick-and-mortar retail sales. There was also concern about the Centers for Medicare and Medicaid Services altering its drug-buying program and several presidential candidates’ support of potential “Medicare for All” policies. Healthcare costs, as one of the charts later in this report reveals, have been tracking closely with gross domestic product growth, so the traditional arguments for healthcare reform based on healthcare costs rising significantly faster than the overall economy may not hold this time around, but affordable access to care for all will likely be the focus going forward .

But as we move ahead in 2019, a strong economy, along with the Federal Reserve now potentially holding the line on interest rates, seems to be helping global equity markets. Political turmoil in Congress, however, and concerns about a trade war with China are leading to market volatility as of mid-May. Several specialty pharma companies are encountering numerous headwinds, including: politicians sniping pharma companies over drug pricing; class action lawsuits and regulators going after the likes of Purdue Pharma in the opioid crisis; new market entrants in branded and generic categories; and proposals for CMS to modify its drug-buying programs and/or change reimbursement policies. On the healthcare service side, generally speaking, the reimbursement climate is neutral with inflationary-type increases offered by CMS in many healthcare service categories, combined with the introduction of value-based medicine components that will penalize those providers with substandard care.

Healthcare Segment Performance

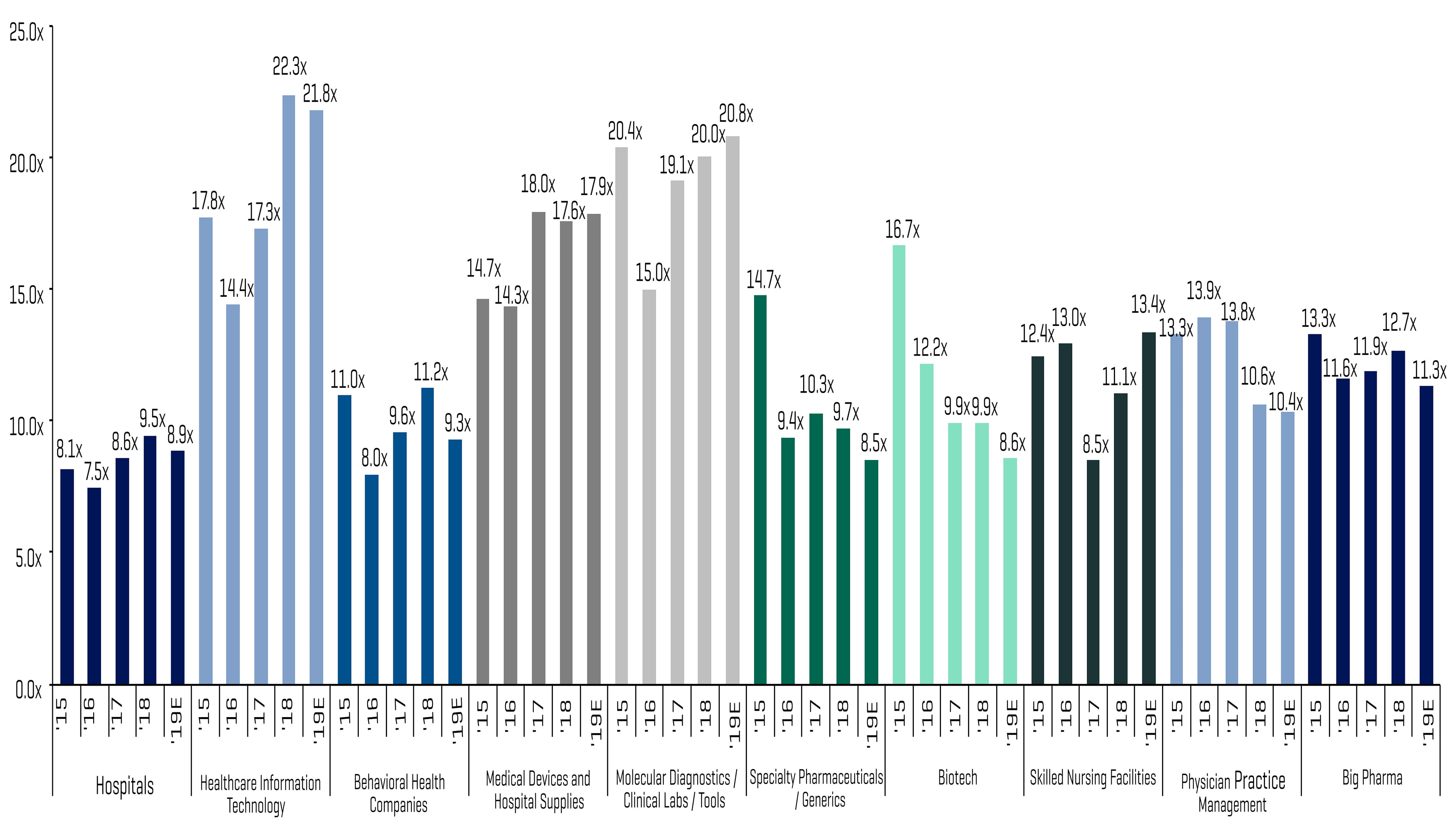

Despite the headwinds, nearly all segments that we track delivered strong stock price performance during the first quarter. The exception was hospitals, which experienced a group median decrease of 4.7% for the quarter largely due to weak performance from long-term care facilities that offset better performance of the larger integrated health systems such as Community Health Systems, HCA Healthcare, and Tenet Healthcare.

The molecular diagnostics and tools, medical devices and hospital supplies, skilled nursing facilities (SNFs), and behavioral health categories all saw double-digit stock price increases, outperformed the market, and led the healthcare sector with group median increases of 24.7%, 19.7%, 13.4%, and 13.3%, respectively. Through new product developments and growing market adoption, medical device companies continue to see core growth in emerging areas like transaortic valve replacement (TAVR), external insulin pumps, and continuous glucose monitoring.* They are also benefiting from consolidation opportunities and procedure growth in emerging and more established markets. The surprises in the quarter were strong stock performance in the SNF sector and M&A multiple expansion that accompanied a big pick-up in M&A activity in the quarter (see below.)

Healthcare information technology (+10.3%), Big Pharma (+9.3%), physician practice management (+8.4%), biotech (+6.4%), and specialty pharmaceuticals/generics (+5.9%) all underperformed the market and other healthcare verticals.

Historical Revenue Growth of Segments Monitored by Stout Vs. Annual Health Expenditures and GDP Growth

Notes:

[a] For each period, total revenue figures are derived from the sum of all comparable companies listed in the appendix (Healthcare Public Company Analysis).

[b] CMS tracks National Health Expenditure Accounts (NHEA), which are the official estimates of total health care spending in the United States annually.

Source: www.cms.gov, Historical and Projected NHEA tables.

M&A Market Update

M&A Market Key Takeaways:

- Recovering public markets performance and a continuation of strong M&A activity

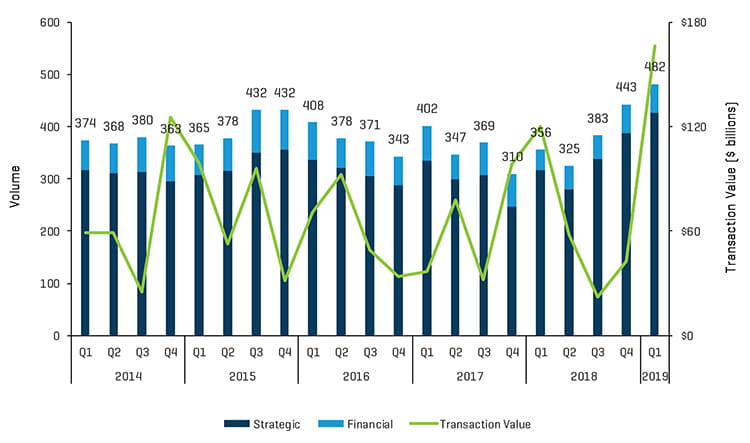

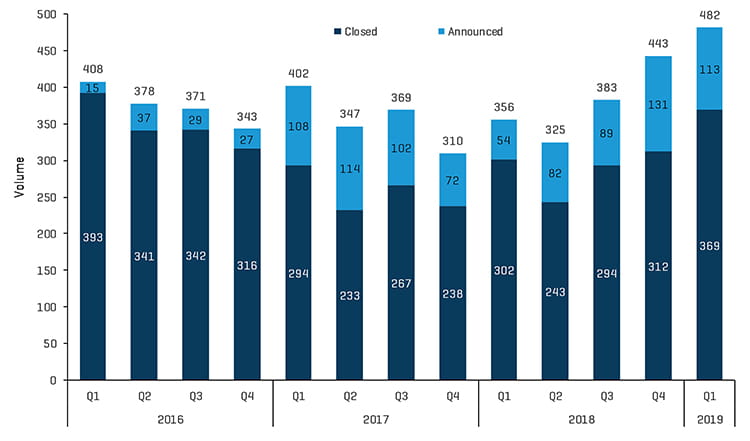

- Highest deal-volume quarter (482 total announced/closed transactions) in the last five years

- Highest deal-value quarter ($166.1 billion) in the last five years, driven by Bristol-Myers Squibb’s (NYSE:BMY) landmark acquisition of Celgene (NASDAQ:CELG)

- Skilled nursing segment experienced tremendous M&A activity as an aging population and probably greater reimbursement visibility drives deal activity and valuation multiples

- Deal volume in physician practice management segment remained strong as private equity-backed roll-ups continued

M&A Market Outlook

As we indicated above, we had a record quarter in terms of M&A activity in the first quarter of 2019, with 482 deals announced and/or closed versus 356 in the 2018 first quarter. A surge in M&A activity in the SNF/assisted living sector was a big contributor with 72 deals versus 43 in the fourth quarter of last year. The stock market performance strength among SNFs, combined with the level of M&A activity, may have been indicative of a collective sigh of relief that the new Patient Driven Payment Model (PDPM) for SNF payments for fiscal year 2020 will increase 2.5%. CMS changing the definition of “group therapy,” which currently covers groups of four patients, to now allow as few as two patients to as many as six was also a positive development that has been requested by stakeholders for several years. This change will allow SNFs to group six patients with one therapist, for example, while only paying for one therapist and getting reimbursed for six. The offset is that SNFs need to get patients with the same diagnosis and treatment to be able to take advantage of this group therapy category, and changes to resource utilization group (RUG) reimbursement rates could also have an impact. In the final assessment, providers should at least be able to reduce their number of therapy staff to offset wage increases or reimbursement pressure. The program is expected to be cost-neutral to the government.

Consolidation of the physician practice management sector continued to be robust with 55 deals announced/closed versus 60 in the prior quarter. Ophthalmology and dermatology in particular saw a number of add-on acquisitions.

Biotech had a number of the largest transactions in the quarter, including Bristol-Myers Squibb acquiring Celgene, Eli Lilly buying Loxo Oncology, Roche acquiring Spark Therapeutics, and Danaher acquiring General Electric‘s BioPharma business.

Q1 2019 M&A Transactions: Volume and Value

Source: Source: S&P Capital IQ and Stout Industry Research

Historical M&A Transactions: Announced vs. Closed

Source: S&P Capital IQ and Stout Industry Research

Q1 2019 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

Q4 2018 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

Public Comparable Companies: Historical EBITDA Multiples

Source: S&P Capital IQ; Multiples calculated from comparable companies universe that Stout tracks

Notable M&A Transactions

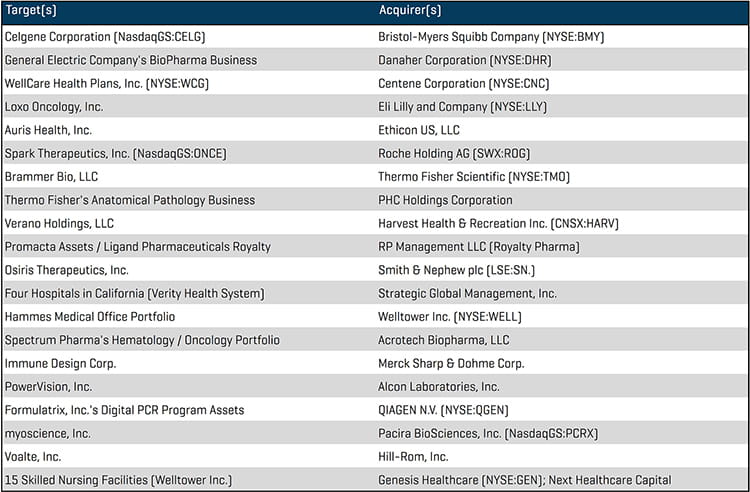

Global biopharmaceutical company Bristol-Myers Squibb (NYSE:BMY) announced the approval of an issuance of common stock in connection with the company’s pending merger with biopharmaceutical company Celgene (NASDAQ:CELG). The transaction, valued at more than $90 billion including debt, represents one of the largest pharmaceutical mergers in history. The acquisition is expected to close in the third quarter of 2019.

Global science and technology healthcare innovator Danaher (NYSE:DHR) announced its acquisition of the Biopharma business of GE Life Sciences (GE BioPharma) for a cash purchase price of approximately $21.4 billion. GE Biopharma is a leading provider of instruments, consumables, and software that support the workflows of developing biopharmaceutical drugs.

Multi-national healthcare enterprise Centene (NYSE:CNC) and WellCare Health Plans (NYSE:WCG), a provider of government-sponsored managed care services, announced that Centene will acquire WellCare in a cash and stock transaction representing a total enterprise value of approximately $17.3 billion. The combined entity would have approximately 22 million members across all 50 states.

Global pharmaceutical company Eli Lilly (NYSE:LLY) announced the successful completion of its acquisition of Loxo Oncology, a biopharmaceutical company with a focus on developing medicines for genetically defined cancers. The acquisition, valued at approximately $8 billion, will be funded with cash and is expected to provide Eli Lilly a strong pipeline of investigational cancer medicines.

Swiss multinational healthcare company Roche Holding (SWX:ROG), announced its acquisition of biotech company Spark Therapeutics (NASDAQ:ONCE) for approximately $4.8 billion. Spark is the only biotech company that has successfully commercialized a gene therapy for genetic disease in the United States. The transaction is expected to close in the second quarter of 2019.

Harvest Health & Recreation (CNSX:HARV), one of the largest cannabis companies in the United States announced its acquisition of Verano Holdings, one of the largest privately held multi-state, vertically integrated licensed operators of cannabis facilities. The all-stock transaction represents an estimated purchase price of approximately $850 million, marking another landmark deal in the continually expanding cannabis sector. Post-transaction, Harvest will hold licenses that will allow the company to operate up to 200 facilities in 16 states and territories across the country.

Biopharmaceutical company Ligand Pharmaceuticals (NASDAQ:LGND) announced the sale of its Promacta-related intellectual property rights, currently licensed to Swiss multinational biopharmaceutical company Novartis (SWX:NOVN), to private equity drug royalty investor Royalty Pharma for approximately $827 million in cash. The transaction gives Royalty Pharma rights to the royalty stream on worldwide net sales of Promacta.

Q1 2019 Largest M&A Transactions

Source: S&P Capital IQ