English

English

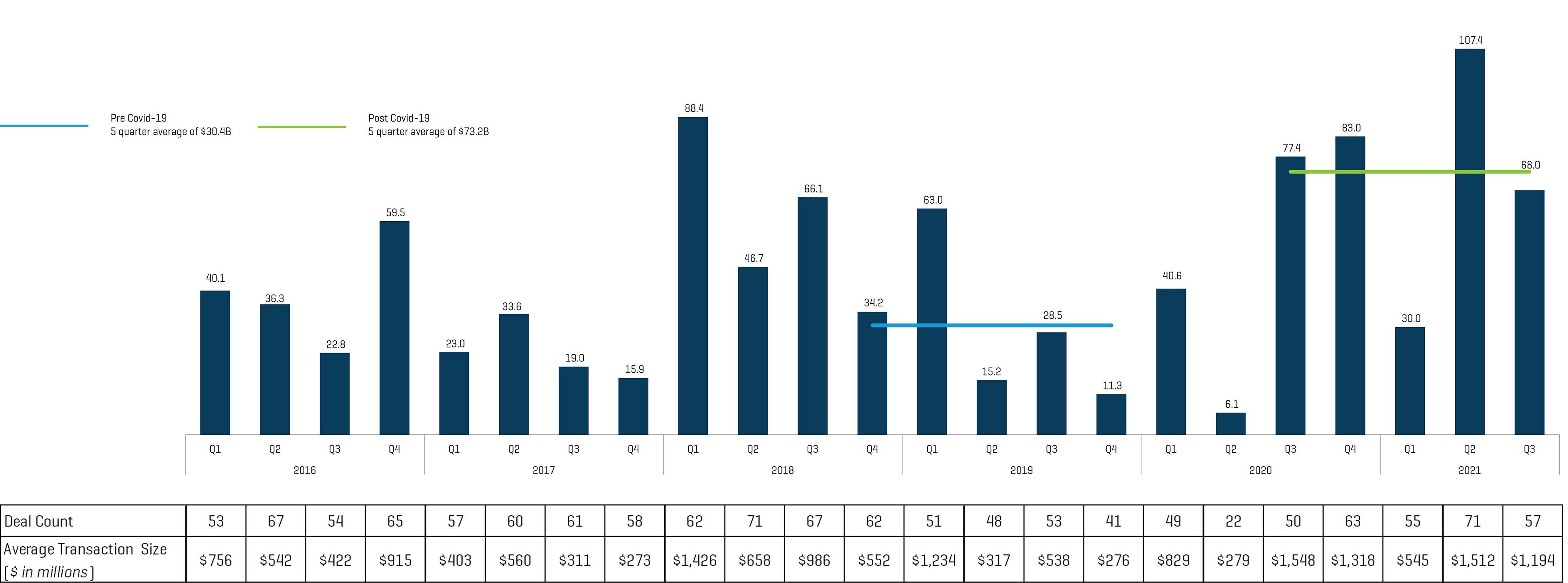

Post Covid-19 (Q3 2020), quarterly announced M&A transaction values for professional services businesses are up 140%, relative to the quarterly transaction values for the same period leading into the pandemic, with approximately $73 billion worth of deals being announced per quarter since Q3 2020. Acquirers are pursuing larger transactions, with deal sizes 62% above levels realized over the last five years. In addition, aggregate announced deal volume (announced transactions with and without deal values) is also up 48% post Covid-19.

The outlook for M&A and capital markets deal activity in professional services continues to be robust. There are many factors that contribute to this, including:

- Strong underlying fundamentals as clients continue to outsource capabilities and prioritize digital transformation initiatives

- Multiple buyer groups investing in the sector

- Increasing number of private equity firms with dedicated investment strategies for the space

- Sub-sectors continue to be extremely fragmented, despite heightened levels of M&A, and are target rich for buy & build (consolidation) strategies

Key considerations for business owners moving into 2022:

- Strategic interest is targeted – acquirers are seeking differentiated capabilities, underpinned by proprietary IP and technology

- Consolidation in partner networks has strategic implications – larger entities can reinvest incremental resources in growth, business development, and proprietary offerings

- Business owners should expect to receive a continued stream of inbound, unsolicited inquiries from investors

QUARTERLY DEAL ACTIVITY (5-YEARS)

Quarterly Deal Volume ($ in billions)

Note: Deals show above represent only those with announced deal values.

Sources: CapitalIQ, Mergermarket, public disclosures and company announcements

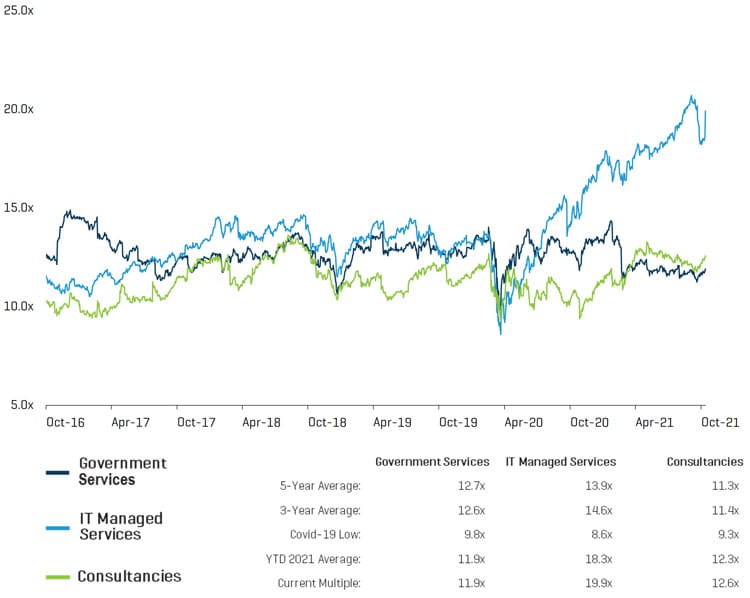

Public Market Performance

The public company indices that represent the professional services space are: Government Services, IT Managed Services, and Consultancies.

INDEXED SHARE PRICE PERFORMANCE (5-YEARS)

TEV / FORWARD EBITDA MULTIPLE (5-YEARS)

Note: Government Services index includes: ICF International, Inc. (NasdagGS :ICFI), Leidos Holdings, Inc. (NYSE: LDOS), ManTech International Corporation (NasdagGS: MANT), Science Applications International Corporation (NYSE: SAIC), Maximus, Inc.(NYSE: MMS), and Booz Allen Hamilton Holding Corporation (NYSE: BAH). IT Managed Services: Accenture plc (NYSE: ACN), Infosys Limited (NYSE: INFY), Wipro Limited (BSE: 507685), Cognizant Technology Solutions Corporation (NasdaqGS: CTSH), and Capgemini SE (ENXTPA: CAP). Consultancies: FTI Consulting, Inc. (NYSE:FCN), Huron Consulting Group Inc. (NasdaqGS: HURN), CRA International, Inc. (NasdaqGS: CRAI), The Hackett Group, Inc. (NasdaqGS: HCKT), and Information Services Group, Inc. (NasdaqGM:III).

Sources: CapitalIQ, Mergermarket, public disclosures and company announcements

Transaction Comparables

The transactions represented below are LTM bellwether deals with disclosed valuations and multiples. With proper positioning, valuation levels for publicly traded firms can provide guidance for private businesses with strong operating and financial profiles.

Sources: CapitalIQ, Mergermarket, public disclosures and company announcements

Within this professional services comparables space the mean and median EV / Revenue multiples are 1.9x and 1.3x, respectively. The mean and median EV / EBITDA multiples are 12.1x and 11.7x, relatively. Strong multiples are optimistic for companies within the space looking to enter a sales process and receive a premium valuation.

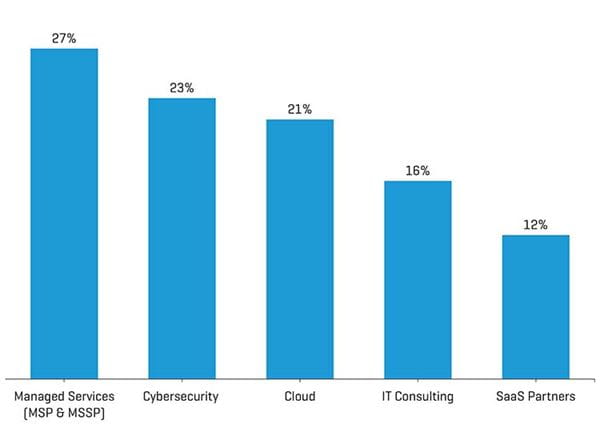

Key Capabilities and Areas of Focus for M&A in 2021

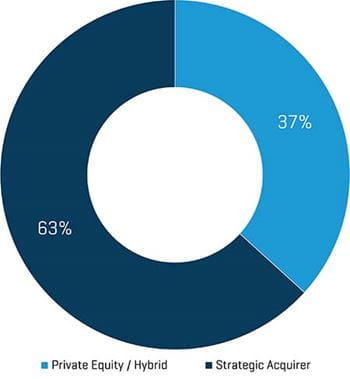

Throughout 2021 professional services transactions, there is a mix of both private equity / hybrid buyers as well as strategic buyers. The private equity and hybrid buyer pool make up 37% and strategic acquirers 63%.

Capabilities targeted in acquisitions throughout 2021 include: Managed Services (MSP & MSSP), Cybersecurity, Cloud, IT Consulting, and SaaS Partners (ServiceNow, Salesforce, Oracle, Microsoft, Workday, and Google).

CAPABILITIES TARGETED

MIX OF PRIVATE EQUITY VS. STRATEGIC ACQUIRERS IN TRANSACTIONS

Note: Percentages above are not mutually exclusive but represents number of times in which specific capabilities are referenced in deal announcements. SaaS Partners Firms include: ServiceNow, Salesforce, Oracle, Microsoft Dynamics, Workday, and Google. Sources: CapitalIQ, Mergermarket, public disclosures and company announcements

Qualitative Criteria in Focus

Expertise: Elements of the business which provide the Company with competitive advantages over the long-term

Management: Keyman risks and how much ‘work’ as well as operational support will be required to deliver on the business plan

End-Market and Capabilities: Sector dynamics throughout course of Covid-19 as well as competition and resource availability across subsectors

Intellectual Property: Scalability of proprietary tools, technologies, and resources and how they map to a well-defined market segment as well as adjacencies

Quantitative Criteria in Focus

Scale: Affords multiple advantages, providing a platform effect for growth through add-on activity and reinvestment in the business

Client Base: Blue chip clients, marquee projects, and access to ongoing relationships with these accounts are a value driver

Backlog and Pipeline: Sustainability of the backlog and pipeline through Covid-19 as well as risks for delays and potential to pull forward opportunities with additional resources

Profitability and Margins: Acute focus will be on margin durability over-time and mechanisms for sustaining profitability levels post transaction

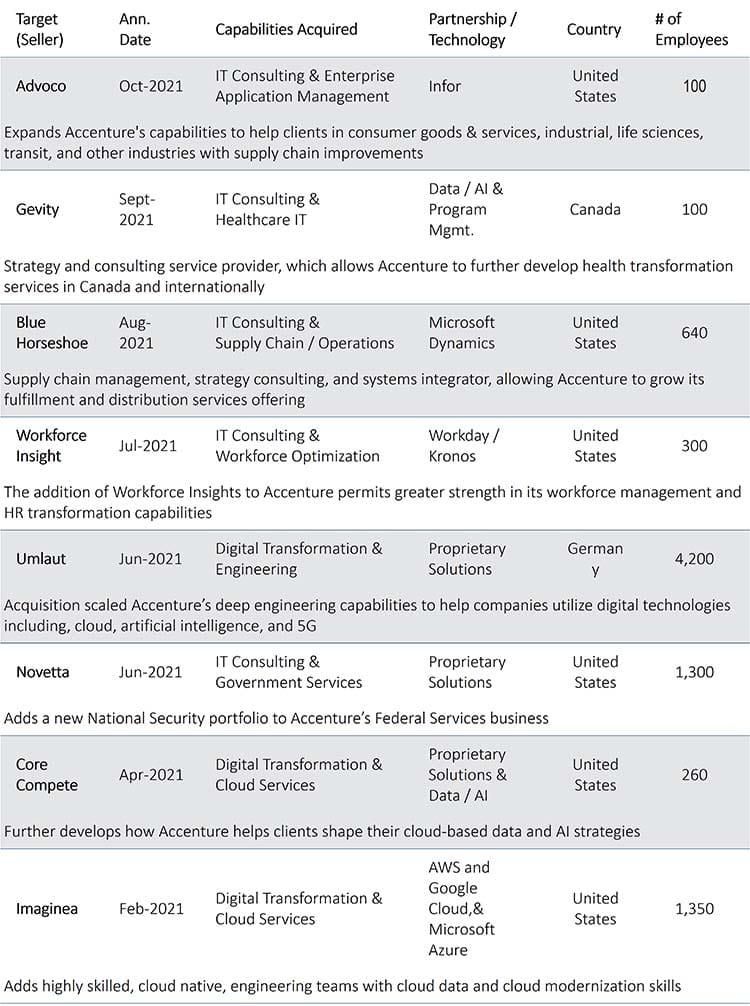

Accenture – One of the Most Acquisitive Firms in the Space

Acquisition Summary Statistics:

- Number of Deals: 54 during the last twelve months (9/30/2021)

- Average Deal Size: ~370 employees

- Total Employees Acquired: ~16,500

- Total Investment: $4.1 billion

- Investment per Deal: $77 million

- Investment per Employee Acquired: ~$254K

- Targeted Capabilities: E-commerce, Healthcare IT, Workforce Management, Supply Chain, Cloud Integration, and Implementation

- Targeted Partner Channels: AWS Cloud, Google Cloud, Microsoft Azure, Microsoft Dynamics, Oracle, and SAP

Note: Investment per Deal and per Employee Acquired calculated using Accenture’s acquisition investment TTM (8/31/2021) however deal count is TTM (9/30/2021). Sources: CapitalIQ, Mergermarket, public disclosures and company announcements

Key Observations

Reviewing Accenture’s acquisitions over the last twelve months provides visibility into the capabilities and industries which are areas of strategic growth. The Company has invested heavily in business, IT, and digital transformation consultancies with cloud integration and implementation capabilities. Supply chain capabilities were also a focal point in several transactions.

Acquisition targets had proprietary offerings as well as a range of partnership strategies. These partnership models ranged from firms with one vendor as well as groups with a broad range of partners.

Convergence in the following areas continues to be a major theme:

- Agency and marketing capabilities complement analytic and consultancy offering

- Digital Engineering capabilities used to enrich user experience, digital marketplaces, E-commerce platforms, and digital products

- Cyber and physical security, leveraging shared data, and offering complete enterprise solutions

- Requirements of commercial customers and US Federal Agencies

NOTABLE ACQUISITIONS