English

English

The first half of 2020 portrayed quite a dichotomy. The three major sectors of construction start types – residential, non-residential building and non-building – posted year-over-year gains in January, February, and March. Activity nearly halted for non-essential projects in April and May, then rebounded nicely in June. Year-to-date total construction starts were down 14% compared with the same period in 2019 per Dodge Data. Residential starts dropped 5%, non-residential decreased 22% and non-building starts fell 14%.

M&A activity during the period followed a similar path. As the calendar turned to 2020, backlogs were strong, sellers were preparing for transactions and buyers (both strategic and financial) were open for business. The credit markets were wide open. By April, many M&A processes were put on hold as buyers and sellers agreed to take a pause and focus on their own near-term COVID-19 concerns. Lenders paused to focus on their existing portfolios and the ability to accurately project 2020 results became murky for many potential sellers.

The pause in the market allowed sellers to prioritize efficiencies within their companies, with many seeing decreased overhead due to lower non-job costs and higher utilization rates. Several segments (such as transportation and water) saw projects accelerated, boosting revenues. Advisors were able to work with their clients to be ready to approach the market once the overall mood shifted.

Now, buyers are ready, credit markets are reopening (albeit at potentially higher rates and lower total leverage appetites) and halted projects are beginning to move. It has become a sellers’ market again, with demand for healthy, sustainable businesses that are positioned for growth for the remainder of 2020 and into 2021 outweighing supply of such firms. This should bode well for valuations and activity in the coming quarters.

Key Takeaways

- Industry performance negatively impacted during the second quarter

- M&A activity significantly reduced during the same period

- Pause in activity allowed sellers to focus on their operations, improving efficiencies in the process for many

- Buyers have dry powder and credit markets are open for business

- Valuation multiples returning to historical averages for larger, more stable firms positioned to benefit in key segments over the coming quarters

Industry Statistics

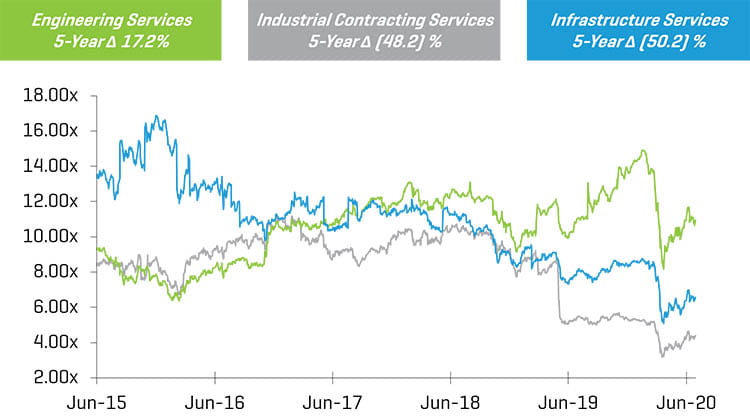

5-Year Historical Enterprise Value / LTM EBITDA Multiples

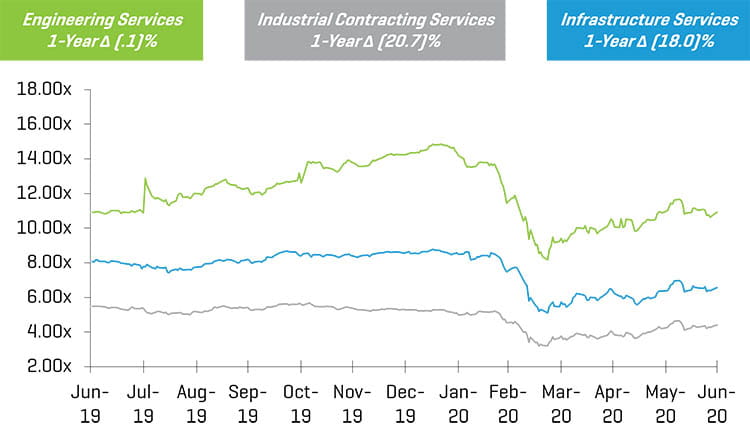

1-Year Historical Enterprise Value / LTM EBITDA Multiples

Public E&C Company Year-Over-Year Changes

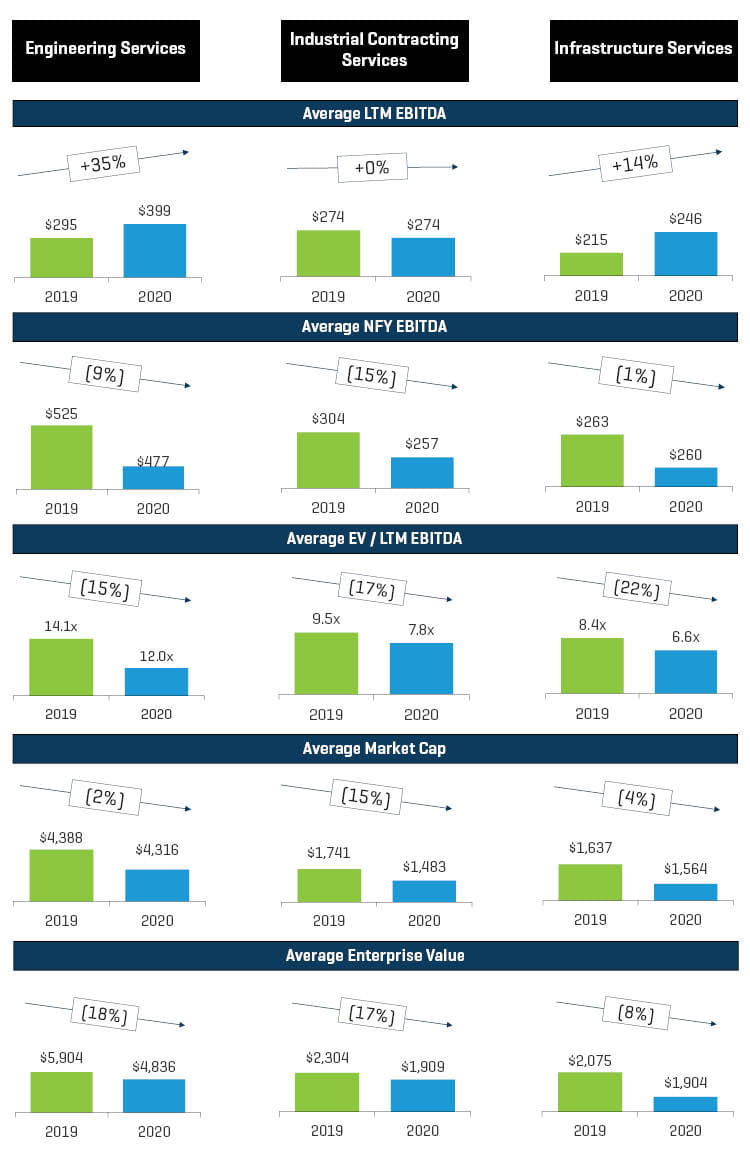

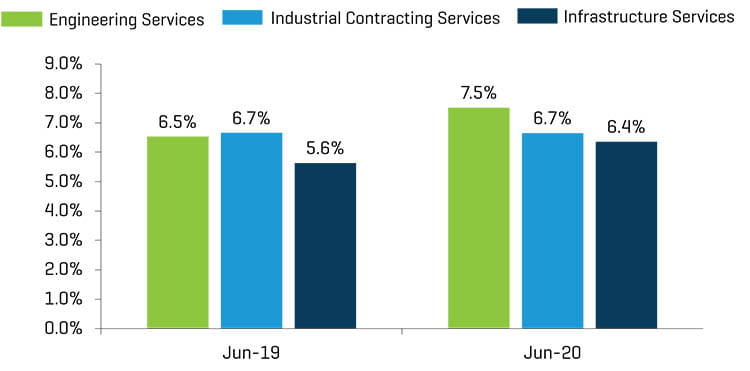

Average last-12-month (LTM) EBITDA has improved year over year for Engineering and Infrastructure Services firms and remained flat for Industrial Contracting. This is a good sign that firms were able to withstand the pandemic’s effects for now. LTM gross margin has held steady or improved for all three categories. Stock market declines and concerns about future revenues have negatively impacted market capitalizations and enterprise values across sectors.

LTM EBITDA Margin

Engineering Services

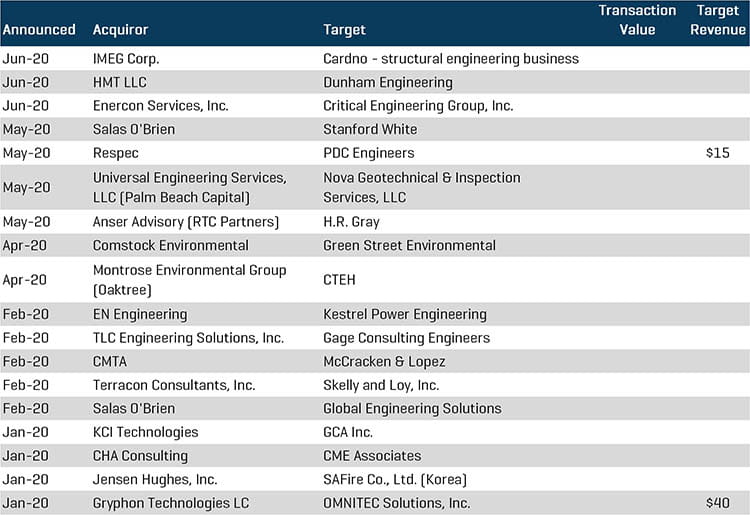

Other than a few specific situations, the segment saw improving LTM EBITDA and gross margins. Average market capitalizations rebounded from March lows. M&A activity was somewhat muted with no major transactions announced. Significant transactions include:

- Salas O’Brien continued its acquisition activity with the additions of Stanford White and Global Engineering Solutions. Stanford White provides engineering services to education, government, healthcare and science/ technology clients. Global Engineering Solutions is an engineering, program management and construction management firm.

- Enercon Services, Inc. acquired Critical Engineering Group, Inc., a provider of program management and engineering services for data centers and mission critical communications centers.

- EN Engineering (Kohlberg & Co.) has entered into a partnership with Kestrel Power Engineering, which provides specialized consulting services to the North American electric power generation market.

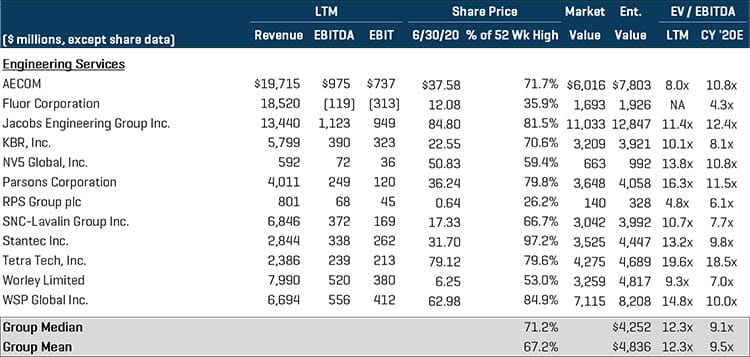

Engineering Services Public Comparables

Select M&A Transactions – Engineering Services

Industrial Contracting Services and Infrastructure Services

While the performance for many public firms in the Industrial Contracting and Infrastructure Services segments was negatively impacted during the first half of 2020, M&A activity continued on its strong pace seen in 2019. Both private equity-backed firms and pure strategic buyers were active in the segments. Significant transactions include:

- Kohlberg & Co. acquired GPRS Holdings from CIVC Partners. GPRS provides utility locating and concrete scanning services to utilities, contractors, engineering firms, and environmental consultants.

- Day & Zimmermann Group, Inc. acquired Minnotte Contracting Corp. The company is a union mechanical contractor and maintenance company serving industrial customers and power utilities.

- IES Holdings Inc. (NASDAQ: IESC) acquired Plant Power & Control Systems, LLC and Aerial Lighting & Electric, Inc. PPCS is a manufacturer and installer of custom engineered power distribution equipment. Aerial is an electrical contractor specializing in the design and installation of electrical systems for multi-family developments.

- Comfort Systems USA, Inc. (NYSE: FIX) acquired Starr Electric Company, Inc. a provider of electric installations across North Carolina. Comfort also announced the acquisition of BCH Holdings, Inc. a provider of mechanical contracting services.

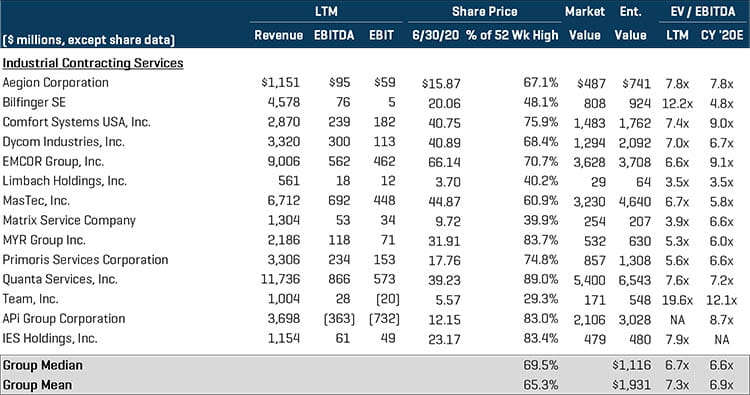

Industrial Contracting Services Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

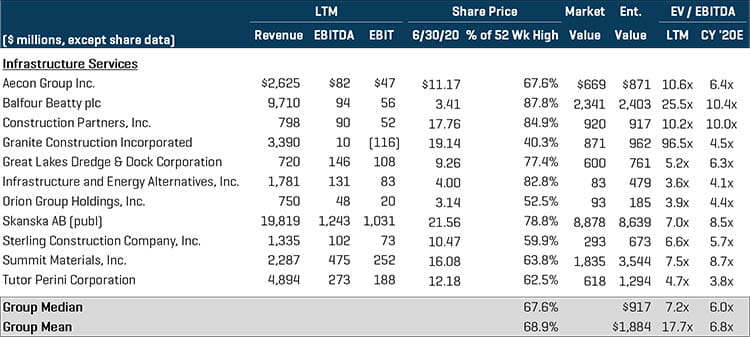

Infrastructure Services Public Comparables1

(1) Multiples above 20x are excluded from the mean/median calculation

Select M&A Transactions – Industrial Contracting and Infrastructure Services

Industry Indexes for this report:

Engineering: ACM, FLR, J, KBR, NVEE, PSN, LSE:RPS, TSX:SNC, TSX:STN, TTEK, ASX:WOR, TSX:WSP

Industrial: AEGN, XTRA:GBF, FIX, DY, EME, LMB, MTZ, MTRX, MYRG, PRIM, PWR, TISI, APG, IESC

Infrastructure: TSX:ARE, LSE:BBY, ROAD, GVA, GLDD, IEA, ORN, OM:SKA B, STRL, SUM, TPC