English

English

The S&P 500 gained 11.7% during the fourth quarter of 2020, while the Healthcare Services and Life Sciences equities that we track in this report performed well during the quarter, increasing 18.9%. Healthcare Services and Life Sciences even outperformed the tech-heavy NASDAQ in the quarter, which was up 15.7%. Optimism about the 95% efficacy of the vaccines from Moderna and Pfizer appear to have boosted confidence in a swift economic recovery in 2021 and lifted the market as a whole.

With respect to full year of 2020, the S&P 500 was up 16.3%, Stout’s Healthcare Services and Life Sciences Universe was up 25.4%, and the NASDAQ was up a whopping 43.6% for its’ best performance since 2009.

Healthcare Services

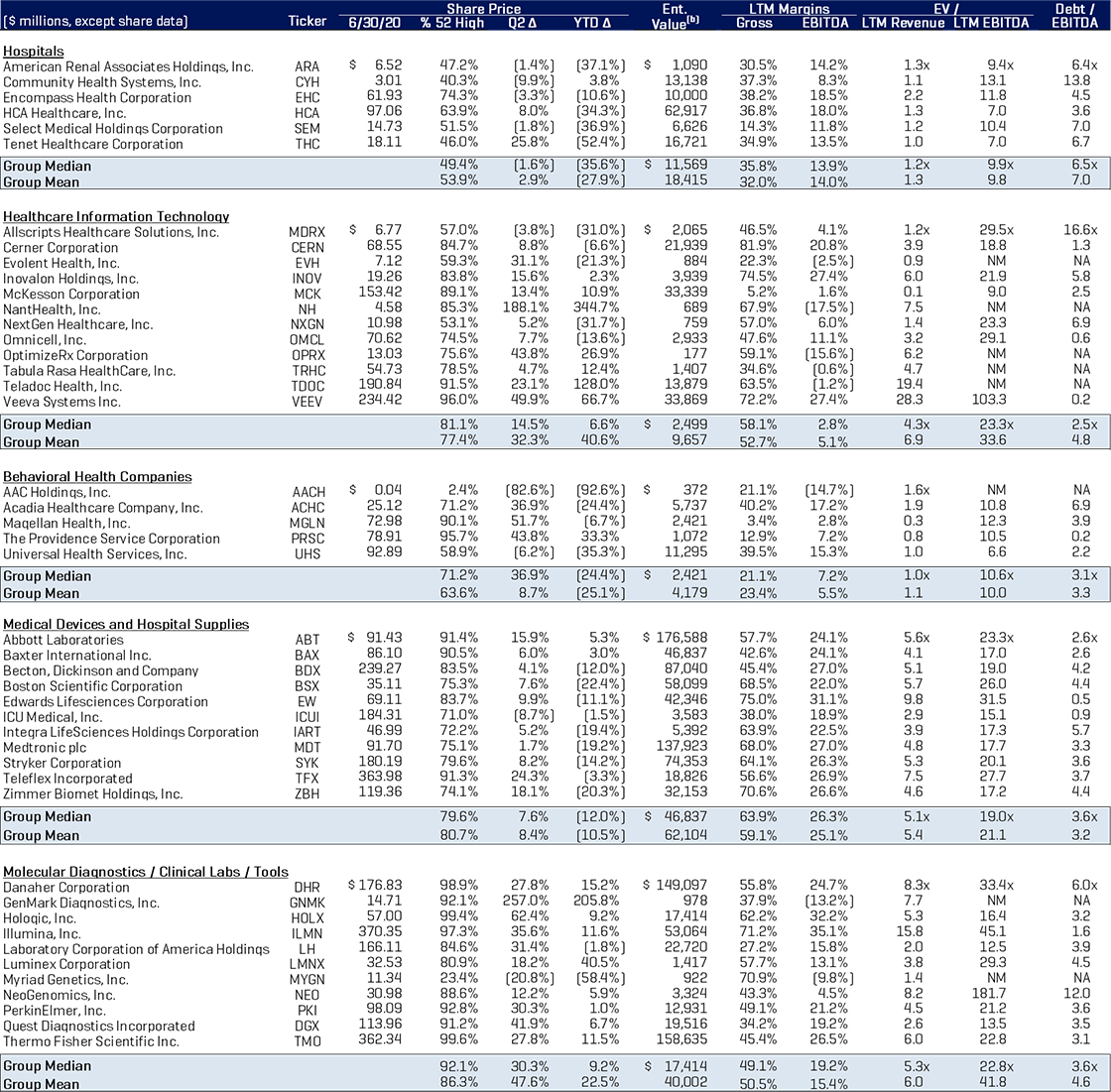

The healthcare post-acute care service segments were the best performers in the fourth quarter with the median price performance of Hospitals (+32.9%), Behavioral Health (+28.6%), and Skilled Nursing Facilities (+31%) rallying significantly off of lows that were created by COVID-19 infections and visits crowding out elective procedures as well as patient census declines due to COVID fears and deaths.

Hospitals also performed well for the full year with the median price increasing 18.5% on enthusiasm that elective procedures will return and probably surge in 2021 given the vaccine rollout, post- election relief and probably bargain hunting in a market where many stocks in the tech sector for example have risen to very rich valuations. We also think that the hospital industry has streamlined and shed excess capacity on some level.

Behavioral health stocks jumped 51.3% in 2020 with strong performance from Acadia Healthcare, DLH Holdings and ModivCare. Skilled Nursing stocks did not fare as well given a drop in patient census that will take more time to recover and were off 23.2%.

In an article published by Barron’s on June 19, 2020, they state that “The House of Representatives committee overseeing the U.S. response to the coronavirus pandemic has launched an investigation into the five largest nursing home companies, requesting detailed data on their handling of the COVID-19 deaths and operations at the facilities.” They later attribute 40% of COVID deaths to nursing home residents, which obviously does not help the sector. All of that being said, we know that these facilities will continue to play an important role in healthcare over time as will home care. These providers will likely adapt their treatment models to admit patients with higher levels of acuity as technology improves and offer additional services as a growing number of patients are moved out of the higher cost acute care setting earlier.

Physician Practice Management was up 34.8% in the fourth quarter and 26.4% for year. This group had mixed results as groups that were risk contracting probably faired well, while fee for service providers focused on elective procedures took a big hit to revenue and profitability. Most of our clients in this sector, such as practices in dermatology, ophthalmology, dental, ortho-spine and interventional pain, that are performing elective procedures are just now getting back to pre-COVID levels on a consistent month to month basis. A few of the larger transactions in this segment during the quarter were Sun Capital’s acquisition of Miami Beach Medical for more than $500 million1 and the United Surgical Partners acquisition of 45 ASCs from Surgical Center Development, Inc. for $1.1 billion. Gryphon Investors also acquired Physical Rehabilitation Network from Silver Oak Services Partners for an undisclosed price.

Healthcare Information Technology stocks were up 23% in the fourth quarter of 2020 and 47% for the full year of 2020. Teladoc was up 138% for the year and added the acquisition of InTouch, but slipped 8.8% on the fourth quarter probably on profit taking and as vaccine news became more positive relative to the perceived need for telemedicine and questions about whether reimbursement for all forms of telemedicine will continue post-COVID. HCIT was pretty much strong across the board whether it be for companies focused on bioinformatics and cloud storage, e-scripts or technology for value-based outcomes.

Medical Devices and Life Sciences

Medical Device and Hospital Supply stocks were up 13.2% and 9.3% in the quarter and year, respectively, and this group has been a stable outperformer over many years and was not as impacted during COVID as the healthcare service sectors. Devices used in elective procedures were impacted some, but then IV fluids and pumps, syringes, devices used in cardiac, neuro, and peripheral vascular surgery and medical supplies used for PPE and respiratory applications grew.

A couple of notable transactions here during the quarter were Teleflex’ acquisition of Z-Medica, a manufacturer of surgical hemostats and wound dressings, for $525 million. Steris also acquired Key Surgical, a leading global provider of sterile processing, operating room, and endoscopy products, for $850 million.

Molecular Diagnostics, Tools and Clinical Labs were up 8.1% and 39.5% for the quarter and year, respectively, and here you have beneficiaries of COVID testing and other indications as well as developers of DNA based diagnostics moving closer to the point of care such as GenMark (+203% for the year.) A very interesting deal in this sector in our view was Exact Sciences acquisition of Thrive Earlier Detection, a company with a liquid biopsy (blood for example as opposed to taking a tissue sample of a solid tumor) technology for earlier cancer detection. The hope here is that one day we can detect deadly cancers like pancreatic, Ovarian and certain types of breast cancer much earlier to allow for prevention and curative treatment.

Stout has also been active in working with medical device and pharma contract manufacturers where we see a lot of opportunity for growth. Stout just announced that we advised Life Science Outsourcing on its partnership (majority sale) with Public Pension Capital and we are representing additional clients in the sector currently. Separately, we saw that Cirtec/3i acquired NovelCath.

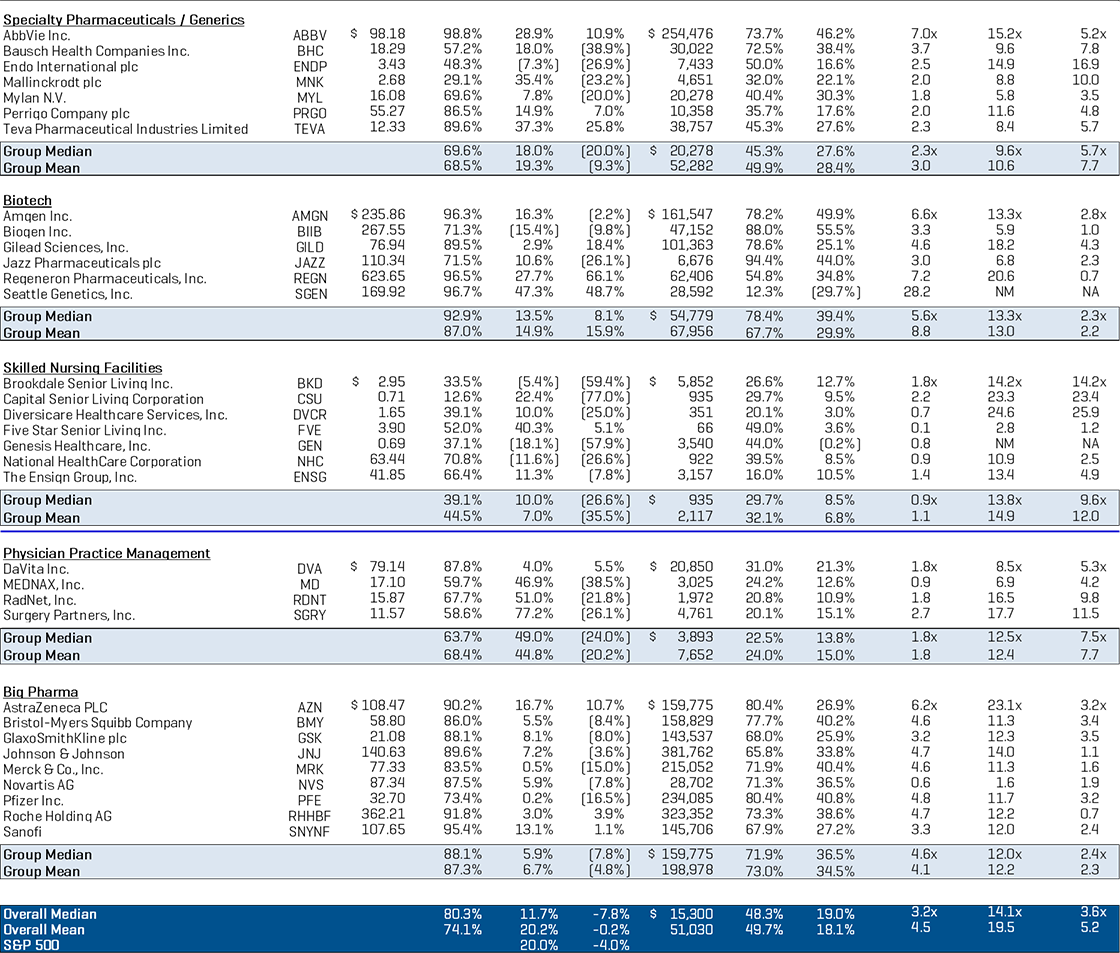

Specialty Pharmaceuticals were up 22.3% in the quarter but down 6.8% for the year. Mallinckrodt in particular plummeted 94.2% on news of Medicaid Acthar gel liability, opioid litigation, and bankruptcy concerns. Endo International PLC acquired BioSpecifics for $658 million in the quarter, which manufacturers Xiaflex injectable collagenase for Dupuytren’s Contracture and Peyronie’s Disease.

The worst performing sectors in healthcare in the fourth quarter were Biotech (-10%) and Big Pharma (+0.3%.) Obviously, there were better performers among the COVID vaccine manufacturers like Pfizer and Johnson and Johnson, but economic (unemployment and Co-pays), patent expiration, product liability, law of large number and political concerns about drug pricing will continue to weigh on these sectors intermittently. Biotech and Pharma were up 3% and down 3.7%, respectively, for the full year of 2020.

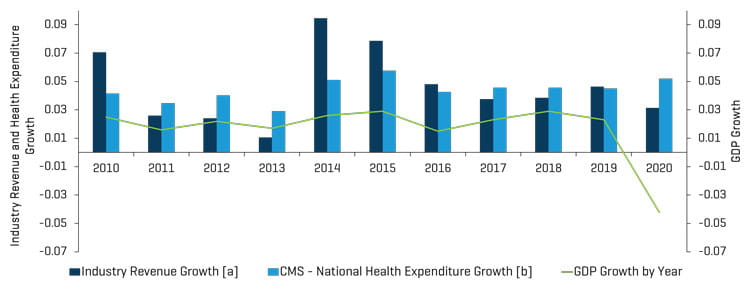

In the table below, you can see that Stout’s Healthcare Universe of companies saw revenue grow 3.1% in 2020, whereas real GDP for the U.S. economy declined more than 3% due to the impact of COVID-19.

Historical Revenue Growth of Segments Monitored by Stout vs. Annual Health Expenditures and GDP Growth

Notes:

[a] For each period, total revenue figures are derived from the sum of all comparable companies listed in the appendix (Healthcare Public Company Analysis).

[b] CMS tracks National Health Expenditure Accounts (NHEA), which are the official estimates of total health care spending in the United States annually.

Source: www.cms.gov, Historical and Projected NHEA tables.

Healthcare M&A Market Update and Outlook

M&A Market Key Takeaways:

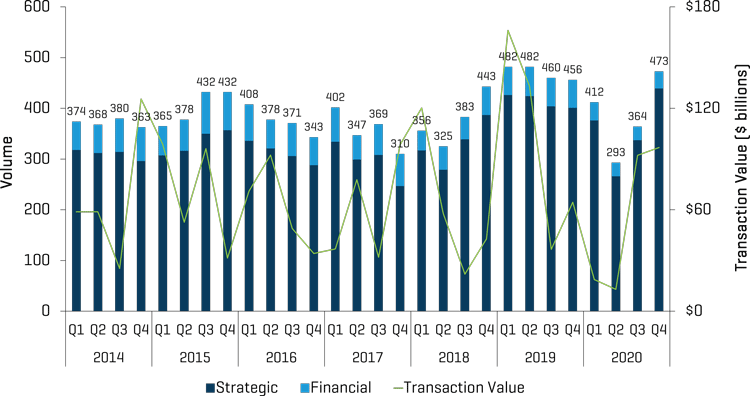

- M&A activity rebounded in the last quarter of 2020. Transaction volume in the fourth quarter was 473 transactions announced and/or closed, a slight increase from last year’s fourth quarter of 456 transactions, and significantly improved over second and third quarters of 2020, which were 293 and 364, respectively. The 293 transactions in the second quarter were the lowest level in any quarter since at least 2014. Nearly half of the 109 sequential jump in the number of transactions in 4Q’20 came in the physician practice management sector where a wide range of add-ons closed that had probably been postponed due to COVID impact on the businesses. These acquisitions occurred across the board in dermatology, ophthalmology, allergy and infectious diseases, ENT, imaging centers, surgical centers, dental, urgent care, primary care, women’s health and wound care.

- Overall transaction value of deals announced and/or closed in the fourth quarter came in at more than $96 billion compared with the previous year’s $64 billion, driven by AstraZeneca PLC’s acquisition of Alexion Pharmaceuticals for more than $40 billion. We would also mention that enterprise values are not reported for many private transactions, so total number of transactions is a more reliable metric. On the flip side, the largest transactions will generally involve a public buyer.

- We would also note that half of the top 20 transactions by dollar value were in biotech and pharma given the size of the industry and the fact that companies in these sectors typically access the public markets earlier in their corporate life cycle (pre-revenue) whereas service providers typically do not.

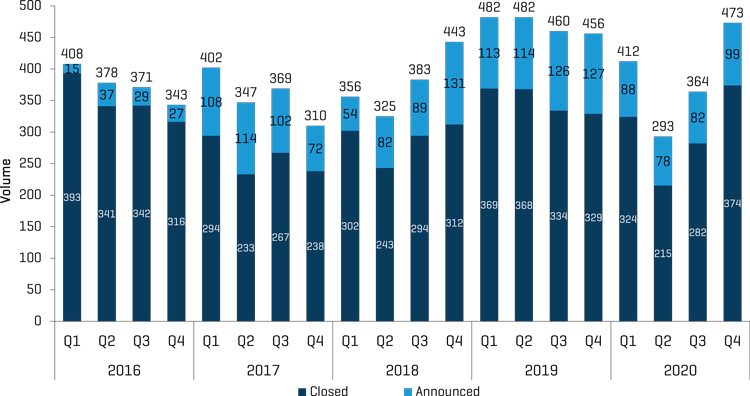

- Closed deals in the fourth quarter of 374 was the highest we have seen since early 2016. Announced deals of 99 in the fourth quarter compared with 127 in the fourth quarter of 2019.

- The total of deals announced and closed in 2020 was 1,542, a 17.9% decrease compared with 1,880 in 2019. No doubt the COVID-19 pandemic had a large effect in delaying the announcement and closing of deals throughout 2020 and we expect to see a large uptick in deals in 2021. Total transaction value of deals announced and/or closed was $220 billion in 2020, down 44.9% due to the large pharma mergers announced and/or closed in the first two quarters of the 2019 and decreased deal flow caused by COVID-19.

Q4 2020 M&A Transactions: Volume and Value

Source: Source: S&P Capital IQ and Stout Industry Research

Historical M&A Transactions: Announced vs. Closed

Source: S&P Capital IQ and Stout Industry Research

Analysis of Healthcare Sub-Sector M&A Activity

M&A activity in all sectors has picked up since 3Q’20.

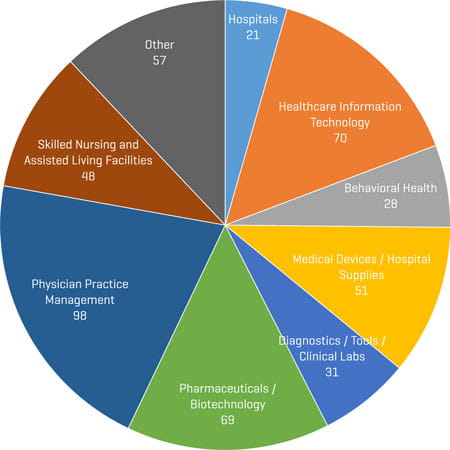

Q4 2020 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

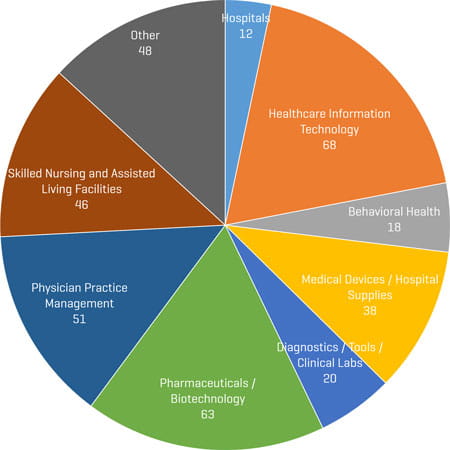

Q3 2020 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

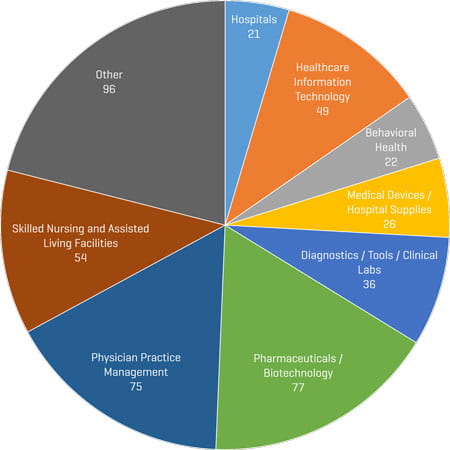

Q4 2019 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

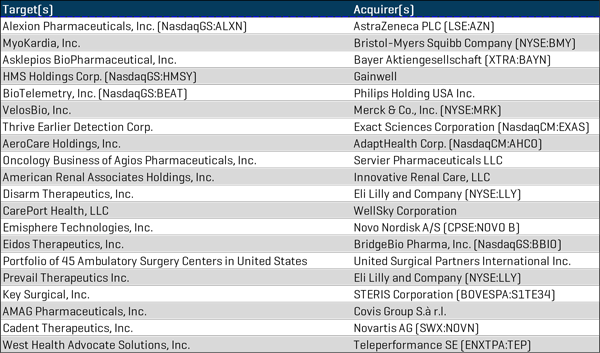

Notable Q4 2020 M&A Transactions

AstraZeneca (LSE: AZN) has announced its definitive agreement to acquire Alexion Pharmaceuticals (NasdaqGS: ALXN). AstraZeneca, through this acquisition, will create a greater scientific presence in immunology, expand geographical, improve growth and profitability. AstraZeneca's $39 billion buy of Alexion Pharmaceuticals

Bristol Myers Squibb (NYSE: BMY) announced its definitive agreement to acquire Myokardia (Nasdaq: MYOK) for $13.1 billion or $225.00 per share in cash. The acquisition strengthens BMY’s portfolio, pipeline and scientific capabilities and will generate meaningful long-term growth.

Asklepios BioPharmaceutical was acquired by Bayer Aktiengesellschaft (XTRA: BAYN) for up to $4 billion. The acquisition will support Bayer’s cell and gene therapy platform.

Veritas Capital-Backed Gainwell acquired HMS Holdings Corp (NasdaqGS: HMSY), an industry-leading technology, analytics and engagement solutions provider helping organization reduce costs and improve health outcomes.

Philips announced its acquisition of BioTelemetry (NasdaqGS: BEAT) which is a strong fit for Philips’ cardiac care portfolio, and its strategy to transform the delivery of care along the health continuum with integrated solutions.

Merck & Co., Inc. (NYSE: MRK) announced it will acquired VelosBio, which is developing VLS-101, an antibody-drug conjugate targeting ROR1 that is being evaluated in Phase 1 and a Phase 2 clinical trial for the treatment of patients with hematologic malignancies and solid tumors, respectively.

Exact Sciences Corporation (NasdaqCM: EXAS) announced its acquisition of Thrive Earlier Detection for more than $2 billion. The acquisition will position Exact Sciences as a leader in blood-based, multi-cancer screening.

In-home equipment supplier AdaptHealth (Nasdaq: AHCO) has entered into a definitive agreement to acquire AeroCare Holdings, a technology-enabled respiratory and home medical equipment distribution platform for about $2 billion.

Agios Pharmaceuticals announced the sale of its oncology business to Servier Pharmaceuticals for an initial payment of $1.8 billion and a potential $200 million in regulatory milestone, plus royalties.

Innovative Renal Care, a portfolio company of Nautic Partners, announced its acquisition of American Renal Associates (NYSE: ARA). The acquisition was later completed in early 2021.

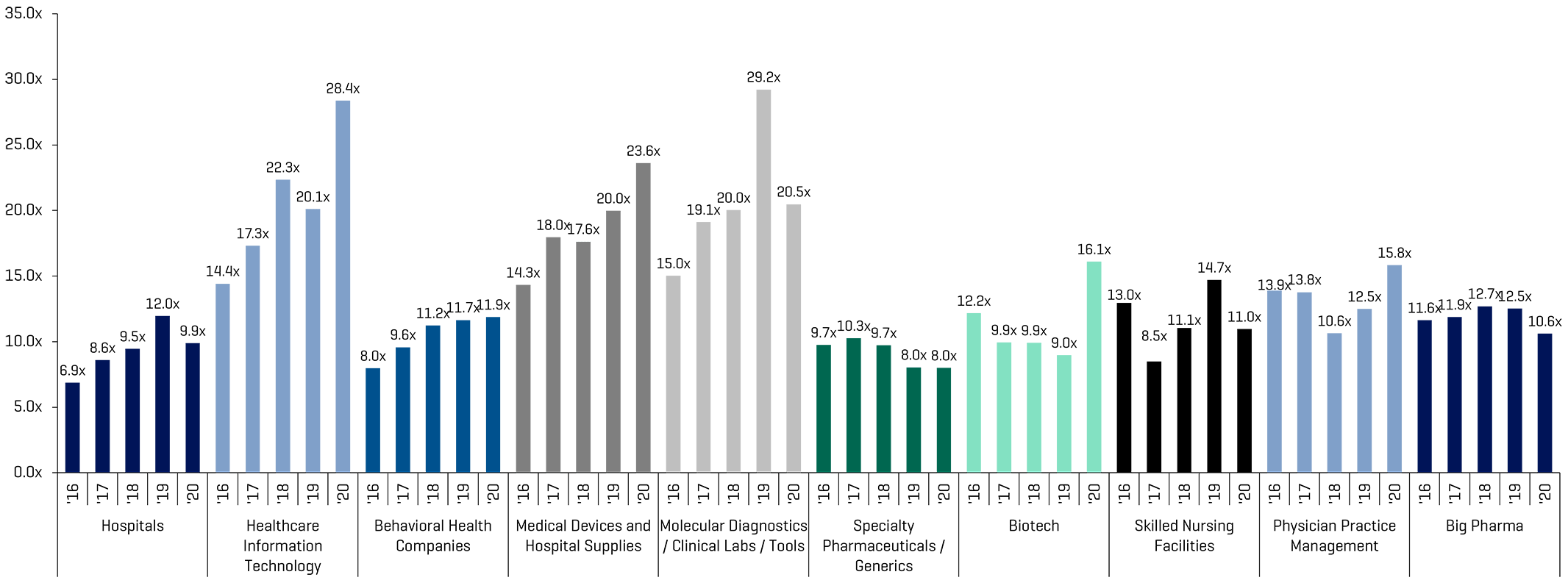

Public Comparable Companies: Historical and Forward EBITDA Multiples

Source: S&P Capital IQ; Multiples calculated from comparable companies universe that Stout tracks

Q4 2020 Largest M&A Transactions

Healthcare Public Company Analysis

Source: S&P Capital IQ

Notes:

(a) Market value based on fully-diluted shares including conversion of all exercisable in-the-money options, less shares repurchased using option proceeds.

(b) Enterprise Value equals Market Value plus total straight and convertible debt, preferred stock and minority interest, less cash and investments in unconsolidated subsidiaries.

LTM EBITDA, EBIT and Net Income exclude extraordinary items.

--

1South Florida Business Journal.