English

English

There’s no question that the plastics industry is a significant contributor to the nation’s economy. As the third-largest manufacturing industry in the United States, behind petroleum and automotive, and ahead of basic chemicals, the industry employs more than 940,000 workers and creates more than $427.3 billion in annual shipments.1 But statistics tell only part of the story. Just try going a day without plastic.

From the most mundane daily tasks such as brushing your teeth, driving to work, and texting – to lifesaving medical devices and high-tech military components and equipment – plastics have become an inextricable part of our daily lives, contributing to health, safety, efficiency, and convenience, among others.

The use of plastics to produce virtually any product has resulted in a highly competitive global industry with thousands of participants that offers attractive financial opportunities for business owners, prospective buyers, sellers, and long-term investors. That makes it essential for plastics processors to clearly understand the factors that drive value, as well as steps they can take to nurture value at every stage of the business lifecycle. By examining two similar companies, the following analysis provides a compelling look at the factors that enable one plastics processor to command a higher value than another, employing Stout’s unique “value quadrant” tool. Additionally, in the event the owner is eventually interested in realizing the value of the company through a sale, specific action steps are provided to assist in attracting strong interest and full valuations from a range of buyers.

What Makes One Company More Valuable Than Another?

While demand for plastics continues to surge, in many ways, the industry’s success may also be its Achilles’ heel. The current industry environment has little to no barriers to entry with many of the characteristics of a commodity industry. As a result, plastics processors and manufacturers that have historically experienced the most success – and are likely to be successful in the future – are market leaders that have carefully plotted their course, resulting in unique attributes, such as a specific product, process, or market niche.

But how do you get from here to there? The simple answer is careful planning and thoughtful decision-making that remains laser-focused on the business’ end goals. In the words of the late author and businessman Stephen Covey: “To begin with the end in mind means to begin each day, task, or project with a clear vision of your desired direction and destination, and then continue by flexing your proactive muscles to make things happen.”

As we’ll illustrate through the use of our value quadrant tool, each decision a business owner makes, no matter how large or small, plays a role in determining tomorrow’s value. However, not all decisions have the same level of impact. That’s why it’s critical for business owners to understand what drives value in a plastics processor and what considerations allow one company to command a higher value relative to another.

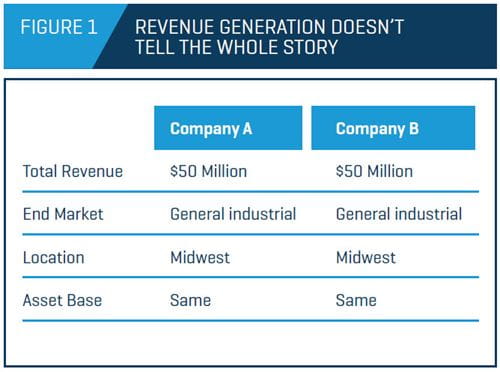

In many instances, valuation levels for companies with similar asset bases and operating metrics can exhibit significant variances in earnings before interest, taxes, depreciation, and amortization (EBITDA) multiples. A comparison of two companies below gets to the root of 1) why valuation levels can vary so dramatically between what appear on the surface to be two identical companies, and 2) why it’s important for business owners to make day-to-day and long-term decisions in the context of driving long-term business value.

In Figure 1, Companies A and B each generated $50 million in revenue, are located in the same geographic region, and share a similar end market and asset base. However, in the eyes of a valuation expert, and more important the market, that’s where the similarities end.

Valuation Method Basics

Before we dive deeper into a comparison of the two companies, including what drives value, we first need to understand how companies are valued. To determine the value of a company, no matter the context, several valuation methodologies will be applied in an effort to “triangulate” the value of the company.

The most commonly used approaches are:

- Discounted cash flow analysis (DCF)

- Leveraged buyout analysis (LBO)

- Market approach

- Underlying asset approach

Although market approach, with its ease of calculation (i.e., 5x EBITDA), is the most frequently used methodology, the DCF approach has more relevance in measuring the true underlying value of a business. When buyers acquire companies, they are essentially purchasing the right to the future stream of free cash flows generated by the business (along with the assets which are in place to generate those free cash flows). By definition, free cash flow is calculated as cash flow from operations less capital expenditures:

FCF = EBIT*(1-tax rate) – Change in Net Working Capital

+ Depreciation and Amortization – Capital Expenditures

Where EBIT = Earnings Before Interest and Taxes

Conceptually, it represents cash that is “left over” after paying bills, funding everyday business activity, and investing in machinery and equipment. This excess cash is then available to pay down debt, pay out dividends, pursue acquisitions, and fund strategic growth initiatives.

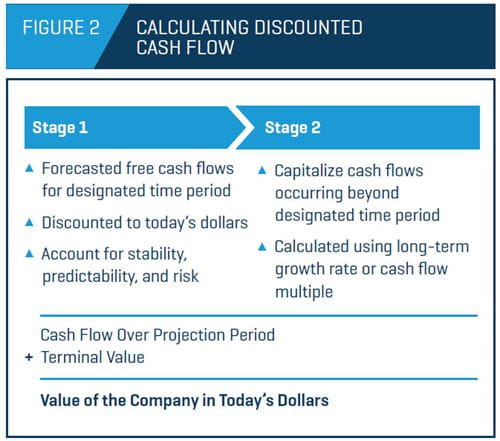

Understanding DCF

The discounted cash flow analysis is a two-stage process (Figure 2). The first stage involves taking the free cash flows forecasted over the projection period (typically five years) and equates them to today’s dollars by discounting them at a rate commensurate with the overall risk of the business. The amount of risk of the projected cash flows (i.e. stability and predictability, etc.) will impact the discount rate and, accordingly, the value (the higher the discount, the lower the value).

The second stage capitalizes all of the cash flows occurring beyond the projection period in perpetuity (the terminal value), which is commonly calculated using an expected long-term growth rate or a cash flow multiple. The sum of the present value of the cash flows occurring over the projection period, plus the terminal value, equals the value of the company in today’s dollars.

Because the buyer or current owner of the company is ultimately interested in the right to the free cash flow generated by the company, the better the company is able to clearly articulate and predict the future cash flow (i.e., the ability to produce a clear and concise road map such as a booked business schedule), the greater the credit they are likely to receive in the form of a higher purchase price.

Where the Real Work of Determining Value Begins

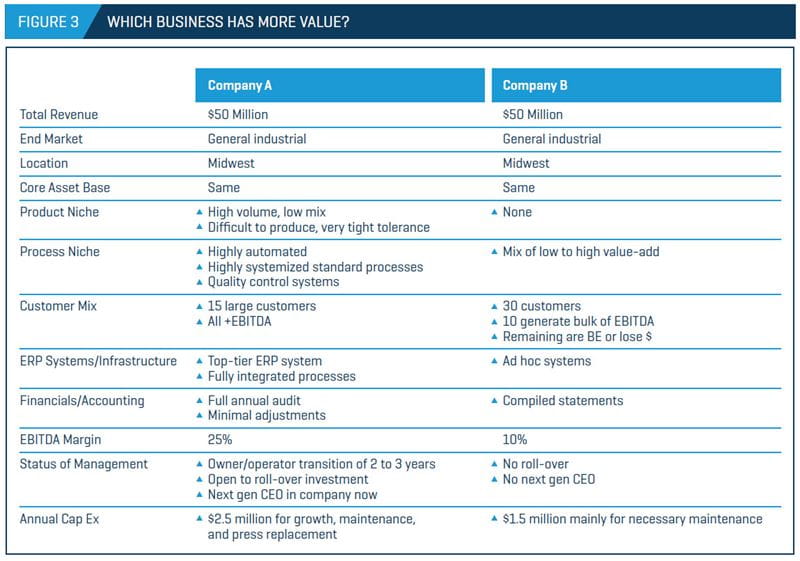

Figure 3 illustrates some of the different attributes that determine which companies are valued at the high end versus the low end of the value range. It’s evident in our comparison that Companies A and B vary broadly on annual capital expenditures – the amount each is willing to invest in the business over time, and market approach. Company A also differs from Company B in that it’s a niche market player, an important distinction that carries significant implications across all aspects of the business, especially where future free cash flow is concerned.

Before you can determine how to increase the value of the business and effect change, you need to first understand the drivers of free cash flow and how business decisions translate to a quantifiable increase in value over time, which begins with identifying the key drivers of business value. However, getting to a point where you can clearly and comfortably predict future free cash flows can be easier said than done.

That’s where the insight of professionals with a proven record of producing valuations that hold up to scrutiny over time, combined with deep experience and knowledge of the industry and sector, can make a critical difference for business owners seeking to realize the full value of the businesses they’ve built.

Evaluating the Key Drivers of Free Cash Flows for Plastics Processors

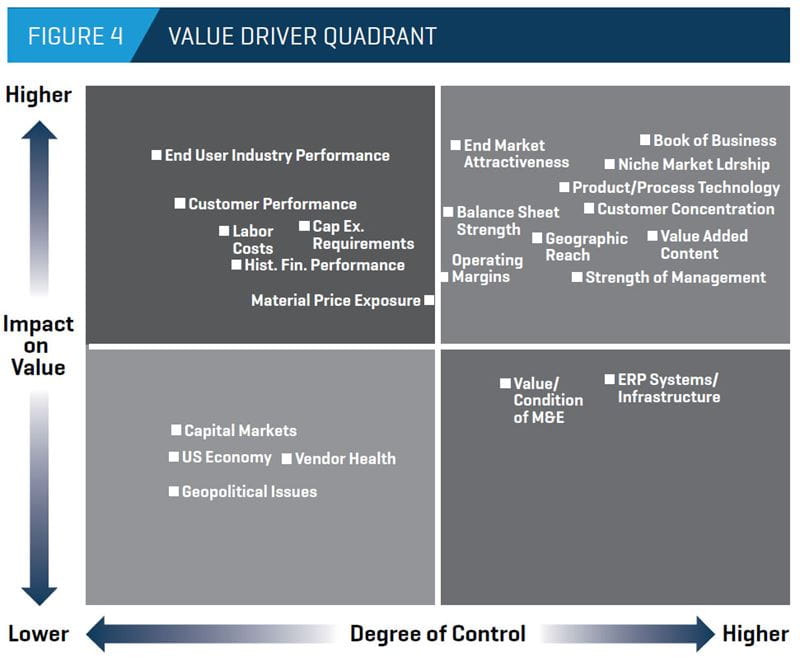

With extensive time working with plastics processors and manufacturers, and businesses throughout the industrial space, Stout professionals have amassed significant expertise in determining the relative value drivers that have the greatest impact on plastics processors. Our four-quadrant approach to assessing key value drivers, illustrated in Figure 4, is a valuable tool businesses can use to inform their short- and long-term decision-making. Key drivers are plotted based on the degree to which they impact value and the degree to which management has direct control over each factor.

Higher-Impact, Higher-Control Factors

Let’s look at how the four-quadrant tool is used to affect value. The items plotted in the upper-right quadrant of the chart represent those with the most impact on value and where management theoretically has the highest degree of relative control. Accordingly, these areas form the focus of both the buyer’s due diligence in a transaction scenario, as well as management’s value-building initiatives. The most critical “higher impact, higher control” value drivers include the following.

Book of business – The book of business (existing business running now + booked but not running business + future potential business) provides a realistic view of the company’s near-term and future revenue expectations and the sources of that revenue. The more predictable, attractive, and profitable the book of business, the more value a buyer would theoretically place on the company. In many ways, the characteristics of a company’s book of business is the culmination of all of the other value drivers.

Niche market leadership – Leadership in a particular niche offers the current owner of the business significant benefits, such as higher barriers to entry, less competition, more loyal customers, and higher profit margins. A company that commands leadership in a particular niche, resulting in aboveaverage industry margins, will be coveted by potential buyers, many of whom do not have a strong position in any aspect of their business and are looking to achieve this position through an acquisition.

End market attractiveness – Due to the widespread use of plastics in product manufacturing, a processor can find itself in the supply chain of almost any end-user industry – each of which possesses unique attributes, including growth, contraction, competitiveness, pricing pressure, maturity, cyclicality, and use of technology. The end market’s effect on the value of the company can be significant, as many acquisitions are undertaken with the specific goal of breaking into an attractive industry. Of course, the opposite is true for those in underperforming or unpopular industries.

Customer concentration – High customer concentration generally detracts from the value of the company, primarily due to the level of risk perceived by a potential buyer when a relatively small number of customers account for a significant amount of the company’s business.

Process/product technology – The ability to differentiate in a crowded marketplace based on high-value-added capabilities remains a major factor in determining value, as well as buyer considerations. Companies can add value either by offering technologically advanced proprietary products or by developing process technology, which allows them to be more nimble, efficient, and cost effective while providing better quality.

Geographic reach – A processor with a well-conceived and attractive geographic footprint will create added value and appeal to a wider array of customers and potential buyers. While extension of geographic footprint and access to emerging markets are two of the primary goals of expansion via acquisition, geographic expansion that is not driven by a clear strategy may not be productive in the end.

Balance sheet strength – By the very nature of business valuation, the strength of the balance sheet (mainly in terms of working capital and debt level) of the company does not factor directly into the enterprise value or overall value of the company. However, when it comes to determining attractiveness from an acquisition perspective, an undercapitalized, overleveraged company will, over time, tend to lag in its ability to address many of the aforementioned value drivers. Eventually “catch-up” capital expenditures will be needed on the part of the existing owner or a new buyer to maintain competitiveness, resulting in reduced future cash flows generated by the business.

Strength of management team – Management teams with a proven track record are valuable in every industry, and continuity of management can be a key factor in a successful post-transaction integration. Buyers can derive significant value from a management team with the depth and capability to execute the company’s strategic plan well into the future. An often-overlooked aspect of management in a transition setting is the length of time that owner/operator will be willing to remain with the business afterward as well as whether the next generation leader of the business is currently in place. Generally, the more continuity in management, the lower the perceived risk, resulting in a higher value.

Lower-Impact, Higher-Control Factors

Factors in the lower-right quadrant of the chart, while within the control of management and important aspects of a business, don’t have the same impact on value as the major drivers in the upper-right quadrant. ERP systems, front-end infrastructure, and value and condition of the M&E can have a detrimental impact on value if they have been neglected historically and will require an additional capital influx from a buyer. As a result, the seller may be required to accept a discount equal to or greater than the amount needed to invest in the business to make up for any historical deficiencies.

Lower-Impact, Lower-Control Factors

Items in the lower-left quadrant, such as the health of the U.S. economy or geopolitical issues, while critical to the performance of the industry as a whole, do not heavily impact the relative value of one company versus another as they tend to affect the entire industry in a similar manner.

Higher-Impact, Lower-Control Factors

Items in the upper-left quadrant can have a high impact on value, but a management team generally has minimal influence over these factors. While a company may be able to strategically move in or out of a particular customer or industry over time, timing and end-user performance are beyond the company’s control.

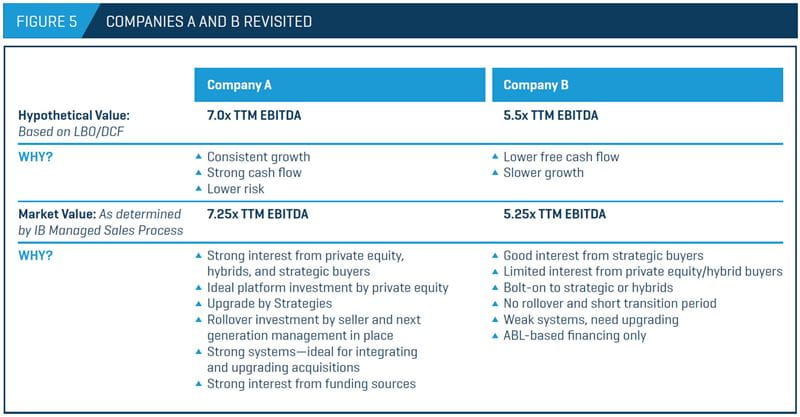

Companies A & B Revisited

Once you have a clear understanding of the factors that influence value, it becomes easier to differentiate Companies A and B from a valuation perspective. Armed with this knowledge, let’s take a second look at how Companies A and B add up (Figure 5).

As a result of focusing on the “higher-impact, higher-control” aspects of the business, and strategically navigating the “higher-impact, lower-control” factors, Company A is assigned a market value of 7.25x EBITDA, while Company B is valued at 5.25x EBITDA. Company A has solidified its place in the marketplace, attracting strong interest from private equity, hybrids, and strategic buyers by focusing on a specific niche, proactively making significant capital investments over time, and ensuring a transition plan is in place to seamlessly usher in the next generation of management, among others.

Company B, on the other hand, garners less interest from private equity or hybrid buyers due to its less defined business focus and weak, reactive approach to reinvestment in operations and infrastructure, resulting in no clear competitive advantage and an inability to differentiate itself in a crowded market. While still a potential target for strategic buyers, it commands lower value in the marketplace.

Improving Your Business Decisions

Although Company A is the clear winner in our hypothetical analysis, the good news is there are many steps Company B and plastics processors facing similar challenges can take to increase free cash flow and better position the business for long-term value at any stage of business growth. As demonstrated in Figure 5, our four-quadrant approach is a valuable tool for informing both short- and long-term business decisions. It’s also important to seek guidance from professional advisors and valuation experts with specialized expertise in mergers and acquisitions, divestitures, and restructuring who can help improve the presentation of the company now and when business owners are ready to sell or exit the business.

- Gayle S. Putrich, “US plastics industry growth setting records, SPI says,” PlasticsNews, December 3, 2015.