English

English

Today’s low interest rate environment has increased fixed-income investor demand for alternative investments generating higher yields than traditional fixed-income investments. Among them, are saleleaseback transactions which have experienced record activity since 2010, with total deal volume for 2015 reaching about $11.6 billion, according to Real Capital Analytics. While the sale-leaseback market slowed slightly in 2014, when deal volume reached $10 billion, it still surpassed the market’s previous production peak in 2007, when about $8 billion in sale-leaseback transactions were completed.1

Access to credit has also played an important role in driving demand. Nearly a decade after the financial crisis, bank credit remains relatively expensive and more conservatively structured for non-investmentgrade companies than prior to the recession, making it challenging for many middle-market companies, especially those with less than $25 million in revenues, to access bank financing at reasonable interest rates and terms. While mezzanine and opportunity funds have tried to bridge part of the gap in financing demand, this solution is not without significant cost. These funds typically require an 18% to 22% all-in return which is comprised of a relatively high interest rate of 11% to 13% and warrants for equity to make up the additional return. While this type of capital can be useful, it is expensive, contains restrictive covenants, and often includes material personal recourse.

Why Should Business Owners Consider a Sale-Leaseback Arrangement?

A sale-leaseback arrangement is an alternative to bank, mezzanine, and mortgage financing that effectively separates the “asset value” from the “asset’s utility value” in a company’s real estate investment. As a result, a saleleaseback arrangement can help to:

- Unlock a company’s real estate value

- Enable a company to reduce its investment in non-core business assets, such as buildings and land

- Liberate cash in exchange for executing a long-term lease

Sale-leaseback transactions can be a smart move by operating businesses that own their real estate. Since real estate values tend to rise and rents tend to drop when interest rates are low, business owners have an opportunity to sell their real estate high when rental returns are low, and keep occupancy costs at a predictable cash outflow by locking in long-term rental rates. In certain cases, companies have taken advantage of the opportunity to sell and lease back properties when real estate values were high, and later repurchased the same buildings when rates reverted to more typical, lower valuations.

6 Key Benefits for Business Owners

In the right set of circumstances, a sale leaseback transaction can provide a number of benefits to middle-market companies as sellers of real estate.

1. Set Your Own Lease Terms

Because the seller is also the lessee, the

seller has significant bargaining power

in structuring the property lease. In

addition to realizing their investment

in the real estate, the lessee has the

opportunity to negotiate an acceptable

lease agreement with the investor

acquiring the property. Typical leases

run 10 to 15 years. The seller, now the

tenant, can also negotiate extension

options after the lease expiration, and

can also include terms for early lease

termination if the tenant sees a need for

more flexibility.

2. Retain Control of Real Estate

Most sale-leaseback agreements are

structured as triple-net leases, so

the tenant will be responsible for the

taxes, insurance, and common area

maintenance. A long-term, ‘hands-off’

lease from the investor provides the

tenant similar control over the property

as was the case when the tenant owned

the property. The tenant can work with

the special purpose investor and include

options that will provide for future

expansion and sublease of the property.

3. Tax Savings

Generally, lessees that are engaged in a

lease are able to write off their total lease

payment as an expense for tax purposes. As

property owners, the interest expense and

depreciation were the only tax deductions

available. As a result, a sale-leaseback may

have a greater tax advantage.

4. Greater Value to the Real Estate

Unlike a mortgage, a sale-leaseback

agreement can often be structured to

finance up to 100% of the appraised value

of the company’s land and building. As a

result, a sale-leaseback more efficiently uses

the company’s investment in the real estate

asset as a financing tool.

5. No Financial Covenants

Because rules governing REITs prevent the

active management of real estate assets, a

sale-leaseback agreement generally contains

few covenants. Fewer covenants provide a

company with greater control over its own

business and operations, and reduces risk in

difficult operating environments.

6. Attractive Implied Financing Rates

A sale-leaseback agreement has an implicit

financing rate (“cap rate”) embedded in the

future rent payments. Although the sale-leaseback

cap rates are frequently slightly

more than similar mortgage rates, a sale-leaseback

provides cash proceeds for up to

100% of the appraised value of the property

versus the 65% to 75% of appraised value

under a typical mortgage. A sale-leaseback

investor has recourse only to the real estate

as collateral and a relationship with the

seller through the lease agreement. As a

result, the sale-leaseback is slightly more

expensive than senior financing and less

expensive than mezzanine financing.

When Should Business Owners Consider a Sale-Leaseback Agreement?

When an Alternative to Senior or Mezzanine Debt Is Advantageous

As described earlier, typical mezzanine financing has an all-in cost of between 18% and 22%. Mezzanine lenders will often include PIK (Payable in Kind) interest and equity ownership as part of their total return structure. The implied financing rate, the Cap Rate, of a sale-leaseback is generally hundreds of basis points lower than mezzanine capital and does not require equity ownership from the selling entity. The proceeds from a saleleaseback transaction can be used to refinance the mezzanine portion of the capital structure or as an alternative if there is no mezzanine to replace the company’s senior debt. In both instances, the company’s balance sheet ratios will improve substantially.

When Capital Is Needed for Growth

A sale-leaseback can be used to free up cash to grow a business through acquisition or to acquire growth capital, additional facilities, technology, and equipment. With the tightening of the credit markets, many businesses do not have access to as much credit as they need to achieve their growth objectives; many are too close to their borrowing limit to consider expansion or make an acquisition of a competitor. Sale leasebacks can be used as an off-balance-sheet financing structure that gives the seller the opportunity to turn a non-earning asset into growth capital. The company can then save the available bank financing for acquisitions and growth opportunities in the future. The sale-leaseback proceeds could also be used for other corporate purchases like the buyout of a shareholder or a special cash distribution. The absence of covenants in sale-leaseback arrangements provides business owners with significant discretion in determining the best use of their company’s cash.

When Undergoing a

Corporate Restructuring or

Seeking Exit Financing

Businesses that are struggling for liquidity to

pay creditors or are considering a bankruptcy

might look to a sale-leaseback for capital.

Depending on the value of the company’s

real estate, a sale-leaseback can supply a

considerable amount of liquidity and be a

quick initial step to begin a reorganization

process. Sale-leaseback investors can work to

meet tight time frames. If a potential seller is

able to provide historical financial statements,

a business plan, projections, and a description

of the planned use of proceeds, sale leaseback

investors can make rapid investment decisions

– often within 45 days.

When Packaging a Business for Sale

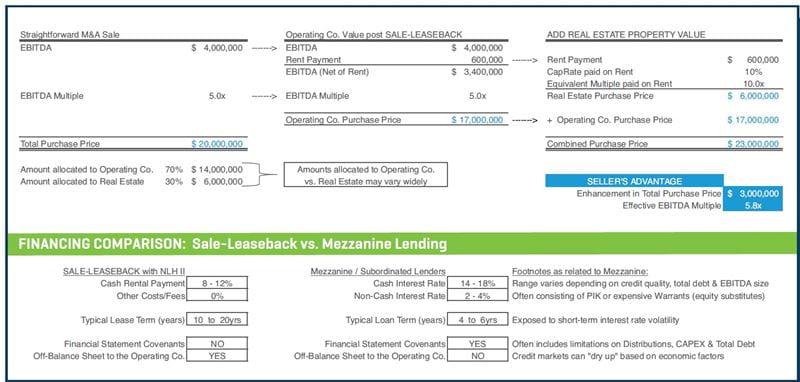

It is well-known that most private equity groups are not in the business of owning and managing real estate. Often, a savvy business owner who is contemplating selling his company can benefit by taking the real estate out of the company sales transaction and, by doing so, maximize the value of the real estate and increase the overall gross sale proceeds. If the real estate is left in the transaction, the full value is seldom realized as the EBITDA multiple often does not value the company’s real estate at its true fair market value. Sale-leaseback investors will typically make their offer price based on an appraisal, extensive real estate market study, and a review of comparable market lease rates. The seller can complete a sale-leaseback and negotiate a long-term lease, and pull out the real estate sale proceeds or repay corporate debt before the sale of the business.

The example below illustrates how a sale-leaseback helps to increase the proceeds to the seller in a corporate sales transaction. As shown, the rent expense will slightly lessen the EBITDA, therefore lessening the price of the operating entity. However, when the proper value of the real estate is recognized in a separate sale, and added to the proceeds of the company sale, a higher overall price is achieved.

How to Get Started

When an Alternative to Senior or Mezzanine Debt Is Advantageous

Sale-leaseback deals are primarily executed in conjunction with Real Estate Investment Trusts (REITs), which are tax advantaged structures designed to hold non-operating real estate assets. All sale-leaseback investors follow a disciplined approach to conducting their due diligence, similar to the due diligence efforts used when acquiring any real estate. Building and land appraisals, local market research, comparable lease and sales data, location, and accessibility analysis are just a few areas which will be considered during due diligence. The investor will also evaluate the tenant’s credit strength using analyses similar to those used by lending institutions and corporate acquirers. Finally, when sale-leaseback investors consider investment opportunities, they will contemplate the long-run marketability of the real estate once it’s vacant.

The size and shape of the building will also play a role in the functionality equation when underwriting the property. The investor is very interested in the alternate uses and users for the real estate when the tenant vacates the property. All of these alternative-use factors will affect the lease payment in the sale leaseback transaction.

How REITs Are Driving Demand for Sale- Leaseback Transactions

A REIT is a tax advantaged structure designed to hold non-operating real estate assets. REITs typically provide investors high dividends plus the potential for moderate long-term capital appreciation with lower risks than typical equities, resulting in a sweet spot for many investors seeking a more reliable, risk-adjusted income stream.

As REITs become better understood and more frequently utilized by investors and their financial advisors—not only as an alternative to stocks, bonds, and cash, but increasingly, as a critical component of a well-diversified investment portfolio—demand for the income-producing vehicles has increased. This is reflected in the S&P Dow Jones Indices’ decision to add REITs as the 11th sector in the S&P Dow Jones Indices’ Global Industry Classification Standard (GIC®) in late 2016, separating a new Real Estate Sector from the Financial Sector. This has also increased investor demand as S&P balanced investors add REIT stocks to their portfolios.

- National Real Estate Investor; December 28, 2015.