English

English

Benjamin Cloutier co-authored this report.

Introduction

Inpatient Rehabilitation Facilities (IRFs) are specialized healthcare institutions that provide intensive rehabilitation services to patients recovering from serious medical conditions such as strokes, spinal cord injuries, brain injuries, major orthopedic surgeries, and neurological disorders. These facilities offer multidisciplinary care, including physical therapy, occupational therapy, and speech-language pathology, under the supervision of rehabilitation physicians and specialized nursing staff. Unlike skilled nursing facilities (SNFs) or general acute care hospitals, IRFs focus on short-term, high-intensity rehabilitation to help patients regain independence and improve their functional abilities.

As with IRFs, long-term acute care hospitals (LTACHs) are unique facilities designed to provide extended medical care for patients with serious, complex, and chronic conditions that require prolonged hospitalization. Unlike traditional acute care hospitals, where patients typically stay for a few days, LTACH patients often require weeks or even months of specialized treatment. These facilities cater to individuals who need intensive medical care, such as ventilator support, complex wound management, prolonged intravenous medications, or rehabilitation for multi-organ failure and severe infections. LTACHs help bridge the gap between short-term hospital stays and post-acute care settings like SNFs or home health care.

LTACHs and IRFs serve critical roles in the continuum of care, ensuring that patients with severe, complex, and rehabilitative needs receive the appropriate level of medical attention and therapy. These facilities reduce the burden on traditional acute care hospitals, lower readmission rates, and improve patient outcomes by providing targeted care.

LTACHs focus on treating patients requiring prolonged hospital-level care, typically for severe respiratory failure, multi-organ dysfunction, complex wound care, or long-term intravenous medications. These patients often cannot be discharged to a skilled nursing facility or home care due to the intensity of medical services required. By extending acute-level treatment, LTACHs help stabilize critically ill patients, preventing frequent hospital readmissions and allowing for a smoother transition to lower acuity sites of care.

IRFs are essential for patients recovering from serious injuries, neurological disorders, strokes, or major surgeries, helping them regain mobility, cognitive function, and daily living skills. Unlike SNFs, IRFs provide intensive, physician-led therapy; this focused approach results in faster recovery times, higher patient independence, and lower long-term healthcare costs by preventing complications and reducing the need for future hospitalizations.

Both LTACHs and IRFs play a significant role in improving healthcare efficiency by ensuring that patients receive the appropriate level of care at the appropriate time. Their presence can free up acute care hospital beds, enabling acute care hospitals to focus on emergency and short-term care needs while transitioning patients who require longer recovery periods to specialized settings. This approach to care can help reduce overall healthcare costs, prevent avoidable complications, and enhance patient quality of life.

With an aging population and an increasing number of patients with complex conditions, the demand for LTACHs and IRFs continues to grow. These facilities fill crucial gaps in post-acute care, ensuring that patients receive the specialized medical attention and rehabilitation they need to regain independence and improve long-term health outcomes. Their role in the healthcare system is valuable, helping lead to better patient outcomes, cost-effective care solutions, and a bridge between short-term acute care hospital stays and home-based recovery.

Federal Reimbursement Trends

IRF Prospective Payment System1

In August 2025, CMS released the final rule for the Inpatient Rehabilitation Facility Prospective Payment System (IRF PPS) for FY 2026, effective October 1, 2025, through September 30, 2026. This rule introduced several key updates impacting IRFs. CMS finalized a 2.6% increase in IRF PPS payment rates for FY 2026. This adjustment is derived from a 3.3% market basket update, reduced by a 0.7% productivity adjustment. The standard payment conversion factor will rise from $18,907 to $19,3712,3, which serves as the base per-discharge amounts used to calculate Medicare IRF PPS payments before case-mix and other adjustments. These updates reflect CMS’s ongoing efforts to refine payment systems and quality reporting for IRFs, ensuring that reimbursement rates align with current economic conditions and that quality metrics effectively capture patient care standards. IRFs that do not comply with the Quality Reporting Program (QRP) requirements face a two-percentage point reduction in their Annual Increase Factor. CMS estimates this update will result in an overall increase of $340 million in aggregate IRF payments for FY 2026.

CMS has finalized several changes to the IRF QRP, including the removal of two COVID-19 quality measures and removal of four Social Determinant of Health (SDOH) data elements. These updates aim to enhance the quality, comprehensiveness, and relevance of data collected, ultimately improving patient care outcomes.

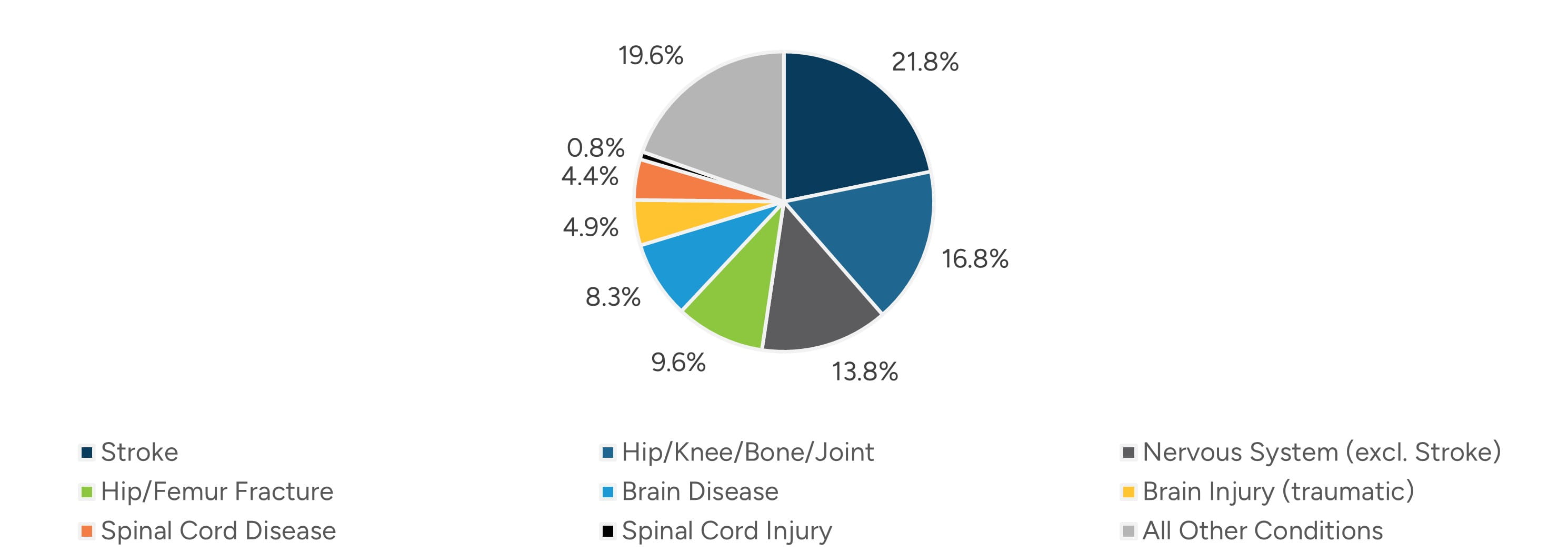

As outlined in the QRP data, the top patient case condition reported for the 2024 reporting period was Stroke at 21.8%, as further shown in Figure 1.

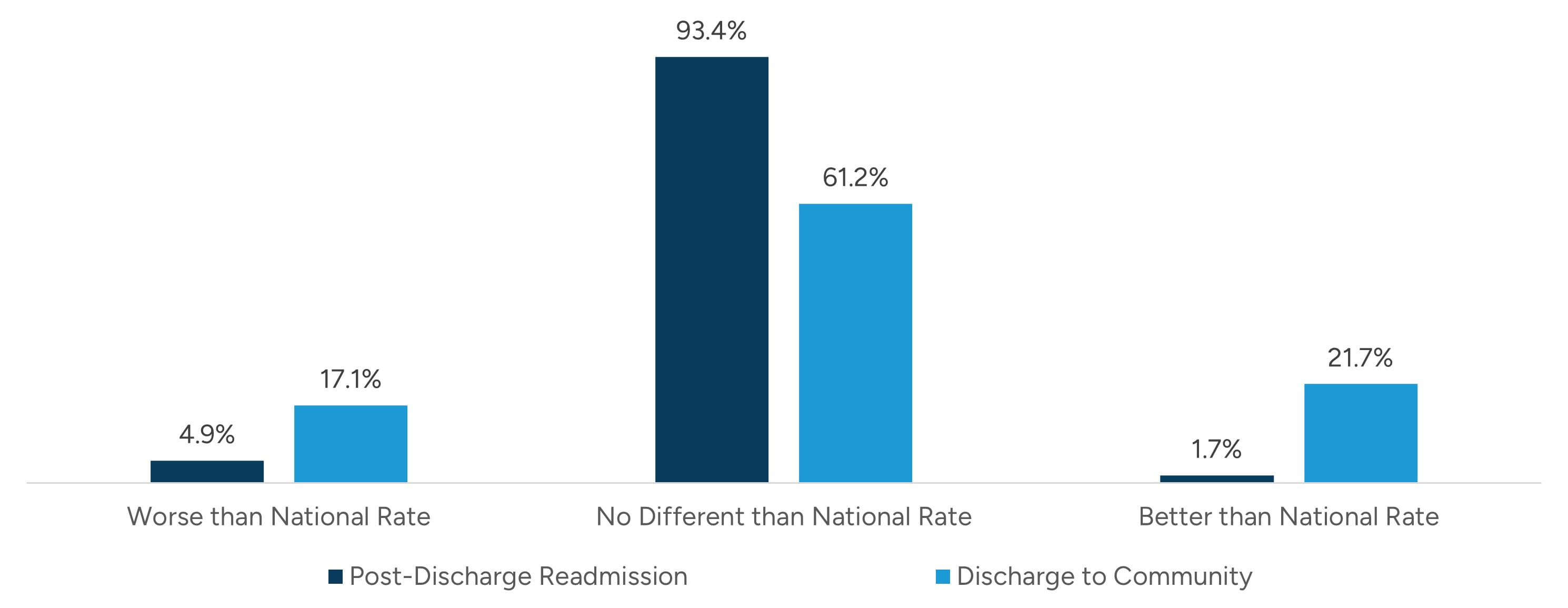

The QRP data also outline certain discharge statistics for the reporting hospitals, as outlined in Figure 2.

Figure 1: IRF Patient Case Mix - Top Conditions

Figure 2: IRF Provider Performance vs. National Rate

LTACH Prospective Payment System4

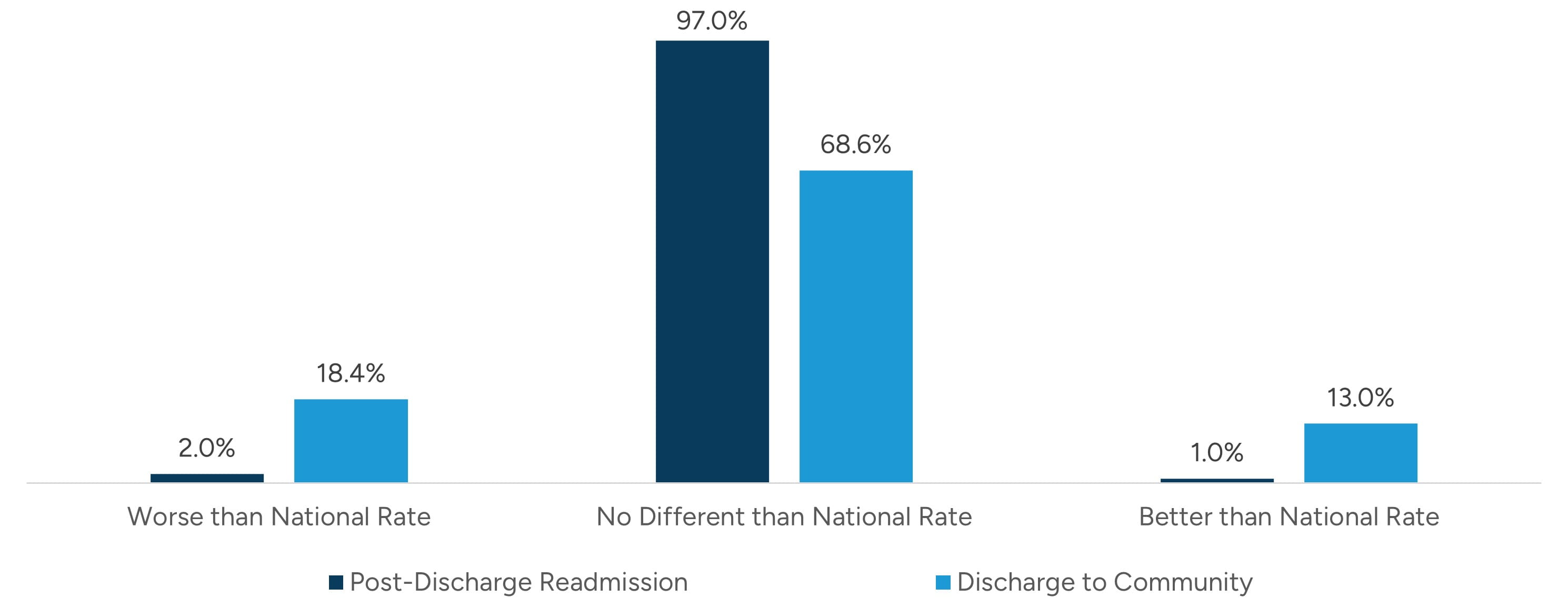

In July 2025, CMS released the FY 2026 Final Rule for the Long-Term Care Hospital Prospective Payment System (LTACH PPS), effective October 1, 2025, through September 30, 2026, finalizing a 2.7% increase in the standard LTACH PPS rate, reflecting a market basket increase of 3.4%, with a productivity adjustment reduction of 0.7%. Similar to IRFs, facilities that fail to comply with QRP requirements may be subject to a two-percentage point reduction. Like the IRF program, this has been effective in improving patient outcomes, as only 2% of LTACHs perform worse than the national post-discharge readmission rate and 18% perform worse than the national rate for discharge to community. Discharge statistics reported for LTACHs are outlined in Figure 3.

Figure 3: LTACH Provider Performance vs. National Rate

Figure 4: Top 10 States by LTACH Count

The LTACH QRP modified reporting requirements for the COVID-19 vaccine as well as removed four SDOH standardized patient assessment data elements in the FY 2026 rule.

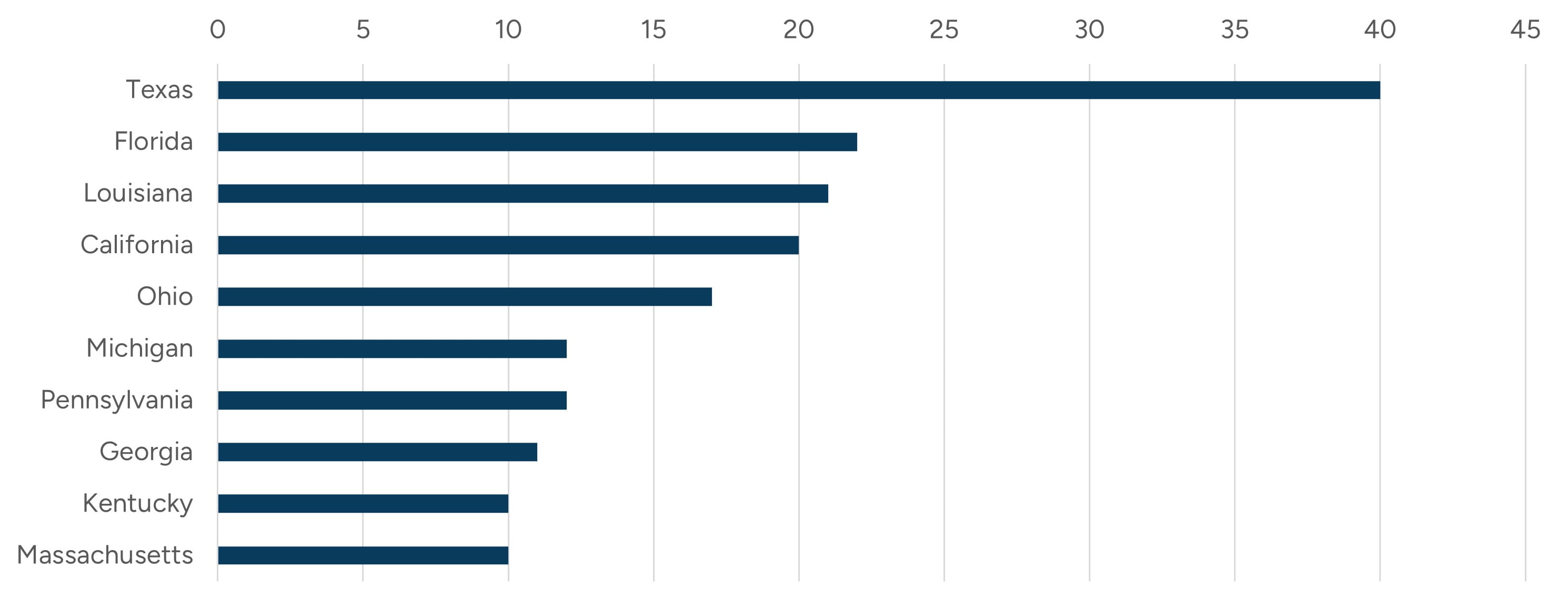

Utilizing the QRP data, Figure 4 outlines the top states in which LTACHs are located.

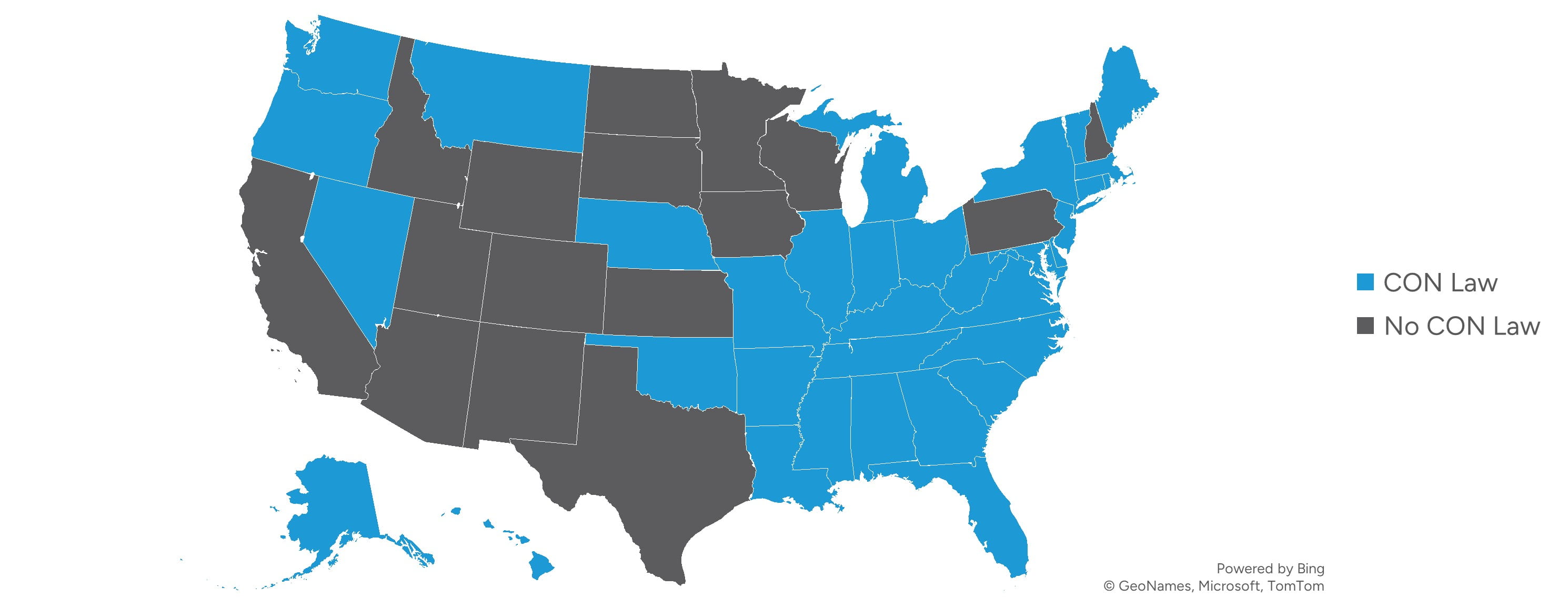

Certificate of Need Reform

Certificate of Need (CON) laws are state regulatory mechanisms for approving major capital expenditures and projects for certain healthcare facilities. In a state with a CON program, a health planning agency or other entity must approve the creation of certain new healthcare facilities or the expansion of an existing facility’s services in a specified area. CON programs primarily aim to control healthcare costs by restricting duplicative services and determining whether new capital expenditures meet a community need. Currently, 35 states and Washington, D.C., operate CON programs, with wide variation by state.5

Figure 5: Map of Certificate of Need States

In recent years, states are increasingly re-evaluating their CON laws, with some maintaining strict regulations while others move toward reform or repeal. Supporters argue that CON laws help control healthcare costs, prevent unnecessary facility duplication, and ensure services align with community needs. Critics claim these laws create barriers to competition, limit access to care, and hinder healthcare innovation. Several states have enacted significant CON reforms in recent years that materially impact the development of IRFs and LTACHs. Florida eliminated CON requirements for LTACHs effective July 1, 2019, and IRFs effective July 1, 2021, through HB 21.6 South Carolina enacted sweeping CON reform through SB 164, signed May 19, 2023, which removes CON requirements for nearly all healthcare facilities, including specialty hospitals, effective January 1, 2027.7 Tennessee passed Public Chapter 985 in May 2022, which phases out CON requirements for certain healthcare facilities, including a phaseout for LTACHs as of December 1, 2027.8

Collectively, these reforms signal a broader trend toward deregulation in select states, creating more favorable environments for IRF and LTACH investment and capacity growth. The debate over CON laws remains ongoing, with growing momentum for deregulation as policymakers weigh market competition against healthcare planning.

Population Impacts

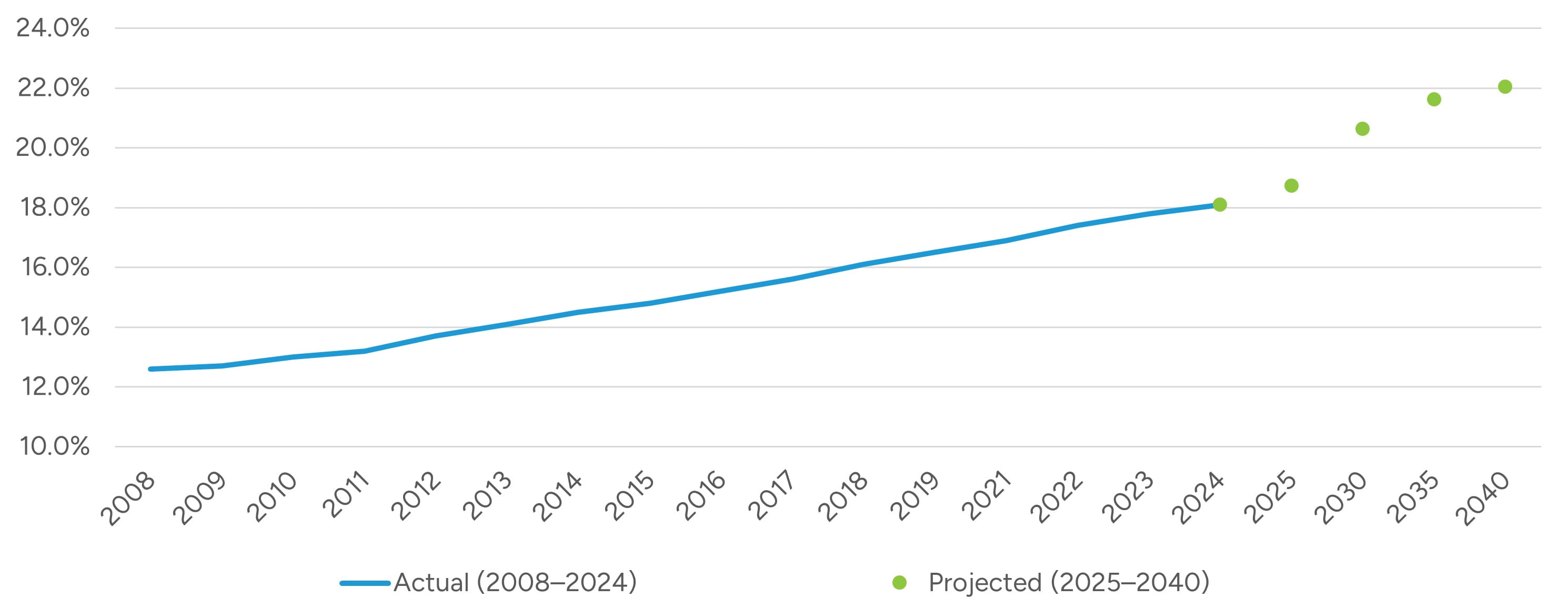

As the U.S. population continues to age, the demand for rehabilitation services in IRFs and LTACHs is expected to rise significantly. Utilizing data from Kaiser Family Foundation (KFF), adults aged 65 or more have increased in total percentage of the population every year since 2008, rising from 12.6% in 2008 to 18.1% in 2024.9 By 2030, all baby boomers will be over the age of 65, and by 2034, there will be more adults over 65 than children.10

Figure 6: Population Distribution - % of People Age 65+ in United States

This demographic shift will increase the number of elderly individuals with complex health conditions, requiring specialized care, such as post-surgical rehabilitation, stroke recovery, and management of chronic diseases like heart disease, diabetes, and dementia. As these conditions become more prevalent among older adults, both IRFs and LTACHs will need to expand services to meet this growing demand for rehabilitation and long-term care.

The aging population will also increase the prevalence of functional decline, requiring longer recovery times and more intensive rehabilitation. IRFs will experience higher demand for services focused on mobility, strength, and restoring independence, while LTACHs will see more patients with multi-comorbidities needing extended care, including respiratory therapy, wound care, and post-surgical recovery. Medicare and Medicaid will be the primary sources of funding for many elderly patients, which could impact reimbursement rates and financial viability for both types of facilities. The aging population’s increased reliance on these programs will drive higher patient volumes.

Insights from Publicly Traded Companies

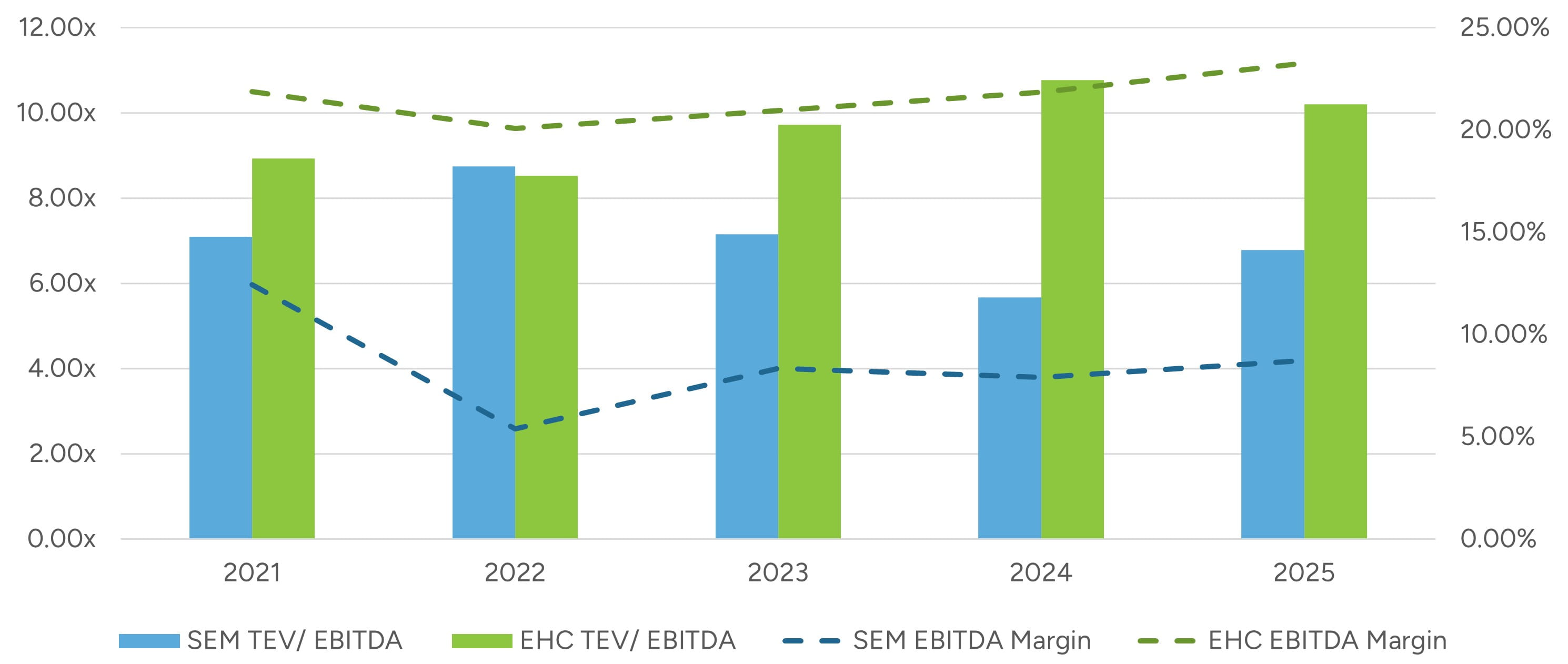

Publicly traded companies that are active in the IRF and LTACH industry are useful for analyzing specific industry trends, transaction activity, and valuation multiples. Encompass Health Corporation (NYSE: EHC) and Select Medical Holdings Corporation (NYSE: SEM) are the two largest publicly traded companies in the space.

Based on review of 2025 financial statements, SEM generates approximately 45% of its revenue from LTACHs, and 24% of its revenue from IRFs; however, given the higher margins generated from IRFs, over half of SEM’s adjusted EBITDA is generated by its IRF segment. In contrast, EHC operates purely in the IRF sector, after spinning off its home health and hospice business into Enhabit, Inc. in 2022. Figure 7 outlines the trend of valuation multiples for the two companies over the past year.

Figure 7: Total Enterprise Value to EBITDA Multiples and EBITDA Margins11

It should be noted that SEM spun off Concentra Group Holdings Parent Inc. (NYSE: CON) on November 25, 2024, while EHC spun off Enhabit, Inc. (NYSE: EHAB) on July 1, 2022. These actions may have impacted margin and valuation trends before and after these events.

While it can be helpful to look at valuation multiples of public companies, there are limitations and other factors that need to be considered when comparing to private businesses. Encompass and Select Medical are relatively large in size and scope, which generally reduces overall business risk relative to a single hospital. Additionally, as mentioned earlier SEM operates in two main segments: IRFs and LTACHs. Diversified revenue sources can also typically reduce overall company risk compared to a single hospital.

SEM and EHC earnings calls, investor presentations, and other public filings provide insights into their performance and the overall state of the IRF and LTACH sectors.

Select Medical Holdings Corporation (NYSE: SEM)

SEM delivered strong financial results in 2025, showing the effects of strategic expansion. The IRF segment remains the company’s primary growth engine. In 2025, IRF revenue increased 16.1% to $1.29 billion, with adjusted EBITDA rising 13.4% to $278.6 million and adjusted EBITDA margins of 21.6% (down modestly from 22.1% in 2024). IRF volume growth was strong, with admissions increasing 9.3% and revenue per patient day rising 5.9%. During 2025, Select added 212 IRF beds and, across 2026 and 2027, expects to add approximately 399 additional beds, the vast majority of which appear to be related to IRF (including 166 beds already added early in 2026). Recent and upcoming openings include facilities with Cleveland Clinic (Ohio), Baylor Scott & White (Texas), CoxHealth (Missouri), Banner Health (Arizona), and AtlantiCare (New Jersey).

In contrast, Select Medical’s commentary on the LTACH sector reflects a more measured growth profile. In 2025, LTACH revenue increased 1.4% to approximately $2.48 billion, but adjusted EBITDA declined 12.0% to approximately $265.4 million, with adjusted EBITDA margins compressing from 12.3% to 10.7%. Admissions increased modestly (1.0%), revenue per patient day grew 2.4%, and occupancy improved slightly to 69%. Labor conditions have stabilized meaningfully since the post-pandemic peak in agency usage, with agency staffing now approximately 15% of the labor mix and overall labor margins running near targeted levels. While reimbursement complexity and regulatory oversight remain structural considerations for the LTACH sector, management does not anticipate significant high-cost outlier headwinds in 2026.

Overall, Select Medical continues to position itself as one of the largest operators of critical illness recovery hospitals (104 facilities) and rehabilitation hospitals (38 facilities) in the United States. The company appears focused on scaling its higher-growth IRF platform through joint ventures with major health systems while managing reimbursement and cost pressures in LTACH.

Encompass Health Corporation (NYSE: EHC)

Encompass Health is the nation’s largest owner and operator of inpatient rehabilitation hospitals, with 173 IRFs across 39 states and Puerto Rico as of December 31, 2025. The company treated approximately 263,300 discharges in 2025, generating $5.94 billion in net operating revenue and $1.27 billion in adjusted EBITDA, reflecting 10.5% and 14.9% year-over-year growth, respectively. These results underscore continued structural strength in the IRF industry, supported by favorable demographic trends, constrained bed supply nationally, and increasing patient acuity. Management has consistently highlighted the widening demand–supply imbalance, noting that, while the Medicare-eligible population continues to expand, the number of IRFs nationally has remained relatively stable over the past decade.

From a strategic standpoint, EHC continues to invest aggressively in capacity expansion. In 2025, the company opened eight de novo hospitals totaling 390 beds and added 127 beds to existing hospitals, for total net bed additions of 517. Occupancy increased to 75.9% for the full year 2025, up from 74.6% in 2024, reinforcing management’s thesis that incremental capacity is being absorbed efficiently. Looking forward, 2026 guidance contemplates eight additional new hospitals (389 beds) and approximately 175 bed additions to existing hospitals.

Labor conditions improved meaningfully in 2025, contributing to margin expansion. Salaries and benefits declined to 51.9% of revenue in Q4 2025, down from 53.9% in the prior year period, reflecting lower premium labor (i.e., contract labor, sign-on, and shift bonuses) utilization despite hospital openings and capacity growth. However, management expects 3.0% to 3.5% wage inflation in 2026, reinforcing labor as the largest and most margin-sensitive cost category.

Regulatory headwinds continue to increase, particularly under the Review Choice Demonstration (RCD), which now affects IRFs in multiple states and subjects Medicare claims to pre-claim review processes. Additionally, the new Transforming Episode Accountability Model (TEAM) introduces a mandatory bundled payment framework beginning in 2026 across 189 markets. While only about 2% of EHC’s discharges fall within TEAM parameters based on 2024 data, bundled payment expansion represents a longer-term structural shift toward cost accountability in post-acute care.

Overall, Encompass’s 2025 performance reflects durable industry fundamentals: favorable demographics, persistent supply constraints, pricing support from Medicare updates, and operational leverage from disciplined labor management.

Medicare Cost Reports12

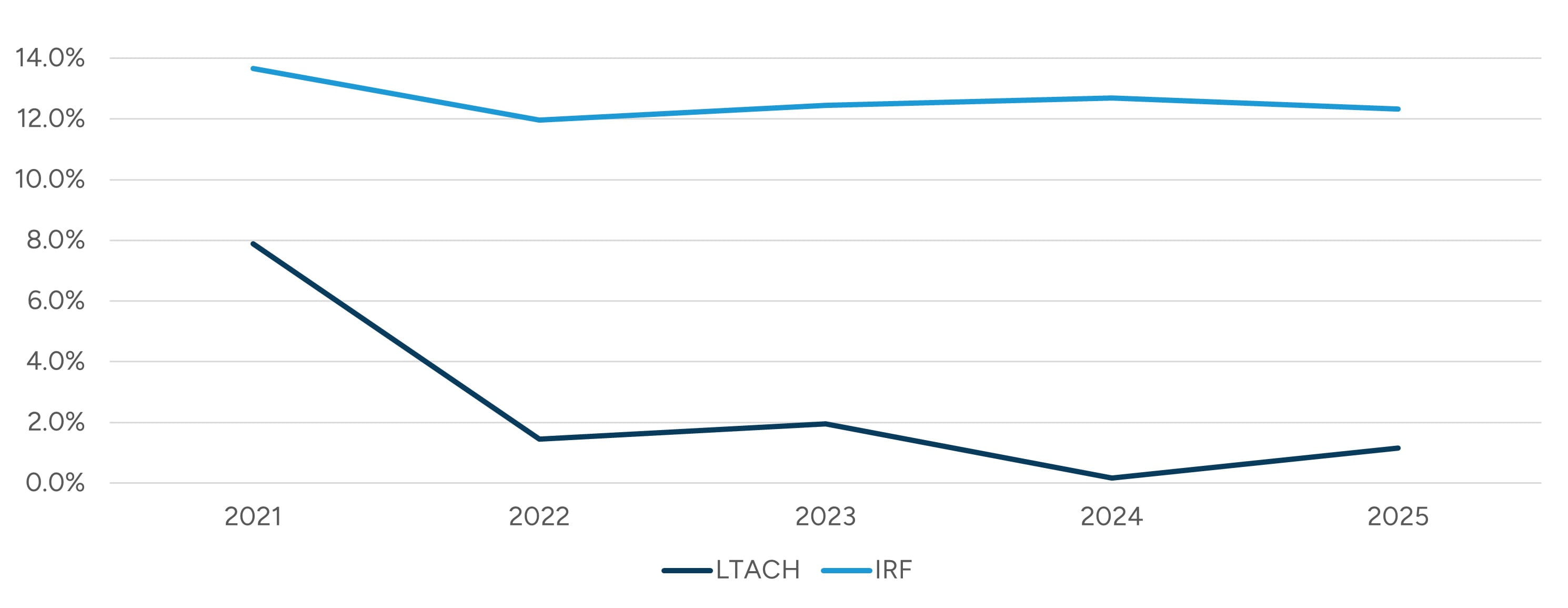

Medicare cost reports can also provide insights into the operations of LTACHs and IRFs. Figure 8 below outlines EBITDA margins for both types of facilities over the last five years. IRFs have shown more favorable EBITDA margin trends as compared to LTACHs over the historical period, which is consistent with insight from SEM’s operating segments discussed previously, in which IRF margins are notably higher than LTACH margins.

Figure 8: EBITDA Margins

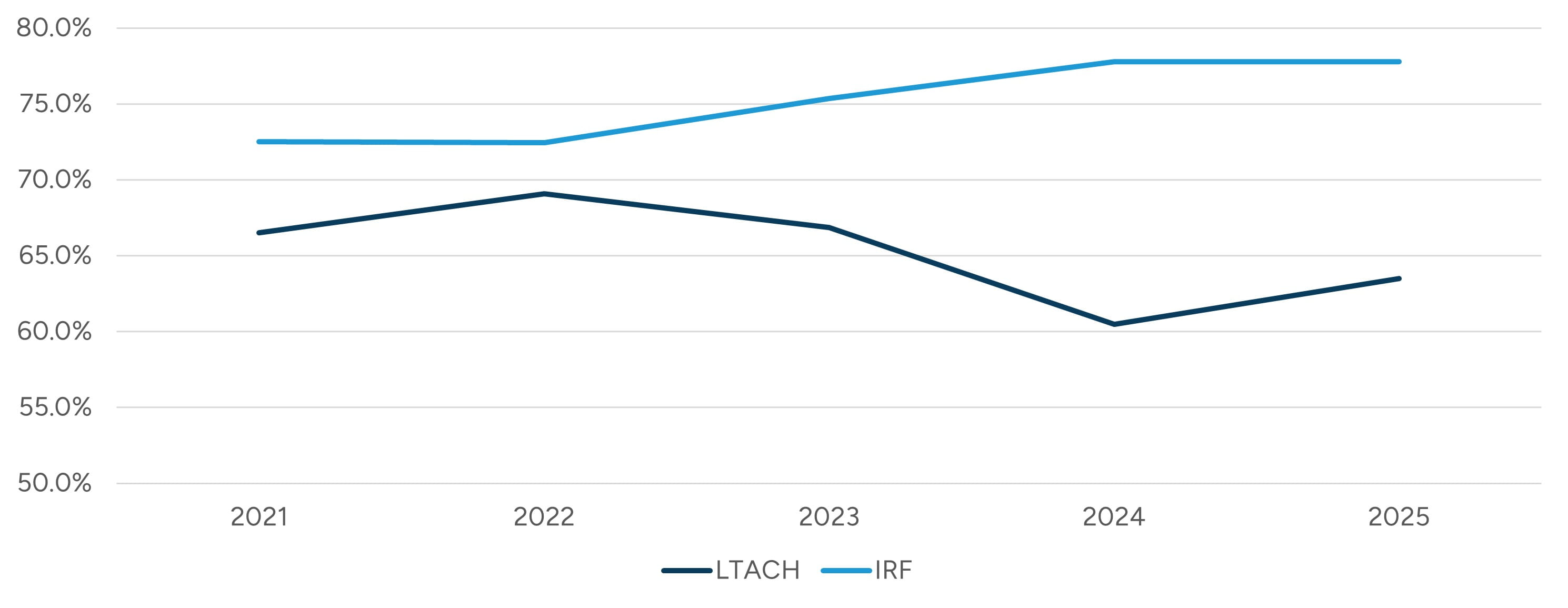

As outlined in Figure 9, IRF occupancy levels have been trending upward in recent years, consistent with commentary from public company operators about the positive outlook for market absorption of new beds in the IRF sector.

The overall industry occupancy ratio in 2024 for IRFs was 74.0%, which is slightly below the median reported figure outlined in Figure 9, while for LTACHs the figure of 61.4% was approximately in line with the reported median.

Figure 9: Median Occupancy Percentage

Other insightful metrics that can be gleaned from the cost report data include revenue per day and per bed, as outlined in Figures 10 and 11.13

Figure 10: 2024 LTACH Revenue Percentile Benchmarks

|

|

n |

25th |

50th (Median) |

75th |

90th |

|---|---|---|---|---|---|

| Revenue per Day | 333 | $1,710 | $2,019 | $2,385 | $2,958 |

| Revenue per Bed | 333 | $297,140 | $448,490 | $609,730 | $760,101 |

Figure 11: 2024 IRF Revenue Percentile Benchmarks

|

|

n |

25th |

50th (Median) |

75th |

90th |

|---|---|---|---|---|---|

| Revenue per Day | 378 | $1,644 | $1,823 | $2,073 | $2,526 |

| Revenue per Bed | 378 | $426,848 | $515,878 | $609,883 | $742,526 |

Transaction Activity

While we note many operators in the IRF and LTACH sector have focused on expansion through de novo facilities and/or through joint ventures (which may be de novo or have existing assets to contribute), there are still transactions of existing facilities among operators taking place. While details of many of these transactions are private in nature, some transactions have had financial deal terms publicly reported. Figure 12 and Figure 13 contain data points from certain transactions over the last decade in these sectors.

Figure 12: Rehabilitation Hospital - Valuation Multiples

|

|

Data Points (n) |

25th Percentile |

Median |

75th Percentile |

|---|---|---|---|---|

| Enterprise Value / Revenue | 12 | 0.8x | 1.3x | 1.6x |

| Enterprise Value / EBITDA | 8 | 7.5x | 8.5x | 9.9x |

Figure 13: LTAC Hospital - Valuation Multiples

|

|

Data Points (n) |

25th Percentile |

Median |

75th Percentile |

|---|---|---|---|---|

| Enterprise Value / Revenue | 9 | 0.2x | 0.4x | 0.5x |

| Enterprise Value / EBITDA | 3 | 6.0x | 7.3x | 7.5x |

Private Companies

In addition to SEM and EHC, there are notable large, private companies that have substantial portfolios of IRFs and LTACHs.

PAM Health

PAM Health (formerly Post Acute Medical) is a privately held, national post-acute operator focused primarily on IRFs and LTACHs. Over the past two years, PAM Health has been actively expanding its footprint in both the IRF and LTACH segments primarily through acquisitions and de novo development. In October 2024, PAM completed a major strategic acquisition of 16 specialty hospitals from Curahealth — including eight LTACHs and eight IRFs across multiple states — significantly enlarging its post-acute care network and entering new markets for both service lines.14 Additionally, PAM acquired standalone facilities such as the Southern Indiana Rehabilitation Hospital in late 2024 and the Ocoee Rehabilitation Hospital in Florida in August 2025, each broadening its IRF presence and enhancing regional coverage.15

Simultaneously, PAM has pursued de novo development of rehabilitation hospitals to meet growing post-acute demand. Plans announced in 2025 include development of three new IRF hospitals in Florida, as well as IRFs in Ohio, Indiana, and Nevada.16

ScionHealth

ScionHealth is a national healthcare system headquartered in Louisville, Kentucky, formed in late 2021 following a corporate restructuring involving LifePoint Health and the former Kindred Healthcare long-term acute care hospital business. Through subsequent growth, ScionHealth’s network has expanded to roughly 94 hospital campuses — approximately 76 specialty (primarily long-term acute care) hospitals alongside 18 community hospital locations — and eight senior living communities serving patients nationwide.17

In January 2023, ScionHealth completed the acquisition of Cornerstone Healthcare Group, adding 15 specialty hospitals (including post-acute care facilities) and approximately 3,000 employees to its network, further broadening its footprint and care delivery capacity.18

Vibra Healthcare

Vibra Healthcare is a privately held specialty hospital operator focused on critical care hospitals, inpatient medical rehabilitation hospitals, and related post-acute services. Founded in 2004, Vibra operates 21 critical care hospitals, inpatient medical rehabilitation hospitals, and hospital-based skilled nursing units across 10 states. The company’s growth strategy has long emphasized partnerships, joint ventures, and market-specific specialty hospital development.19

In recent years, Vibra has continued to expand its rehabilitation footprint through both development and partnership activity. In July 2025, Vibra announced plans to relocate Vibra Hospital of the Central Dakotas to a new freestanding facility in Bismarck, North Dakota, combining 20 LTACH beds with a new 30-bed inpatient medical rehabilitation program. More recently, in January 2026, SEM and Vibra announced a joint venture for Southern Kentucky Rehabilitation Hospital, a 76-bed inpatient rehabilitation hospital in Bowling Green, Kentucky, reflecting Vibra’s continued use of partnerships to reposition and grow rehabilitation assets.20

Madonna Rehabilitation Hospitals21

Madonna Rehabilitation Hospitals is a nonprofit rehabilitation hospital system based in Lincoln, Nebraska, with principal campuses in Lincoln and Omaha. Madonna has expanded its platform in recent years, including the 2022 opening of a new 59-bed patient wing on its Lincoln campus and continued service growth in Omaha. Nationally, Madonna has been recognized as the fourth-largest rehabilitation hospital system in the country by Modern Healthcare and maintains longstanding CARF accreditation across multiple rehabilitation categories.

Ernest Health22

Ernest Health is a privately held network of rehabilitation and long-term acute care hospitals headquartered in Mesquite, Texas, and backed by One Equity Partners. The health system operates 29 medical rehabilitation hospitals and seven long-term acute care hospitals across 13 states, including Arizona, California, Colorado, Idaho, Indiana, Montana, New Mexico, Ohio, South Carolina, Texas, Utah, Wisconsin, and Wyoming. Ernest Health was founded with a mission to bring specialized post-acute care to smaller and rural communities that were otherwise underserved.

The network has expanded significantly in recent years, with seven hospitals opening since 2020. In a recent expansion of services, Northern Idaho Advanced Care Hospital expanded its services in Post Falls, Idaho, by adding a new medical rehabilitation unit in December 2025. Clinically, all eligible Ernest Health rehabilitation hospitals have been ranked in the top 10% nationally by Netsmart Technologies based on outcomes data for the period from October 2023 to September 2024. In 2025, fifteen Ernest Health hospitals were recognized among America’s Best Rehabilitation Centers.

CommuniCare Health Services23

CommuniCare Health Services is a large, family-owned post-acute operator whose platform is broader than the pure-play IRF/LTACH companies, encompassing skilled nursing rehabilitation, long-term care, assisted living, independent rehabilitation facilities, and LTACH operations. The company has grown into one of the nation’s larger post-acute providers, with a footprint spanning multiple Midwestern and Mid-Atlantic states.

A significant recent expansion came through its assumption of operations of Stonerise in West Virginia and Southeast Ohio in 2022. CommuniCare announced that the transaction added 17 healthcare centers, seven home health agencies, and affiliated therapy and hospice services, expanding its footprint to more than 110 healthcare centers across seven states and nearly 14,000 beds. While this expansion is centered more on skilled nursing and broader post-acute services than freestanding IRFs or LTACHs specifically, it materially increases the company’s scale and reinforces its position as an important private post-acute operator.

Mary Free Bed Rehabilitation

Mary Free Bed Rehabilitation is a nonprofit rehabilitation system based in Grand Rapids, Michigan, and consistently ranked among the nation’s leading rehabilitation providers, comprising over 60 locations across Michigan, Indiana, Illinois, Virginia, and West Virginia.24

The organization has pursued active capacity expansion in response to sustained demand, with construction beginning in June 2025 and completing in February 2026 on a newly expanded sixth floor, adding 20 private inpatient rehabilitation rooms, driven by an inpatient census that had regularly exceeded 90% over the prior year.25 Looking further ahead, Mary Free Bed is scheduled to open the Joan Secchia Children’s Rehabilitation Hospital in 2026, a joint venture with Corewell Health Helen DeVos Children’s Hospital that will be Michigan’s first and only freestanding pediatric rehabilitation hospital.26 In August 2025, Mary Free Bed announced an expanded relationship with Beacon Health System under which it began managing Memorial Hospital’s inpatient rehabilitation program in Indiana.27 In addition, Mary Free Bed’s partnership materials indicate ongoing development projects, including a new 50-bed hospital with Valley Health expected in 2026 and another new 50-bed hospital with Vandalia Health expected in 2027, demonstrating a meaningful pipeline of future inpatient rehabilitation growth.28

Shirley Ryan AbilityLab

Shirley Ryan AbilityLab (formerly the Rehabilitation Institute of Chicago) is a Chicago-based, nonprofit physical medicine and rehabilitation system widely regarded as one of the preeminent rehabilitation providers in the country, having been ranked the No. 1 rehabilitation hospital in the U.S. by U.S. News & World Report for 35 consecutive years.29 The system operates a 262-bed flagship translational research hospital in downtown Chicago, together with a network of more than 30 sites of care across the Midwest providing inpatient, day rehabilitation, and outpatient services, primarily across Illinois and Indiana.30

Shirley Ryan AbilityLab has continued to expand its clinical footprint through both partnerships and capital investment. In June 2025, the Illinois Health Facilities and Services Review Board considered a project to renovate approximately 50,500 square feet on the 16th floor of the flagship hospital to expand outpatient and day rehabilitation capacity, with an estimated completion date in late 2026.31 Most notably, in 2023 the Gilbert Family Foundation, Henry Ford Health, and Shirley Ryan AbilityLab announced a partnership to develop a new 72-bed physical medicine and rehabilitation facility in Detroit.32

Lifepoint Rehabilitation

Lifepoint Rehabilitation is a business unit of Brentwood, Tennessee-based Lifepoint Health (backed by Apollo Global Management) and represents one of the most active and expansive IRF development platforms in the country. Its primary model centers on joint venture partnerships with health systems to develop and operate freestanding IRFs, with Lifepoint Rehabilitation typically managing day-to-day operations. As of late 2024, Lifepoint Rehabilitation operated 45 freestanding inpatient rehabilitation facilities and managed more than 250 hospital-based rehabilitation units across the country.33

The business has grown rapidly. In February 2025, Lifepoint celebrated the opening of Peak Rehabilitation Hospital in Apex, North Carolina, a 52-bed facility developed as a joint venture with Duke Health and WakeMed.34 Simultaneously, a number of additional joint ventures are in development, including partnerships with St. Luke’s Health (CommonSpirit) for a new 40-room rehabilitation hospital in the Greater Houston area, announced in December 2025, and Texas Health Resources, which broke ground on a new rehabilitation hospital in Denton, Texas, in November 2025.35 PeaceHealth and Lifepoint also received state regulatory approval in 2025 to construct a 50-bed inpatient rehabilitation hospital in Vancouver, Washington, adding to a concurrent PeaceHealth joint venture already underway in Springfield, Oregon.36

Conclusion

The IRF and LTACH sectors remain essential components of the post-acute care continuum, supported by strong demographic tailwinds, rising patient acuity, and continued reliance from acute care hospitals to manage throughput and outcomes. Operators that demonstrate clinical quality, compliance strength, and labor discipline are positioned to perform well. Public company performance highlights stronger near-term growth and margin stability in IRFs relative to LTACHs, though both serve indispensable roles for complex patient populations.

- “FY 2026 Inpatient Rehabilitation Facilities Prospective Payment System Final Rule — CMS-1829-F,” webpage, Centers for Medicare & Medicaid Services. Accessed on January 30, 2026.

- “Medicare Program; Inpatient Rehabilitation Facility Prospective Payment System for Federal Fiscal Year 2025 and Updates to the IRF Quality Reporting Program,” Department of Health and Human Services, Centers for Medicare & Medicaid Services. Accessed on February 26, 2026.

- “Medicare Program; Inpatient Rehabilitation Facility Prospective Payment System for Federal Fiscal Year 2026 and Updates to the IRF Quality Reporting Program,” Department of Health and Human Services, Centers for Medicare & Medicaid Services. Accessed on February 26, 2026.

- “FY 2026 Hospital Inpatient Prospective Payment System (IPPS) and Long-Term Care Hospital Prospective Payment System (LTCH PPS) Final Rule — CMS-1833-F.” Centers for Medicare & Medicaid Services. Accessed on February 5, 2026.

- Certificate of Need State Laws. National Conference of State Legislatures. Accessed on January 30, 2026.

- Florida Legislature, HB 21 (2019), and as summarized by The Florida Senate 2019 Summary Of Legislation Passed, Committee on Health Policy, CS/HB 21 — Hospital Licensure, accessed February 26, 2026.

- South Carolina Legislature, SB 164 (2023).

- Fiscal Memorandum, SB 2009 — HB 2269, April 9, 2024, Tennessee General Assembly Fiscal Review Committee, last accessed February 26, 2026.

- Population Distribution by Age. Kaiser Family Foundation. Accessed on January 30, 2026.

- Jonathan Vespa, “The U.S. Joins Other Countries With Large Aging Populations,” United States Census Bureau, March 13, 2018. Accessed on January 30, 2026.

- S&P CapitalIQ.

- Based on information available as of March 2026.

- 2024 was relied upon given the lack of reported data points for 2025 from RAND Medicare cost report data.

- “PAM Health Acquires 16 Specialty Hospitals from Curahealth and Nautic Partners, LLC.,” PAM Health, news release, October 21, 2024.

- Accessed from PR Newswire on February 26, 2026.

- Ibid.

- “Why Join ScionHealth,” ScionHealth, webpage, accessed on February 27, 2026.

- “ScionHealth Completes Acquisition of Cornerstone Healthcare Group,” PR Newswire, January 23, 2023.

- “Company History,” Vibra Healthcare, webpage.

- “Vibra Hospital of the Central Dakotas to Relocate and Expand Services in Bismarck,” Vibra Healthcare, news release, July 10, 2025; “Select Medical and Vibra Healthcare Form Joint Venture to Provide Inpatient Rehabilitation Services in Southern Kentucky,” Select Medical, news release, January 6, 2026.

- Obtained from Madonna Rehabilitation Hospital website.

- Obtained from Ernest Health website.

- Obtained from CommuniCare Family of Companies website.

- Obtained from Mary Free Bed Rehabilitation website.

- “Mary Free Bed Expands Access to Inpatient Rehabilitation,” Mary Free Bed Rehabilitation, news release, February 13, 2026.

- “Mary Free Bed Foundation – Giving Guide 2025,” Crain’s Grand Rapids Business, webpage, November 3, 2025.

- “Mary Free Bed Expands Access to Inpatient Rehabilitation,” Mary Free Bed Rehabilitation, news release, February 13, 2026.

- “The Mary Free Bed Advisory Group,” Mary Free Bed Rehabilitation, webpage.

- “Shirley Ryan AbilityLab Ranked No. 1 by U.S. News & World Report for 35th Consecutive Year,” Shirley Ryan AbilityLab, July 29, 2025.

- “Locations,” Shirley Ryan AbilityLab, webpage.

- Illinois Health Facilities and Services Review Board, Project 25-017 (Shirley Ryan AbilityLab), June 24, 2025.

- “Gilbert Family Foundation Contributes Nearly $375 Million in Partnership with Henry Ford Health to Bring Shirley Ryan AbilityLab to Detroit,” Gilbert Family Foundation, Henry Ford Health, and Shirley Ryan AbilityLab, press release, September 6, 2023.

- “Lifepoint Rehabilitation recognizes 27 freestanding inpatient rehabilitation facilities and 18 acute rehabilitation units awarded on Newsweek’s list of America’s Best Physical Rehabilitation Centers 2024,” Lifepoint Health, news release, September 12, 2024.

- “Duke Health, WakeMed and Lifepoint Health Celebrate Opening of New Rehabilitation Hospital,” WakeMed, news release, February 18, 2025.

- “News & Media,” Lifepoint Health, webpage.

- “PeaceHealth, Lifepoint Rehabilitation receive state approval for construction of new Rehabilitation Hospital in Vancouver,” PeaceHealth, webpage.