English

English

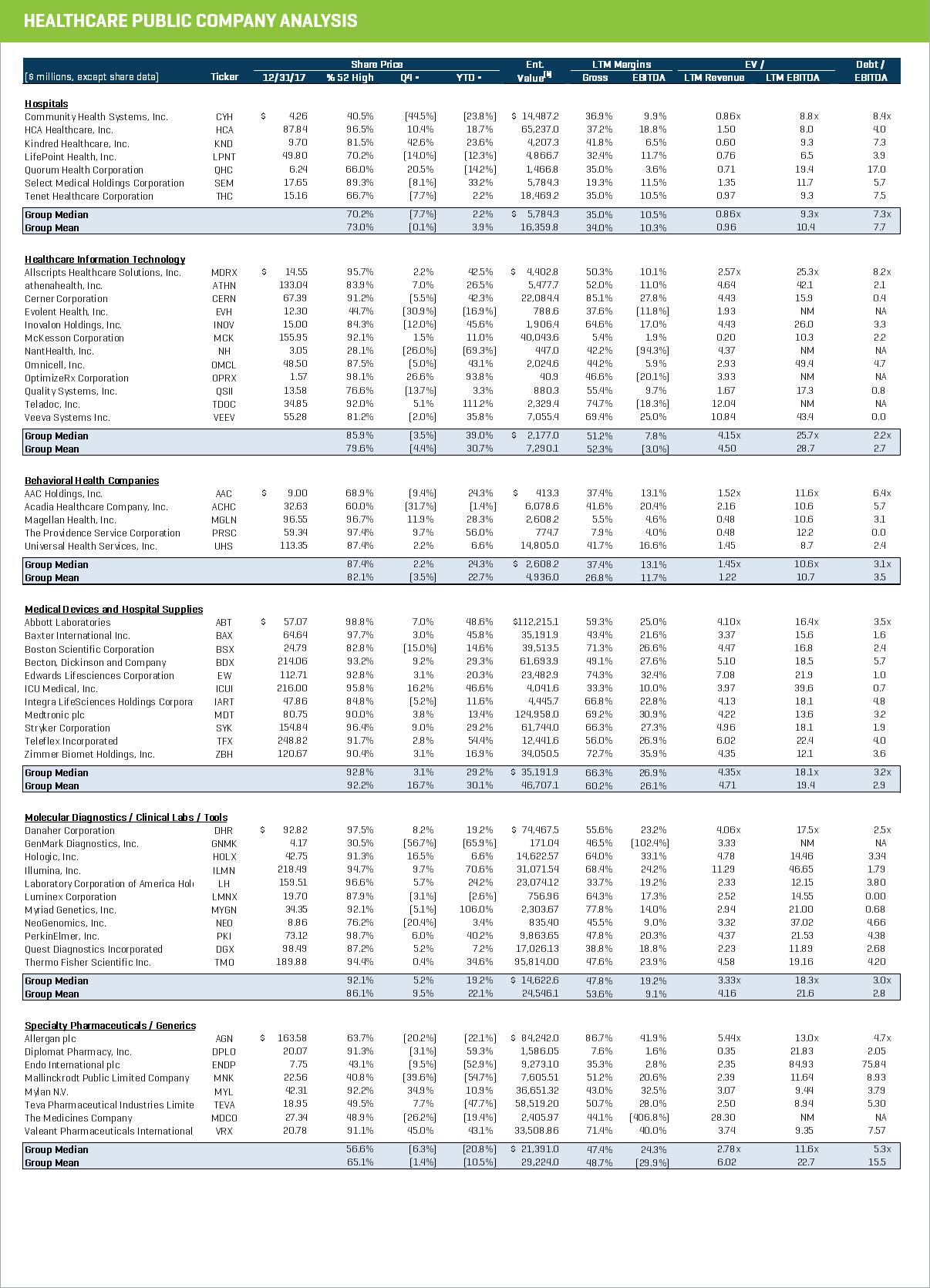

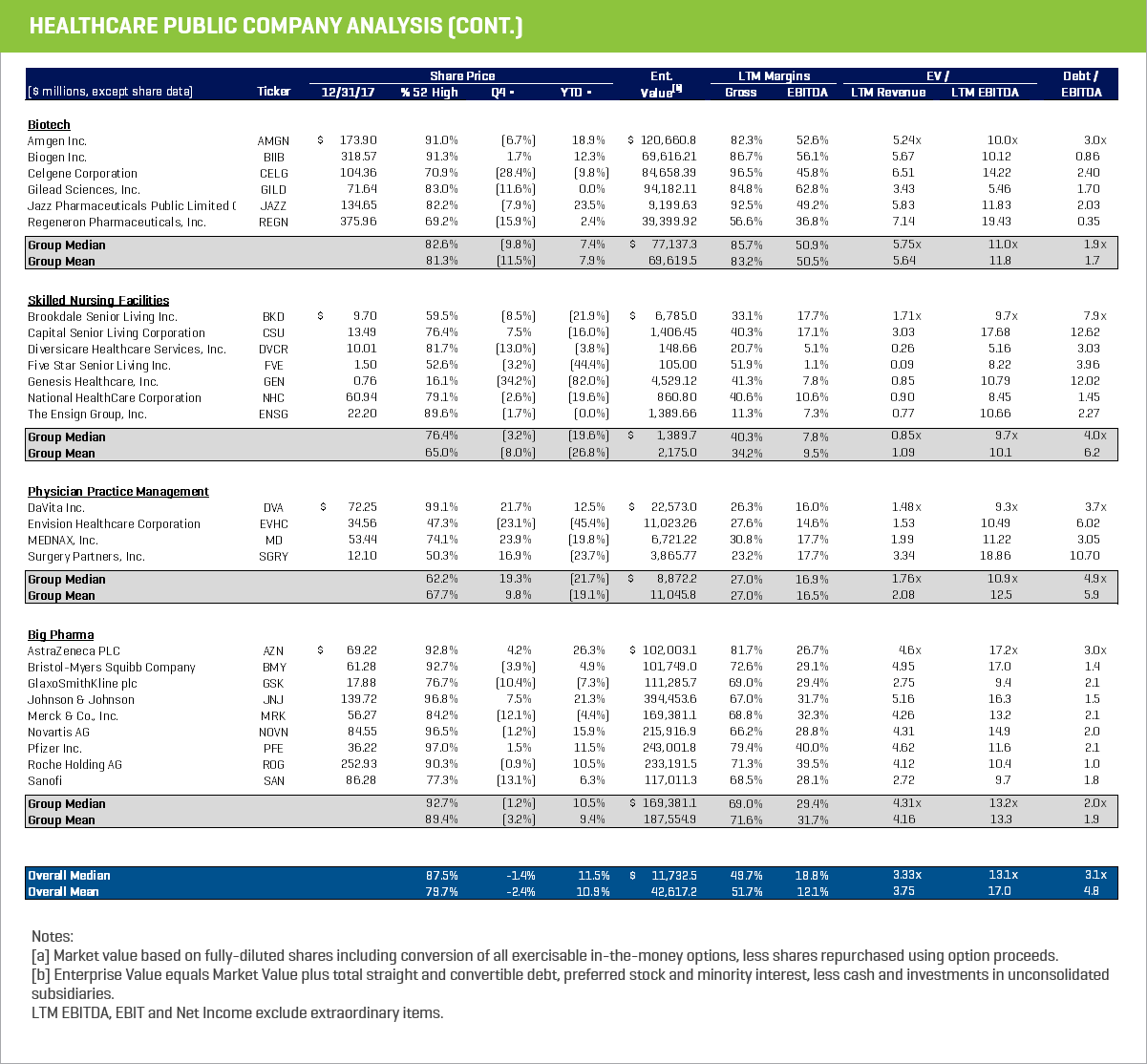

The S&P 500 finished fourth quarter and full year 2017 up 6.12% and 19.42%, respectively, benefiting from expectations of improving corporate earnings and the Trump Administration corporate tax cuts amid a relatively favorable interest rate environment. Healthcare stocks underperformed the market with the average of the industry subsegments that we monitor in this report being up 10.9% for the year and down 2.4% in the fourth quarter of 2017. Not surprisingly, healthcare service stocks were the laggards with skilled nursing facilities and large multi-disciplined physician practices declining 27% and 19%, respectively. Hospitals were up just 3.9% for the year. Healthcare service providers continue to be affected by ongoing reimbursement pressure, growth in in-network contracting, risk sharing and now cuts in federal subsidies for Affordable Care Act (ACA) plans. Big Pharma, Specialty Pharma, and Biotech all underperformed reporting changes of 9.4%, -10.5%, and 7.9%, respectively, due to concerns about regulatory (e.g., concerns about opioid recalls), payor/cost containment pressures from pharmacy benefit managers, patent expirations, pipeline weakness and generic competition.

Medical devices, molecular diagnostics and tools, and healthcare information technology companies all outperformed the market increasing 30.1%, 22.1%, and 30.7%, respectively. Consolidation of the large medical device businesses and tools and diagnostics companies are giving those players the bundling and margin benefits of scale, whereas healthcare information companies will benefit from a wide variety of growth factors such as the need for new systems to evaluate patient cost outcomes under value based care, cyber security to protect medical records, and data-intensive applications for bioinformatics.

The Trump Administration executive order, to defund cost-sharing subsidies to insurance companies participating in the Obamacare exchanges to help cover the cost of co-payments and deductibles for low-income individuals, has raised concern that healthcare service providers will now have to absorb these costs. The Tax Cuts and Jobs Act also eliminated the individual insurance mandate and associated tax penalties, which could mean fewer healthy persons obtaining insurance and insurance companies having fewer and a sicker pool of patients that they are insuring. This could put upward pressure on premiums in 2018.

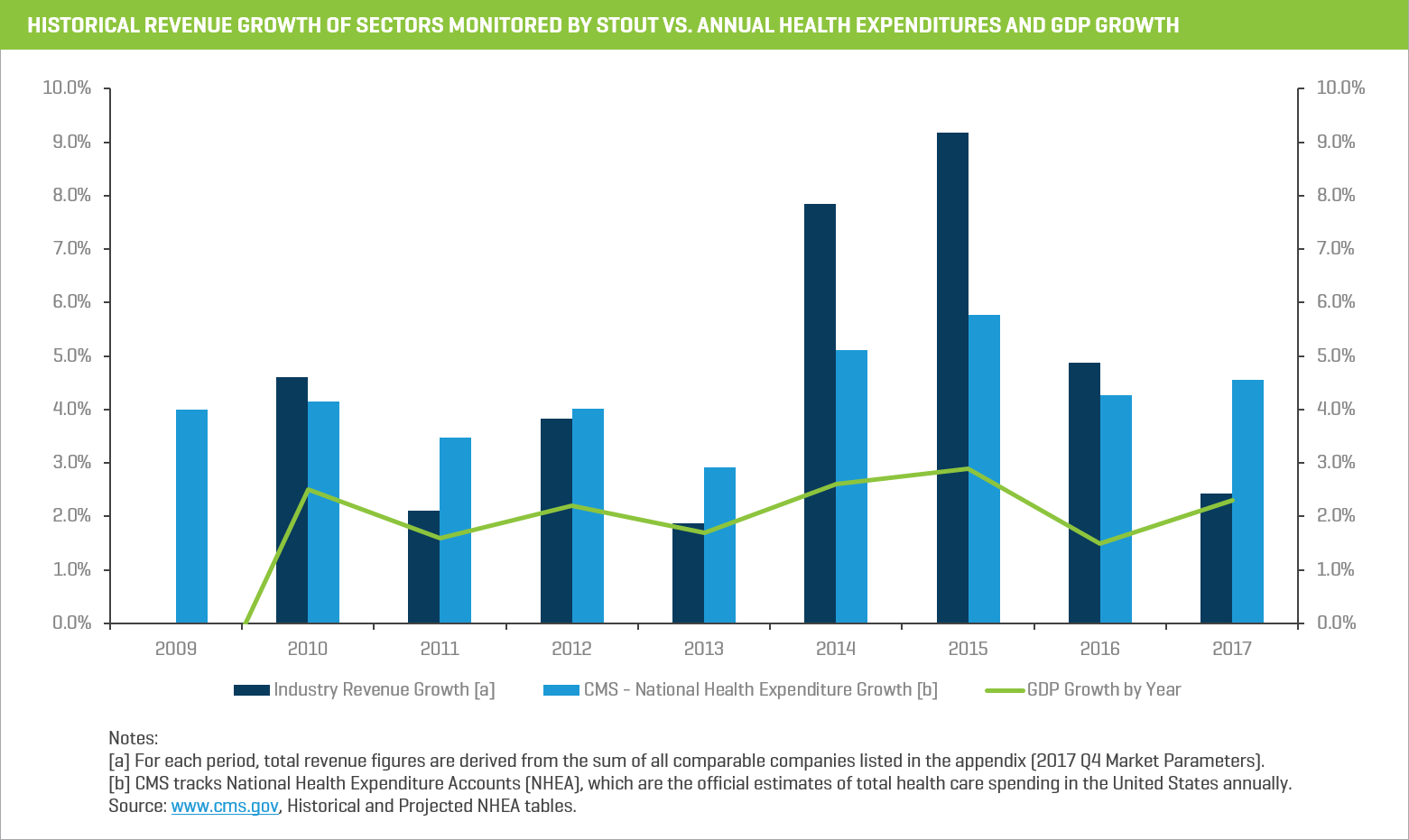

As of this writing, the market has been volatile of late due to concerns about the Fed and the potential for rising inflation and interest rates. Healthcare reform rhetoric has died down in Washington after the administration failed to get reform (Repeal and Replace) legislation passed. It looks like the administration will tackle healthcare spending and regulatory issues piecemeal rather than in a comprehensive plan. Using the aggregate revenue growth (across all healthcare verticals) of the companies listed in the “Healthcare Public Company Analysis” in this report, it looks like healthcare spending only grew about 2.5% in 2017, which is in line with gross domestic product (GDP) growth for the year. Healthcare cost containment measures, at least by this measure, seem to be working. Maybe a complete overhaul of healthcare will not be necessary if the existing regulatory framework and market forces can constrain expense growth in 2018 and 2019.

The Centers for Medicare and Medicaid Services (CMS) previously reported that in 2016 U.S. healthcare spending increased 4.3% to reach $3.3 trillion, or $10,348 per person. Healthcare spending growth decelerated in 2016 after the initial impacts of ACA coverage expansions and strong retail prescription drug spending growth in 2014 and 2015. The overall share of GDP related to healthcare spending was 17.9% in 2016, up from 17.7% in 2015.

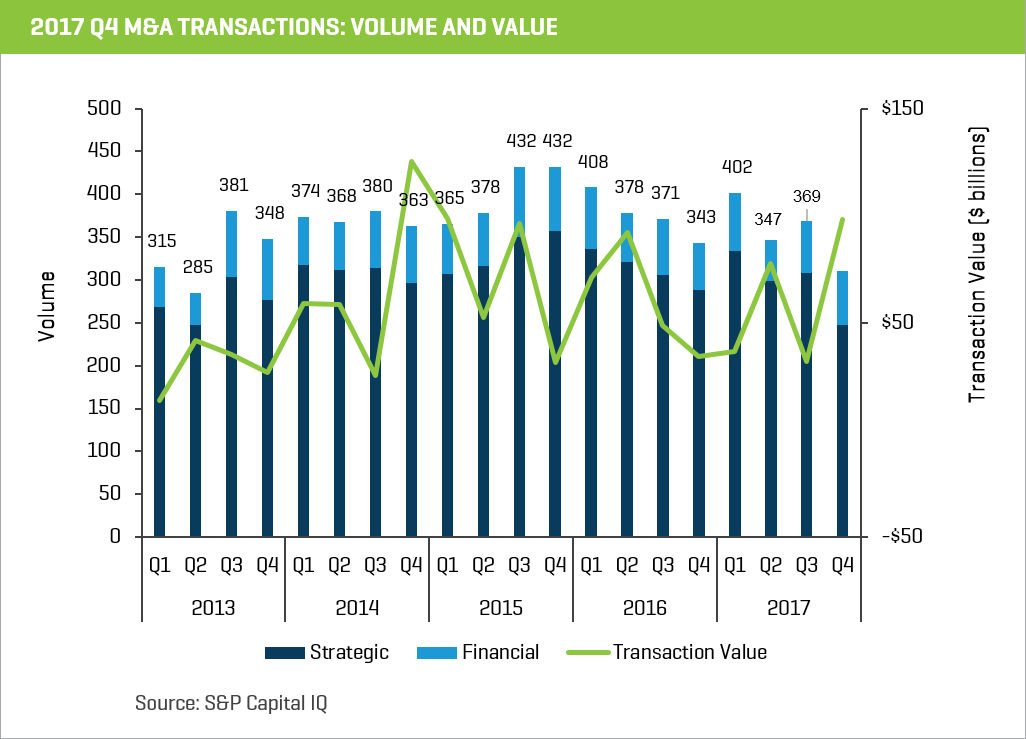

The fourth quarter of 2017 saw the lowest level of M&A activity (310 Transactions) in healthcare since the second quarter of 2013 (285 transactions), but the year itself was another period of healthy activity, which we expect to continue given that interest rates remain low, multiples are high, and private equity has plenty of dry powder for acquisitions.

Recent Healthcare & Life Sciences Trends

Physician Practice Management

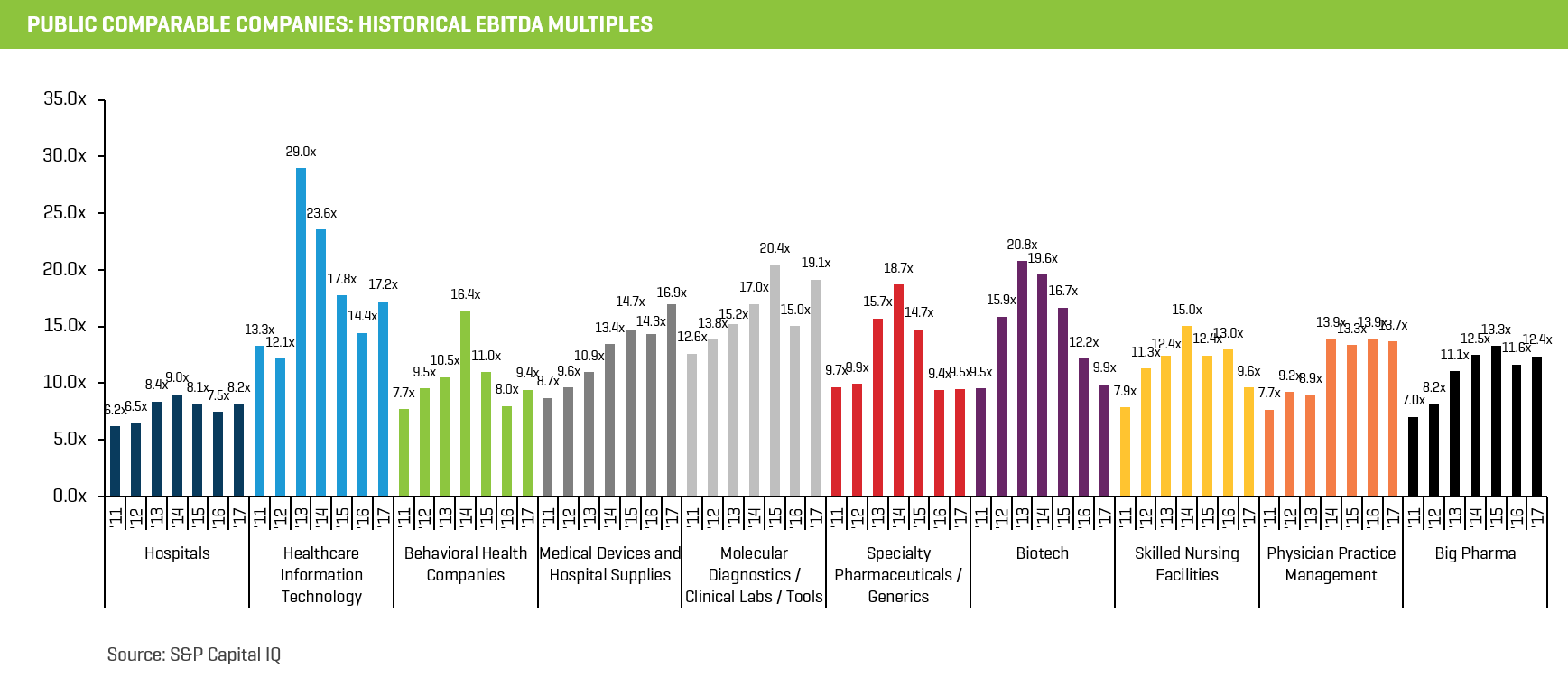

The large public multidisciplined physician practice management companies are trading at 12.5x LTM EBITDA, and this is consistent with where acquisitions of large private platform are happening in the sector. The big news in this space late last year was UnitedHealth (Optum) announcing plans to buy Davita Medical Group for $4.9 billion. Review of the Davita financials indicates that 2017 adjusted operating income was about $52 million and the business has approximately $239 million in annual depreciation and amortization expense, yielding EBITDA of an estimated $291 million. This puts the EV to EBITDA multiple on the deal at about 16.8x. Revenues for DMG were $4.7 billion for full year 2017, putting EV to revenue at just over 1x.

Multiples vary by discipline, but in general smaller practices are being acquired from 7x to 10x and platforms are trading anywhere from 11x to 15x. This multiple arbitrage, in addition to acquisition and organic growth that can be achieved, creates a tremendous opportunity for private equity to continue to roll up this fragmented industry, particularly those areas with above average growth, favorable demographics, and a high cash pay component to their business and where reimbursement and regulatory pressures are less of a factor.

At a recent industry conference, a CEO of a large practice commented that he thought that the ophthalmology sector was only 2% consolidated. Factors driving ophthalmology practice growth include:

- Advanced multifocal lens adoption increasing as patients can correct presbyopia, near- and far-sightedness with a single procedure and Medicare only covers the basic cost of the surgery and implant for these premium lenses, while the patient pays the rest out of pocket

- New implants in development for the treatment of presbyopia (need for reading glasses caused by a different mechanism of action than myopia or hyperopia) could provide an additional revenue source for practices

- New drugs for both wet and dry age-related macular degeneration could drive higher revenue and/or profit growth for retinal practices in the future, and payor-incentive payments for use of lower cost drugs (for example, Avastin versus Lucentis or Eylea) could boost practice profitability

- Co-management and consulting with optometrists could lead to more medical testing and screening of patients for conditions like diabetic retinopathy that in turn lead to more referrals;

- A shortage of ophthalmologists could limit pressure on reimbursement and keep demand high for existing practices

- The demographics of an aging population should continue to drive an increase in patient count

Since the beginning of 2013, there have been over 40 large practices acquired in ophthalmology with PE firms including: Waud, Shore Capital, Cortec Group, Blue Sea Capital, HIG, Sterling Partners, Flexpoint Ford, Harvest Partners, Audax, and others having made platform acquisitions.

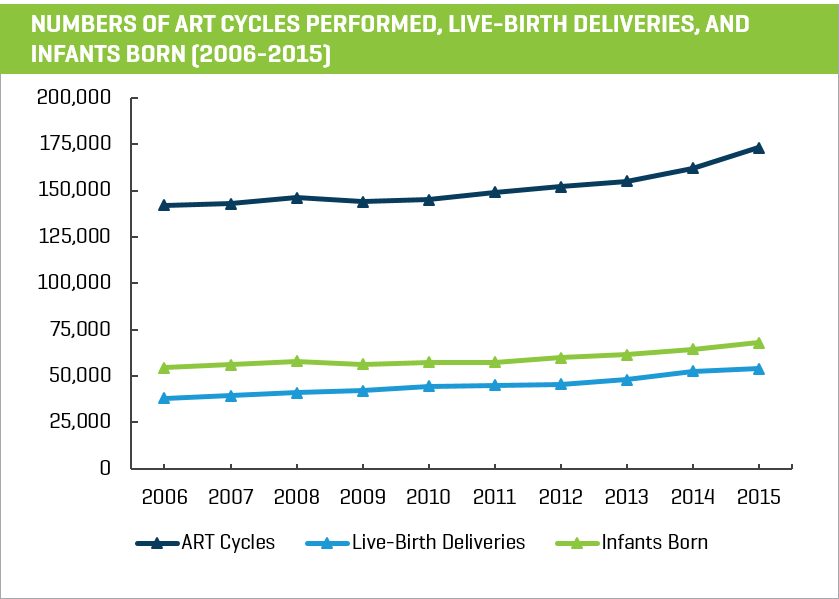

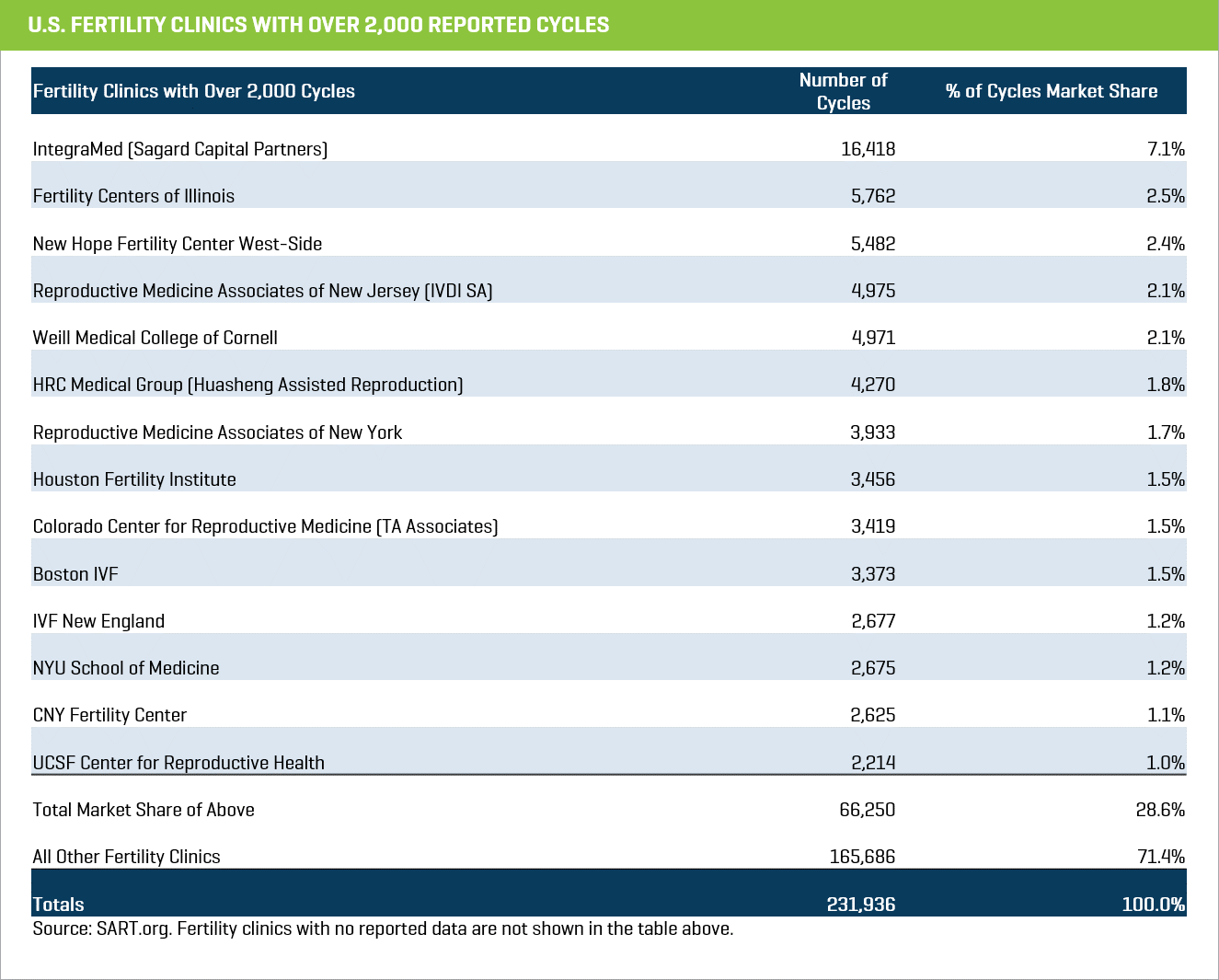

Fertility clinics are another sub-segment of physician practice management of keen interest as there is a large private pay mix, the industry is growing and very fragmented, and not yet picked over. According to IBISWorld, U.S Fertility clinic industry revenue grew to an estimated $1.91 billion in 2017 from $1.88 billion in 2016, and has grown at a rate of over 4.0% annually over the last five years. Industry growth has accelerated in recent years due to couples having delayed family starts in the past (as couples pursue financial stability), wider availability of insurance coverage, improved fertility success rates in assisted reproductive technologies (ART), higher disposable income from an improving economy, and moderating treatment costs. It appears that growth in the number of cycles has been partially offset by greater availability of insurance coverage for fertility treatments and associated pricing pressures, but this still appears to be a growth opportunity for well managed practices barring regulatory interference.

Behavioral Health – Substance Abuse Treatment in a Perfect Storm

Imagine needing treatment for a loved one and having to contend with an insurance company denying admissions or treatment for that person. It’s a perfect storm in substance abuse treatment right now with insurance companies cutting per diem rates for treatment and trying to partner for in-network contracts while limits placed on the use of Google keywords have crimped the ability of many providers to generate leads/referrals to their websites and call centers. Federal task forces cracking down on bad actors who participated in body brokering schemes or excessive or fraudulent billing for residential treatment or urinalysis is probably good in the long run but has also blemished the industry’s reputation.

We suspect that insurers are tired of paying, often repeatedly, for residential treatment for patients when they are not seeing much in the way of favorable results from cost outcomes studies. We do think that there is a real need for outcomes data, and, in fact, Stout has a group dedicated to predictive analytics and working with providers to help forecast what outcomes will be for a given admission. That data could be used to influence admissions and subsequently used by providers to obtain contracts or favorable reimbursement from payors.

In any event, the opioid crisis is not going away and politicians and payors alike need to address the problem and treat patients, so the investment opportunity exists in this space. We think that one of the main problems is that patients are treated for too short a timeframe. It seems like 60 days of treatment might simply be too short for many patients. They probably need a year of therapy in many cases, albeit maybe not in an inpatient or full residential treatment setting. A bill introduced in Congress late last year makes us wonder if Sober Living could end up being more widely adopted and reimbursed as part of an extended treatment regimen once SAMHSA does more to establish best practices.

In December of 2017, Rep. Judy Chu (CA-27), joined by nine other bipartisan Members of Congress, introduced the Ensuring Access to Quality Sober Living Act. This bill would authorize the Substance Abuse and Mental Health Services Administration (SAMHSA) to develop best practices for recovery residences that promote sustained recovery from substance use disorders. Recovery residences, often known as sober homes, are family-like, shared living environments that are free from alcohol and illicit drug use, and centered on peer support and connection to services that help individuals just out of treatment continue on their journey to recovery.

Skilled Nursing Facilities

CMS’ Final Rule for Fiscal 2018 will increase payments to SNFs by an estimated 1%, or $370 million, from payments in fiscal year 2017. This estimated increase is attributable to a 1 market basket increase required by section 411(a) of the Medicare Access and CHIP Reauthorization Act of 2015 (MACRA). Some of the other reimbursement changes introduced for SNFs include the adoption of a value based purchasing program whereby CMS, beginning in 2019, will hold back 2% of per diem payments to cover the cost of implementation of a SNF Value Based Purchasing Program. Providers will have an opportunity to recapture up to 60% of the amount held back, but providers that fail to meet cost/quality metrics could lose these payments.

We understand the reimbursement challenges that SNFs are confronted with but with an aging population, limited industry capacity, an average capitalization rate of 12% and rationalization of competition, we think there are some very good investment opportunities to be had in this sector. Those willing to accept that reimbursement pressures will continue, and those able to dig in and proactively manage the business to take advantage of opportunities to increase referrals, improve productivity and case mix, and lower costs will be poised to take advantage.

Medical Devices and Hospital Supplies

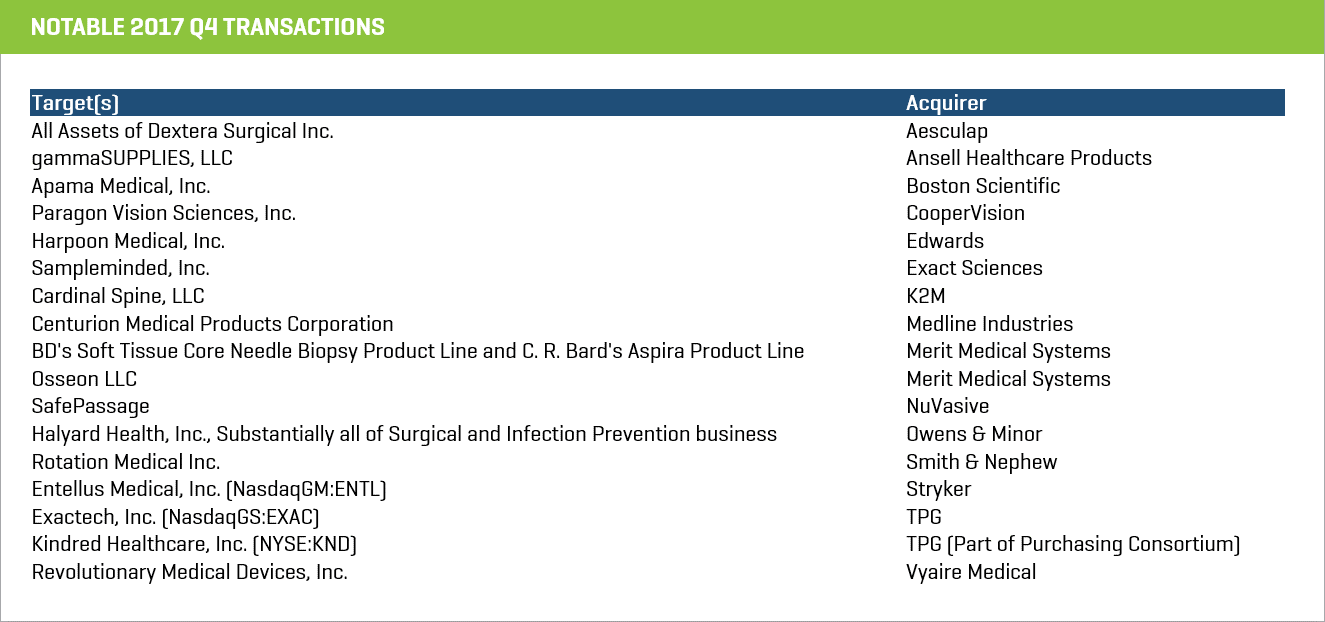

The medical device and hospital supply sector remains quite healthy as margins remain high on proprietary medical technology, the large manufactures have oligopoly-like positions in their respective segments (for example cardiovascular versus ortho-spine), and are achieving enhanced bundling capability (broad product offering leads to greater importance to customer) and economies of scale (margin benefit from distribution leverage and integration cost savings). Most of the transactions lately have been tuck-in acquisitions to either expand the market leader into an adjacent market or to improve their market position in an existing surgical arena with a paradigm changing technology. Given that the large manufactures are trading, on average, at 19x LTM EBITDA and the cost of capital is cheap it’s not surprising that M&A activity here remains pretty robust. We have provided a list of 15 of the transactions that took place in the medical device and hospital supply world during the fourth quarter of 2017 below: