English

English

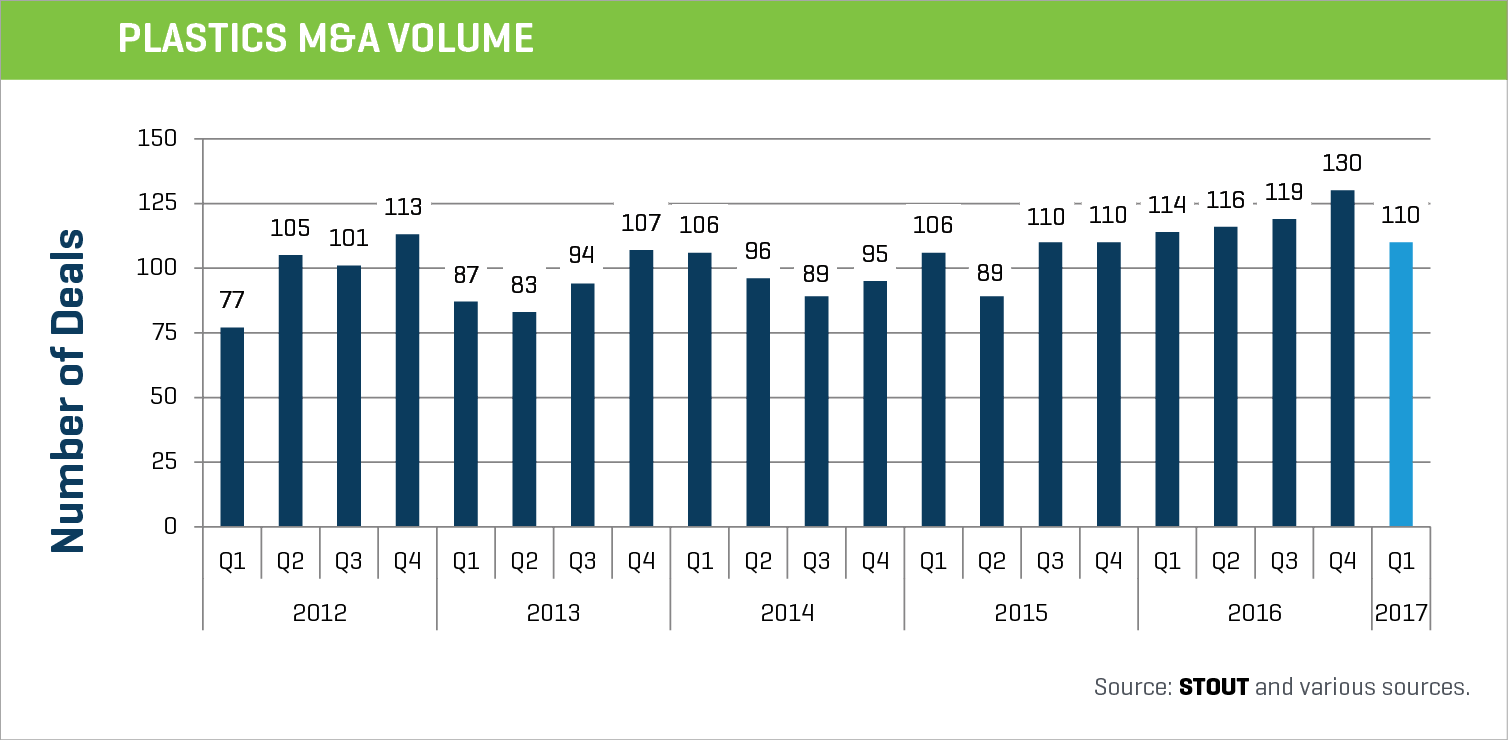

Strong plastics industry M&A activity continued in Q1 2017 with 110 transactions, a slight 3.5% decrease year over year (YOY) as compared to 2016 and consistent with the quarterly average over the past two years.

Robust activity is expected for the remainder of 2017, with solid credit markets, relatively low cost of capital, ample equity financing from strategic and financial buyers, positive macroeconomic trends, strong financial performance in many sectors, and valuation levels that continue to be at or near all-time highs.

Key Q1 Themes

- Continued strong overall plastics industry M&A activity

- Medical plastics companies remain in high demand

- Injection molding activity continues to grow, along with several niche segments

- Strategic buyers and private equity sellers saw increased activity

- Cross-border M&A activity surged

- Stock market and overall valuation levels at or near all-time highs

- Continued low cost of capital and high level of availability

- Key macroeconomic indicators remain strong

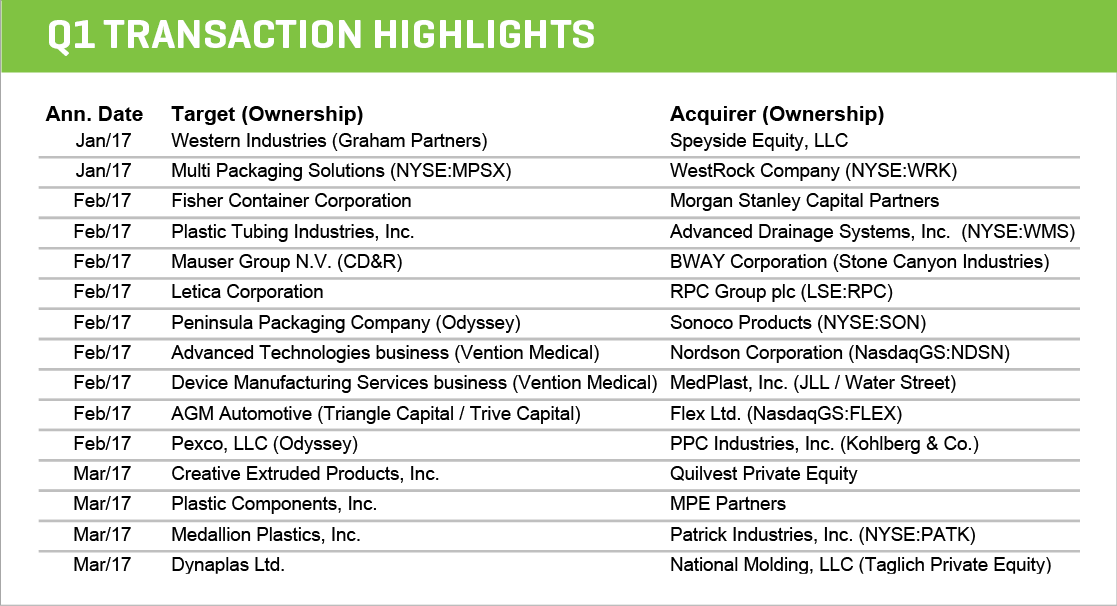

Stout Proprietary M&A Database Highlights

End Market Activity

Medical plastics M&A activity increased 25% during the first three months of 2017, YOY, and companies in that sector continue to be in high demand. Plastic packaging M&A activity also increased during the first three months of 2017, increasing 9%, YOY. Automotive and industrial activity, which tends to be more cyclical, was down 29% and 8%, respectively.

Activity by Process

M&A activity involving seven out of the 10 plastic processes tracked by Stout were flat or up during the first three months of 2017, including several niche segments such as blow and rotational molding, tool & die, and machinery. Within the three largest segments, injection molding was up 8%, while resin/compounding and extrusion were down 37% and 24%, respectively.

Buyer and Seller Trends

Strategic buyers led the charge during Q1 2017 with an 8% increase YOY, and approximately 1/3 of those buyers were public or large private companies. Financial buyers continue to deploy capital with a 5% increase YOY, while hybrid buyer (private equity-owned strategics) activity declined 39%. On the sell side, private equity sellers saw the biggest jump during the first three months of 2017 with a 21% increase YOY, while the number of companies sold by private business owners increased 4%. Corporate carveouts declined 31%.

Activity by Geography

Cross border M&A activity surged during the first three months of 2017, increasing 64%, YOY. International transaction activity was flat, while domestic activity declined 19%, YOY.

Market Trends

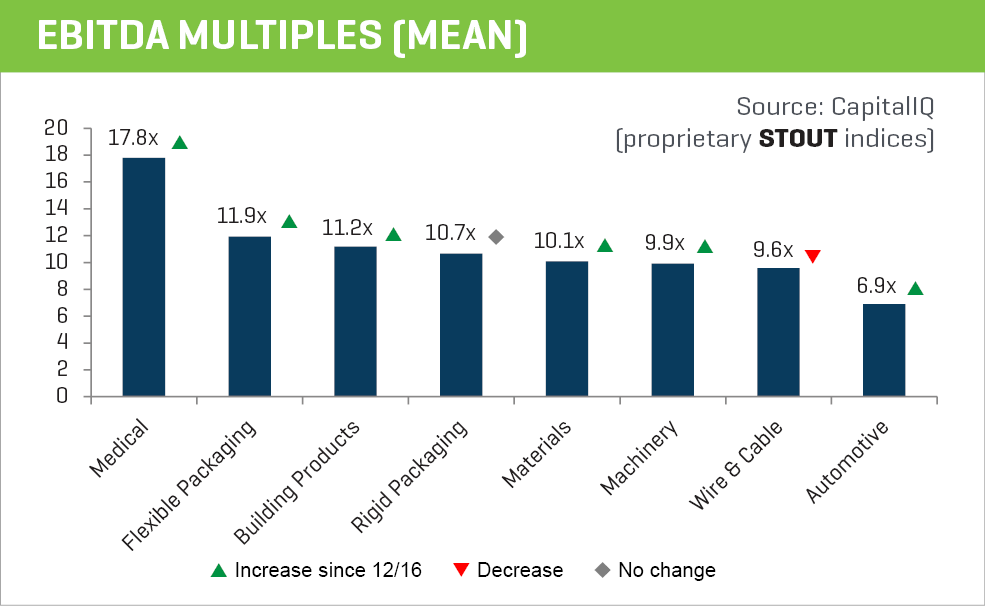

Plastics Industry Multiples

Overall stock market performance continued to be at or near all-time highs during Q1 2017 with all major market indices up for the quarter. For the first three months of 2017, the Dow was up 3.9%, while the S&P 500 and Nasdaq were up 4.6% and 8.9%, respectively. Within the plastics industry, all public company segments continue to maintain relatively high valuation levels, with seven out of eight plastics industry sectors that Stout tracks ending flat or up for the quarter.

Macroeconomic Metrics

Key macroeconomic indicators, including GDP, consumer confidence, unemployment and other metrics remained strong during the quarter. Capital markets continue to be favorable for M&A activity. Cost of capital remains relatively low and there is ample financing available for transactions. Crude oil and natural gas prices were lower during Q1 2017, although resin pricing in general was relatively flat for the quarter.