English

English

One need only watch the headlines to know that substance dependence or abuse is a growing crisis in the United States. Deaths from opioids have been rising sharply for years, and drug overdoses alone are responsible for more deaths under age 50 than any other cause in the U.S. According to Substance Abuse and Mental Health Services Administration (SAMHSA), approximately 20.1 million people ages 12 or older had a substance use disorder (SUD) in the past year, including 15.1 million people who had an alcohol use disorder and 7.4 million people who had an illicit drug use disorder.

Federal officials estimate that opioid abuse drains nearly $80.1 billion a year from the U.S. economy due to expenses tied to health care, criminal justice, and lost productivity. Alternatively, SUDs represent a large market opportunity because the U.S. currently spends about $36 billion a year on addiction treatment, while only a fraction of those who need help are actually getting care. We expect this market will continue to grow as the country grapples with an opioid crisis that has become a very public and political issue.

According to the Suboxone website of drug manufacturer Indivior, there were approximately 2.1 million people who had abused or were dependent on opioids – such as heroin – or prescription painkillers in 2016.

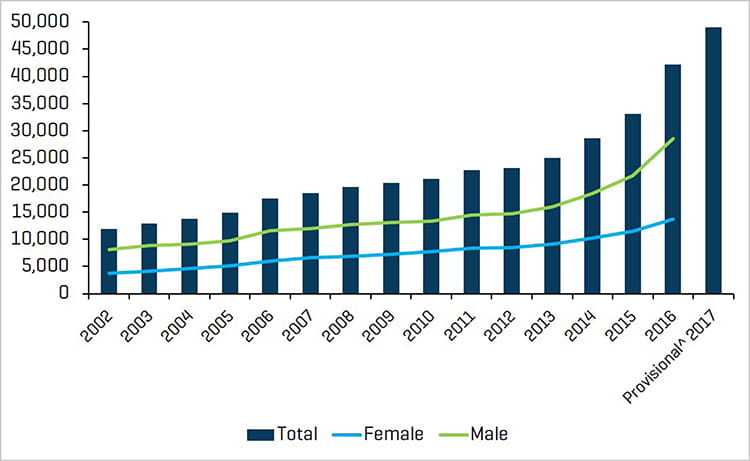

Number of Deaths Involving Opioid Drugs

Source: drugabuse.gov; National Center for Health Statistics, CDC Wonder

Insurance has historically provided limited coverage for these patients, whether it be for residential or outpatient treatments. Legislative changes imposed by the Affordable Care Act and the Mental Health Parity Act have mandated coverage of SUDs as an essential healthcare benefit. Growing availability of insurance coverage for SUDs has helped expand the market; however, there are always those that spoil a good thing with body brokering scams and/or fraudulent or excessive billing practices, which has led federal task forces to crack down on unscrupulous fringe players. The industry is now confronted with resistance from insurance companies and state governments (Medicaid) that have wrestled to understand the problem as well as how to best treat these patients in a cost-effective manner.

Insurance Companies Reign in Residential Treatment Centers

Residential treatment center (RTC) providers have been facing pressure on several fronts as insurance companies have been cracking down on bad actors by conducting audits and attempting to “claw back” expenses for what they describe as medically unnecessary treatments or excessive billing for urinalysis.

Insurance companies have been denying admissions wherever possible on the basis of medical necessity and reducing per diem payments for residential treatment, partial hospitalization, or intensive outpatient treatments. Additionally, in some cases, insurance companies are attempting to drive providers to go in-network, reducing length of stay in residential facilities, and attempting to drive patients to the lower-cost outpatient setting. At this setting, the cost is not always covered, but patients can receive a range of services from counseling to medication-assisted treatment (MAT).

MAT includes the prescription of drugs such as methadone, Suboxone, Subutex, or Vivitrol. These drugs help reduce withdrawal symptoms of opioid (or alcohol) dependence, while simultaneously working to block all existing opiates from affecting the body. Dosages are titrated down as patients stabilize, and then patients are placed on a maintenance dose while simultaneously undergoing counseling. Insurance companies argue in favor of medication-assisted outpatient treatment as opposed to residential treatment (abstinence) on the basis of available clinical evidence and outcomes data.

The problem here is that establishing outcomes for traditional residential programs is challenging for any given provider because tracking patients over the long term is difficult and patient treatments are neither standardized nor benchmarked across competing facilities. This does not, however, indicate that residential treatment is not needed. Addiction does not only involve chemical dependence, but also the circumstances, emotions, and thoughts that led to the initiation of the disorder.

To recap, the industry is facing reimbursement cuts, reduced length of stay, loss of patients to outpatient treatment, federal task force investigations, insurance audits, and claw backs.

Google keyword changes have also made patient acquisition more difficult. In September 2017, Google stopped accepting ads for rehab centers until the tech giant could determine how to prevent unethical treatment providers from using the Google platform to capture and steer patients into suboptimal programs. Some advertisers posed as caregivers, when in reality they were call centers that sold leads on patients to the highest bidder.

Opportunity Persists for Investors and Operators

Despite all of this, in our opinion, there will be plenty of ways to achieve superior returns in this growing sector by investing in smart, forward-thinking management teams.

Our understanding of the patient-admission process, based on our visits to many facilities and conversations with providers, is perceived as follows:

When a patient or family member calls a residential treatment center, an agent for the provider will:

- verify benefits

- attempt to obtain a pre-authorization for treatment from the insurance company

To obtain pre-authorization, in many – but not all – states, patients are first required to undergo a pre-certification process whereby they must see a physician to establish that residential treatment is medically necessary. (Pre-certification is illegal in some states and cannot be used to deny admission to an RTC.)

If the physician deems treatment medically unnecessary, then admission may be denied. The insurance company’s next line of defense may be to indicate that detox is required for three days, though many providers claim patients need seven days, and patients will be sent to an outpatient facility thereafter. If the patient is not doing well in the outpatient setting, the RTC may request a utilization review to allow residential treatment that may then be granted for a specific period of time, such as 21 days. We have also heard arguments that some insurance providers are discouraging patients from going to other states for treatment, when in certain instances, leaving the state may be just what certain patients need.

In the final analysis, insurance companies would probably prefer that patients go to a detox hospital and then be discharged to an outpatient clinic, such as a methadone clinic, in order to reduce costs. We do believe that reimbursement pressure, reductions in length of stay in residential treatment, lower payment for urinalysis, and marketing challenges have some private equity firms focused on outpatient opportunities. However, we believe residential treatment is essential and that such treatment will grow as a result.

Another visible trend we may see involves more providers moving to, and patients being treated in, large 200-bed campus-like facilities as opposed to the six-bed house model. As providers are forced to go in-network, smaller six-bed housing facilities may have difficulty accepting lower rates given their overhead.

Outpatient Treatment and Medication-Assisted Therapy

One of the significant arguments today in treating SUDs is abstinence versus MAT. RTCs typically offer a continuum of care that begins with detox and is followed, in sequence, by residential treatment, partial hospitalization, intensive outpatient treatment, and, finally, ongoing counseling and sober living.

These programs typically focus on abstinence. They employ therapists such as licensed mental health counselors, certified addiction professionals, and masters-level therapists. Services offered may include:

- Cognitive behavioral therapy

- Contingency management

- Motivational enhancement therapy

- 12-step programs

MAT, on the other hand, is provided in an outpatient setting or clinic and is based on substituting opioids like heroin, hydrocodone, or oxycodone with medications that alleviate withdrawal symptoms and/or cravings, such as methadone or Suboxone.

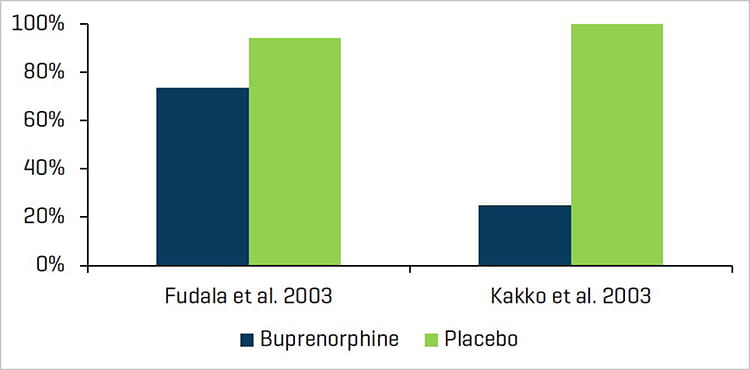

Opioid Use with or without Buprenorphine Treatment

Source: drugabuse.gov

Clearview Capital recently acquired Community Medical Services Holdings, a Scottsdale, AZ-based, fast-growing provider of MAT programs for patients suffering from SUDs. This acquisition is consistent with the theme of growth in outpatient treatment investment.

Many RTCs are responding by establishing their own outpatient facilities to take advantage of industry trends, capture a wider range of patients (via Medicaid, for example), and provide a complete continuum of care.

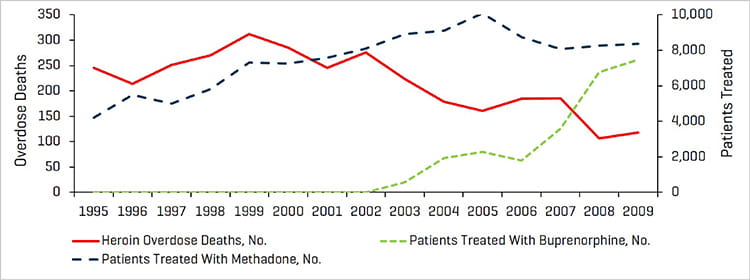

Insurance companies are favoring lower-cost MAT and argue for this on the basis of clinical evidence. However, insurance may not cover the cost of MAT. The chart below provides some examples of data supporting MAT:

Medication-Assisted Treatment and Heroin OD Deaths

Source: drugabuse.gov

We would note that state Medicaid funding may also cover the cost of outpatient care, whereas it may not completely cover residential treatment.

There is a gap in coverage for Medicare patients that require residential treatment, and we are continually monitoring developments, such as this, throughout the behavioral health sector.

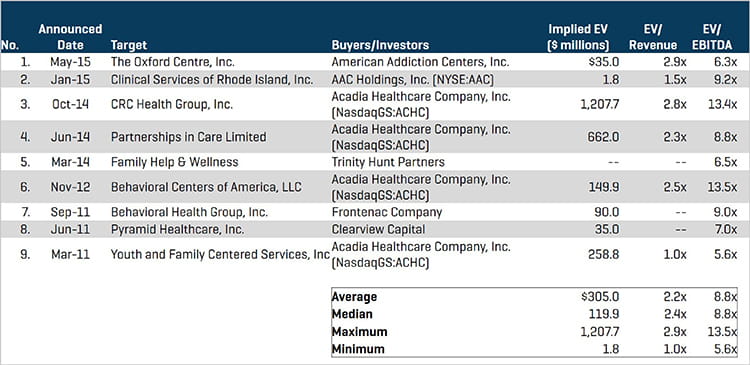

Recent M&A Activity in Behavioral Health

Source: Stout Research

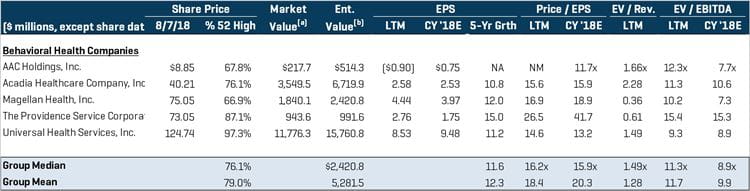

Relevant Publicly Traded Companies

Source: Stout Research

Prospective Strategic and Hybrid Buyers

Source: Stout Research

Hybrid Buyers & Private Equity Sponsors

Source: Stout Research

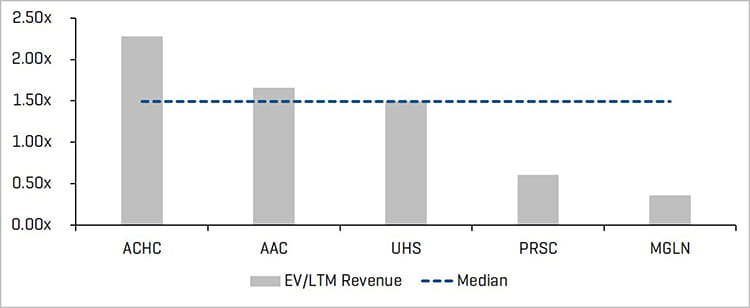

EV/LTM Revenue

Source: Stout Research

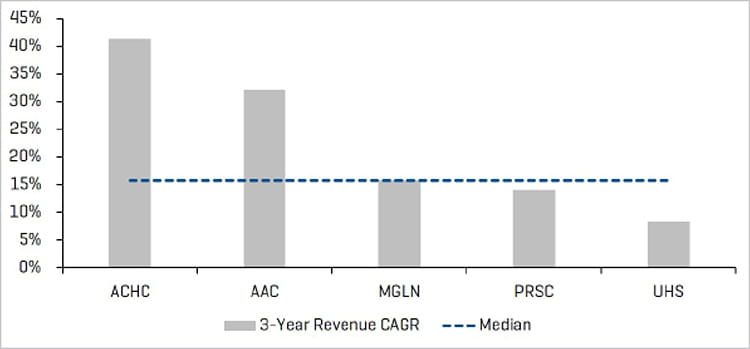

3-Year Revenue CAGR

Source: Stout Research

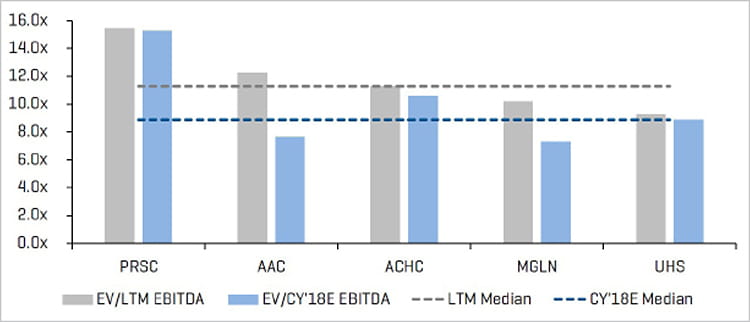

EV/LTM and CY 2018E Adjusted EBITDA

Source: Stout Research

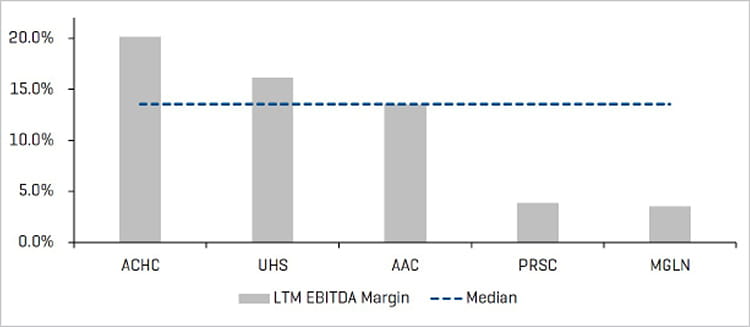

LTM EBITDA Margin