English

English

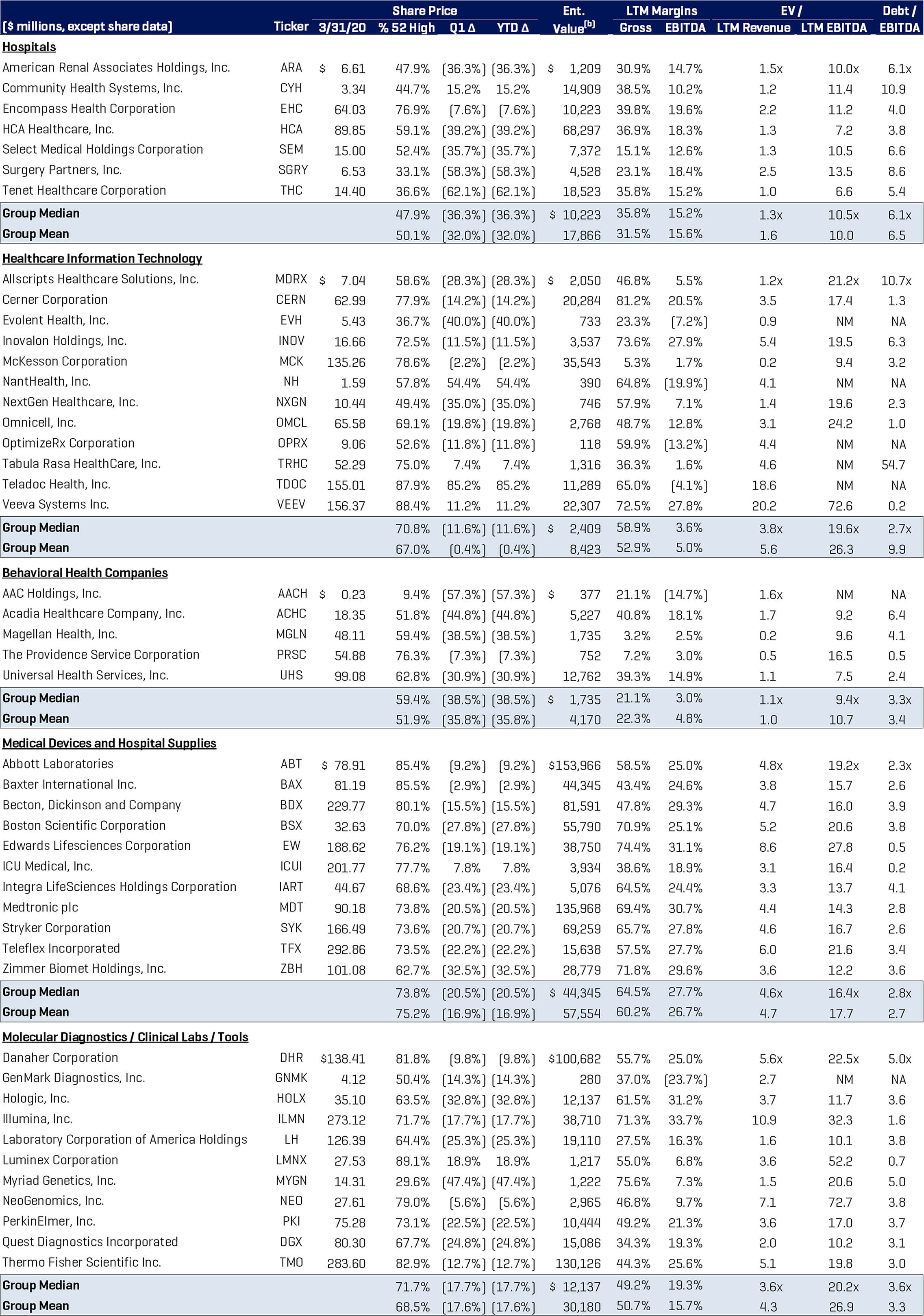

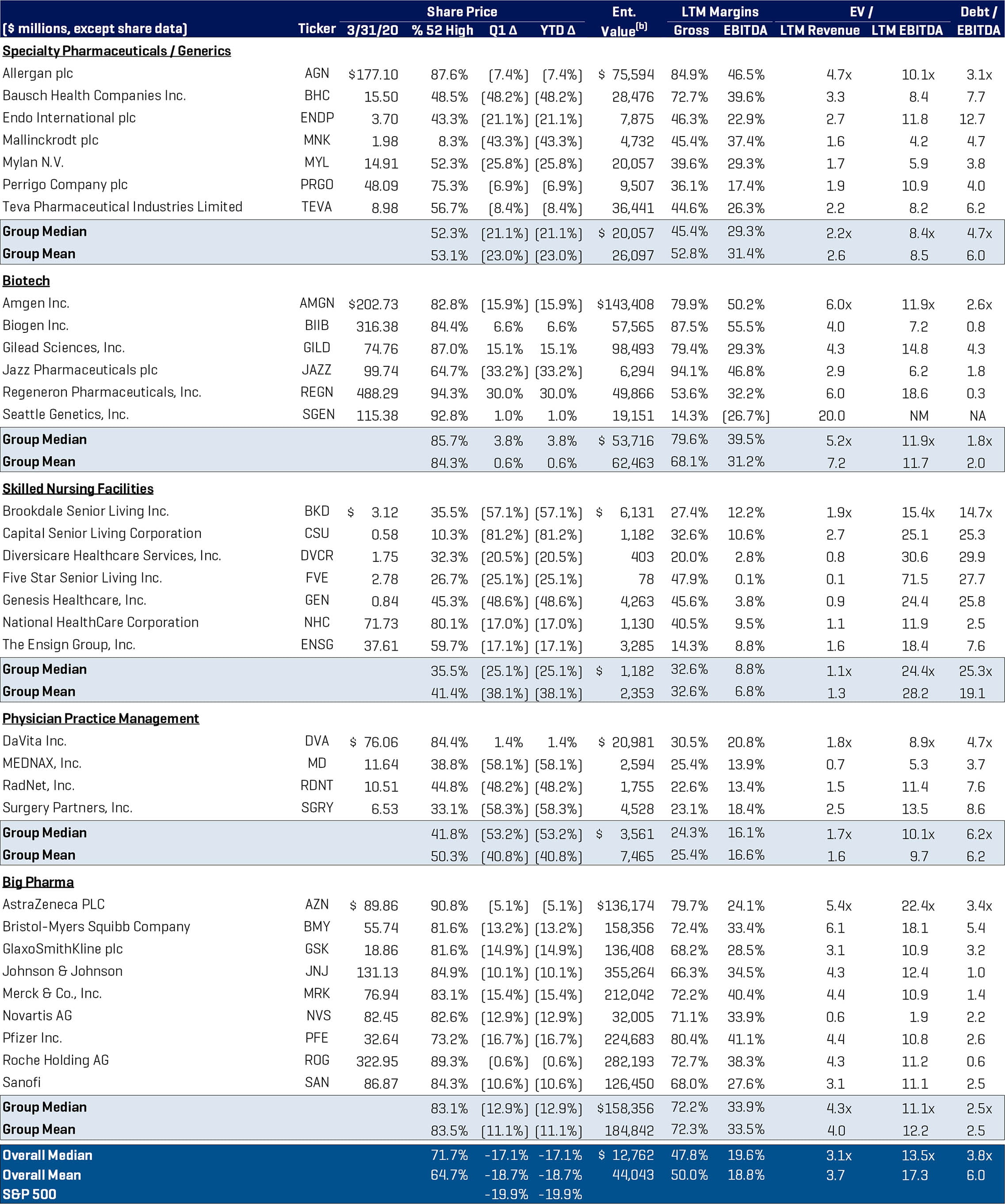

The S&P 500 dropped 19.9% during the first quarter of 2020, while the Healthcare Services and Life Sciences equities that we track in this report performed similarly, decreasing 18.7%. The devastating financial market and economic impact of the COVID-19 pandemic and related shelter-at-home policies restrictions began in mid-February and led to a market bottom in mid- to late March.

The two healthcare sectors that managed to avoid a decline were, not surprisingly, Biotech and Healthcare Information Technology, each positioned to benefit from COVID-19 in different ways. Biotech and large pharma are working on molecular diagnostic tests for diagnosis, antibody tests for monitoring, vaccines development, and antivirals, such as Remdesivir from Gilead Sciences. Regeneron and Gilead each traded up during the quarter.

Telemedicine has realized a significant windfall from COVID-19 as emergency measures have been adopted to provide for expanded patient access to telemedicine care and reimbursement for a broader range of services. Teladoc Health, Inc. was a big beneficiary and its stock jumped 85.2% in the quarter, a quarter that also saw them announce the acquisition of InTouch.

A few other individual stocks that performed well during the quarter included Community Health Systems, Inc. +15.2%, NantHealth, Inc. +54.4%, and Luminex +18.9%.

Big Pharma (-11%), Medical Devices and Hospital Supplies (-16.9%), Molecular Diagnostics/Clinical Labs/Tools (-17.6%), Specialty Pharmaceuticals/Generics (-23%), Hospitals (-32%), Behavioral Health (-35.8%), Skilled Nursing Facilities (-38.1%) and Physician Practice management (-40%) stocks were down double digits. This performance is pretty much what you would expect as we elaborate on down below in this report where we discuss sub-sector performance.

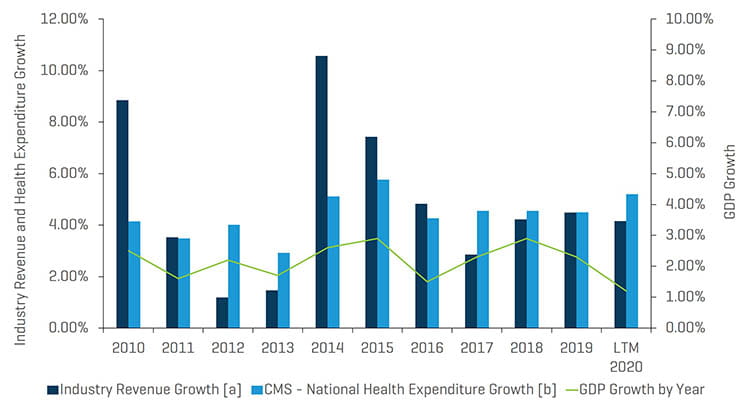

In the table below, you can see that Stout’s Healthcare Universe of companies saw last-12-month revenue grow 4% for March 2020, which was slightly above GDP.

Historical Revenue Growth of Segments Monitored by Stout Vs. Annual Health Expenditures and GDP Growth

Notes:

[a] For each period, total revenue figures are derived from the sum of all comparable companies listed in the appendix (Healthcare Public Company Analysis).

[b] CMS tracks National Health Expenditure Accounts (NHEA), which are the official estimates of total health care spending in the United States annually.

Source: www.cms.gov, Historical and Projected NHEA tables.

M&A Market Key Takeaways:

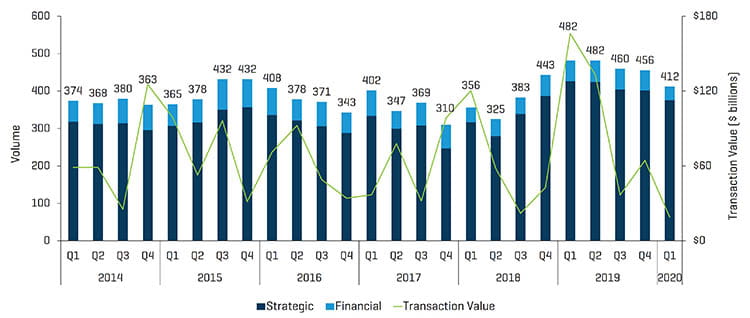

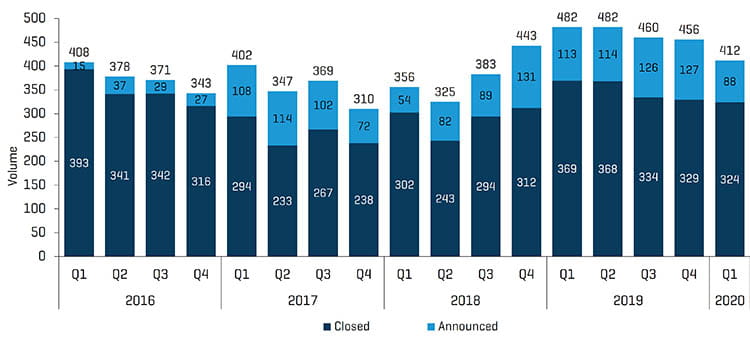

- M&A activity saw a significant drop off in healthcare in the first quarter of 2020 as deal volume came in at 412 transactions announced and/or closed, a decrease from a level of 482 transactions in the first quarter of 2019, due no doubt to the onset of COVID-19 and the shelter-at-home restrictions that began significantly slowing down the economy and delaying deal closures. We would note that an examination of the individual transaction data reveals that there were few closings since mid-March. Likewise, announced deals were at their lowest level in eight quarters.

- Overall transaction value of deals announced and/or closed in the first quarter of 2020 came in at roughly $19 billion compared with the previous year’s $166 billion, the lowest quarterly value in more than six years. We would note that the $90 billion merger of Bristol-Myers and Celgene in the year earlier period was one significant factor impacting the comparison. The other was the deal delays or terminations of discussions resulting from the COVID-19 pandemic.

- We would also mention that enterprise values are not reported for many private transactions, so total number of transactions is a more reliable metric. On the flip side, the largest transactions will generally involve a public buyer.

Q1 2020 M&A Transactions: Volume and Value

Source: Source: S&P Capital IQ and Stout Industry Research

Historical M&A Transactions: Announced vs. Closed

Source: S&P Capital IQ and Stout Industry Research

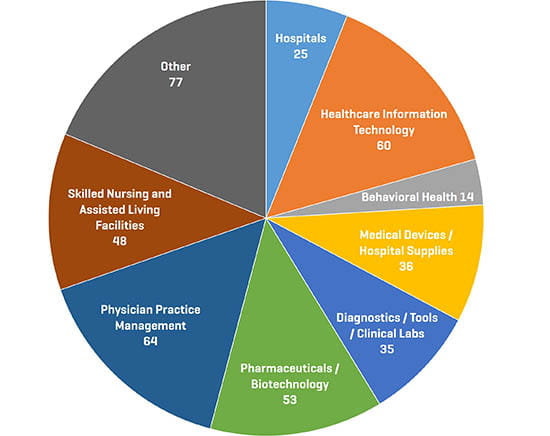

Q1 2020 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

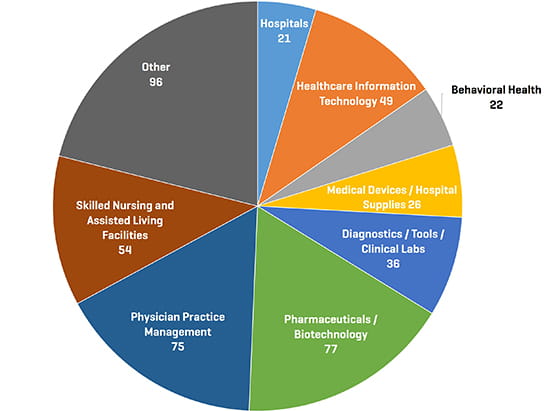

Q4 2019 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

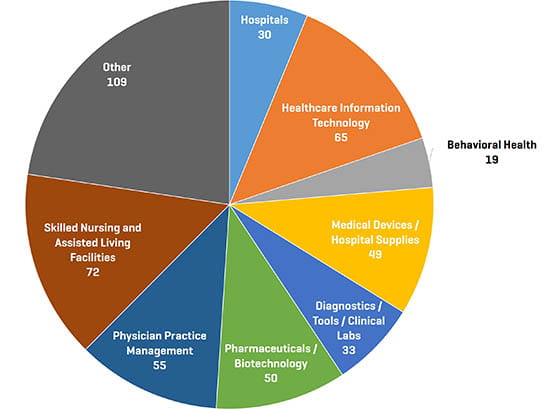

Q1 2019 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

Analysis of Healthcare Sub-Sector M&A Activity – Observations and Trends

Physician Practice Management, Healthcare Information Technology, and Pharma/Biotech remain the most active sectors with regard to number of transactions.

Consolidation of the Physician Practice Management sector experienced an uptick with 64 deals announced/closed in the first quarter of 2020, up from 55 in the year-earlier quarter.

Two notable private transactions closed in the quarter include Sun Capital Partner’s acquisition of West Dermatology and the Schweiger Dermatology acquisition of Advanced Dermatology. Physical therapy, ophthalmology, and orthopedic practices also saw activity during the quarter.

Healthcare Information Technology saw 60 transactions in the quarter versus 65 a year ago and 49 in the prior quarter. COVID-19 has increased and transformed payor coverage and adoption of telemedicine consultations across sub-specialties in a matter of months, and many believe that clinic visits and evaluations may be forever changed as a result. Interestingly, telehealth companies spent a decade struggling to transform the industry, in some cases even being forced to change their business model to pivot and adapt to a lack of previous adoption. The coronavirus pandemic has altered the landscape and increased market acceptance overnight. A notable transaction in this sub-sector in the quarter was Teladoc’s acquisition of InTouch Health. Telehealth solutions will continue to be an area of focus given the expanded reimbursement and scope of services that can be offered.

Acquisitions in this sector spanned a wide range of technology services during the quarter, including telehealth physician consultations and interpretive services, transcription, healthcare consulting, software for patient scheduling and lead/referral generation, software for electronic prescriptions, practice management, electronic health record and billing software, vendor management systems software, remote patient monitoring systems and software, inventory tracking and management software, IT services, support and security, etc.

Needless to say, this sector will continue to grow and consolidate as technology evolves to accommodate changes in: a) the delivery of care; b) healthcare practice size and structure; c) regulatory guidelines and reimbursement systems; and (d) adoption of value-based care and the need for analytics, among other factors.

Pharmaceuticals / Biotechnology realized a slight increase in deal flow increasing to 53 in the first quarter of 2020 compared to 50 in the first quarter of 2019, and a decrease from the previous quarter’s surprisingly high level of 77 transactions. A notable deal here was the Eli Lilly acquisition of Dermira in the dermatology sector. Many of the transactions in this sector are smaller reverse mergers for biotechs that fail a P3 trial and then become a vehicle for a private company to access the capital markets. We also saw a number of CBD related pharma company deals during the quarter.

Skilled Nursing and Senior Housing activity fell Off in the first quarter. There were 48 Skilled Nursing/Senior Housing deals in the quarter versus 72 in the year earlier quarter. After picking up significantly in 2019, it looks like activity here will subside for a while unless driven by distressed asset sales in the next few quarters. Highly publicized fatalities reported for COVID-19 in a select group of skilled nursing facilities is likely to impact census and financial results. We anticipate that covenant breaches could start to crop up for those leveraged operators after the second quarter of 2020, and our Special Situations team is here to help those in need of financial restructuring advice.

Medical device and supply transactions came in at 36 in the quarter and were down from 49 a year ago. There were a number of deals here in the ortho/spine and related osteobiologics sectors (bone graft materials), but most of the deals were smaller tuck in transactions. Deals in orthopedics and biologics included NovaBone Products (bone graft material), Tutogen Medical, Arthrosurface (minimally invasive joint resurfacing and biologics), and Parcus Medical (devices for sports medicine surgery). The advent of COVID19 is increasing demand for products like ventillators, pulse oximetry, oxygen therapies and concentrators, cytokine filters, nasal swab kits and COVID19 related diagnostics and antibody tests. As a result, some of the device sales lost for elective surgeries will be offset by increases in other areas. We do see a significant opportunity to consolidate the fragmented medical device OEM/contract manufacturing sector, where we are currently in market with a deal.

Diagnostics / Tools / Clinical Labs remained flat at 35 in Q1’20 compared to 36 in the previous quarter and slightly above 33 a year ago.

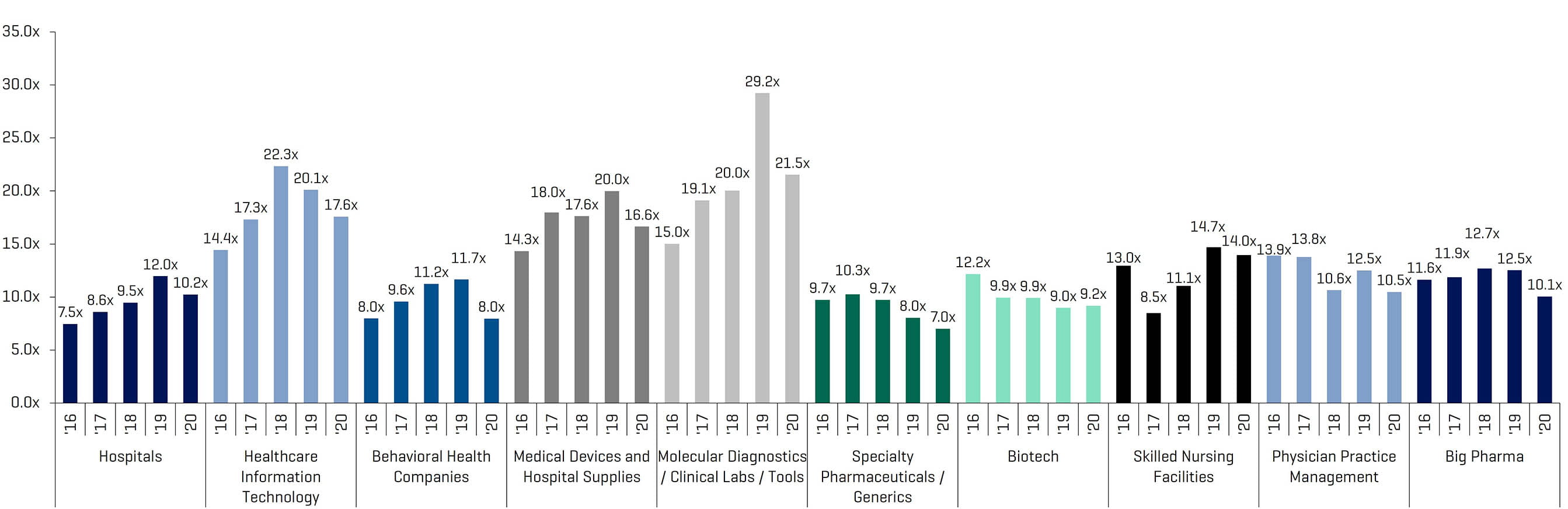

Enterprise Value to EBITDA multiples for the publicly traded sectors in this report expectedly decreased for all sectors except for a relatively flat performance from the Biotech group.

Public Comparable Companies: Historical and Forward EBITDA Multiples

Source: S&P Capital IQ; Multiples calculated from comparable companies universe that Stout tracks

Notable Q4 2019 M&A Transactions

DXC Technology sold its state and local health and human services business to Veritas Capital for $5 billion in cash or nearly 3x its annual revenue of $1.4 billion.

Gilead Sciences Inc. purchased Forty Seven Inc., a biotech company with a promising blood-cancer therapy. Gilead paid a nearly 65% premium at $95.50 per share for a purchase price of over $4.9 billion.

Eli Lilly and Company announced its successful acquisition of Dermira, Inc. to expand its dermatology pipeline.

Clarivate Analytics closed its acquisition of Decision Resources Group from Piramal Enterprises Limited.

Welltower sold its prominent west coast senior living portfolio for more than $740 million to an unnamed operator.

InTouch Health reached an agreement to be acquired by Teladoc for $600 million including $150million in cash. The deal is expected to add $80 million to Teladoc’s top line.

Montagu Private Equity acquired RTI Surgical Holdings Inc.’s OEM business for $490 million. The divestiture will turn RTI into a pure play spine company.

AMN Healthcare Services, Inc., a leader in innovation in healthcare talent solutions and staffing solutions announced its acquisition of Stratus Video, a leading provider of video remote language interpretation services for the healthcare industry.

Collegium Pharmaceutical acquired the rights to Nucynta, a pain drug franchise, from Assertio.

Select Medical Holdings Corporation and Dignity Health announced the completion of the transaction to combine Concentra Group Holdings with U.S. HealthWorks.

Q1 2020 Largest M&A Transactions

Source: S&P Capital IQ

Healthcare Public Company Analysis