English

English

This is an exciting time for the Material Handling industry. Business is booming due in part to e-commerce. E-commerce and omnichannel marketing are transforming traditional supply chains, forcing all companies to change the way they move, track, and store material. Retailers, wholesalers, manufacturers and logistics companies are erecting enormous fulfillment centers and utilizing all available warehouse space. According to the Wall Street Journal, warehouse space is at its tightest since 2000. Companies are utilizing integrated material handling systems, state-of-the-art technology, and automation. They must evolve because consumers and businesses have grown accustomed to low cost two-day shipping. Thank you, Amazon.

Key Takeaways

- E-commerce and omnichannel marketing are driving today’s Material Handling boom

- SIGMAT performance vs. diversified indices signals favorable outlook for the industry

- M&A valuation multiples across many industries are at historical highs

- Q2 Material Handling forward trading multiples far exceed historical averages

- Small material handling system integrators may be ripe for consolidation

- Q2 saw significant acquisition activity due in part to excitement surrounding the Material Handling industry

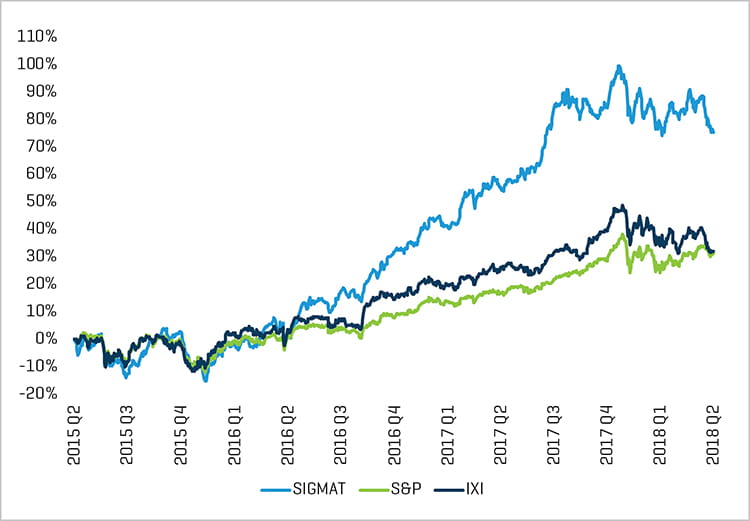

Stock price performance of Stout’s Index of Global Material Handling Companies (the “SIGMAT”)[1] highlights the industry’s favorable performance relative to more diversified indices (Figure 1).

FIGURE 1. SIGMAT PERFORMANCE VS. DIVERSIFIED INDICES (LAST 3 YEARS)

Source: S&P Capital IQ and Stout Research

M&A Market

Perhaps equally exciting is today’s mergers and acquisitions (M&A) market. Global M&A values reached a record $2.5 trillion in the first half of 2018, according to Thomson Reuters Deals Intelligence. In the U.S., valuation multiples across many industries are at historical highs primarily due to an imbalance between the demand from buyers and the supply of sellers. High demand for acquisitions is driven by excessive levels of undeployed private equity capital (or “overhang”). This overhang in the U.S. now exceeds $550 billion, making private equity eager to put capital to work.

U.S. corporations may be equally eager to put capital to work. Corporations have high cash availability because of tax reform, repatriation, and a favorable lending environment. These factors contribute to the high demand for acquisitions. The supply side, however, is not keeping up. There simply are not enough sellers to satisfy the demand from buyers. This imbalance has helped create today’s seller’s market characterized by historically high valuations.

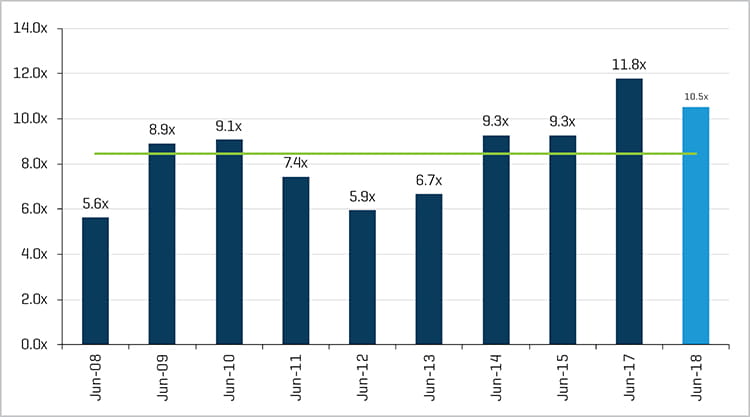

Within the Material Handling industry, public company trading valuation multiples for companies are well above historical averages. Median forward EBITDA of companies in the SIGMAT was 10.5x at the end of the second quarter, well above the 10-year second-quarter average of 8.5x (Figure 2).

FIGURE 2. SIGMAT FORWARD EBITDA MULTIPLES (VS. 10-YEAR AVERAGE)

Source: S&P Capital IQ and Stout Research

Material Handling M&A activity has been marked by a handful of mega deals in recent years. In 2016, KION Group purchased Dematic for $3.2 billion and Honeywell purchased Intelligrated for $1.5 billion. Dematic and Intelligrated were the two largest U.S.-based systems integrators at the time, making the acquisitions transformative for the domestic Material Handling industry landscape. The timing of acquisitions also signaled that the industry may have been at the front end of an unprecedented growth phase.

In addition to Dematic and Intelligrated, the material handling system integrator landscape consists of several global giants, including SSI Schaefer and Daifuku. The big are getting bigger, as revenue for the top 20 global integrators grew by over 16% in the last fiscal year and order backlogs are growing. Beneath the top tier, there is a fragmented second tier of systems integrators that are also performing well and could be ripe for consolidation. These smaller integrators, which serve small to midsized companies are benefiting from the favorable industry trends, as companies of all sizes need to adapt and transform their supply chains. Large integrators have their hands full with the large projects, leaving plenty of opportunities for smaller integrators. Consolidation among a few of these players could allow them to effectively compete for big projects.

In addition to systems integrators, the Material Handling industry consists of several subsectors, including manufacturers and suppliers of (i) automated guided vehicles, (ii) conveyors and sortation products, (iii) cranes/hoists, (iv) dock equipment, (v) lift trucks, (vi) mezzanines/platforms, (vii) storage and retrieval systems, (viii) racks/racking, (ix) safety solutions, and others. The excitement surrounding the Material Handling industry is favorably impacting each of these subsectors and is leading to M&A activity. Companies looking to capitalize on the tremendous growth potential of Material Handling are making acquisitions. Noteworthy second-quarter transactions include the following:

Tsubaki Acquires Central Conveyor Company

On June 15, New State Capital Partners closed on its sale of Central Conveyor Company to U.S. Tsubaki Holdings, a subsidiary of Japan-based Tsubakimoto Chain Co., for approximately $140 million. Central Conveyor manufactures custom material handling systems, storage/retrieval systems, and automated conveyance solutions. Tsubaki sees significant growth potential in the U.S. market, and this acquisition provided it with access to blue-chip U.S. customers, particularly within the automotive industry.

Patricia Industries Acquires Piad Group

Patricia Industries closed its acquisition of Sweden-based Piab Group from private equity firm EQT on June 14. Piab provides automation products to companies within e-commerce, logistics, food, and other industries. Piab’s products are utilized in a variety of manufacturing and material handling settings and provide solutions for companies looking to increase efficiency in an increasingly automated and competitive world.

CapitalWorks Acquires C&M Conveyor

Cleveland-based private equity firm, CapitalWorks, purchased C&M Conveyor from Blue Sage Capital on June 5. C&M Conveyor is a designer and manufacturer of automated material handling and conveying systems. It has a specialization in the corrugated box industry and seems to be well-positioned to benefit from favorable trends within Material Handling.

Hyster-Yale Materials Handling Acquires China Business

Lift truck manufacturer, Hyster-Yale, acquired a 75% stake in China-based Zhejiang Maximal Forklift Company for approximately $90 million on June 1. This was a strategic acquisition to expand Hyster-Yale’s global lift truck manufacturing capabilities and expand its presence in China’s rapidly expanding Material Handling industry.

SSI Schaefer Acquires Incas

Global material handling systems integrator, SSI Shaefer, acquired Italy-based Incas S.p.A. on May 28. The Incas acquisition strengthened Shaefer’s southwestern Europe presence and enabled it to become the strongest player within the Italian intralogistics market.