English

English

Companies pursue merger and acquisition (M&A) transactions for many reasons. These range from seeking economies of scale or diversifying pre-existing business lines to gaining access to new customers or acquiring unique intellectual property. Despite the valid justification acquirers may have, there are numerous studies and articles that cite failure rates of M&A transactions to be well over 50%, which implies that most M&A transactions fail to deliver the anticipated value. Partial acquisitions are one avenue to mitigate the risk of failure in M&A transactions.

Partial acquisitions represent M&A transactions where less than 100% of a target entity is acquired. Partial acquisitions may allow entry to a new geographic market or product line without assuming total control of the business, thus limiting the acquirer’s exposure. Over time, the acquirer may decide to purchase additional interests in the business, which are known as step acquisitions. Step acquisitions are an avenue whereby an acquirer can obtain control of a business in stages over a period of time as opposed to all at once.

Prevalence of Partial and Step Acquisitions

We analyzed domestic M&A transaction activity over the past 10 years to ascertain the prevalence of partial and step acquisitions. Partial acquisitions were defined as any transaction within the initial search criteria whereby less than a 100% interest in the target entity was sought. Step acquisitions were defined as any transaction within the initial search criteria that disclosed one of the following features:

- Majority shareholder increasing ownership stake

- Majority shareholder purchasing remaining shares

- Minority shareholder gaining majority control

- Minority shareholder increasing ownership stake

- Minority shareholder purchasing remaining shares

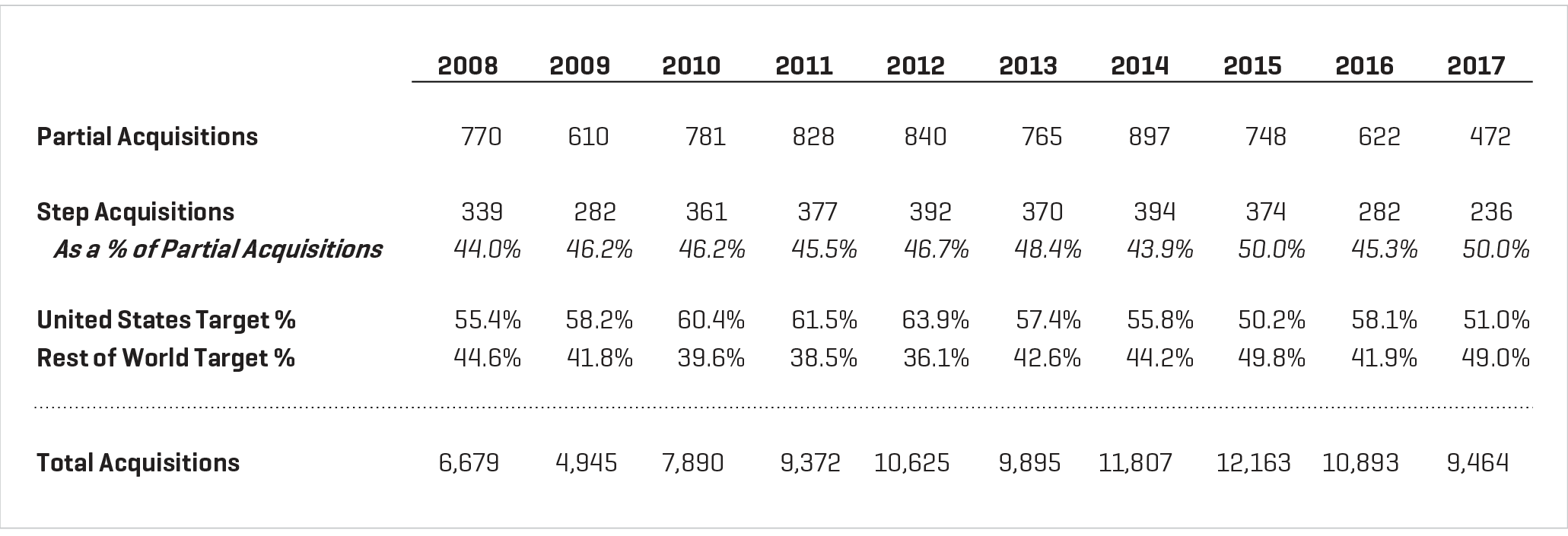

The annual number of step acquisitions has fluctuated over the past 10 years and, in fact, has decreased at a faster rate than the overall decrease in M&A transactions recently. But during this time, the percentage of step acquisitions relative to total partial acquisitions in a given year has remained rather consistent, at around 45% to 50% (Figure 1).

Figure 1. Breakdown of Partial and Step Acquisitions

Source: S&P Capital IQ

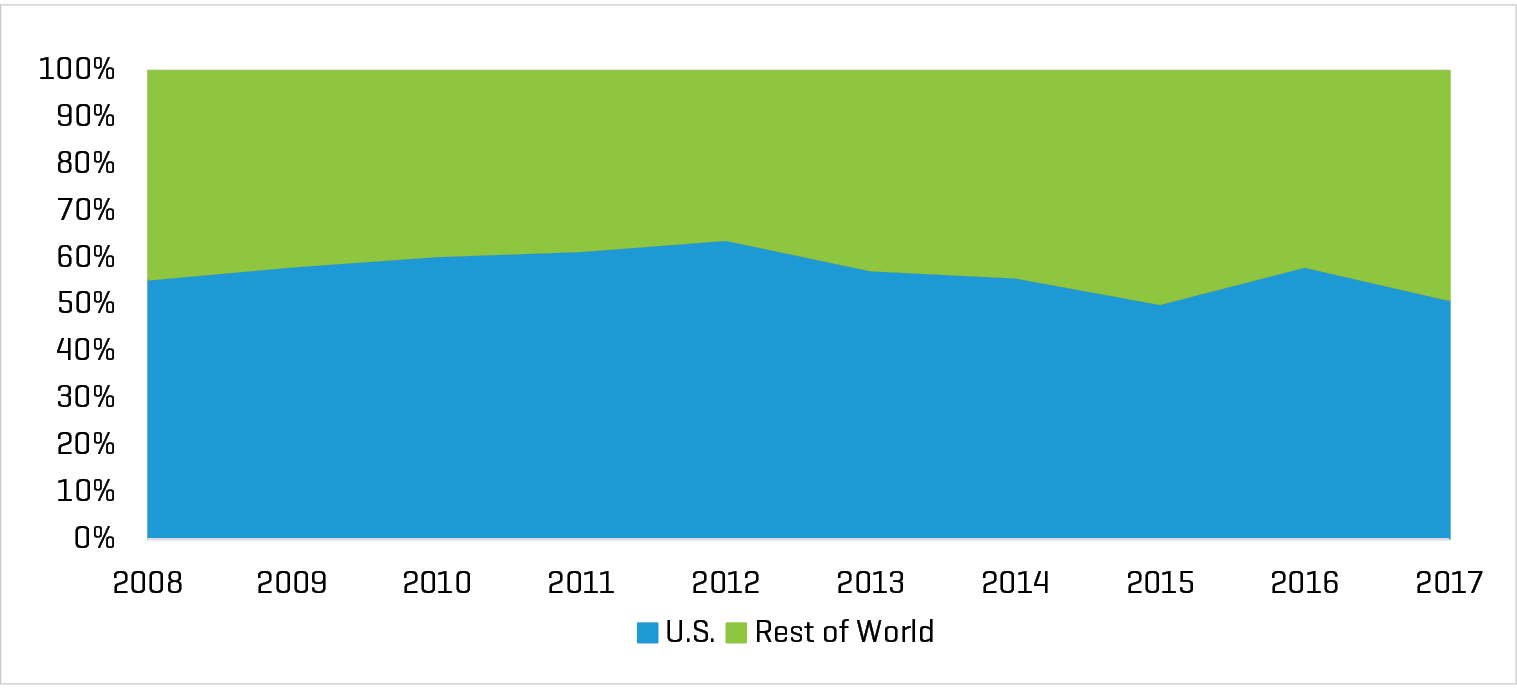

Approximately 40% to 50% of step acquisition target entities were domiciled outside the United States, with an increasing trend toward nondomestic deals during the past decade (Figure 2). This trend supports one benefit of partial acquisitions, as step acquisitions allow an acquirer to gain familiarity with the operations and laws in a particular foreign jurisdiction prior to transitioning to a controlling or wholly owned investment. This can be particularly attractive to U.S.-based companies that have not focused on international markets historically but are looking for new growth opportunities while trying to limit risk by not having to fully commit prior to developing additional experience and expertise. However, there is certainly still risk associated with reliance on other shareholders in the target entity (particularly if the acquirer does not have control of the investment).

Figure 2. Domicile of Step Acquisition Target Entities

Source: S&P Capital IQ

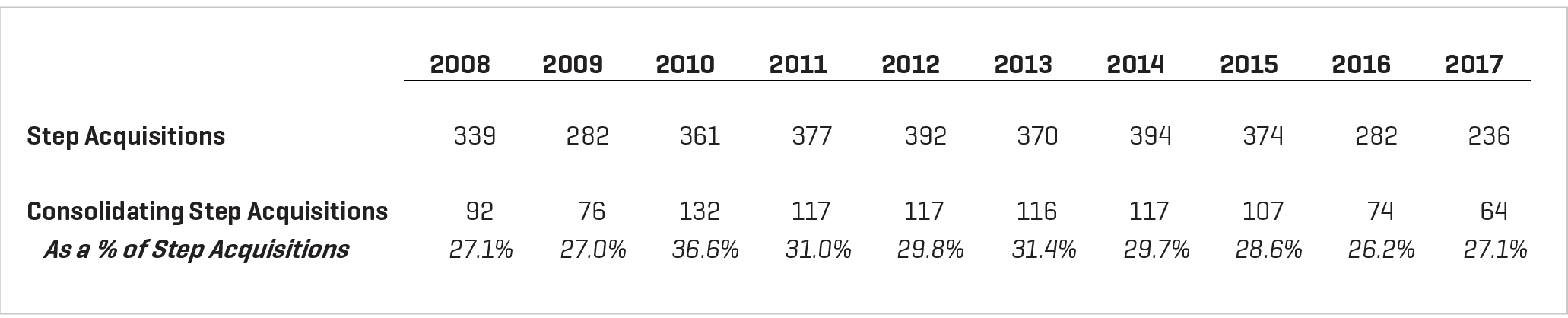

The ownership percentage sought and/or cumulatively owned following a step acquisition dictates the accounting treatment (and potential valuation requirements) associated with the acquired business. As we discuss later, when the acquirer’s post-transaction cumulative ownership percentage exceeds 50%, the acquirer is required to consolidate the entity on its balance sheet via the acquisition method of accounting (assuming the acquired business is defined as a “business”). As detailed in Figure 3, the share of consolidating step acquisitions generally follows the volume of step acquisitions overall.

Figure 3. Step Acquisitions Triggering Consolidation Accounting

Source: S&P Capital IQ

Note: Consolidating Step Acquisitions represent transactions in which a minority shareholder gained majority control and/or purchased the remaining shares.

Although the total number of partial and step acquisitions on an annual basis accounts for only a fraction of total M&A transaction activity by U.S. acquirers, these acquisition types are still prevalent in the market. It is important for acquirers to be aware of the necessary accounting treatments and implications that go along with different cumulative ownership percentages. While every step acquisition does not require a change in accounting treatment, there are certain triggers that result in a change to the accounting treatment and any resulting valuation requirements, particularly when consolidation accounting is triggered.

Accounting Implications

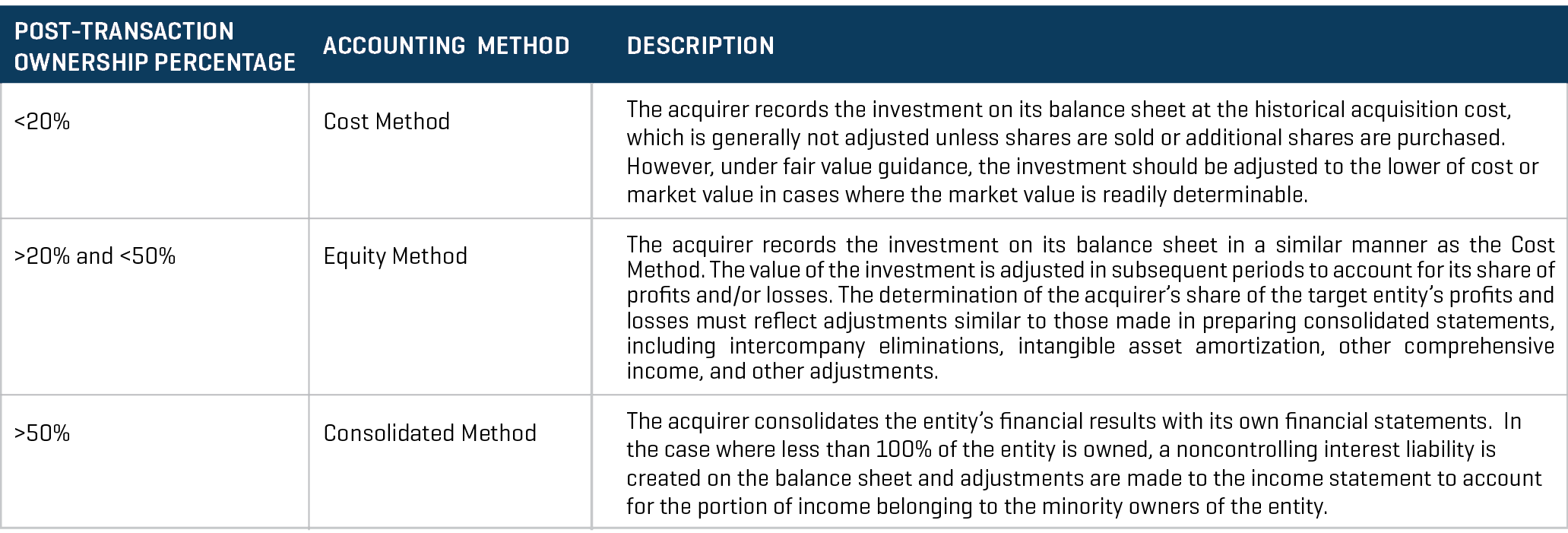

The accounting rules surrounding partial and step acquisitions differ based on the total ownership interest held by the acquirer, as shown in Figure 4.

Figure 4. Step Acquisitions by Accounting Method

Note: While the 20% and 50% thresholds are cited within Financial Accounting Standards Board Accounting Standards Codification, there is language within the guidance suggesting that these percentages are not necessarily fixed percentages, as the true determinant relates to the influence and control maintained by the acquirer. For example, ASC Topic 323-10-15 states that an investment (direct or indirect) of 20% or more of the voting stock of an investee shall lead to a presumption that in the absence of predominant evidence to the contrary, an investor has the ability to exercise significant influence over an investee, and evidence that an investor owning 20% or more of the voting stock of an investee may be unable to exercise significant influence over the investee’s operating and financial policies requires an evaluation of all the facts and circumstances relating to the investment.

For step acquisitions, one must determine if the subsequent investment triggers a change in accounting based on the initial ownership percentage combined with the new investment. At the point of consolidation, the reporting entity must recognize the following under U.S. generally accepted accounting principles (GAAP) at the acquisition date:

- 100% of the identifiable net assets, as measured in accordance with Financial Accounting Standards Board Accounting Standards Codification (ASC) Topic 805

- Noncontrolling interest at fair value

- Goodwill as the excess of a) over b) below:

a) The aggregate of i) the consideration transferred, as measured in accordance with ASC Topic 805, which generally requires acquisition-date fair value; ii) the fair value of any noncontrolling interest in the acquiree; and iii) the acquisition-date fair value of the acquirer’s previously held equity interest (PHEI) in the acquiree.

b) The net of the acquisition-date amounts of the identifiable assets acquired and the liabilities assumed.

A Step Acquisition of a Business When Control Is Obtained for a U.S. GAAP Company

Acquirer Company has a 30% PHEI in Target Company, with a carrying value of $30 million. Acquirer Company purchases an additional 50% interest in Target Company for $500 million in cash. The fair value of Acquirer Company’s PHEI is determined to be $300 million.[1] The fair value of the noncontrolling interest is determined to be $200 million.[2] The net aggregate value of the identifiable assets and liabilities, as measured in accordance with ASC Topic 805, is determined to be $850 million.

The journal entries recorded on the acquisition date for the 50% controlling interest acquired would be as follows ($ in millions), noting that tax consequences on the gain have been ignored for illustrative purposes:

|

Identifiable Net Assets |

$850 |

|---|---|

|

Goodwill (see following table) |

$150 |

|

Cash[3] |

$500 |

|

Equity Investment[4] |

$30 |

|

Gain on PHEI[5] |

$270 |

|

Noncontrolling Interest[6] |

$200 |

|

Fair Value of Consideration Transferred |

$500 |

|---|---|

|

Fair Value of Noncontrolling Interest |

$200 |

|

Fair Value of PHEI |

$300 |

|

Subtotal |

$1,000 |

|

Less: 100% of Identifiable Net Assets |

($850) |

|

Goodwill |

$150 |

- For simplicity, we have presented the fair value of the noncontrolling interest and the PHEI on a pro rata basis with the consideration transferred for the controlling interest. The fair value of each of these interests may require an independent valuation.

- Ibid.

- Cash paid for the 50% interest acquired in Target Company.

- Elimination of the carrying value of the 30% PHEI.

- The gain on the 30% PHEI is recognized within the income statement ($300 million less $30 million).

- Fair value of the 20% noncontrolling interest is recognized in equity.