English

English

Building on our theme of quarterly changes for the industry in the first half of 2020, the third and fourth quarters followed suit. We entered 2020 with strong backlogs, a favorable outlook for new starts across the three primary project types (residential, non-residential building, and non-building), and a robust M&A environment. That came to a near halt for much of the industry (and the economy) in the second quarter. The third quarter showed some improvement, but the industry (and investors) hit the pause button as the elections loomed and the pandemic did not ease as expected. Finally, the fourth quarter showed somewhat of a rebound for several project categories, and the M&A market reopened in earnest in October. The year ended strong for M&A, and the outlook for 2021 has improved for the industry.

As a whole, construction starts fell 10% in 2020 to $766 billion, per Dodge Data. Non-residential building had the largest decline of 24%, led by declines in manufacturing, commercial, and institutional categories. One bright spot was the warehouse and data center segment. Non-building construction starts declined 14%, with the utility/gas plant, environmental, and miscellaneous categories showing notable declines. The highway and bridge category (deemed essential) increased by 8%. The residential market posted an overall increase in starts of 4%, with singlefamily starts increasing a robust 11% for the year.

Looking forward, the industry is expecting the much-discussed infrastructure bill to further boost public spending in the road/ bridge category, for manufacturing spending to rebound as capital plans put on hold in 2020 move forward and for the warehouse/ data center segment to continue its strong run. This optimism is reflected in the Dodge Momentum Index finishing the year on a high note, jumping 9% to 134 in December.

M&A activity finished the year on a very strong note as both strategic and financial buyers were active. Common themes in the engineering and construction services segments include strategics shedding non-core (often project-based) divisions and investing in new, potentially more stable businesses. Financial buyers harvested assets that they had planned on selling earlier in the year, as multiples increased and credit markets reopened. On the buy side, financial firms sought out firms with recurring revenues and client spending tied to maintenance spending as opposed to capital budgets/new facilities.

Key Takeaways

- Industry performance negatively impacted during the second and third quarters

- M&A activity significantly reduced during the same period

- Industry outlook positive due to infrastructure bill and delayed projects starting

- M&A finished the year on a high note and shows no signs of slowing down

- Buyers attracted to recurring revenue/non-project-based revenues

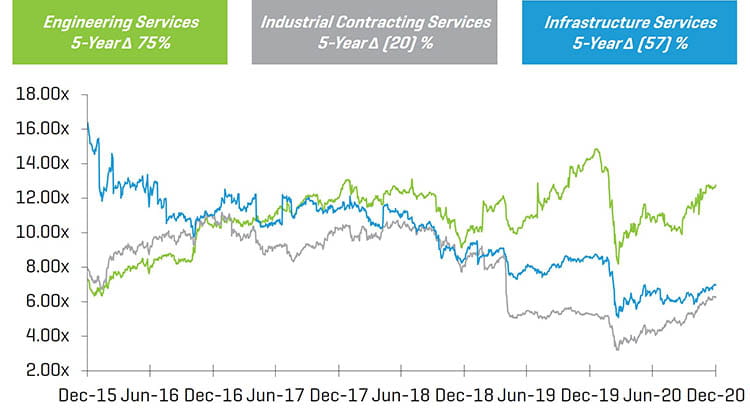

5-Year Historical Enterprise Value / LTM EBITDA Multiples

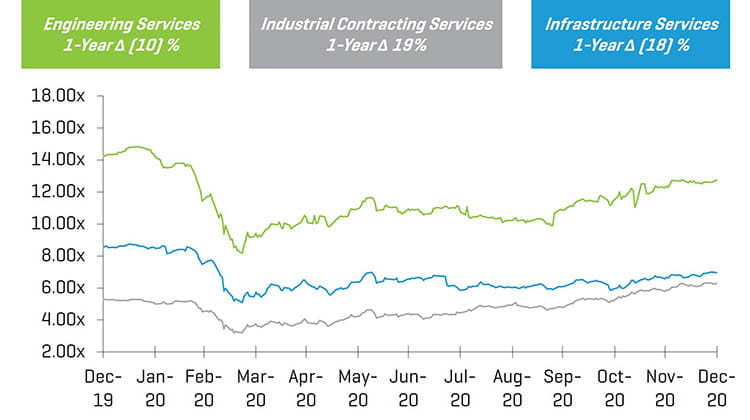

1-Year Historical Enterprise Value / LTM EBITDA Multiples

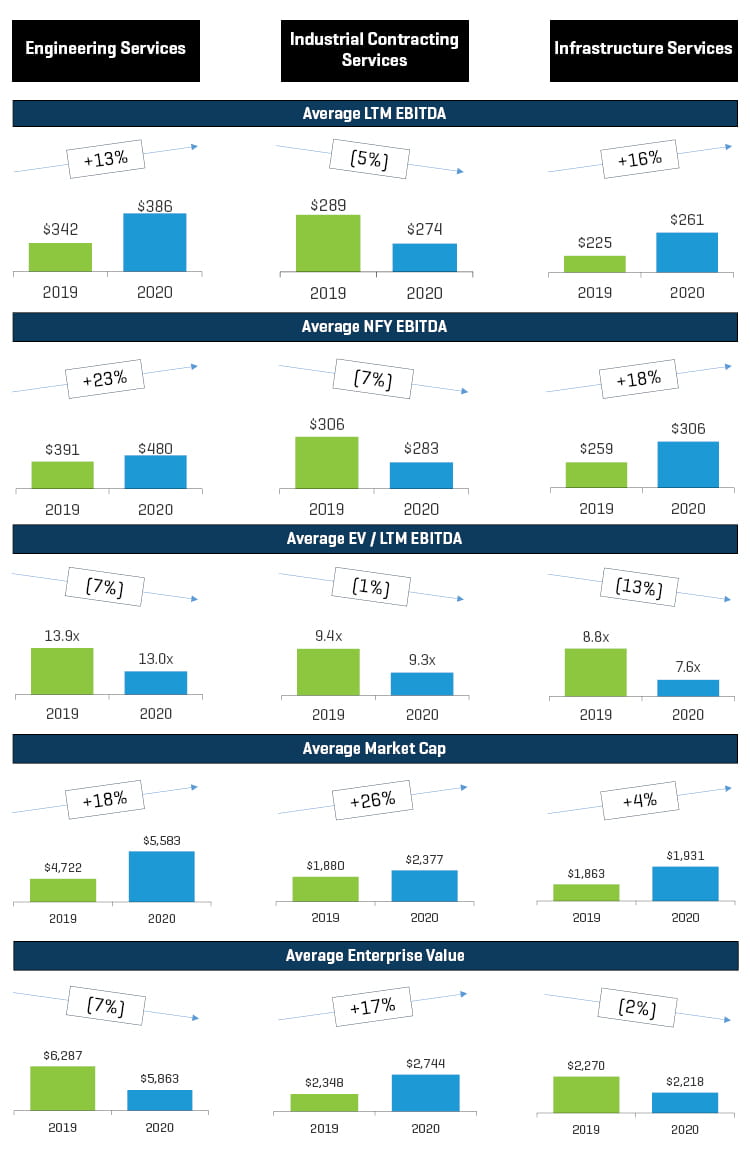

Public E&C Company Year-Over-Year Changes

Average last-12-month (LTM) EBITDA improved year over year for Engineering and Infrastructure Services firms and declined slightly for Industrial Contracting. This is a good sign that firms were able to withstand the pandemic’s effects for now. LTM EBITDA Margin has held steady or improved for two of three categories. Average EV/LTM EBITDA has decreased; however, Average Market Cap has increased for all three categories. This indicates positive sentiment for the sector.

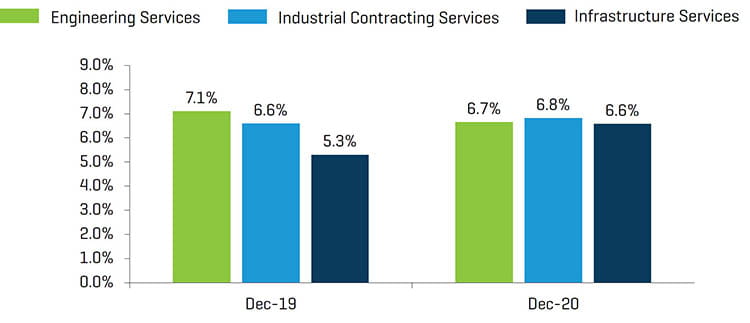

LTM EBITDA Margin

Engineering Services

While the segment saw lower LTM EBITDA margins at year end, average market capitalizations rebounded from March lows.

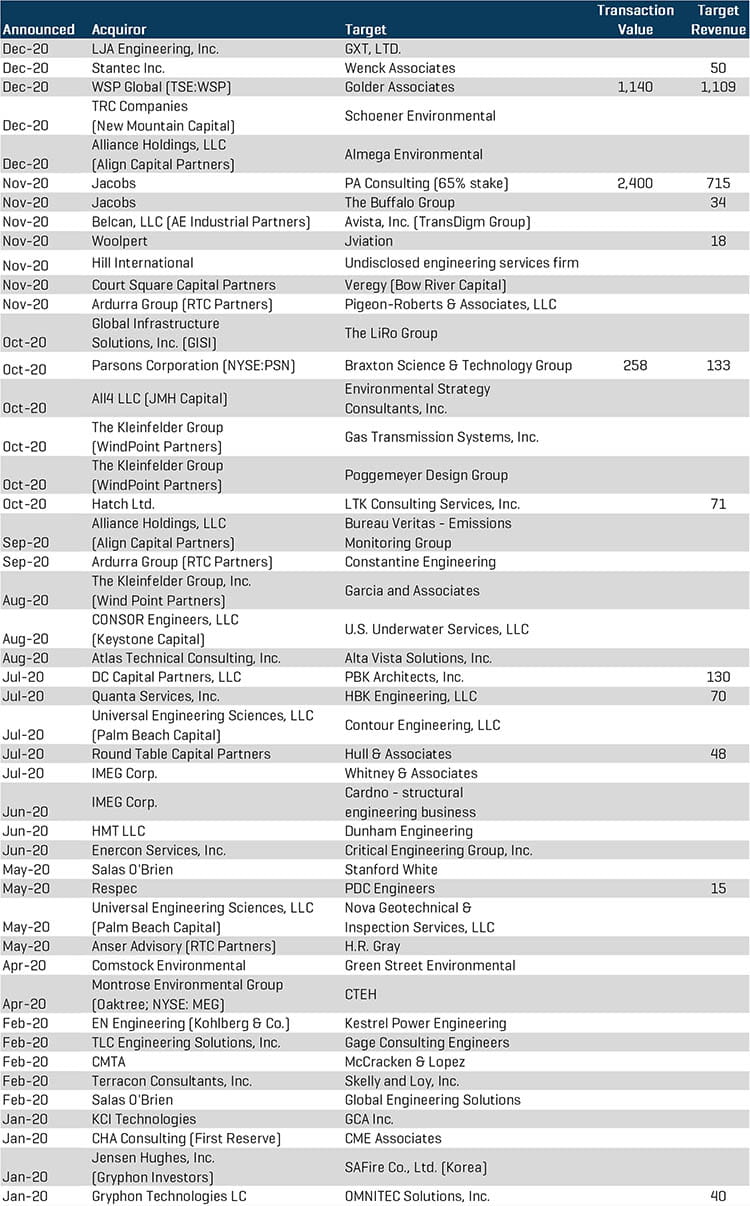

M&A activity was somewhat muted in the first half of 2020, with activity increasing in the final two quarters. Significant transactions include:

- Parsons Corp. (NYSE:PSN) continued its growth in the space, cyber, and intelligence markets with the addition of Braxton Science & Technology Group. BSTG provides mission critical products and advanced engineering services to the U.S. government and agencies.

- Global Infrastructure Solutions, Inc. (GISI) acquired The LiRo Group, a provider of construction/ program management, engineering and inspection services to state and local governments and agencies.

- Jacobs Engineering Group (NYSE:J) acquired a 65% stake in PA Consulting, a leading U.K.-based innovation and transformation consulting firm.

- WSP Global (WSP.TO) acquired Golder Associates, a Toronto, Ontario based consulting and engineering services firm.

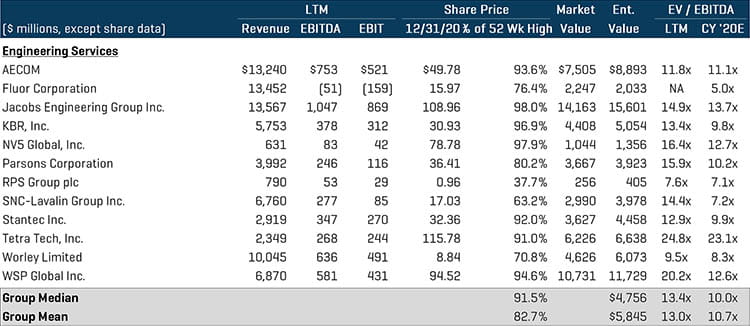

Engineering Services Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions – Engineering Services

Industrial Contracting Services and Infrastructure Services

While the performance for many public firms in the Industrial Contracting and Infrastructure Services segments was negatively impacted during the first half of 2020, most firms finished the year on a positive note with increasing margins and market caps. The last two months of the year saw very strong M&A activity, with both strategics and private equity firms spending aggressively.

Significant transactions include:

- Kohlberg & Co. acquired GPRS Holdings from CIVC Partners. GPRS provides utility locating and concrete scanning services to utilities, contractors, engineering firms, and environmental consultants.

- Day & Zimmermann Group, Inc. acquired Minnotte Contracting Corp. The company is a union mechanical contractor and maintenance company serving industrial customers and power utilities.

- IES Holdings Inc. (NASDAQ: IESC) acquired Plant Power & Control Systems, LLC and Aerial Lighting & Electric, Inc. PPCS is a manufacturer and installer of custom engineered power distribution equipment. Aerial is an electrical contractor specializing in the design and installation of electrical systems for multi-family developments.

- Comfort Systems USA, Inc. (NYSE: FIX) acquired Starr Electric Company, Inc. a provider of electric installations across North Carolina. Comfort also announced the acquisition of BCH Holdings, Inc. a provider of mechanical contracting services.

- Southland Holdings acquired American Bridge Company, greatly expanding Southland’s capabilities and geographic footprint.

- Critical Point Capital acquired AECOM’s power construction division, an example of large strategics divesting non-core assets in order to focus on core, often non project-based capabilities. AECOM also sold its civil construction business to Oroco Capital in December.

- First Reserve Corp. took private The Goldfield Corporation, a provider of construction and maintenance services to electric utility and industrial customers.

- Primoris Services Corp. (NASDAQ:PRIM) acquired Future Infrastructure Holdings, a provider of maintenance, repair, upgrade and installation services to the telecom, gas utility, and infrastructure markets.

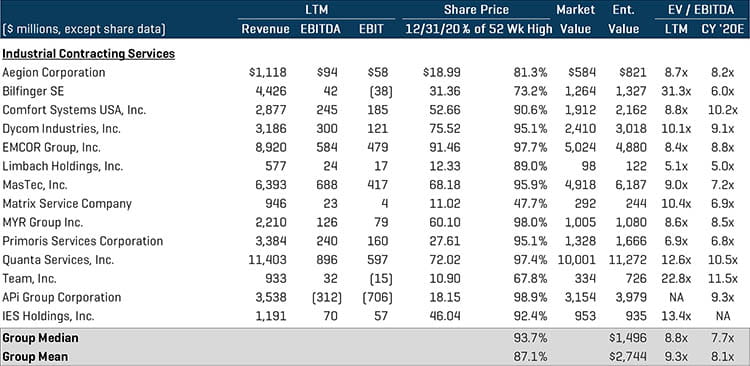

Industrial Contracting Services Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

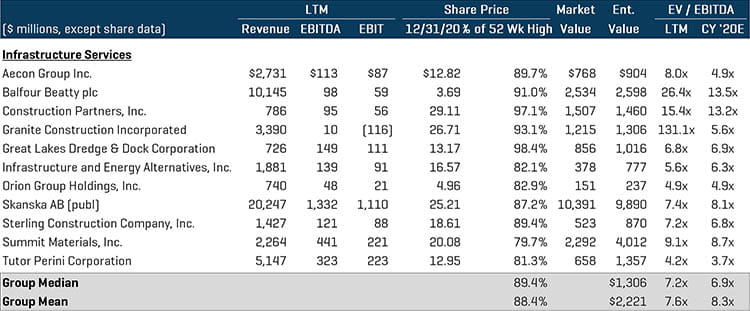

Infrastructure Services Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions – Industrial Contracting and Infrastructure Services

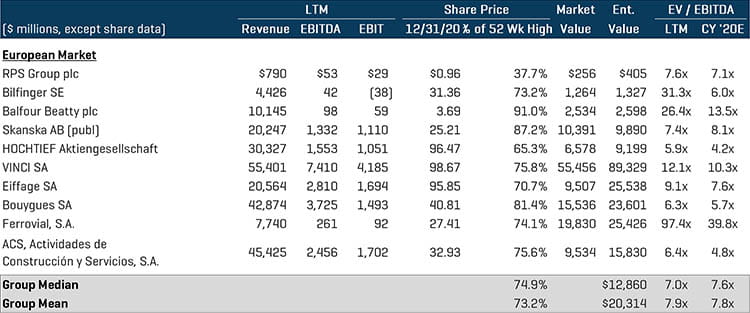

European Market

Significant transactions include:

- Abertis, and Manulife Investment Management, on behalf of John Hancock Life Insurance Company (U.S.A.) acquired Elizabeth River Crossings HoldCo LLC from Skanska AB (OM:SKA B).

- VINCI SA (ENXTPA:DG) acquired ACS Servicios’ industrial services division, including the engineering and works activities, interests held in eight concessions and PPPs relating mainly to energy projects as well as a platform for the development of new projects in the renewable energy sector.

- Eiffage SA (ENXTPA:FGR) agreed to acquire 49.9% stake in Toulouse-Blagnac Airport S.A. from SAS Casil Europe.

European Market Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

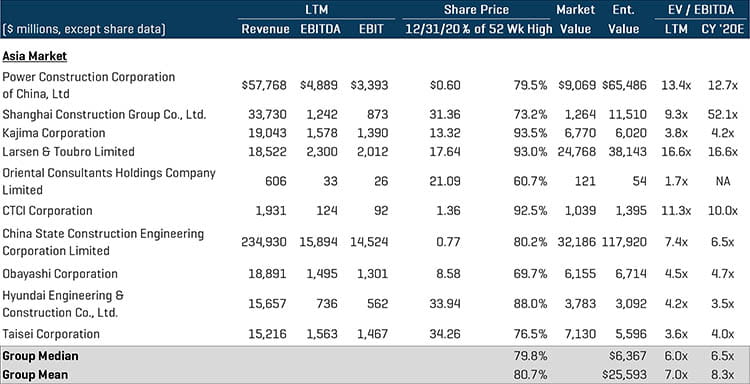

Asian & Indian Market

Significant transactions include:

- Shanghai Construction Group Co., Ltd. agreed to acquire a majority stake in Tianjin Housing Construction Development Group Co., Ltd. from Tianjin Jincheng State-owned Capital Investment and Operations Co., Ltd. for approximately CNY 330 million.

- Langold Real Estate Co., Ltd. (SZSE:002305) agreed to acquire PowerChina Real Estate Group Ltd. from Power Construction Corporation of China, Ltd (SHSE:601669) and Powerchina Construction Group Ltd. for CNY 10.9 billion.

Asian & Indian Market Public Comparables1