English

English

In January 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-01 to clarify the definition of a business. This update was issued in response to feedback from stakeholders that the definition of a business was applied too broadly, causing many transactions to be recorded as business combinations that may have been more appropriately classified as asset acquisitions.

By clarifying the definition of a business, FASB intended to add guidance to assist entities with evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses.

Determining What You Bought

Under prior ASC 805 guidance, three elements to an integrated set of activities (a “set”) were required for an entity to be classified as a business: inputs, processes, and outputs. ASC 805-10-55-4 previously defined these as follows:

- Inputs: economic resources that create, or have the ability to create, outputs when one or more processes are applied (i.e., fixed assets, intellectual property, the ability to obtain materials, or employees, among others)

- Processes: systems, standards, protocols, conventions, or rules that, when applied to an input or inputs, have the ability to create outputs (i.e., operational processes or resource management processes)

- Outputs: the results of inputs and processes applied to those inputs that provide or have the ability to provide a return in the form of dividends, lower costs, or other economic benefits directly to investors or other owners, members, or participants

Under the old definition, a set could be classified as a business without all inputs or processes that a seller used to operate the business if market participants could acquire the business and continue to produce outputs (e.g., an acquisition of inputs could be considered a business if it was combined with the acquirer’s processes to produce an output). Prior guidance further complicated the definition of a business by indicating that outputs are not always required to qualify as a business.

Under new ASC 805 guidance, the FASB maintains inputs, processes, and outputs as the main elements of a business. However, it removes considerations that complicated the prior definition and identifies new considerations that have less ambiguity.

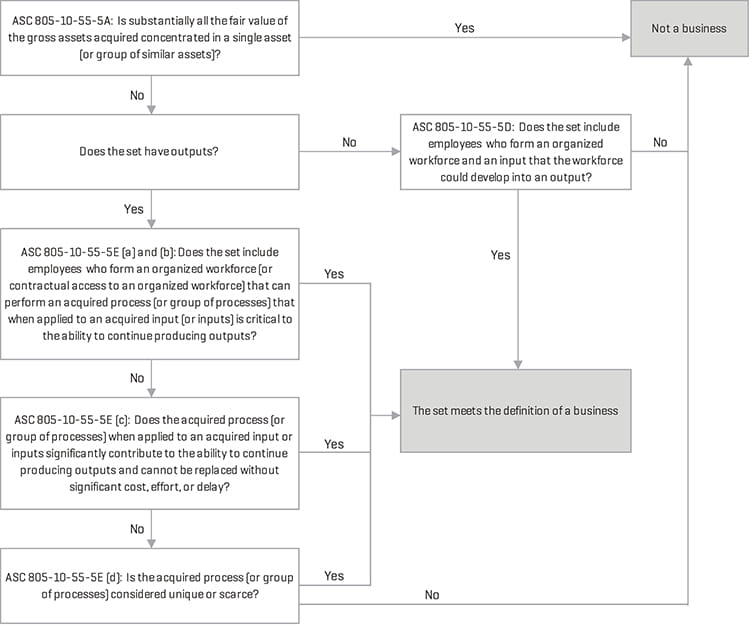

First, the market participant exception was removed. In addition, new guidance indicates that while not all inputs or processes that a seller uses to operate the business are necessary, the set must minimally include an input and a substantive process that together significantly contribute to the ability to create output in order to be classified as a business. Second, the FASB changed the definition of output to be the result of inputs and processes to those inputs that provide goods or services to customers, investment income (such as dividends or interest), or other revenues. Importantly, the new guidance outlines a framework in ASC 801-10-55-5A through 5E to determine when a set is or is not a business (Figure 1).

While the term “substantially all” is not explicitly defined within the new guidance, other U.S. generally accepted accounting principles (GAAP) generally interpret substantially all to be 90%. When applying the framework outlined in Figure 1, ASU 2017-01 clarifies that the following should both be considered single assets in accordance with ASC 805-10-55-5B:

- A tangible asset that is attached to and cannot be physically removed and used separately from another tangible asset (or an intangible asset representing the right to use a tangible asset) without incurring significant cost or significant diminution in utility or fair value to either asset (for example, land and building)

- In-place lease intangibles, including favorable and unfavorable intangible assets or liabilities, and the related leased assets

When assessing a group of similar assets, the following items do not meet the stipulated criteria:

- A tangible asset and an intangible asset

- Identifiable intangible assets in different asset classes (e.g., customer relationships and trademarks)

- A financial asset and nonfinancial asset

- Different major classes of financial assets (e.g., accounts receivable and marketable securities) (ASC 805-10-55-5C)

Furthermore, the new guidance stipulates that a continuation of revenues does not, on its own, indicate that both an input and a substantive process have been acquired. Thus, contractual arrangements, such as customer contracts, customer lists, and leases (when the set is a lessor), should be excluded from the analysis outlined in ASC 805-10-55-5E.

Why It Matters

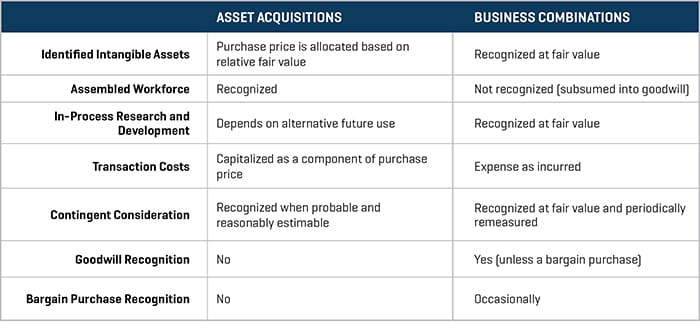

The new definition of a business does not change the acquisition method of accounting for business combinations or the accounting for asset acquisitions outlined in ASC 805-50. However, given the narrower definition of a business outlined in ASU 2017-01, asset acquisitions have become more frequent, particularly in the life science, real estate, and asset management industries. Therefore, we highlight some key differences between the accounting treatment for business combinations and asset acquisitions under U.S. GAAP.

RECOGNITION OF INTANGIBLE ASSETS

For business combinations, ASC 805 states that an intangible asset shall be recognized as an asset apart from goodwill if it falls under the following conditions:

1. It arises from contractual or other legal rights

2. It is “separable” (i.e., the asset is able to be separated or divided from the acquired entity and sold, transferred, licensed, rented, or exchanged, regardless of whether there is an intent to do so)

To the extent that the purchase price plus the fair value of any noncontrolling interest in the acquiree exceeds the net of the fair values of the tangible and intangible assets acquired and liabilities assumed, the excess value shall be recognized as goodwill (ASC 805-30-30-1). Because an assembled workforce is not an identifiable asset in business combinations, it is subsumed into goodwill (ASC 805-20-55-6).

Conversely, there is a much lower threshold for recognizing intangible assets in asset acquisitions. ASC 350-30-25-4 indicates that intangible assets in asset acquisitions may meet asset recognition criteria in FASB Concepts Statement No. 5, Recognition and Measurement in Financial Statements of Business Enterprises (CON 5), without meeting the contractual-legal criterion or the separability criterion. Given the less stringent recognition criteria, an assembled workforce may be recognized as an intangible asset in asset acquisitions. Goodwill, however, is not recognized. Instead, the cost of the group of assets (i.e., the purchase price) should be allocated to the individual assets acquired or liabilities assumed based on relative fair value (ASC 805-50-30-3).

IN-PROCESS RESEARCH AND DEVELOPMENT

In a business combination, in-process research and development (IPR&D) assets are recognized and measured at fair value regardless of whether they have an alternative future use, and are assigned an indefinite useful life until completion or abandonment of the associated R&D efforts.

In asset acquisitions, tangible and intangible assets that are used in R&D activities are recorded as an asset or assets if they have alternative future uses (ASC 730-10-25-2(c)). Otherwise, they are expensed. Emerging Issues Task Force (EITF) Issue No. 09-2 was intended to address inconsistencies between the accounting for IPR&D in business combinations (in which it is always recorded as an asset regardless of alternative future use) and asset acquisitions (in which the presence of an alternative future use is required to record an asset). An ASU Exposure Draft issued by the FASB in 2009 proposed similar treatment for IPR&D in a business combination and asset acquisition. However, the ASU was never finalized, and the FASB ultimately removed the topic from its EITF agenda. The American Institute for Certified Public Accountants (AICPA) Accounting & Valuation Guide, Assets Acquired to Be Used in Research and Development Activities, provides best practices in accounting for IPR&D acquired in an asset acquisition.

MEASURING THE COST OF AN ACQUISITION

Transaction cost recognition differs between asset acquisitions and business combinations. Per ASC 805-50-30-1, transaction costs should generally be capitalized as a component of the purchase price for asset acquisitions. The costs should then be recognized as they become payable. For business combinations, ASC 805-10-25-23 indicates that transaction costs should not be recorded as a component of the purchase price and should instead be expensed as incurred. Because transaction costs are capitalized in asset acquisitions (rather than expensed), near-term net income will be higher but long-term net income will be lower as depreciation and amortization are higher due to a higher asset base.

There are also notable differences regarding contingent consideration measurement. In asset acquisitions, contingent consideration is recognized when probable and reasonably estimable, as discussed in ASC 450-20-25-2. When resolved, the amount by which the fair value of the contingent consideration issued or issuable is in excess (or shortfall) of the amount that was recognized as a liability shall increase (or decrease) the cost of the investment, as discussed in ASC 323-10-35-14A. In business combinations, ASC 805-30-25-5 indicates that acquirers shall recognize the fair value as of the acquisition date as part of the consideration transferred. Changes in the fair value for contingent liabilities will be recognized in earnings until the contingency is settled.

BARGAIN PURCHASE

In the event that the fair values of the tangible and intangible assets acquired and liabilities assumed exceed the total purchase price of the transaction in a business combination, the resulting gain shall be recognized in earnings on the acquisition date, as discussed in ASC 805-30-25-2. For asset acquisitions where this situation holds true, the purchase price should be allocated to the individual assets acquired or liabilities assumed based on relative fair value.

MEASUREMENT PERIOD

One final area of note relates to the measurement period for business combinations and asset acquisitions. In a business combination, the acquirer has up to one year to make provisional adjustments to the amounts recognized at the acquisition date to reflect new information obtained about material facts and circumstances that existed as of the acquisition date. However, guidance for asset acquisitions does not recognize the concept of a measurement period. Thus, assets are to be recorded at fair value on the acquisition date, and any subsequent adjustments are considered accounting errors. Although this difference is based on the theory that the accounting in an asset acquisition is inherently less complex than the accounting in a business combination, as detailed in this article and summarized in Figure 2, both accounting treatments have unique requirements that will require in-depth analysis.