English

English

Background

A major midstream energy company suspected the insured value of its gas processing plant was too high, and they were paying for more coverage than necessary. The company needed an accurate estimate of replacement value for its state-of-the-art facility, and they engaged Stout to help.

During construction, one of our client’s cryogenic natural gas processing plants (the “West Texas Plant”) encountered significant delays that drove up the cost of the plant to over $140 million -– significantly higher than other recently built plants of a similar size. For the past several insurance renewals, the company reported the replacement value of its property using the original construction cost basis recorded on its fixed asset listing.

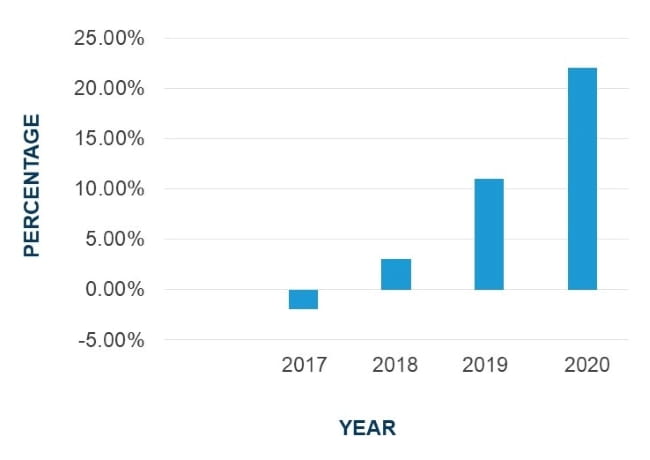

At first, this approach proved convenient for its simplicity. Insurance prices were low enough that over-insuring the property wasn’t a major financial or operational concern. However, a hardening property insurance market meant the price of the company’s excess coverage was getting more expensive (Figure 1). Adding further urgency to the situation was the fact that this trend showed no signs of letting up.

Our client was told by their insurance broker to expect premium increases of 40%-50% during their upcoming renewal.

In normal circumstances, relying on a fixed asset listing to develop replacement values for insurance can be a convenient and reasonable approach. But this situation required a different approach.

Our client realized they would need to leverage the expertise of valuation specialists to produce an independent opinion of value that would satisfy insurers during the upcoming renewal.

Figure 1: Annual US Property Insurance Pricing Change

Source: Global Insurance Market Index Q3 2020, Marsh & McLennan Companies, November 2020

Our Process

We began our analysis by gaining an in-depth understanding of our client’s facility and operations. We discussed the history of the facility and the technical aspects of the operations with plant management, as shown below:

Information Gathered and Reviewed:

- Process flow diagrams

- Capacity, technology, and age of major processes and assets

- Aerial maps and plant layout drawings

- Building and structure data

- Fixed asset listings

- Discussions with plant management

After considering the facts and circumstances at hand, we decided to employ two different valuation techniques: a detailed cost buildup method and a facility benchmarking analysis. Our plan was to develop a value estimate using each method, compare the results, and ultimately conclude a replacement value for our client’s plant.

The Cost Buildup Method

Using this method we segmented the plant into its various components. We then estimated the replacement cost of each component based on capacity, construction, and process technology (Figure 2).

Figure 2: Cost Buildup Method Example

Types of Data Used:

- Construction cost manuals

- Chemical engineering reference books

- Gas processing industry publications

- Data from the West Texas Plant

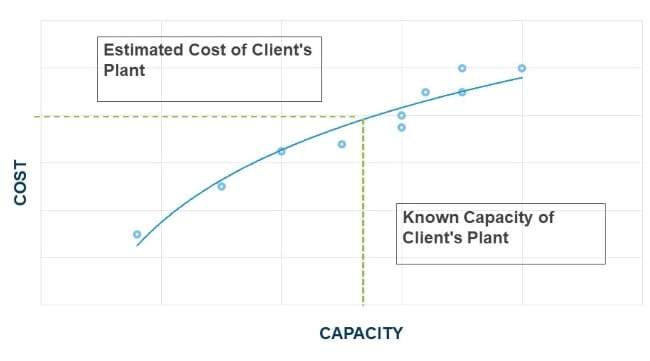

The Facility Benchmarking Analysis

This approach involved estimating the cost of the West Texas Plant based on the actual construction costs of similar gas processing plants (Figure 3). We identified a number of plants similar in age, technology, and location. We then utilized a regression model as shown below to investigate the relationship between the construction cost and capacity of the similar plants. Using this model, we were able to estimate the replacement value of the West Texas Plant based on its known capacity.

Figure 3: Facility Benchmarking Regression Model - Cost and Capacity of Similar Plants

Types of Data Used:

- Publicly available plant cost data

- Confidential third-party plant construction cost data

- Location adjustment factors

- Stout’s internal database of plant costs

Comparing the Estimates

We compared our estimates from each method and found they were reasonably consistent – within about 10% of each other. As suspected, these estimates were significantly less than the original cost recorded on our client’s fixed asset listing.

Confirming With Industry Experts

When valuing a complex property, it is often useful to solicit input from industry experts. Their feedback can provide a real-world perspective that helps improve the quality of a valuation. In this case we reached out to a major engineering and construction firm that specializes in designing and building gas processing plants. We discussed our valuation process with the company’s construction manager who ultimately confirmed that our approach and conclusions were reasonable based on his experience.

Result

After analyzing the relevant facts and compiling our value estimates, our concluded replacement value for the West Texas Plant was around 40% lower than the plant’s original construction cost. Our client then used our valuation opinion to successfully acquire insurance for an amount much more reflective of actual replacement value of their facility. Although the new valuation represented a significant change from prior years, the insurers found our approach and resulting replacement value to be sufficiently supportable and reasonable.

Key Takeaways

Inaccuracies in reported insurable values can be caused by a number of factors as shown in the list below. It is also important to realize that “inaccuracy” refers to both over and undervaluation of property. Both can limit a risk manager’s ability to appropriately understand their property exposures.

Common sources of valuation inaccuracy

- Using a trending approach over long time periods

- Non-historical cost and date information within an asset listing (accounting adjustments, impairments, bankruptcy, used asset purchases, internal transfers, etc.)

- Using price indexes/cost trend data that don’t reflect the underlying assets

- Anomalous events during construction

- Double counting asset repairs, upgrades, and component replacements

- Not considering functional obsolescence and changes in technology

- Including idle, disposed, or out-of-service assets within a valuation

- Attributing value to assets that are excluded from property insurance coverage, and vice versa

Working around these sources of valuation inaccuracy is almost always possible but will usually require techniques that are a step beyond the cursory asset listing-based trending approach. Employing a full range of valuation techniques can pay off when dealing with large exposures or complex circumstances, and when insurance markets require well-developed and supported asset valuations. In any case, quantifying property exposures diligently and thoroughly will lead to better management of risks.