English

English

The S&P 500 gained 20% during the second quarter of 2020 after falling by 20% in the first quarter of 2020 in response to the COVID-19 pandemic and its impact on economic activity as many businesses closed and employees were forced to shelter at home.

The S&P 500 was down 4% year to date through June 30, but is up 3.4% for the year as of mid-September and the unemployment rate is recovering, as well. This has been quite a performance given that earnings for the S&P 500 dropped 32% in the second quarter, and many Wall Street firms pulled earnings estimates in light of the pandemic. The market recovery is likely associated with the positive developments discussed below, but significant risk remains in the market given that one presidential candidate has proposed treating long-term capital gains as ordinary income.

On March 27, 2020 Congress signed the CARES Act into law, which has been very effective in stimulating the economy, preserving jobs, and in fostering the second quarter market recovery. Lower interest rates have also provided some monetary stimulus, while expectations of a flattening of the COVID-19 infection rate curve, optimism about businesses re-opening, and more responsible adoption of personal protective equipment probably contributed, as well. The CARES Act has included the Paycheck Protection Program (PPP) that provided forgivable loans to small businesses that retained employees, one-time payments to individual Americans, increased unemployment benefit payments, and stimulus payments to large corporations and state and local governments.

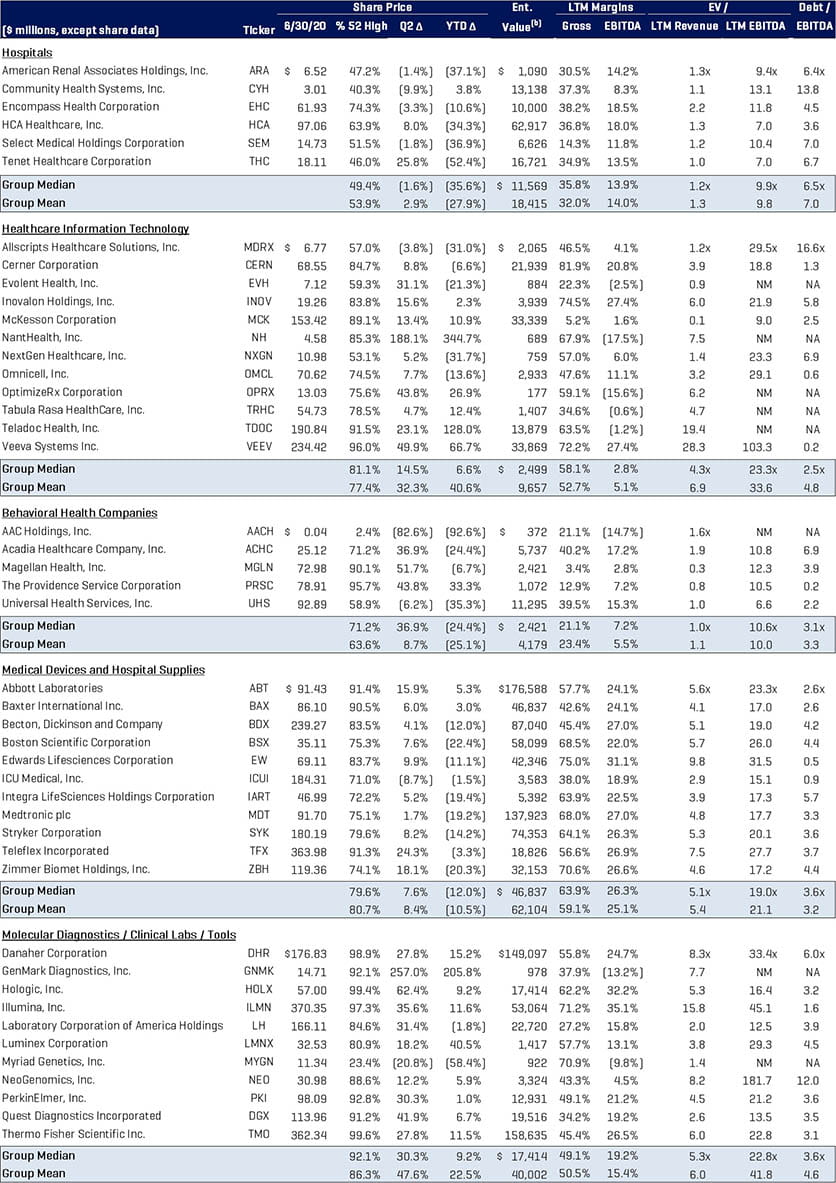

Healthcare Service and Life Science equities that we track in this report performed in line with the markets 20% increase in the second quarter, but outperformed year to date through the end of the second quarter, coming in flat versus the above-mentioned 4% decline for the S&P 500. Healthcare Information Technology was up 40.6% overall year to date (up 32% in the second quarter of 2020) on the adoption of telemedicine and precision medicine and the strong performance of names like Teladoc (+128%), Veeva Systems (+67%) and NantHealth (+345%.)

American Well Corp., a telehealth company, has filed to go public as we write this report and here is an excerpt from their S-1 filing related to telemedicine:

“Looking past COVID-19, we can see that some effects of the current period may be felt beyond the immediate crisis. In particular, we are seeing the growing awareness among consumers of the availability and efficacy of telehealth for many healthcare needs and we are seeing more widespread hands-on experience among providers in delivering care via telehealth. It remains unclear the extent to which the currently more relaxed regulatory environment, favorable reimbursement policies, and leniency with respect to cross-state provider licensure will become normative. However, we believe that the current experience is more likely to be favorable to telehealth and Amwell’s business than otherwise over the longer term.

“The surge in interest in telehealth, and in particular the relaxation of HIPAA privacy and security requirements, has also attracted new competition from providers who utilize consumer-grade video conferencing platforms such as Zoom and Twilio. Compared to those new entrants, Amwell offers simpler video capabilities to meet the new interest in easy, fast video connections. While it is not yet clear how this competitive dynamic will play out, Amwell remains confident that healthcare is a highly specialized application, and that both health plans and health systems will require a secure, HIPAA-compliant, end-to-end platform capable of handling the full care continuum and connecting to appropriate physical Carepoints in the future.”

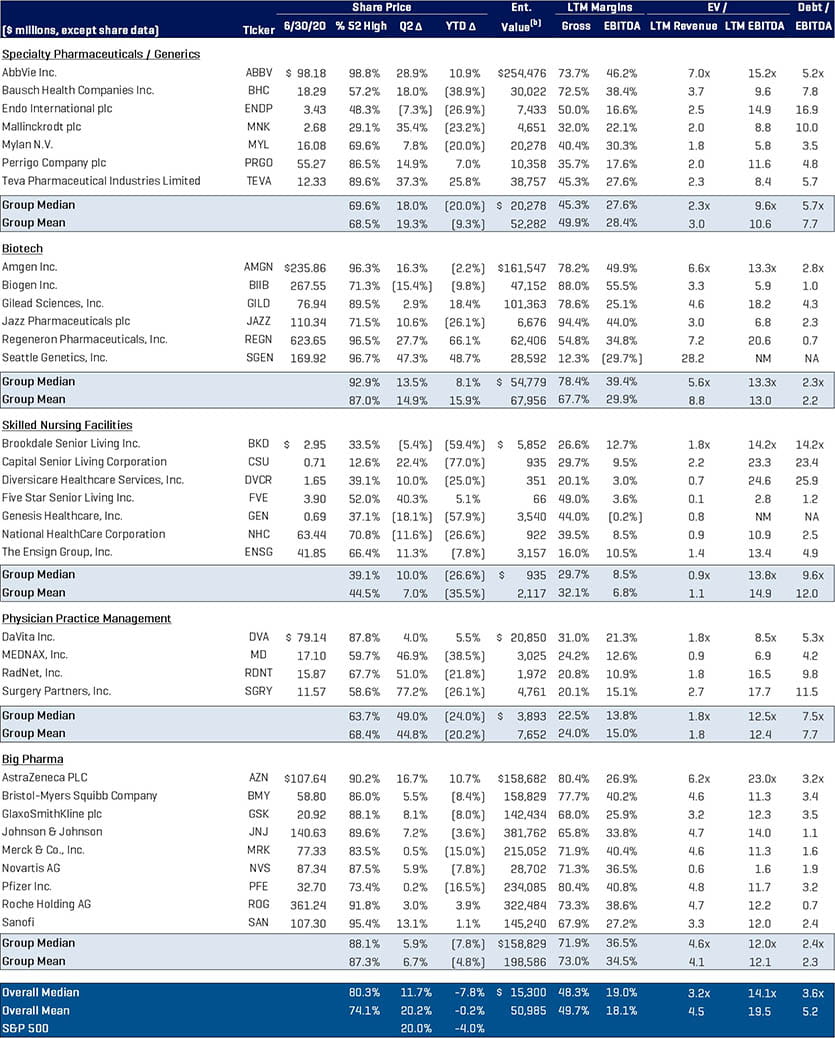

Molecular Diagnostics/Clinical Labs/Tools stocks were up 22.5% year to date overall (up 47.6% in the second quarter) on increased demand for COVID-19 testing, while the biotechs were up 15.9% year to date on excitement about emerging vaccines and antibody and antiviral therapies for COVID-19 and other disease states.

Although each healthcare sector that we track was up in the second quarter, the healthcare services sectors remained down for the year, as providers and patients have avoided treating non-COVID patients in the hospital setting and high infection rates publicized for select post-acute facilities have impacted census. The pandemic also continues to impact elective procedures in some states that have continued restrictions. Skilled Nursing Facilities (-35.5%), Hospitals (-27.9%), Behavioral Health Facilities (-25.1%), and Physician Practice Management (PPM) (-20.2%) were all down year to date. Physician Practice Management did post a significant recovery in the second quarter, increasing 44.8%, but still ended up down year to date, which is consistent with what we see as elective procedures returning to pre-COVID levels. We think that we have seen the worst of the COVID-19 impact in PPM and expect to see deal activity there resume later this year and early next.

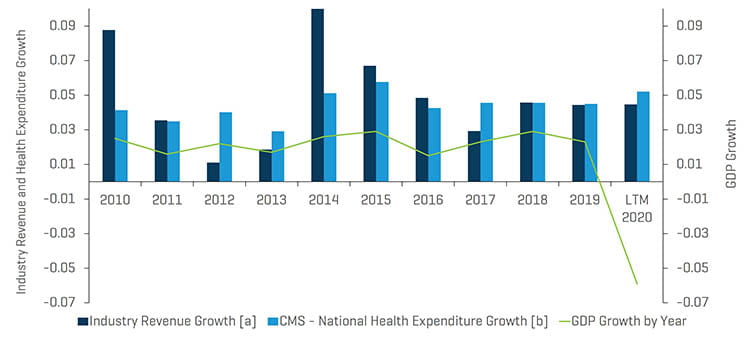

As shown in the table below, GDP growth plummeted in the second quarter of 2020 and revenue and earnings of the S&P 500 were off 32% as we mentioned above. We expect that revenue growth in healthcare will exceed that of the overall economy, and we anticipate M&A transaction volume will bottom out in the second half of the year and increase significantly by the second quarter of 2021.

Historical Revenue Growth of Segments Monitored by Stout Vs. Annual Health Expenditures and GDP Growth

Notes:

[a] For each period, total revenue figures are derived from the sum of all comparable companies listed in the appendix (Healthcare Public Company Analysis).

[b] CMS tracks National Health Expenditure Accounts (NHEA), which are the official estimates of total health care spending in the United States annually.

Source: www.cms.gov, Historical and Projected NHEA tables.

Healthcare M&A Market Update and Outlook

M&A Market Key Takeaways:

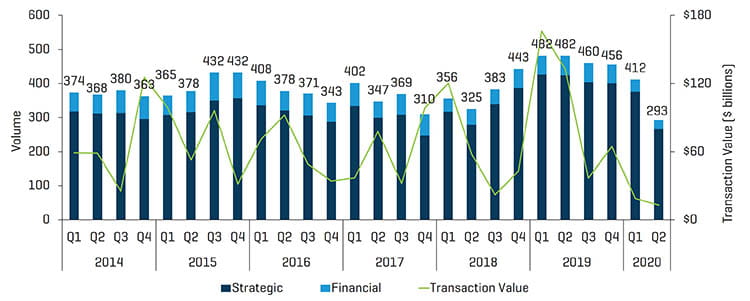

- M&A activity saw a significant drop off in healthcare in the second quarter of 2020 as deal volume came in at 293 transactions announced and/or closed, a decrease from a level of 482 transactions in the second quarter of 2019, due no doubt to the onset of COVID-19 and the shelter-at-home restrictions that has continued to shut down the economy and delay deal closures. This was the lowest deal volume since 285 in the second quarter of 2013.

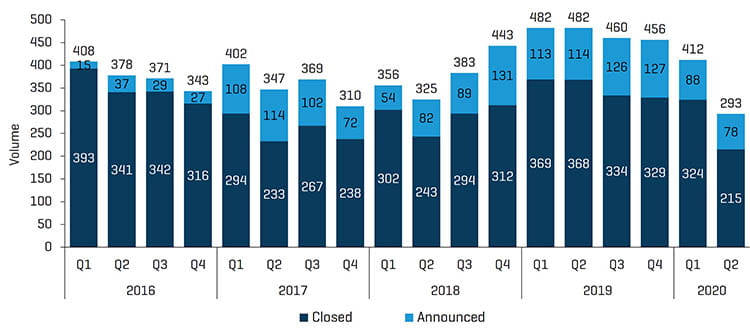

- Announced and closed deals declined 31.5% and 41.5%, respectively, to 78 and 215. We would note that the decline in closed deals suggests that some were called off indefinitely during the quarter due to the impact of the pandemic on revenue and EBITDA. In recent years, a lot of the increased M&A activity in Physician Practice Management has been in the sub-sectors providing elective procedures with private pay mix, such as dermatology, ophthalmology and dental. The pandemic led to ASC closures and cessation of clinic activity for a period of time in March, April and May, causing some management teams to quickly restructure operations and reduce headcount before realizing they could have applied for PPP loans and retained perhaps all staff. For some, the response to the pandemic may have lasting impact and getting back to pre-COVID revenue and EBITDA levels may take time.

- Overall transaction value of deals announced and/or closed in the second quarter of 2020 came in at roughly $13 billion compared with the previous year’s $133 billion, the lowest quarterly value in more than six years. We would note that the $80 billion Abbvie acquisition of Allergan in the year earlier accentuated the negative comparison. Three deals accounted for $5 billion of the $13 billion in the second-quarter transaction value.

- We would note that enterprise values are not reported for many private transactions, so total number of transactions is a more reliable metric. On the flip side, the largest transactions will generally involve a public buyer where values are disclosed.

Q2 2020 M&A Transactions: Volume and Value

Source: S&P Capital IQ and Stout Industry Research

Historical M&A Transactions: Announced vs. Closed

Source: S&P Capital IQ and Stout Industry Research

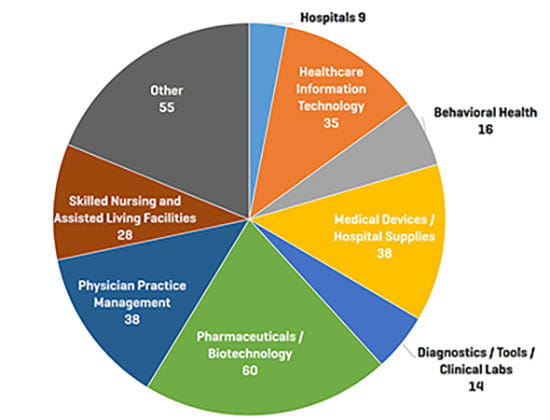

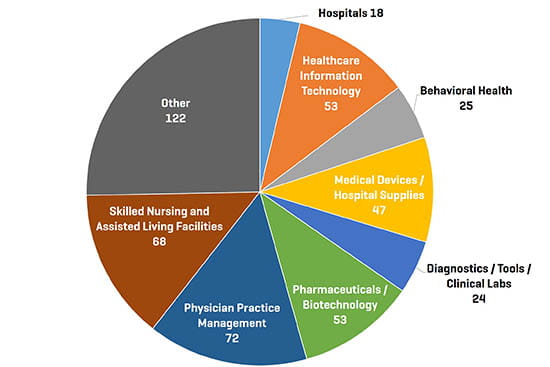

Q2 2020 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

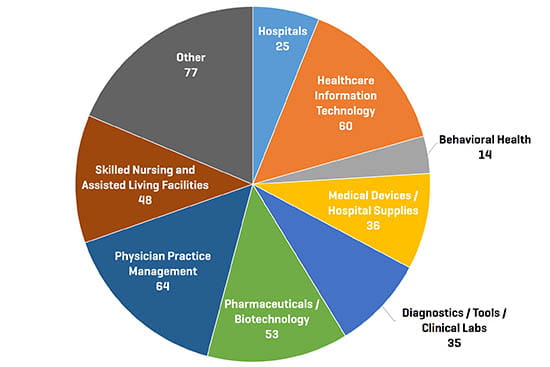

Q1 2020 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

Q2 2019 M&A Transactions by Segment

Source: S&P Capital IQ and Stout Industry Research

Analysis of Healthcare Sub-Sector M&A Activity – Observations and Trends

Pharmaceuticals/Biotechnology, Medical Devices / Hospital Supplies, Physician Practice Management, and Healthcare Information Technology remain the most active M&A sectors. As expected, there was a big drop in M&A activity in Physician Practice Management, Skilled Nursing, Behavioral Health, and Hospital deals given the COVID-19 impact on patient flow for normal elective procedures, telemedicine options and changing trends in discharges to post-acute facilities.

Pharmaceuticals and Biotechnology

Pharmaceuticals and Biotechnology realized a slight increase in deal flow increasing to 60 in the second quarter of 2020 compared with 53 in the second quarter of 2019. Two of the three $1 billion-plus deals in the quarter were in pharma/biotech and included Novo Nordisk’s acquisition of Cordivia Therapeutics and Alexion’s acquisition of Portola Pharmaceuticals. There were a wide range of therapeutic areas involved in M&A activity in the quarter including cardiovascular drugs, cancer immunotherapies, vaccines, CNS, antibiotics, anti-infectives, and antivirals.

President Trump has given the pharma industry an ultimatum to address drug pricing and its impact on the Medicare Part B and D programs, including threatening to force drug manufacturers to sell to the Medicare Program at the lower prices found in international markets and potentially importing from Canada and other markets. He is also scrutinizing the activities of pharmacy benefit managers and rebate programs with an eye toward savings being passed to consumers rather than insurance companies. This topic may become more visible as the election approaches.

The quarter also saw a great deal of activity in growers, manufacturers and distributors of cannabis related products as well as developers of medicinal cannabis related therapies.

Medical Device and Supply

Medical Device and Supply transactions came in at 38 in the quarter and were down from 47 a year ago.

AdaptHealth acquired Solara Medical Supplies, a distributor of continuous glucose monitoring supplies, and ActivStyle, a distributor of incontinence supplies to the home market, during the quarter. Continuous glucose monitoring is, of course, improving the management of HBA1C and clinical outcomes to the detriment of traditional monitoring, while the population continues to age (silver tsunami is on its way) and patient care migrates to the home. Abiomed acquired Breethe, Inc., which is developing an artificial lung/respiratory support device to assist patients who have inadequate lung functions – seemingly timely given the manifestation of COVID-19 symptoms.

Catheter & Medical Design, Inc, a medical device contract manufacturer of tubing for interventional vascular devices, was acquired by Inverness Graham and we continue to see consolidation activity in this sector as OEMs seek outsourced manufacturing partners that can help provide them with end to end solutions. Other activity in the medical device sector in the quarter included a number of add-ons on the orthopedic and spinal implant sector.

Physician Practice Management

Consolidation of the Physician Practice Management sector experienced a downtick with 38 deals announced/closed in the second quarter of 2020, down from 72 in the year-earlier quarter. Once again, deal activity was spread across a wide-range of specialties, but we would note that there was activity in ophthalmology in particular where retinal practices have turned out to be stable through the pandemic while the private pay aspects of ophthalmology such as Lasik and advanced multi-focal lens procedures for cataracts have suffered.

Healthcare Information Technology

Healthcare Information Technology saw 35 transactions in the quarter versus 53 a year ago and 60 in the prior quarter. As we mentioned in our last report, telemedicine has been a hot area within this segment, but overall HCIT deal volume slowed significantly. We suspect this is temporary, but some of the areas that had activity in the quarter included telemedicine services, revenue cycle management (billing and collections), mobile patient pay systems, computer simulated surgery apps, patient data warehousing and analytics, and systems for forecasting patient volumes and optimizing scheduling.

Skilled Nursing and Senior Housing

Skilled Nursing and Senior Housing activity fell off in the second quarter. There were 28 Skilled Nursing/Senior Housing deals in the quarter versus 68 in the year earlier quarter. After picking up significantly in 2019, it looks like activity here will subside for a while unless driven by distressed asset sales in the next few quarters. Highly publicized fatalities reported for COVID19 in a select group of skilled nursing facilities is likely to impact census and financial results. We anticipate that covenant breaches could start to crop up for those leveraged operators after the third quarter of this year and our Special Situations team is here to help those in need of financial restructuring advice.

Diagnostics / Tools / Clinical Labs

Diagnostics / Tools / Clinical Labs saw just 14 transactions in the second quarter compared with 35 in the previous quarter and 24 in the year ago quarter. One of the three large deals in healthcare overall in the quarter was Invitae’s acquisition of ArcherDX and its molecular cancer diagnostics business. COVID-19 diagnostic and antibody testing has certainly increased revenue and product development in this category as it has in respiratory supplies such as face masks and antibody therapy and antiviral development for COVID-19.

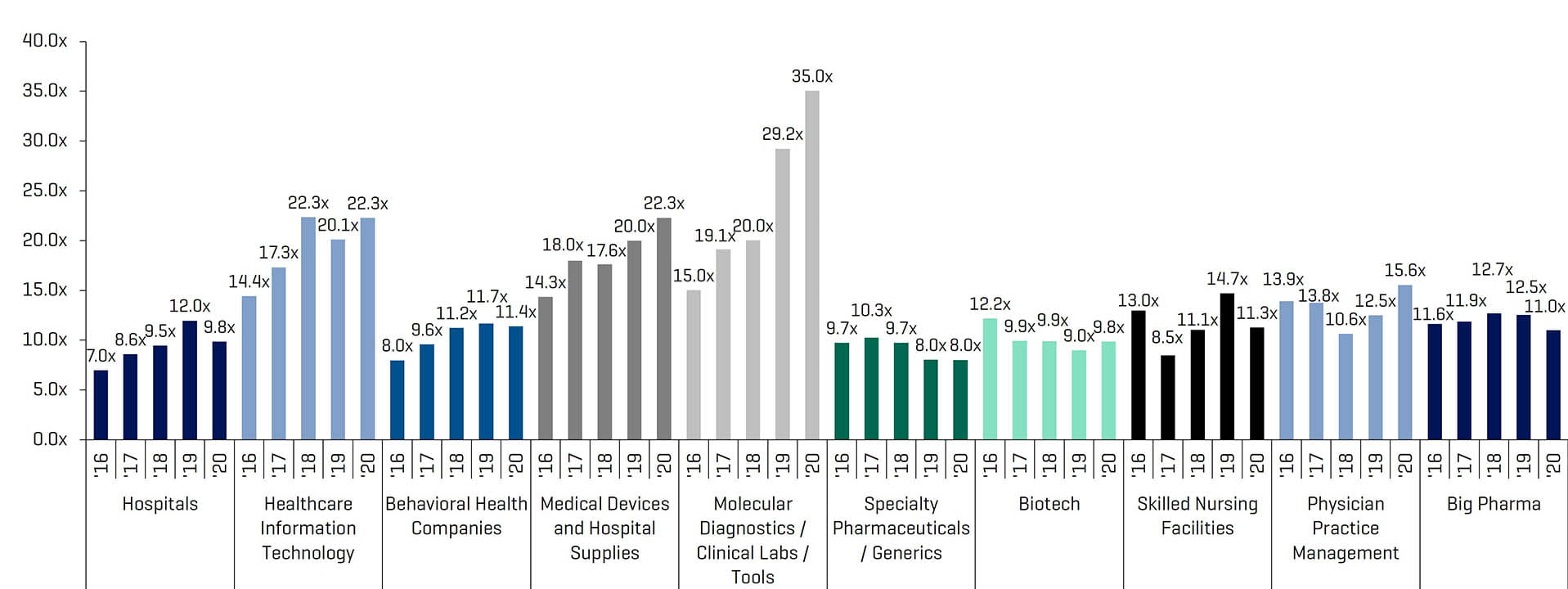

Enterprise value to EBITDA multiples for the publicly traded sectors in this report experienced mixed results with many segments increasing, likely because of strong market performance coupled with decreased earnings due to COVID-19.

Public Comparable Companies: Historical and Forward EBITDA Multiples

Source: S&P Capital IQ; Multiples calculated from comparable companies universe that Stout tracks

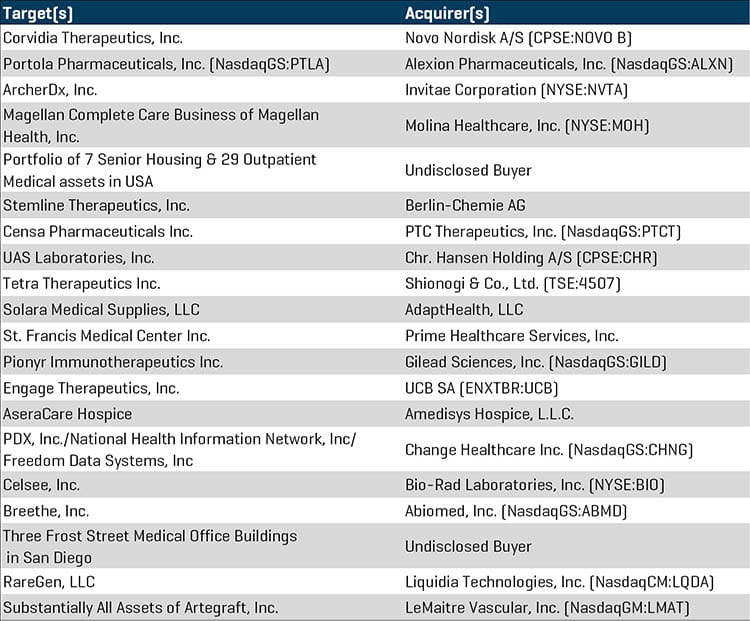

Notable Q2 2020 M&A Transactions

Novo Nordisk A/S announced its acquisition of Corvidia Therapeutics in an effort to expand its presence in treating kidney disease for $2.1 billion.

Portola Pharmaceuticals, a commercial-stage biopharmaceutical company focused on life-threatening blood-related disorders, announced it has entered into a definitive merger agreement to be acquired by Alexion Pharmaceuticals.

ArcherDx and Invitae Corp. have announced a definitive agreement to create a genetics leader in cancer genetics and precision oncology.

Magellan Health sold its Complete Care Business Molina Healthcare for $820 million. With the acquisition, Molina will serve more than 3.6 million members and has a projected pro-forma revenue of over $20 billion for 2020.

Welltower sold a portfolio of seven senior housing and 29 outpatient medical properties for approximately $1 billion to an undisclosed buyer.

Berlin-Chernie AG established its presence in the U.S. biopharmaceutical oncology market with its acquisition of Stemline Therapeutics, which was valued at up to $677 million.

PTC Therapeutics announced its acquisition of Censa Pharmaceuticals, a biopharmaceutical company focused on the development of CNSA-001, a clinical-stage investigational therapy for orphan metabolic diseases, for $538 million.

Chr. Hansen Holding acquired UAS Laboratories for $530 million. Chr. Hansen plans to extend its microbial platform and strengthen its probiotic production flexibility.

Shionogi & Co. has agreed to buy Tetra Therapeutics, a clinical-stage biotechnology company, for roughly $500 million.

Solara Medical Supplies announced its sale to AdaptHealth, which expands its leading in-home medical supplies platform into the large and fast-growing diabetes and incontinence segments. The transaction was valued at $428 million.

Q2 2020 Largest M&A Transactions

Source: S&P Capital IQ

Healthcare Public Company Analysis