English

English

What started as a year in which politics and a pending election were set to take centerstage while strong business conditions and a growing economy were expected to continue to trend, 2020 proved to be the most disruptive year on record for business owners and operators across the economic spectrum. The tire industry was not spared and saw severe disruption and contraction between March and May in most of the country.

Aside from the dislocation caused by the onset of the pandemic and actions taken by local, state and national government, the impact on M&A was all-encompassing – with the second quarter seeing the lowest transaction count on record with just seven transactions recorded in the industry globally.

Beginning in late May and continuing through the summer and into the end of the year, business which was lost or deferred during the first three months of the pandemic came back, with leading wholesalers and retailers serving the pent-up demand generated while pandemic took hold. Aiding this was the first round of stimulus checks distributed to consumers and the rebound in miles driven around the nation.

As always disruptive trends create winners – social distancing, no-touch, and curbside service saw ecommerce boom, with the channel rapidly gaining and holding market share heading into 2021; and commercial dealers and service providers designated as and serving “essential” industry remaining operational serving a booming transportation & logistics industry which continued to move product around the country during the pandemic.

M&A saw a strong rebound in the back half of the year, as delayed, deferred, and new transactions converged on the fourth quarter along with an improved business climate, record amounts of equity available for acquisitions, and low cost, readily-available bank financing for deals. Early in 2021 we are seeing industry-changing moves in retail and commercial and are excited to cover and participate in the year ahead as it unfolds.

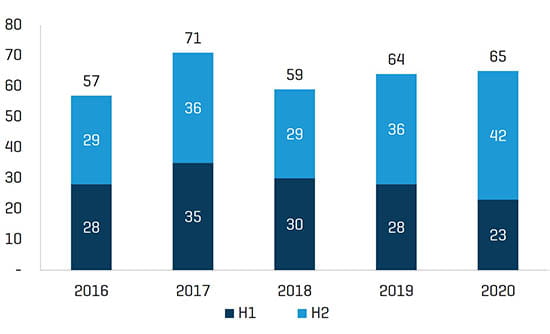

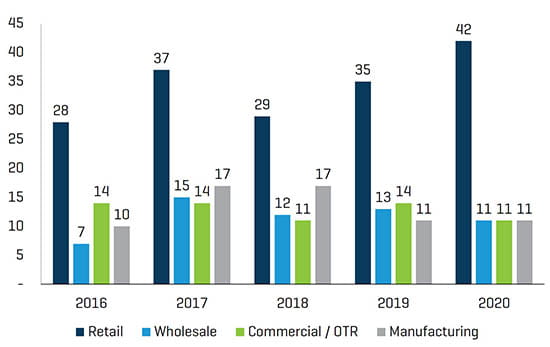

Historical M&A Trends by Period / Sector

Total Transaction Count

Transactions per Sector

Note: Double-count of transactions which are included in multiple industry sub-sectors/categories, have been removed.

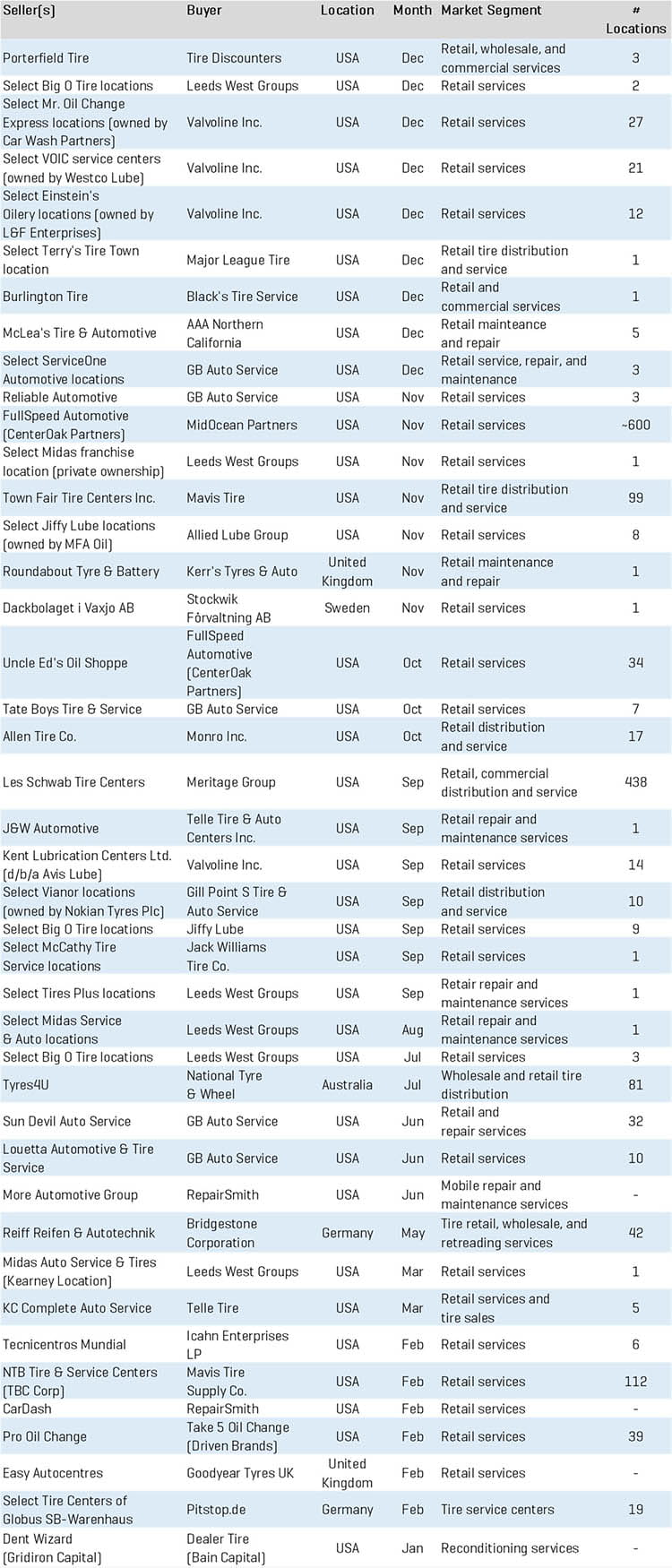

Retail

Retail M&A Transactions - Q4 2020

GB Auto Service

Tucson, Arizona-based GB Auto Service announced a spree of M&A activity, including acquisitions of Oklahoma-based Tate Boys Tire & Service (seven locations), Texas-based Reliable Automotive (three locations), as well as three ServiceOne centers located within the greater Houston area. Established in 2017 as a portfolio company of Greenbriar Equity Group, GB Auto Service has rapidly expanded its footprint via acquisitions over the past three years, having added more than 60 locations throughout 2020, and boasting a grand total of 177-plus outlets across California, Arizona, Nevada, Texas, and Oklahoma. GB Auto Service is now the seventh largest independent retail tire and auto repair dealership in the United States.

Mavis Tire

In November, Mavis Tire Express Services Corp. announced its merger with Connecticut-based Town Fair Tire Centers Inc. Mavis and Town Fair have agreed to combine their operations under a common umbrella, while maintaining their respective management teams and brands, as well as separate headquarters. The merger creates a powerhouse in the Northeast, adding Town Fair’s roughly 99 locations across six states (Connecticut, Massachusetts, Rhode Island, New Hampshire, Maine, and Vermont) to Mavis’ network of 900-plus storefronts throughout the Eastern U.S.

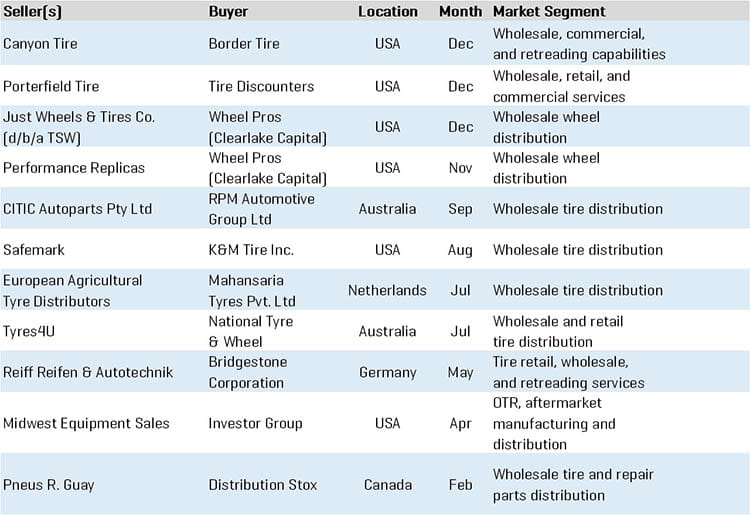

Wholesale

Wholesale M&A Transactions - Q4 2020

Wheel Pros

Clearlake Capital-backed Wheel Pros LLC, an automotive aftermarket wheel manufacturer headquartered in Denver, announced the acquisitions of Performance Replicas and Just Wheels & Tires Co. (d/b/a TSW). Founded in 2010, Performance Replicas is a recognized leader in the distribution of replica wheels, with longstanding relationships across established national and internet retailers. California-based TSW distributes proprietary aftermarket custom wheels and maintains over 5,800 dealer relationships across its network of eight distribution centers.

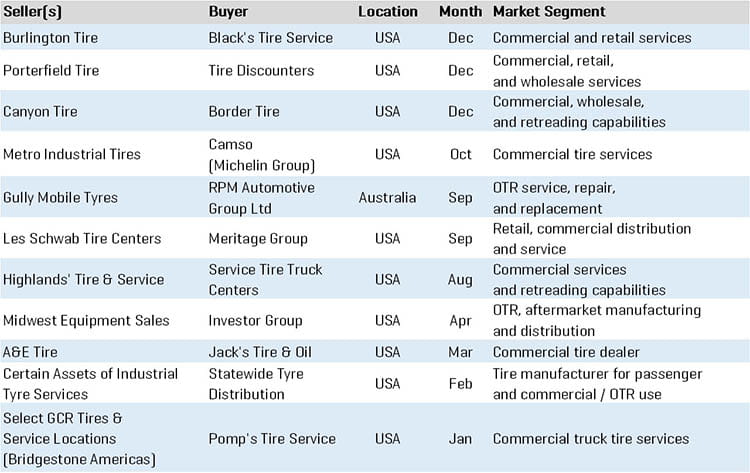

Commercial / OTR

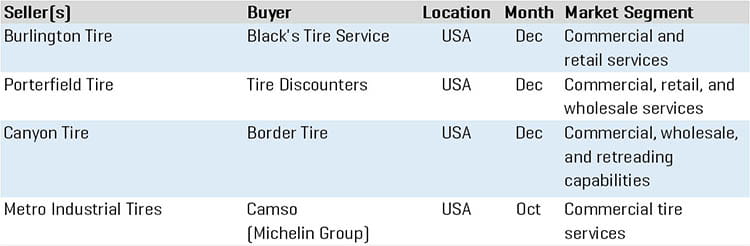

Commercial/OTR M&A Transactions - Q4 2020

Border Tire

Border Tire, a commercial tire dealership and retreader based out of El Paso, TX, announced its acquisition of California-based Canyon Tire in December. Founded in 1990, Canyon operates a retread facility and five commercial outlets throughout Southern California, employing a staff of approximately 140 across all locations. The deal to buy Canyon comes nearly two years after Border Tire’s acquisition of five California TCi Tire locations and one MRT retread plant from Michelin, thus doubling Border’s presence in the region.

Camso North America

In October, Camso North America, a subsidiary of Michelin Group (ENXTPA:ML), announced its acquisition of Metro Industrial Tires. Founded in 1983 and servicing customers in and around the Midwest, Metro is an industrial tire dealer and distributor operating with locations on the north and south side of Chicago, respectively.

Manufacturing

Manufacturing M&A Transactions - Q4 2020

Aurelius Equity Opportunities

Aurelius Equity Opportunities, a German private equity firm, announced its acquisition of London-based OTR wheel manufacturer GKN Wheels & Structures in October. Formerly a subsidiary of Melrose Industries, GKN Wheels designs, manufactures, and supplies wheels for a myriad of applications across the agricultural, construction, industrial, and mining segments. Under new ownership, the existing GKN Wheels management team intends to pursue further sector consolidation strategies and leverage its operational expertise to drive profitable growth across the OTR wheel manufacturing sector.

2020 M&A Transactions by Segment & 2021 Forecasts

Retail

Despite the pandemic, 2020 retail M&A volume reached new highs, with a significant boost from H2 activity pent up from the first half. Scale and the associated benefits of network synergies, purchasing power, operating leverage, and multiple expansion remain key M&A drivers; along with geographic coverage and market density diversifying and de-risking the network.

Retail Forecast 2021

- All signs point to significant transformation in the retail landscape during 2021, as consolidators continue to vie for turf, the large retailers compete for the shrinking pool of regional retailers with some scale, and new capital coming into the industry is pressured to deploy in pursuit of expansion. Look for a vastly different retail landscape at the end of 2021

- Consumer purchasing trends continue the shift to the ecommerce channel, accelerated by the COVID-19 pandemic in 2020 with no reversal in sight. Ecommerce channel presence and integration/alliance with the physical retail network to provide a seamless consumer experience becomes paramount

Retail M&A Transactions - 2020

Wholesale

Wholesale M&A activity dipped slightly in 2020 compared to 2019 levels. Transaction activity was global in scope, with activity across the North America, Europe, and Oceania. Strategic rationale encompassed entrance into new markets, consolidation of operations, focus on enhanced unit volume and related volume benefits, and footprint expansion.

Wholesale Forecast 2021

- Regional consolidation activity to continue in North America as small to mid-size wholesalers continue to be absorbed by larger regional players, albeit at a measured pace

- A rapidly consolidating retail landscape drives innovative decision making and change at the wholesale level, as key wholesalers determine fresh ways to add value (ie: growing brand portfolios, fulfillment, inventory management) and align with the ever expanding and consolidating retail networks

Wholesale M&A Transactions - 2020

Commercial/OTR

Commercial / OTR M&A activity in 2020 was down modestly vs. 2019 levels, though in-line with 2018 results, as activity from manufacturer owned and commercial / OTR dealers increased.

Strategic activity represented the bulk of commercial M&A for 2020, particularly in the United States, where regional players entered new geographies and expanded overall footprint.

Commercial/OTR Forecast 2021

- Interest in the tire sector by capital providers and strategic acquirers looking to take advantage of a fragmented landscape of commercial / OTR independent dealers likely to increase, as capital remains abundant and investment opportunities become scarce

- Alliances are formed and in some cases recalibrated to provide the dealer greater opportunities to drive sales and margin

Commercial/OTR M&A Transactions - 2020

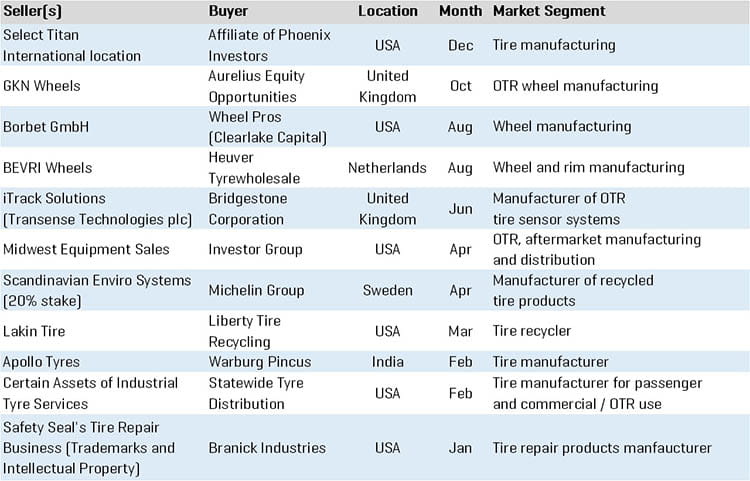

Manufacturing

2020 Manufacturing M&A matched levels seen in 2019, with notable international transactions coming from (i) financial buyers, including Warburg Pincus’ investment in Apollo Tyres and Aurelius Equity’s acquisition of GKN Wheels, and (ii) strategics, including transactions within the segment from both Bridgestone and Michelin.

Manufacturing Forecast 2021

- Majority of activity will remain driven by multinational manufacturers, as well as financial buyers

- Remaining independent, specialty manufacturers continue to be targeted by global strategic buyers seeking new product lines, brands, and growth

Manufacturing M&A Transactions - 2020