English

English

The healthcare industry continues to experience broad merger and acquisition (M&A) activity across a number of sectors. Amid a rising number of transactions, financial buyers appear to be looking to expand further into the space, particularly ophthalmology.

There is presently a significant interest from private equity, private equity-backed management service organizations (MSOs), large independent medical groups, and well-resourced multi-specialty physician groups in acquiring physician practices. This is likely due to public pension funds, endowments, and family offices seeking diversification via the private equity asset class in light of its perceived superior return potential as well as the opinion of many that valuations in the public equity markets are stretched. A low-interest-rate environment, which allows buyers to employ debt to boost returns on invested capital, has also contributed to healthy M&A activity and industry consolidation.

The organic growth opportunities that exist in ophthalmology, private pay components of certain procedures, and the sector’s fragmented ownership structure make it an especially attractive segment for private equity. Conversely, physicians are having to contend with changing technology, regulations, reimbursement systems, and rates instead of spending more time with patients, expanding their practice with new physician hires, building new locations. and negotiating new and incremental contracts with payors. These factors, as well as historically high earnings before interest, taxes, depreciation, and amortization (EBITDA) multiples being paid for practices at present, have inspired physician practice owners to pursue or at least inquire about a sale. The multiples available to practice owners today, in our view, allow them to de-risk their financial future considerably. We believe that any independent practice with more than $5 million in EBITDA should seriously consider an exit.

Another consideration is that insurance groups (e.g., UnitedHealth/Optum) are looking to manage population health. Thus, they will want to acquire practices to be able to service members across a wide geography to ensure their plans are competitive and attractive to employer groups. We have not seen as much activity from insurance buyers in ophthalmology, but we are seeing it in multi-specialty groups.

Ophthalmology Market Summary

Factors driving ophthalmology practice growth include:

- Advanced multifocal lens adoption is increasing as patients can correct presbyopia, myopia (near-sightedness), and hyperopia (far-sightedness) with a single procedure. Additionally, Medicare only covers the basic cost of the surgery and implant for these premium lenses, while the patient pays the rest out of pocket. This leads to very high profitability on advanced lenses.

- New implants in development for the treatment of presbyopia (need for reading glasses caused by a different mechanism of action than myopia or hyperopia) could provide an additional revenue source for practices, although some of the manufacturers of corneal in lays for example have recently had setbacks.

- New drugs for both wet and dry age-related macular degeneration could drive higher revenue and/or profit growth for retinal practices in the future. Conversely, payor-incentive payments for use of lower-cost drugs (e.g., Avastin versus Lucentis or Eylea) could potentially boost practice profitability if the margin granted is sufficient. The government is evaluating new drug buying programs that could adversely impact margin on J-code drugs in the future, so this is a potential offset.

- Co-management and consulting with optometrists could lead to more medical testing and screening of patients for conditions like diabetic retinopathy that in turn lead to more referrals.

- A shortage of ophthalmologists could limit pressure on reimbursement and keep demand high for existing practices.

- The demographics of an aging population should continue to drive an increase in patient count.

- The forecast of cataract cases is expected to approach 50 million by 2050, according to the National Eye Institute, up from around 25 million cases today.

M&A Activity and Dynamics

Consolidation is by no means limited to ophthalmology as a number of large multi-specialty practices were acquired last year. The big news in this space late in 2018 was UnitedHealth (Optum) announcing plans to buy DaVita Medical Group for $4.9 billion.

Review of DaVita’s financial statements indicates that 2017 adjusted operating income was about $52 million and the business has approximately $239 million in annual depreciation and amortization expenses, yielding estimated EBITDA of $291 million. This puts the enterprise value (EV)/EBITDA multiple on the deal at about 16.8x. Revenues for DaVita were $4.7 billion for full-year 2017, putting EV/revenue at just over 1x.

Multiples vary by discipline, but in general smaller practices are being acquired from 7x to 9x, and platforms are trading anywhere from 11x to 15x, tending toward the mid to high end of this range recently. This multiple arbitrage, in addition to acquisition and organic growth that can be achieved, creates a tremendous opportunity for private equity to continue to roll up this fragmented industry, particularly those areas with above-average growth, favorable demographics, and a high cash-pay component to their business, and where reimbursement and regulatory pressures are less of a factor.

At a recent industry conference, a CEO of a large practice commented that he thought that the ophthalmology sector was only 2% consolidated, indicating a tremendous opportunity for consolidation. That number is a bit dated, but we would still say that it likely remains far less than 10% consolidated.

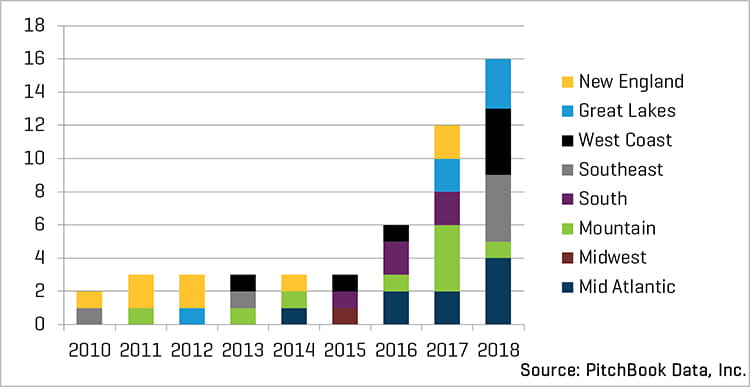

According to PitchBook, there were 16 ophthalmology practices acquired in control transactions in 2018 versus twelve in 2017. We expect the level of activity to remain at this healthy level going forward as more private equity money finds opportunities in the sector. [See figure 1]

US PE Activity (#) in Ophthalmology by Region

Ophthalmology practices that are well-managed can achieve 20% EBITDA margins due to high profitability on cataract procedures that use advanced lenses, for example. This favorable financial profile is attractive to private equity sponsors looking to enter the sector.

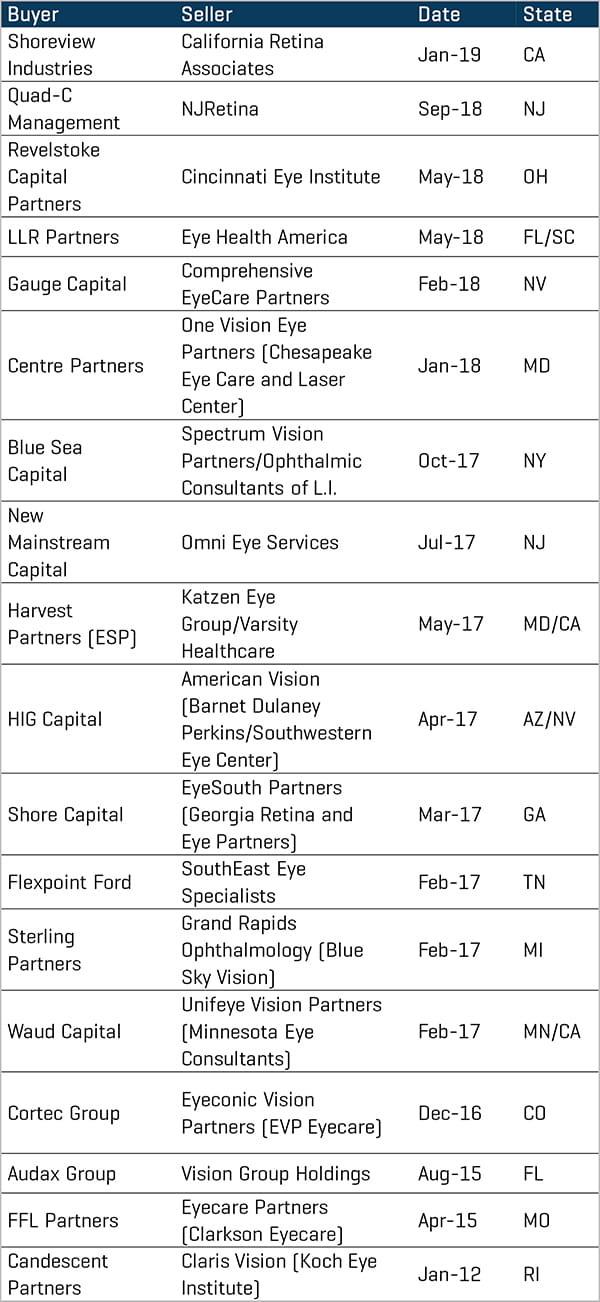

We have highlighted a number of the large platform acquisitions that have taken place in the industry since 2015. We would note that our experience indicates a large number of willing buyers in this market, which bodes well for practices evaluating whether to run a sale process.

Significant Platform Acquisitions

Considerations for Owners

In preparation for a sale process, there are some unique aspects of ophthalmology practices that owners should consider.

- Most practices are compiling their financial statements on a cash or tax basis, and they often do not have a true sense of their earnings on a generally accepted accounting principles (GAAP)/accrual basis. They typically pay out all practice earnings to the owners at year-end and have items (add-backs) that they expense for the business, that are personal or one-time in nature.

- These personal expenses and one-time expenses would, of course, be added back to EBITDA to arrive at adjusted EBITDA to appropriately reflect the business’ ability to generate cash flows. Identifying all of these add-backs is critical as the value of the business at sale will be based on a multiple of adjusted EBITDA.

- If the practice decides to hire an investment banker to run a sale process, physician compensation will need to be adjusted and restated in the financial forecast to reflect the fact that the practice, once sold, will no longer pay out all of the earnings at year-end. In addition, practice physicians will be signing employment agreements that include compensation or a salary that will ultimately be based on percentage of collections. This compensation adjustment should be made to the forecast, along with other add-backs or adjustments mentioned above.

- To understand the GAAP earnings of the practice, owners should consider doing a quality-of-earnings analysis that reflects industry norms for forecasted physician compensation and gives credit for the appropriate add-backs. A sell-side quality-of-earnings analysis can add credibility and validate the financial forecast that will ultimately be presented to potential buyers or investors.

- Proper organization and preparation of financial statements can be very helpful when considering a sale process. It is recommended to compile three years of monthly financial statements with uniformity in expense accounts to enhance comparability of revenue and expense items. Audited financial statements, if practical for the size of the business, would be ideal and obviate the need for a quality-of-earnings report.

- Timing of payment issues should be explored to make sure that big-ticket purchases for drugs at year-end, for example, are properly matched to period revenues to get an accurate GAAP earnings picture.