English

English

While demand for plastics continues to surge, the industry’s success may also be its Achilles’ heel. The industry currently has very low barriers to entry and shares many characteristics with the commodities industry. As a result, plastics processors and manufacturers who experience the most success are market leaders who have carefully plotted their course, resulting in unique attributes, such as a specific product, process, or market niche.

But how can other companies replicate this success?

Mike Benson, a Manufacturers Association for Plastics Processors (MAPP) board member and Managing Director in Stout’s Investment Banking group, returned to this year’s MAPP Benchmarking Conference to moderate another dynamic conversation among a panel of plastics business executives and advisors. The discussion focused on the key drivers of business value, the metrics that are vital for understanding business performance, and the strategies the executives employed to stay laser-focused on their end goals.

Benson was joined by:

- Glen Fish – CEO, Revere Plastics Systems, LLC

- Mike Walter – President, Met2Plastic

- Josef Keglewitsch – Partner, Ice Miller

“To begin each day with the end in mind means to begin each day, task, or project with a clear vision of your desired direction and destination, and then continue by flexing your proactive muscles to make things happen.” - Steven Covey

Benson began the conversation with a quick overview of the various valuation methods typically used to value a business, homing in specifically on discounted cash flow (DCF) as the desired backdrop for the discussion. “DCF is essentially the value of the future stream of free cash flow that a business is deemed capable of generating, along with the assets in place to generate those cash flows,“ he said.

Benson then asked CEOs Glen Fish and Mike Walter what steps they’ve taken over time to build value within their companies and to ensure health, competitiveness, and longevity.

“The true outcome of the value of a business is what it transacts for when it’s sold.” – Benson

Fish joined Revere in 2014 when the company was underperforming. A lender had taken an equity position, cash flow wasn’t there, the company had excess inventory, and few investments were being made. “My first step was to reel in inventory – we implemented a new process that took us from 40 to 29 days and were able to free up cash. Then we looked to upgrade our management team because ultimately we knew the bank did not want to own the business.”

Fish went on to describe customer concentration as one of his company’s biggest detractors, with a majority of revenue being tied to a single account. “We lacked a strategy to diversify our customer base, so we added a business development function, brought in a sales team, and started to have success.” From there, Fish determined where they wanted to compete, joined relevant trade associations, and worked with his team to create their first strategic five-year plan. “Our plan then became stronger each year, and our operations strategy began to align with our sales strategy. I was determined to demonstrate a growth trajectory.”

Walter’s family sold their business earlier than he had thought they would, but he had been preparing for an eventual sale for several years. “What made us most attractive to buyers was our early decision to focus on the markets we wanted to serve and then develop a plan to grow into those markets.” Walter and his team chose two in particular – aerospace and medical – and then worked to gain a footprint and recognition as players in those markets. “We chose these two industries because we saw there would be long-term growth potential, and they were also niche enough where the barriers to entry were higher.” At same time, Walter worked on building bench steps within the organization and developing a strong management team. The third area of focus was putting infrastructure in place (investing in equipment) for long-term success.

Keglewitsch added that owners and executives should start looking at their businesses through the eyes of a buyer, and to be careful not to ignore housekeeping items. “As an attorney, I think about reducing risk and protecting assets – registering [intellectual property] when you have it, minimizing risks within your customer base, and putting careful thought into contractual relationships.” He advised when appropriate, to have long-term contracts in place. “Lock up your critical employees with non-competes, employment contracts, and transaction bonuses. Generally, it’s a very small but critical group of people who help a transaction go through, and it’s important to acknowledge them.”

Benson inquired whether the panelists had a deliberate plan they followed and how they developed their respective strategies.

Fish described developing a vision statement that encompassed who they wanted to be, the end markets they wanted to serve, and then building that into the Revere sales budget. They looked opportunistically at what business they wanted to go win. Then his team looked at what criteria were required to achieve operational excellence and what type of investment in equipment was necessary, and tied that back to their financials. His team used their budget and inventory metrics to determine their daily position.

Walter started with a five-year plan for where they wanted to be and then revisited that plan each year. “Our plan included numbers, goals, vision, size, markets and what we wanted to be for our employees and customers. We then built the financials around that.” He cited the use of several metrics including equipment efficiency and value added per hour, noting these as the types of metrics that managers on the floor can relate to and that drive to the same goal.

Building on the previous question, Benson asked about the ground-level, day-to-day tasks the panelists chose to focus on.

Fish described routine visual evaluation of critical spots on the production floor – productivity targets for various zones that help to meet the company’s business objectives. “We also do a weekly financial forecast review that helps tremendously to minimize surprises. We have separate reviews for financial targets and for our progress toward more strategic initiatives like lean improvements and capital expenditures.” He went on to describe monthly business reviews with the senior leadership team in which they evaluated all four of their facilities for performance, new sales wins, and customer feedback, further noting that the company is extremely transparent.

Walter talked about daily meetings with primary production staff to review the previous day’s results and what could be learned from them. He also described meetings held at the beginning of each week to review performance and discuss key initiatives for moving forward. “We don’t just look at the past but also look at what we’re doing moving forward. It’s a great way to find out if a manager needs support, and it gives them the opportunity to solicit their peers. We implemented the weekly meeting a year ago, and it’s been effective at reducing barriers and enabling information flow across teams.”

He said that once per quarter, they hold a meeting with the entire production tooling team to gauge performance and to provide the team with a senior management perspective on the business. He was sure to add that they also make time to celebrate key milestones.

Continuing the operations-focused discussion, Benson asked Fish and Walter about what metrics they track on their reporting dashboards.

Fish quickly reeled off his daily operating metrics consisting of sales, scrap, inventory, and sales pipeline – how many quotes are in the system and how long they’ve been in there. “Our big focus is diversification, so we watch it very closely. Full pipeline, inventory, and cash at the end of the month.”

Walter first cited the usual suspects of sales and profits but then mentioned monitoring incoming orders and backlog to help them navigate any near-term changes that may be needed. “Looking at an income statement is great, but it’s in the past. Looking at incoming sales gives you time to react. And, it’s not just incoming POs; we also look for trends.”

"When it comes to buying a business, a buyer is going to place a value on your business based on current EBITDA. However, the multiple on that EBITDA is going to be based on the perceived future health of your business." – Benson

Benson acknowledged that the need to go to China had ebbed and flowed, but what had been less discussed was the movement into South America. He asked the panelists which parts of the world were becoming more or less relevant to their businesses.

Fish explained, “On lower tonnage items that package and ship well, we run into Asian competition. We just try to steer clear of these types of things and focus on larger tonnage value-add, which has helped differentiate us. Certain customers want to see presence in Mexico, especially in automotive."

Walter also mentioned the southern migration of U.S. manufacturing facilities, “We’ve seen a lot of our customers move operations from the U.S. to Mexico. So far, we’ve been able to continue to supply them from facilities outside of Chicago.”

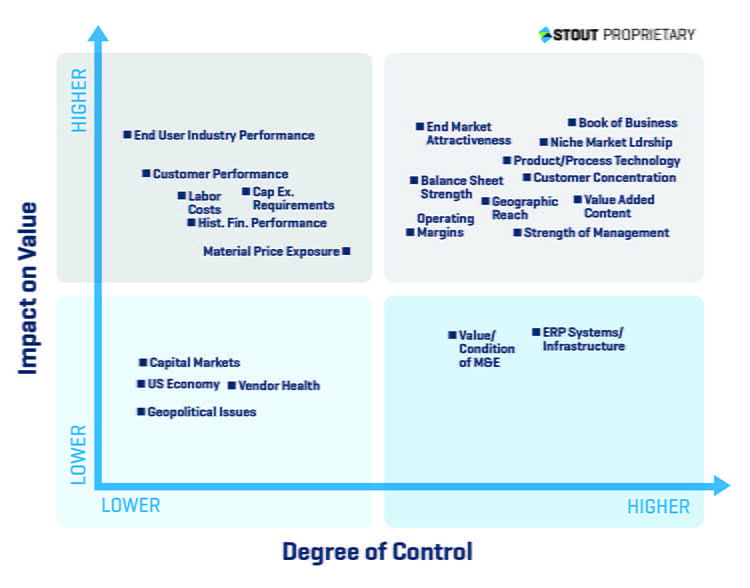

Benson closed the discussion with reference to the Stout Value Driver Quadrant (figure 1): “It’s certainly been our experience in working with plastics processors that those who are able to focus on the ‘high-impact, high-control’ aspects of the business, while strategically navigating the ‘high-impact, low-control’ factors, are those that will trade for higher values, all else being equal. The key is to recognize what those factors are in your business, and begin to pursue a short-, medium-, and long-term plan to help you reach your goals.”

Photo courtesy of Todd Schuett, Creative Technology Corp.

This article was previously published in the Winter 2019 issue of Plastics Business Magazine.