English

English

The S&P 500 finished the second quarter of 2018 up 3.1% (up 1% year to date) as the Trump Administration’s corporate tax cuts as well as other pro-business policies continued to stimulate the overall economy and the market. Rising interest rates and trade-war rhetoric dampened greater upside in equity markets.

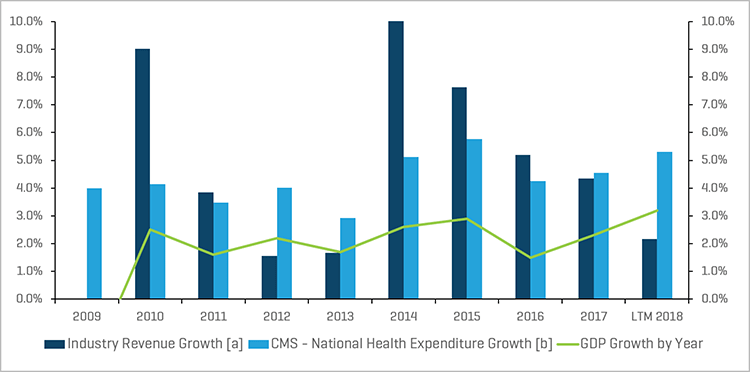

Healthcare stocks in the universe that we track outperformed the market in the second quarter, and they continue to be led by strength in the following segments: healthcare information technology (up 24.5%), medical devices (up 12%), molecular diagnostics and tools (up 17.3%), specialty pharmaceuticals (up 25.1%), and skilled nursing (up 20.9%). Volatility in the sector echoed that of 2017, largely attributable to ongoing concerns over drug pricing and the outlook for Medicare and Medicaid spending and reimbursement. Overall last-12-month (LTM) revenue growth for the healthcare segments that we track was only up 2.2%, with the specialty pharma, large pharma, and large biotech names ranging from -2% to 2%, impacted by patent expirations and competition. The medical devices and molecular diagnostics segments led with growth of 6%-7%. Specialty pharma/generic stocks rallied off of oversold/depressed levels as some firm's like Endo, Bausch, and Mallinckrodt stabilized their businesses despite concerns about competition, Pharmacy benefit managers pressuring prices, and Trump rhetoric/public sentiment that have discouraged price increases.

Historical Revenue Growth of Segments Monitored by Stout vs. Annual Health Expenditures and GDP Growth

Notes:

[a] For each period, total revenue figures are derived from the sum of all comparable companies in the universe that Stout tracks (Healthcare Public Company Analysis exhibit).

[b] CMS tracks National Health Expenditure Accounts (NHEA), which are the official estimates of total health care spending in the United States annually.

Source: www.cms.gov, Historical and Projected NHEA tables.

M&A Market Update

M&A Market Key Takeaways:

- Robust overall healthcare M&A activity echoing trends of the last several years

- Slight decrease in deal value and volume compared with same period last year

- Attractive valuation multiples due to a strong economy, liquidity, and still low rates

- A pro-business administration and lower corporate taxes

- Strategic consolidation in medical devices and molecular diagnostics

- Private equity interest in physician practice management roll-ups and acquisitions in other healthcare service segments

M&A Market Outlook

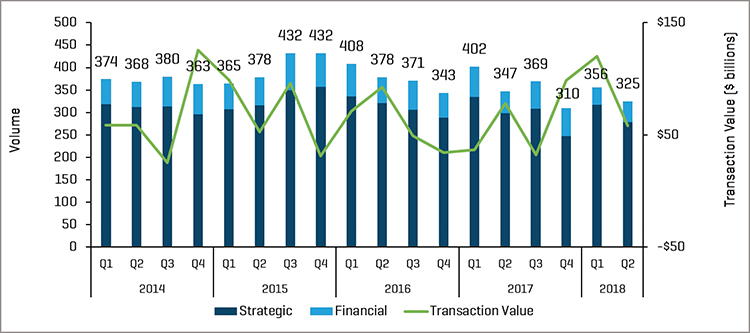

The second quarter of 2018 experienced a continuation of robust M&A activity, fueled by record amounts of private equity dry power and plenty of corporate strategic initiatives. Both deal value ($58 billion) and volume (325 transactions) dipped compared with the same period last year (347 transactions). Still, the quarter performed in line with the high level of activity that has held since prior to 2014, and we see this continuing, barring an increase in interest rates or slower economic growth and a stock market correction.

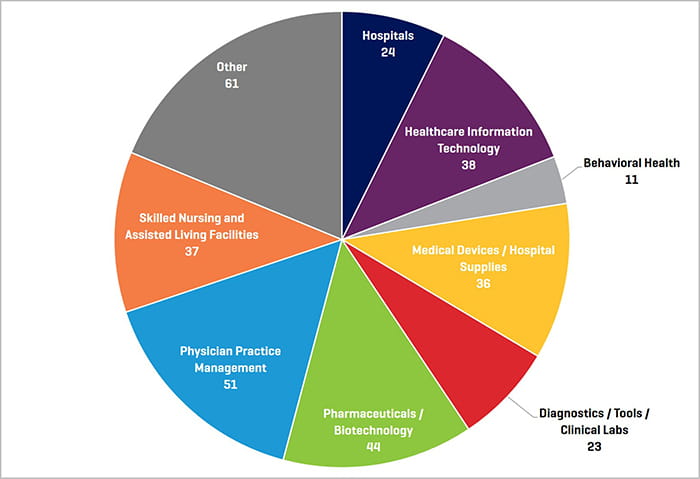

According to a recent survey by West Monroe, about one-third of private equity and strategic buyers listed attractive margins as the primary driver for pursuing healthcare transactions, with growing demand for care and an aging population being secondary motivators. Due to high demand for attractive targets in the space, steep competition has driven high multiples in a variety of segments. Physician practice management and biotechnology transactions led deal volume for the second quarter, with skilled nursing and healthcare information technology following closely behind.

Q2 2018 M&A Transactions: Volume and Value

Source: S&P Capital IQ and Stout Industry Research

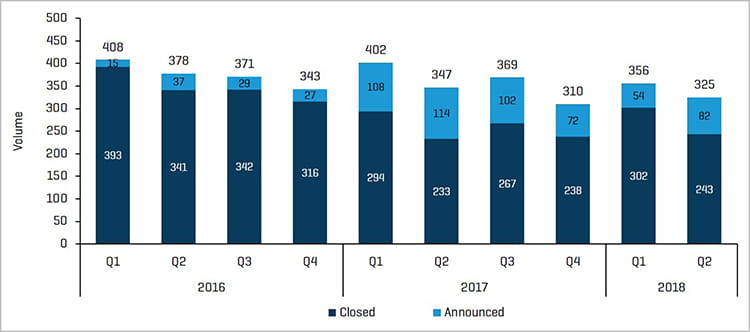

Historical M&A Transactions: Announced vs. Closed

Source: S&P Capital IQ and Stout Industry Research

Q2 2018 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

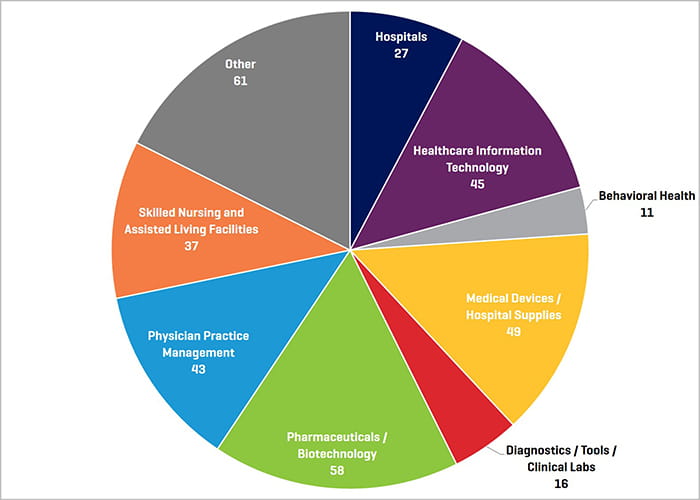

Q2 2017 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

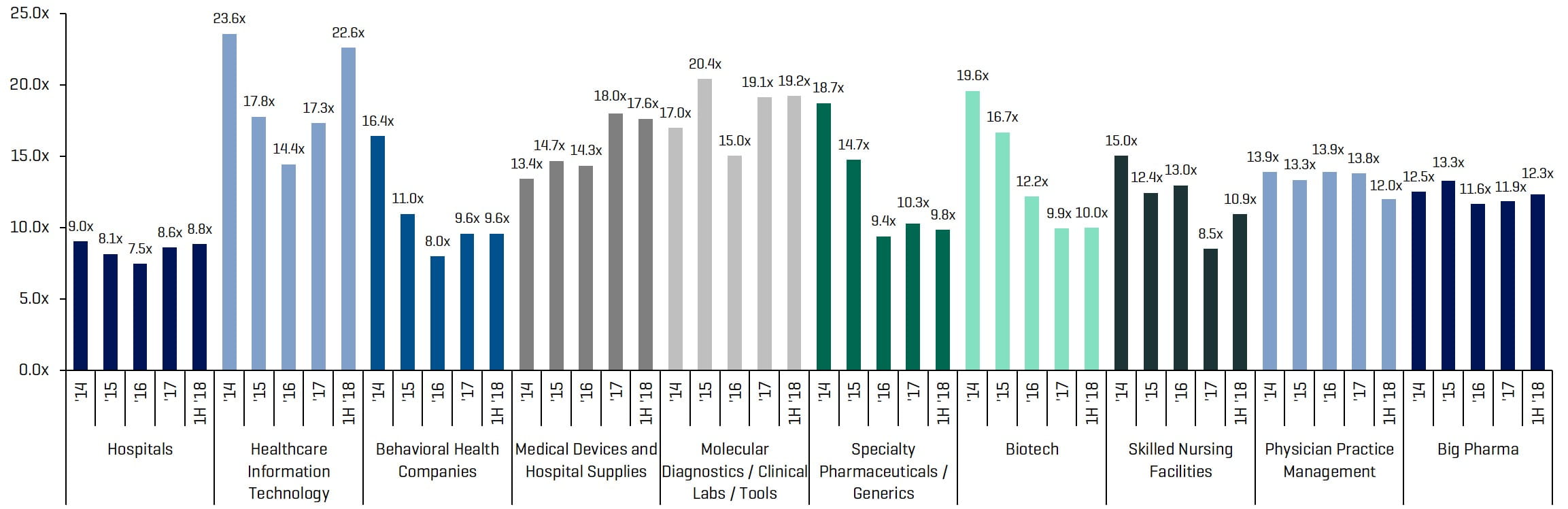

Public Comparable Companies: Historical EBITDA Multiples

Click to view full size chart

Source: S&P Capital IQ; Multiples calculated from comparable companies universe that Stout tracks

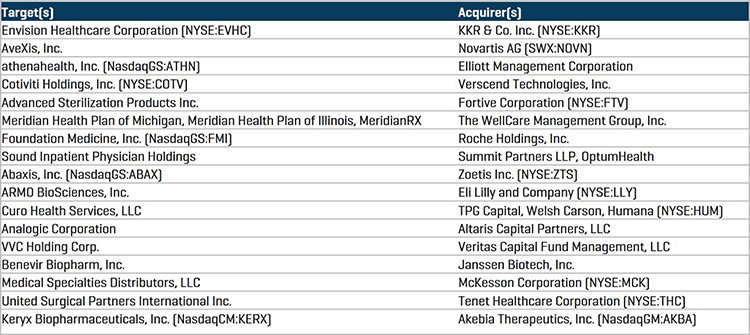

Notable M&A Transactions

Private equity firm KKR & Co. (NYSE:KKR), announced its acquisition of physician staffing group Envision Healthcare Corp. (NYSE:EVHC) for $9.9 billion, including debt. The transaction comes as KKR continues to build its healthcare portfolio of physician medical groups.

Summit Partners LLP and OptumHealth, a part of UnitedHealth Group (NYSE:UNH), announced their acquisition of physician staffing group Sound Inpatient Physician Holdings from Fresenius Medical Care for approximately $2.2 billion.

Global pharmaceutical company Eli Lilly and Co. (NYSE:LLY) completed its acquisition of biotech company ARMO BioSciences, Inc. (NASDAQ:ARMO) for approximately $1.6 billion. ARMO’s clinical immunotherapy drug pegilodecakin is being developed for the treatment of pancreatic cancer.

Swiss pharmaceutical giant Novartis AG (NYSE:NVS) completed its acquisition of gene-therapy company AveXis, Inc. for $8.7 billion. AveXis’ main drug, AVXS-101, seeks to treat deadly spinal muscular atrophy (SMA).

Activist fund Elliott Management Corp. announced an unsolicited bid for healthcare technology company Athenahealth, Inc. (NasdaqGS:ATHN), valuing the software maker at $6.9 billion, including debt. Athenahealth provides network-enabled services for healthcare and point-of-care mobile apps.

Veritas Capital-backed Verscend Technologies, Inc., a healthcare analytics company, announced its acquisition of payment accuracy company Cotiviti Holdings, Inc. (NYSE:COTV) for approximately $4.9 billion in cash.

Diversified industrials conglomerate Fortive Corp. (NYSE:FTV) announced its acquisition of medical sterilization company Advanced Sterilization Products Inc. from Ethicon, Inc., a subsidiary of Johnson & Johnson (NYSE:JNJ), for approximately $2.7 billion in cash.

TPG Capital; Welsh, Carson, Anderson & Stowe; and Humana Inc. (NYSE:HUM) completed their acquisition of hospice operator group Curo Health Services, LLC from Thomas H. Lee Partners for approximately $1.4 billion. The buying group intends to combine Curo with the hospice business of Kindred at Home.

Q2 2018 Largest M&A Transactions

Source: S&P Capital IQ

Recent Healthcare & Life Sciences Trends

Physician Practice Management – Increased Interest and Investment

Interestingly, there was a meaningful spike in the number of physician practice management deals either announced or closed in the second quarter, with 51 deals reported with an average EV/LTM EBITDA multiple in the 12x range. The deals in this segment were spread across a wide range of subspecialties (dermatology, ophthalmology, radiology, GI, etc.), so the interest is broad. Now that quite a few platforms have been established, add-ons are likely starting to have an impact on the number of quarterly transactions, and we suspect that these numbers could move higher going forward. We continue to think that ophthalmology, dermatology, dental, and fertility are great subspecialties for investment and for private equity to add value by bringing in consumer-focused marketing resources; introducing more advanced revenue cycle management, billing, scheduling and information systems; and building scale to improve contracting terms with parties such as payers or vendors.

Behavioral Health – An Untapped Market Opportunity

M&A activity in behavioral health appears to have fallen off, with only 11 deals occurring in the segment during the second quarter. Not surprisingly, it is presently difficult for private equity buyers to predict how all of the current industry disruption is going to shake out.

To recap, the segment is facing reimbursement cuts (cuts in per diem rates for residential treatment), tougher insurance reviews and adjudication for medical necessity of residential treatment, reduced length of stay in residential treatment, loss of patients to outpatient and medication-assisted treatment, federal task force investigations, insurance audits and clawbacks, and changes in the way providers can recruit patients using search engine optimization (Google keyword changes have made patient acquisition more difficult). We have also heard some say that payers are attempting to restrict patients to in-state treatment.

Nonetheless, behavioral health is a large, fragmented market opportunity, and we believe there are plenty of exciting investment opportunities in the segment for those that get the business model correct. The U.S. spends about $36 billion a year on addiction treatment, and only a fraction of those who need help are actually getting care. We expect this market will continue to grow as the country grapples with an opioid crisis that has become a very public and political issue.

We anticipate that private equity buyers will be most interested in outpatient clinics where medication-assisted treatment is delivered (given the payer trends), but residential treatment is critical to managing these disorders and represents a real opportunity for a well-managed consolidator that studies outcomes and can provide payers with a proven model.

Medical Devices and Molecular Diagnostics – New Technologies Lead the Way

Above-average growth, high margins, and consolidation continue to drive stellar performance for medical devices and molecular diagnostics, as does an increase in patient age, surgeries performed, and new proprietary technologies. The movement of a growing number of patients to the outpatient setting will continue to put pressure on hospitals and bolster these segments. Robotics, new methods of neuromodulation, telemedicine, trans-catheter valves, lens implants, personalized genetic testing, improvements in imaging modalities, continuous glucose monitoring and insulin delivery for diabetes, aesthetic dermatology treatments like HydraFacial, and many other technologies represent large, incremental growth opportunities for both medical devices and molecular diagnostics.

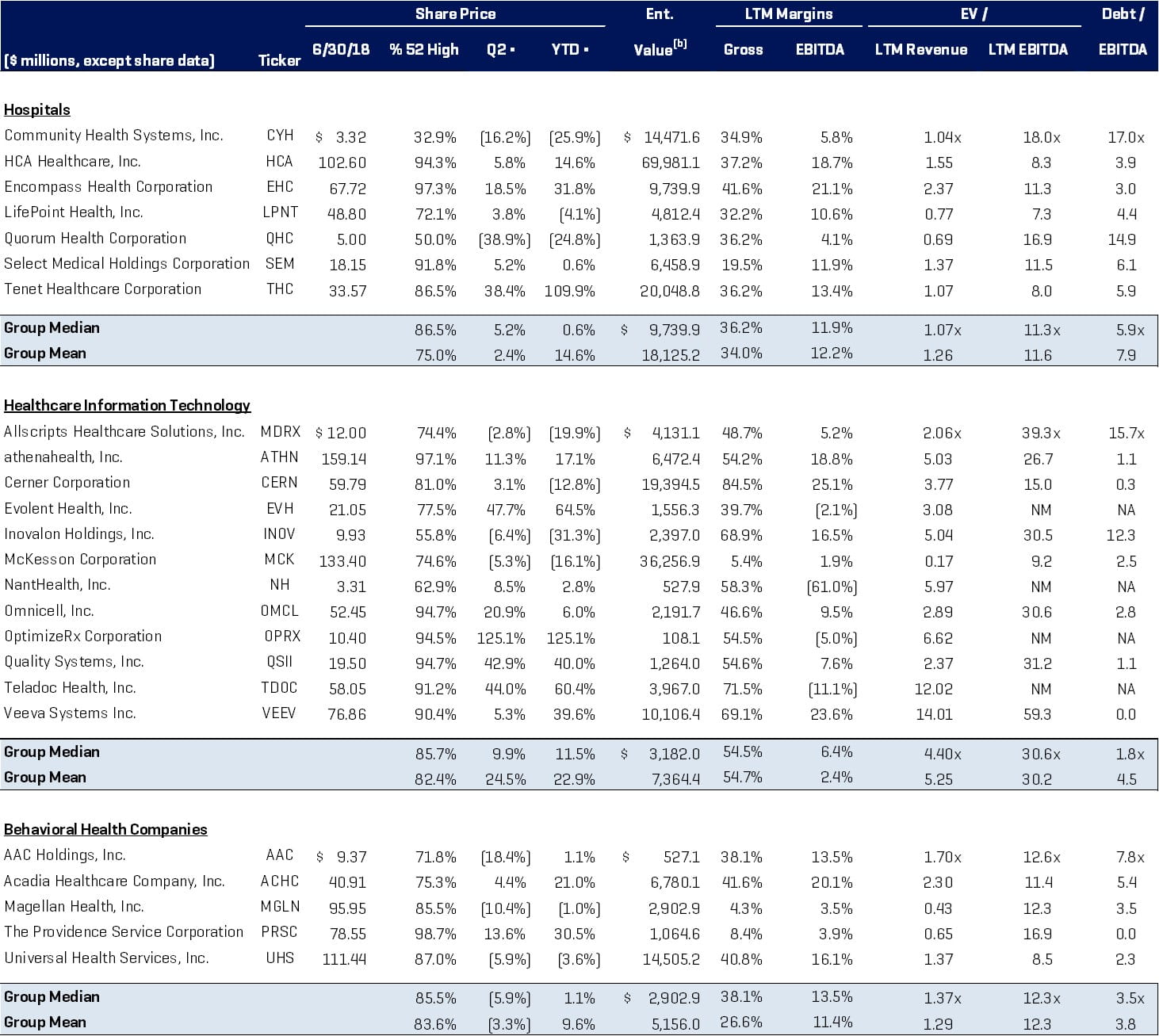

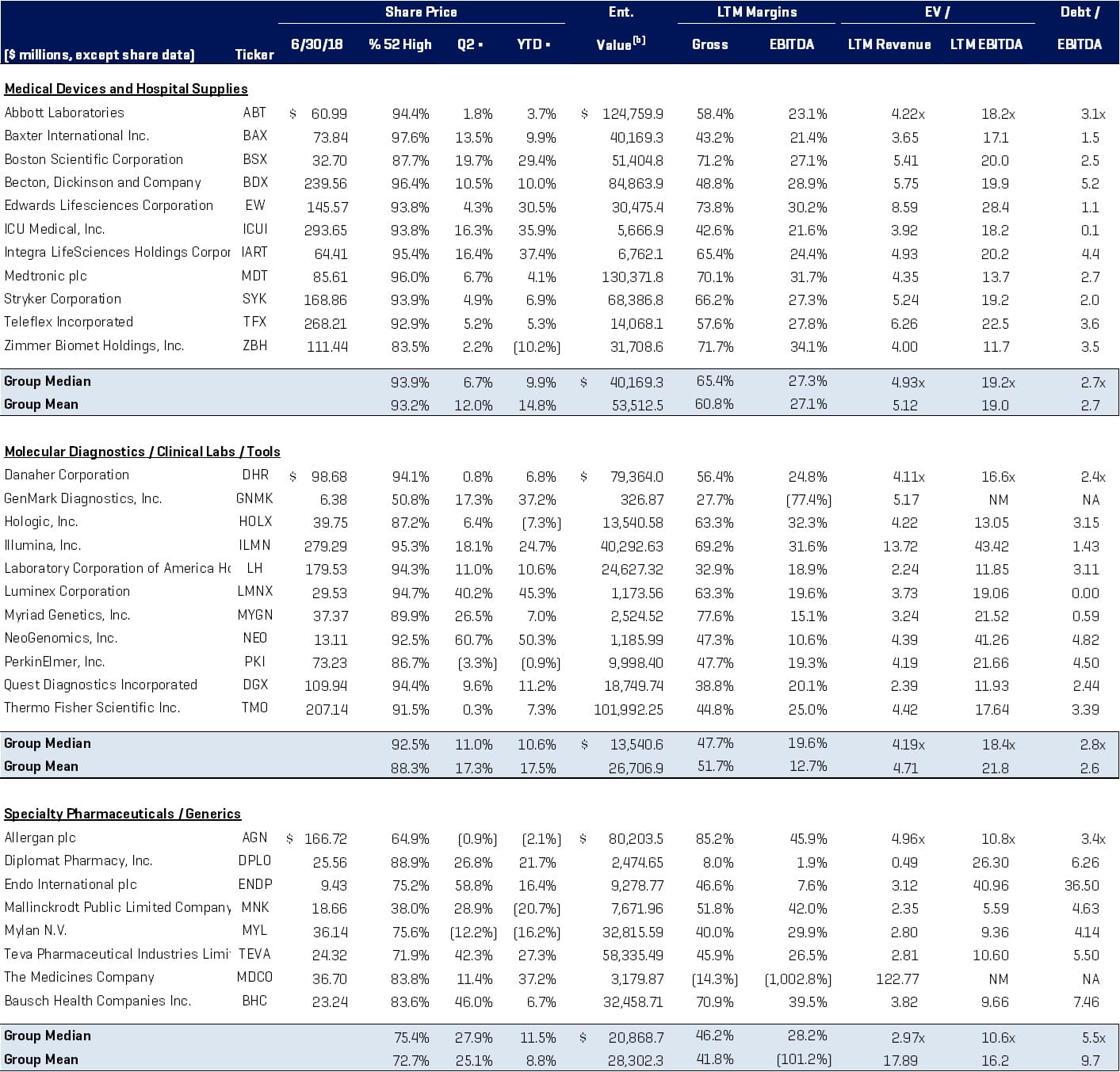

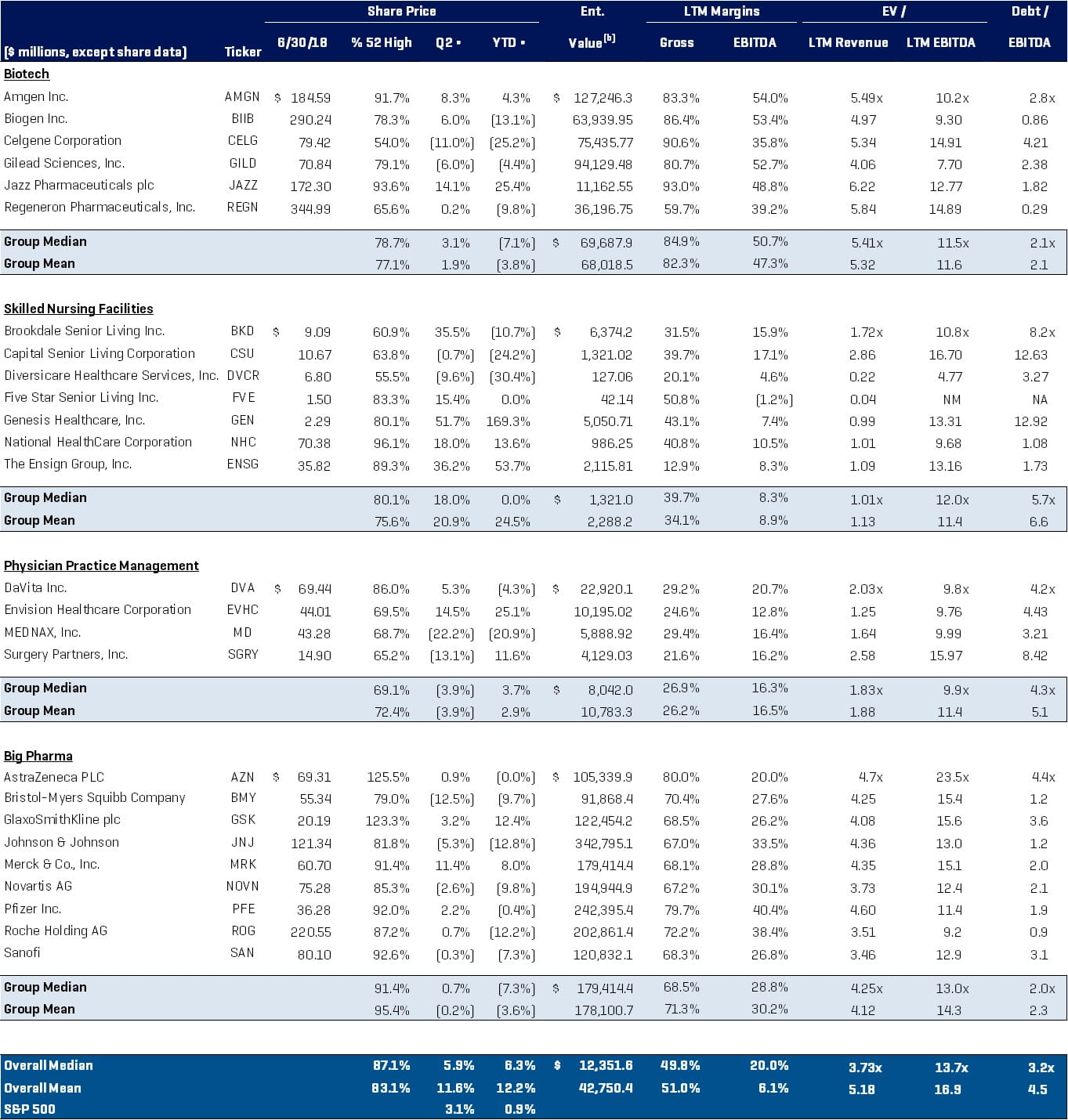

Healthcare Public Company Analysis