English

English

For our updated version of this industry update, see Behavioral Health Industry Update – September 2018.

Recent Behavioral Healthcare Trends

SUBSTANCE USE DISORDERS’ TANGIBLE ECONOMIC IMPACT

According to the Substance Abuse and Mental Health Services Administration’s (SAMHSA) 2014 National Survey on Drug Use and Health, “Substance use disorders (SUDs) occur when the recurrent use of alcohol or other drugs (or both) causes clinically significant impairment, including health problems, disability, and failure to meet major responsibilities at work, school, or home.”

Not surprisingly, SUDs are a significant contributor to high healthcare costs. SAMHSA also stated, “Excessive substance use and SUDs are costly to our nation, due to lost productivity, healthcare, and crime. Addressing the impact of substance use alone is estimated to cost Americans more than $600 billion each year.”

Behavioral healthcare companies can help reduce these costs under the new value-based medicine paradigm by preventing hospital readmissions via mental health and substance use disorder treatment programs.

A LARGE, GROWING, AND UNDERSERVED MARKET

According to SAMHSA, “An estimated 21.5 million people in the U.S. had SUDs in 2014, representing 8.1% of people ages 12 and older, but only 2.5 million people received the specialized treatment they needed in the past 12 months.”

The staggering cost of lost productivity discussed above and statistics on the low percentage of Americans actually getting treatment that need it suggest that there is a lot of growth ahead for the substance abuse treatment center industry.

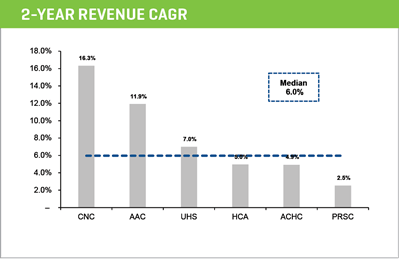

According to the U.S. Department of Health and Human Services, “An estimated $35 billion was projected to be spent in 2014 on U.S. substance use disorder treatment services,” and growth of the market appears to be about 6% in the U.S. if you look at the two-year compound annual growth rate in revenue for the public companies disclosed later in this report.

MARKET FRAGMENTATION MAKES WAY FOR INDUSTRY CONSOLIDATION

According to the National Survey of Substance Abuse Treatment Services, there were approximately 14,995 facilities providing substance abuse treatment annually in the U.S. (the number appears to approach 20,000 if all facilities are included such as half-way houses). The market is highly fragmented with a few large service providers such as Acadia Healthcare ($3 billion in revenue), AAC Holdings, and large hospital systems with leading market shares, followed by a fragmented second tier of private companies with a variety of different business models – in-network versus out-of-network, inpatient and residential versus outpatient, and various treatment and educational programs.

We expect industry consolidation as the new Medicare value-based model of healthcare service and reimbursement is adopted, leading to employer-sponsored insurance, integrated healthcare delivery networks, and third-party payors bringing preferred providers in-network. Risk contracting is expected to rein in costs and improve the quality of care across the continuum of the patient’s healthcare needs. Strategic acquirers and private equity firms will continue to employ geographic roll-up strategies.

CO-MORBIDITIES AND OTHER NEW REVENUE OPPORTUNITIES

There is also an opportunity to expand capacity (acreage), services, and programs offered (for example, skills training, telemedicine, and/or mental health) by behavioral health companies. According to the National Survey of Substance Abuse Treatment Services, “About 45% of Americans seeking substance use disorder treatment have been diagnosed as having co-occurring mental and substance use disorder.”

SOCIAL, POLITICAL, REGULATORY, AND OTHER FACTORS

Various factors should fuel an increase in demand for services: 1) growing social acceptance of treatment for substance abuse and mental health issues, 2) the well-publicized alcohol and opioid addiction crisis, 3) political support for addressing the problem, and 4) expanded reimbursement coverage.

Additionally, changes introduced by the Mental Health Parity and Addiction Equity Act (2008), the Affordable Care Act (ACA) (2010), and subsequent legislation, including the 21st Century Cures Act and the Medicaid and CHIP Managed Care Final Rule (2016), established mental health and substance abuse treatment as Essential Healthcare Benefits. This, in turn, increased available reimbursement coverage for patients and led to market growth, as well as increased investor interest. These pieces of legislation mandated coverage and coverage parity with other medical services.

Beginning in the second quarter of 2017, states across the U.S. began rolling out an increase in Medicaid coverage and reimbursement for substance abuse care that was mandated by the ACA. The new rules increase reimbursement to providers that treat Medicaid patients and loosen restrictions on which Medicaid patients are eligible for substance abuse treatment, as well as where and how they can be treated.

As of this writing, The Trump Administration’s efforts to repeal the ACA could provide states with an option to waive the “Essential Healthcare Benefits” that were mandated by the ACA, which had included behavioral health. This could adversely impact reimbursement available to patients and providers in states that elect the waiver, leading to changes in insurance plans to discontinue drug and alcohol treatment services. We think this is unlikely to have a material impact, given the societal pressure to support these services and the significant amount of productivity lost to substance use disorders.

Reimbursement pressures will continue as a growing number of providers sign contracts to go in-network, and commercial and managed care risk-sharing agreements grow in popularity. This will lead to lower bundled payments and/or per diem payments for lab services, detox, residential treatment, partial hospitalization programs (PHP), intensive outpatient programs (IOP), and professional services versus prevailing fee-for-service (out of network) payments.

Commercial payors are increasingly scrutinizing payments for lab services and evaluating medical necessity, as well as looking at charges for partial hospitalization in residential facilities. Payors may also investigate the classification of claims, dispute claims more voraciously going forward, and push harder for lower per diem rates. Increasing requirements to measure treatment success rates could require more data analyses and systems.

Substance Abuse Treatment: Services and Programs

INPATIENT AND RESIDENTIAL

Inpatient and residential treatment happens within specialty substance use disorder treatment facilities, facilities with a broader behavioral health focus, or specialized units within hospitals. Longer-term residential treatment lengths of stay can be as long as six to 12 months but are relatively less common. These programs focus on helping individuals change their behaviors in a highly structured setting. Shorter-term residential treatment is much more common, and typically has a focus on detoxification (also known as medically managed withdrawal), as well as providing initial intensive treatment and preparation for a return to community-based settings.

PARTIAL HOSPITALIZATION AND INTENSIVE OUTPATIENT

Partial hospitalization or intensive outpatient treatment is an alternative to inpatient or residential treatment. These programs involve people attending very intensive and regular treatment sessions multiple times a week early in their treatment for an initial period. After completing partial hospitalization or intensive outpatient treatment, individuals often step down into regular outpatient treatment, which meets less frequently and for fewer hours per week to help sustain their rehabilitation.

These facilities typically employ licensed mental health counselors, certified addiction professionals, and masters-level therapists. Services offered may include:

- Cognitive behavioral therapy

- Contingency management

- Motivational enhancement therapy

- 12-step programs

TOXICOLOGY TESTING PROVIDERS

Payors typically either incorporate lab testing in a bundled payment for services or pay for a 12-panel urine drug test up to 24 times per year per patient, which tests for amphetamines, methamphetamines, barbiturates, benzodiazepines, marijuana, cocaine, opiates, phencyclidine, methadone, propoxyphene, MDMA (Ecstacy), and extended opiates. Initial 12-panel test toxicology screening is done with a Styrofoam cup that gives a positive reading for one of 12 drugs on the cup itself. If a positive result occurs, the test is sent to a lab for confirmation using LCMS, which is reimbursed separately.

In speaking with private equity and strategic buyers, we have consistently heard that there is a concern about paying much of an EBITDA multiple for lab testing businesses due to concerns that some facilities are not charging for initial lab testing (they may charge for confirmatory testing). Rather, they are incorporating it into per diem payments for treatment services, while others generate half their income from lab testing. As a result, prospective buyers want to see a break out of lab revenue and earnings, and may want to pro form earnings of the provider to adjust lab and out-of-network business to in-network rates.

Prospective buyers have offered a pretty wide range of multiples they would be willing to pay for businesses such as these. There seems to be a view that in certain markets in California and Florida, for example, the business will move to bundled lab payments and in-network services much quicker than in more rural markets. Even here, there is wide disparity of how quickly the market will transition to in-network rates. There appears to be a lot of money chasing in the sector at this time, suggesting that multiples could remain higher in behavioral health at 7x-9x EBITDA on average.

Challenges and Other Considerations

Behavioral health is a big issue for employers — some of which self-insure. A number of technology companies are setting up telehealth operations with therapists to match employees in need of these services with behavioral health providers (including managed care providers), which could drive more patients to in-network providers. Employers are also trying to reduce costs with online counseling and fewer facility-based treatment times.

Unfortunately, a number of well-publicized cases of substance abuse treatment center fraud have sullied the industry. Prospective buyers of these businesses should evaluate in-network versus out-of-network revenue, patient complaints, payor and legal correspondence, and lab contributions to revenue and earnings to make sure that lab testing was medically necessary and not excessive. They should also look at patient referral payments to ensure that there are no unholy alliances (kickback schemes to body brokers, rotation of patients through different facilities, or human trafficking) and review relapse rates and programs to make sure that everything is legitimate. Write-offs for uncollectible accounts are also worth looking into, in order to make sure that co-payments are being pursued. The government (Medicare, Medicaid) and commercial payors will also continue to look at referral practices, and malpractice claims, NIMBY Laws, and corporate practice of medicine issues will have to be managed in the ordinary course of business.

A lot of these issues are already being addressed and, of course, there are always operators who can potentially spoil it for everyone else. However, we continue to think that this industry addresses an important healthcare need and, thus, will continue to grow.

M&A and Valuation Highlights

BEHAVIORAL HEALTH M&A ACTIVITY REMAINS ROBUST

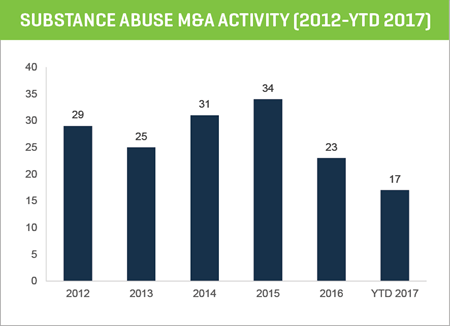

M&A activity among substance abuse treatment centers appears to be bouncing back in 2017. After a lull in activity in 2016, deals are nearing 2015 peak levels, and strategic and private equity demand for acquisitions remains strong.

The 2016 slowdown was likely the result of the market digesting the supply of deals from previous years, buyers evaluating healthcare reform proposals and their impact on the industry in light of the U.S. elections, and the growth in managed care risk contracting and its impact on out-of-network and lab business.

Behavioral health (broadly) and substance abuse treatment centers (specifically) remain attractive segments for investment. We see continued expansion for this profitable and fragmented industry, as the opioid epidemic, regulatory changes, and public policy drive growth in covered lives and treatment service options.

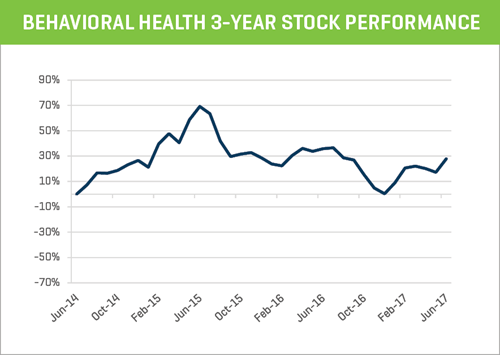

SUBSTANCE ABUSE TREATMENT CENTERS: 2-YEAR STOCK PERFORMANCE

The publicly traded behavioral health companies that operate substance abuse treatment centers have performed well over the last two years, up 47% as a group. The index chart below averages the performance of AAC Holdings (-67%), Acadia Healthcare (+5%), Centene Corporation (+118% ), HCA Holdings (+54%), Providence Service Corporation (+37%), and UHS (+21%).

M&A MARKET & VALUATIONS

- Overall strong M&A market thus far in 2017

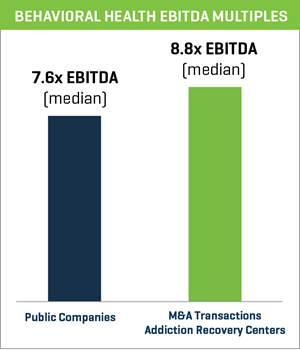

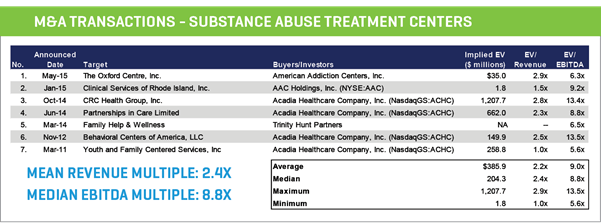

- Recent M&A transactions show that addiction recovery centers are trading at a median valuation of 8.8x EBITDA

- Continued “pent-up” demand for high-quality acquisition targets – private equity and strategic buyers have ample reserves and access to credit, bolstered by historically low interest rates

- Significant activity within healthcare services and facilities, including behavioral health

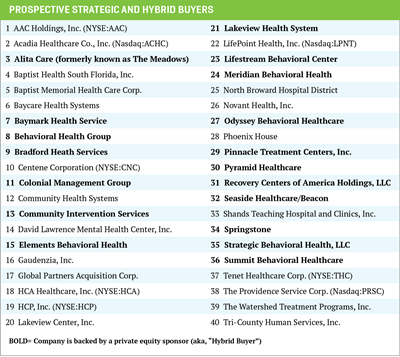

- Large strategic and hybrid buyers are active in consolidating the behavioral health sector and pursuing aggressive acquisition strategies

PUBLIC MARKET & VALUATIONS

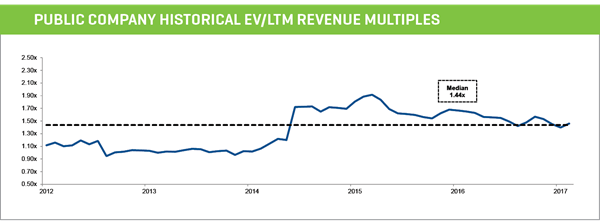

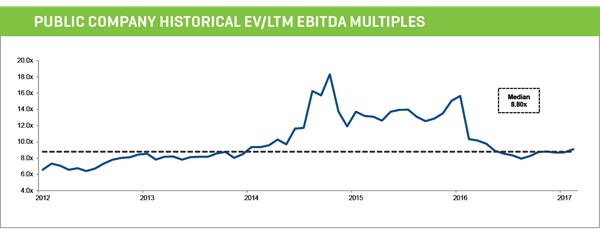

- Publicly traded companies within the behavioral health segment are currently trading at a median valuation of 7.6x EBITDA

- Public markets are favorable, including the behavioral health segment

- Positive growth due to expanded reimbursement coverage and the drug abuse epidemic

- Fragmented industry with high margins attractive to buyers and inspiring industry consolidation

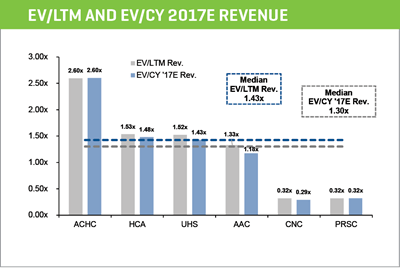

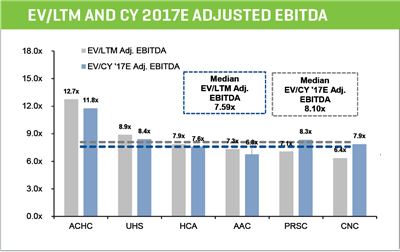

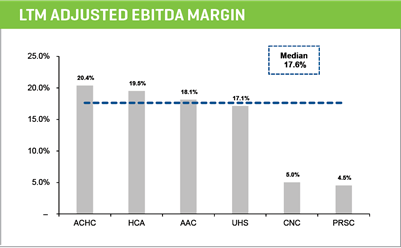

PEER GROUP VALUATIONS

PEER GROUP OPERATING METRICS