English

English

Hospital acquisition activity has remained strong for the past several years. While mega-deals dominate the headlines, like RCCH HealthCare Partners’ $5.6 billion acquisition of LifePoint Health, Inc. and the merger between nonprofit behemoths Dignity Health and Catholic Health Initiatives (139 combined hospitals), the majority of transactions involve the acquisition of regional health systems or community hospitals. According to Irving Levine Associates, approximately 71% of hospital transactions in 2017 involved the acquisition of a single facility.[1]

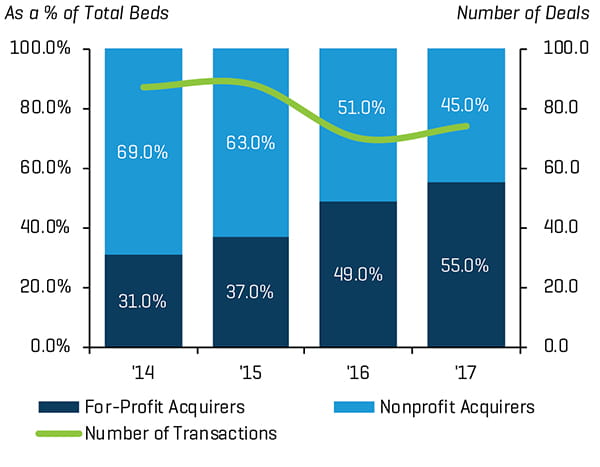

Both nonprofit and for-profit health systems have been active in deal markets; however, for-profits represent an increasing portion of all hospital buyers. For-profit buyers accounted for 55% of the beds acquired in 2017 – up from 31% in 2014 (Figure 1).

Figure 1: Total Beds Acquired

Nonprofit community hospitals have struggled to remain independent. Increased competition, declining reimbursement, rising costs, and limited access to capital present significant challenges for these providers. Partnering with a larger health system through a joint venture, sale, or other arrangement may be necessary for community hospitals to remain viable and continue serving their communities. Nonprofit hospitals will frequently explore sales to for-profit hospital buyers as these potential partners have the scale and leverage necessary to negotiate more favorable payer and vendor contracts and can more readily access equity and debt markets.

Because hospitals are perceived as charitable assets of the community, stakeholders rigorously scrutinize nonprofit conversions. The state attorney general (AG) review plays a significant role in these transactions by serving to both protect the interests of the local community and ensure that the nonprofit’s assets are not sold for less than their fair market value. AGs will commonly engage a qualified professional to perform a fairness opinion or valuation of the target hospital as part of their review.

Overview of Nonprofit Conversion Transactions

Nonprofit hospital conversions can take many forms (e.g., joint ventures, lease arrangements, etc.) but are commonly structured as asset sales. The buyer will purchase the hospital’s operating assets (i.e., net working capital and tangible/intangible assets). Assets that relate to the nonprofit status of the hospital such as donor-restricted funds, assets held by trustees, assets set aside by the board for future needs, and cash and investments are excluded from the transaction. Transaction consideration and excluded assets are contributed to a newly formed foundation or similar charitable organization. Foundations will often use these funds to promote community health and wellness initiatives – particularly those designed to provide care for the indigent.

Stakeholders view nonfinancial deal terms as equally important as cash considerations. Hospital boards negotiate protections into the purchase agreement that are designed to preserve the availability and accessibility of healthcare services provided to the community. Most transactions include provisions requiring the buyer to continue to provide specified core medical services for a defined period (e.g., five to 10 years). Similarly, agreements typically prohibit the buyer from closing material facilities within a designated time. Buyers will often commit to maintaining a charity care policy consistent with that of the seller or buyer’s policies at other owned hospitals. Additionally, capital commitments requiring the buyer to invest a specified dollar amount into capital improvements are commonplace. Frequently, purchase agreements provide for the formation of advisory committees, composed of both buyer and seller representatives, to oversee and enforce the implementation of these commitments. AGs will often engage a monitor to further ensure commitments are met.

Role of the State Attorney General

Many states require that the AG receive advance notice of the transaction (typically 60 to 90 days), though it is common practice to notify the AG early in the process and keep an open line of communication to avoid surprises. Typically, AGs require the nonprofit seller to submit an application addressing the critical aspects of the transaction, including the motivations for pursuing a sale, process for selecting a buyer/partner, valuation, and any material nonfinancial commitments agreed to by the buyer.[2]

State AGs will review all aspects of a nonprofit conversion transaction, including whether the sale benefits the public interest, whether the board acted in an independent manner, and whether fair market value was received for the charitable assets. AGs are usually granted their oversight authority under a combination of state nonprofit corporation law, the common law doctrine of cy-près, or through state legislation.[3] While the focus of the AG’s review will vary based on the specifics of each transaction, Community Catalyst, Inc. (CCI) has developed a legislative framework (“A Conversion Model Act”) for the review of a conversion transaction.

Highlights from the CCI model act are summarized in Figure 2.[4]

Figure 2: Features of the Model Act

|

The AG should receive written notice, including a conversion application, from the nonprofit before it enters into a conversion. Within 90 days from the receipt of notice and application, the AG should notify the nonprofit of its decision; however, this period may be extended by the AG for an additional 60 days. |

|---|

|

The AG shall provide access to all records filed with it concerning the proposed conversion to the public at no cost. Additionally, the AG shall hold at least one initial public hearing in the service area of the nonprofit which provides an opportunity for public testimony no later than 45 days after receiving notice. The AG shall provide access to all records filed with it concerning the proposed conversion to the public at no cost. Additionally, the AG shall hold at least one initial public hearing in the service area of the nonprofit which provides an opportunity for public testimony no later than 45 days after receiving notice. |

|

The AG must find that the terms of the conversion are fair and reasonable to the residents of the state, the public, recipients of the nonprofit's services, and other stakeholders and that the conversion is in the public interest. The AG must find that the terms of the conversion are fair and reasonable to the residents of the state, the public, recipients of the nonprofit's services, and other stakeholders and that the conversion is in the public interest. |

|

The AG must find that the conversion will not result in direct or indirect inurement to any private person or entity and that the conversion will not result in any immediate or future remuneration to an official director or trustee of the nonprofit, except in the form of compensation paid for continued employment with the acquiring entity. The AG must find that the conversion will not result in direct or indirect inurement to any private person or entity and that the conversion will not result in any immediate or future remuneration to an official director or trustee of the nonprofit, except in the form of compensation paid for continued employment with the acquiring entity. |

|

The AG must find that the conversion does not create or have the likelihood of creating an adverse effect on the quality, availability, and affordability of health services to the affected community. Further, the conversion must not result in the decrease or elimination of essential services and health care coverage for the community. The AG must find that the conversion does not create or have the likelihood of creating an adverse effect on the quality, availability, and affordability of health services to the affected community. Further, the conversion must not result in the decrease or elimination of essential services and health care coverage for the community. |

|

The AG must find that the nonprofit used due diligence in selecting the acquirer or in deciding to convert to a for-profit corporation and negotiating the terms and conditions of the conversion or similarly disposing of its assets. Additionally, the AG must find that the nonprofit formulated and issued appropriate requests for proposals in pursuing a conversion. The AG must find that the nonprofit used due diligence in selecting the acquirer or in deciding to convert to a for-profit corporation and negotiating the terms and conditions of the conversion or similarly disposing of its assets. Additionally, the AG must find that the nonprofit formulated and issued appropriate requests for proposals in pursuing a conversion. |

|

All conflicts of interest should be disclosed, including conflicts of interest relating to board members, executives, and experts retained by the transaction parties. All conflicts of interest should be disclosed, including conflicts of interest relating to board members, executives, and experts retained by the transaction parties. |

|

A charitable trust shall be set aside equal to the fair market value of the corporation. The AG shall require that the nonprofit receives full fair market value for its assets. The nonprofit shall be required to conduct an independent valuation of its assets. The AG shall utilize an independent expert to conduct a separate independent valuation unless the AG determines there is a significant reason not to conduct an independent review, then the AG's expert shall review the valuation conducted by the transacting parties. A charitable trust shall be set aside equal to the fair market value of the corporation. The AG shall require that the nonprofit receives full fair market value for its assets. The nonprofit shall be required to conduct an independent valuation of its assets. The AG shall utilize an independent expert to conduct a separate independent valuation unless the AG determines there is a significant reason not to conduct an independent review, then the AG's expert shall review the valuation conducted by the transacting parties. |

|

The AG shall contract with experts to assist in reviewing the proposed conversion. Expert consultant reports should be made available to the public and the AG shall charge the parties submitting the proposed conversion for the cost of the consultants. The AG shall contract with experts to assist in reviewing the proposed conversion. Expert consultant reports should be made available to the public and the AG shall charge the parties submitting the proposed conversion for the cost of the consultants. |

|

Following the approval of the conversion, if necessary, the for-profit shall fund an independent health care access monitor to study and report on community health access by the converted entity, including access to care for indigent persons. If the AG receives information that the acquirer is not fulfilling its commitments, the AG shall hold a public hearing. If the AG determines that the information is true, it shall implement a corrective action plan for the acquirer. Following the approval of the conversion, if necessary, the for-profit shall fund an independent health care access monitor to study and report on community health access by the converted entity, including access to care for indigent persons. If the AG receives information that the acquirer is not fulfilling its commitments, the AG shall hold a public hearing. If the AG determines that the information is true, it shall implement a corrective action plan for the acquirer. |

Source: A Conversion Model Act, prepared by Community Catalyst, Inc., October 2003.

In 1997, the National Association of Attorneys General (NAAG) adopted similar guidelines for the conversion process, as shown in Figure 3.[5]

Figure 3: Features of the NAAG Resolution

|

State attorney general should receive advance written notice of conversions. |

|---|

|

The public should receive advance notice, including the names and addresses of the parties and the terms of the proposed conversion. |

|

A valuation of the charitable assets should be prepared by an independent expert. |

|

Directors and others involved in the transaction should not receive excessive compensation. |

|

The use of proceeds should be consistent with the charitable purpose for which the assets are held by the nonprofit health care entity and not benefit the for-profit purchaser. |

|

The attorney general should be able to recover the costs of reviewing and evaluating the proposed transaction from the parties involved. |

Source: GAO/HEHS-98-24 Not-for-Profit Hospital Conversions.

Valuation is an important focus in both the CCI model act and the NAAG guidelines. Hospital boards regularly commission a fairness opinion to help demonstrate that they have met their fiduciary duty and negotiated a fair price. In practice, AGs want to engage their own financial expert to perform a fairness opinion to guarantee independence and ensure that the nonprofit assets are being acquired for at least fair market value.

Overview of the Fairness Opinion Process

A fairness opinion is a written opinion provided by a qualified financial advisor (e.g., a valuation firm, investment bank, accounting firm, etc.) indicating that a transaction is fair from a financial point of view. Fairness opinions incorporate an analysis of the financial terms of a transaction, including deal price and purchase consideration, but do not constitute legal, regulatory, accounting, insurance, tax, or other similar advice. These opinions do not address the underlying business decisions of the parties involved in the transaction or consider the merits of the transaction relative to alternative strategies or transactions in which the parties may have engaged. A fairness opinion commissioned by the AG is intended to be used as only one piece of input for the AG to consider in the analysis of the transaction. While the AG’s review will certainly include an evaluation of public benefit considerations, such as continuation of core medical services and maintenance of existing charity care policies, these nonfinancial considerations are outside the scope of the fairness opinion.

The due diligence and analysis performed in support of a fairness opinion is extensive and complex. It is best practice for an AG to involve their financial advisor in the process as early as practical so that the advisor can complete their work contemporaneously with the other aspects of the AG’s review. Due diligence will include a detailed review of the parties’ application to the AG, related correspondence, and all relevant transaction and financial documents, including the purchase agreement, presentations to the board by investment bankers and other advisors, board minutes, historical financial statements, and budgets and long-term financial plans prepared by management. The fairness opinion provider will conduct interviews with key hospital executives and their consultants and will frequently perform a site visit to the hospital.

The cornerstone of the fairness opinion will be the valuation analysis. Consideration should be given to the three valuation approaches: the Income Approach, the Market Approach, and the Asset Approach.

- Income Approach – the Discounted Cash Flow Method, a multi-period model, is commonly used in hospital valuations. Cash flow projections developed from board-approved budgets/forecasts are discounted at a rate of return derived from hospital industry market data.

- Market Approach – the Selected Public Company Method and Merger & Acquisition Method are also common hospital valuation methodologies. Pricing multiples derived from stock transactions of publicly traded hospital operators or prior hospital sales are used to estimate a range of indicated value. Given the abundance of hospital merger and acquisition activity over the last 10 years, there is a wealth of available market data that can be used to analyze deal fairness.

- Asset Approach – the Adjusted Book Value Method, a “balance sheet-driven” approach, is used in instances in which the Income and Market Approaches result in an indicated range of value below the net fair market value of the hospital’s tangible and working capital assets.

The fairness opinion will include a review and analysis of other deal terms and the consideration to be received relative to the range of indicated values. Deliverables are typically a short letter outlining the transaction and analysis; however, the letter should be supplemented with a presentation that provides a more detailed overview of the due diligence process and analysis supporting the opinion.

Access to information and management, as well as the complexity of the transaction, are often the most significant variables in concluding the opinion analysis. While fairness opinions can sometimes be completed in as little as two to four weeks, delays in gathering information and scheduling due diligence interviews with hospital executives can extend the process. Engaging a fairness opinion provider early in the process will help to lessen or avoid any information delays.

Special Considerations for Nonprofit Conversions

Nonprofit hospital conversions are unique transactions. Performing a fairness opinion in this setting requires specialized industry knowledge and experience with the nuances of these deals. For example, it is necessary to adjust the valuation to be consistent with the assets included in the deal and the nature of the hospital post-conversion. While nonprofit hospitals may receive financial support from parties such as a foundation, municipality, or local taxing district, this financial support cannot legally continue after the conversion to for-profit ownership. Accordingly, the economic impact of this support must be adjusted from historical and projected financial results to isolate the value of the hospital’s operating assets (i.e., the assets being purchased). Similarly, the economic impact of any excluded assets must also be adjusted from financial results. Failure to make these adjustments will result in a mismatch between the valuation and the consideration to be received.

When a hospital valuation is based on an appraisal of its tangible property due to the expectation of modest cash flow or operating losses, it is essential that the appraisals consider the presence of “economic obsolescence.” Because many of a hospital’s tangible assets, particularly its real property, are considered to be “special purpose” property without an alternative use, appraisers will commonly value these assets based on an estimate of replacement cost. This methodology can result in an overstatement of value if the tangible appraisals are not adjusted to reflect the economics of the underlying business operations.

Additionally, there can be confusion as to what is actually purchase consideration in nonprofit conversions. Nonprofit boards will often present the capital commitment made by the buyer as part of purchase consideration. While capital commitments are important deal provisions as they provide assurance that the buyer will maintain and improve the acquired hospital facilities during their ownership, these capital purchases are buyer-owned assets. Any financial benefit from these capital investments will inure to the buyer’s benefit and not the seller. Including capital commitments as a component of purchase price overstates the true consideration received by the nonprofit seller.

AGs should be aware of these potential missteps when reviewing nonprofit conversion fairness opinions. Mismatching the valuation to the consideration for the assets included in the deal, overstating the value of assets, or overstating the purchase consideration can quickly lead to flawed fairness conclusions.

Assisting in the Nonprofit Conversion Process

As healthcare markets become increasingly competitive, nonprofit community hospitals will continue to seek larger partners to remain viable. These transactions are contentious by nature as stakeholders will actively voice fears about the potential loss of access to healthcare services and local control. State AGs play a key role in reviewing nonprofit conversion transactions and protecting the interests of the communities that these hospitals serve, including ensuring that charitable assets are not sold for less than fair market value. Partnering with an experienced, independent, and objective advisor to provide a fairness opinion analysis will help the AG determine that the consideration received in the nonprofit conversion is fair from a financial point of view.

- The Health Care Services Acquisition Report. 24th Edition, 2018. Irving Levine Associates.

- Ken Marlow, Lanta Wang, and Rex Burgdorfer, “Defending the Deal: The Attorney General Review Process in Nonprofit Hospital Conversions,” AHLA Connections, April 2016.

- U.S. Government Accountability Office. (1997, December). "Not-For-Profit Hospitals Conversion Issues Prompt Increased State Oversight." (Publication No. GAO/HEHS-98-24). Retrieved from https://www.gao.gov/archive/1998/he98024.pdf

- Community Catalyst, Inc. (2003, October). A Conversion Model Act. Retrieved from https://www.communitycatalyst.org/doc-store/publications/a_conversion_model_act_oct03.pdf

- U.S. Government Accountability Office. (1997, December). "Not-For-Profit Hospitals Conversion Issues Prompt Increased State Oversight." (Publication No. GAO/HEHS-98-24). Retrieved from https://www.gao.gov/archive/1998/he98024.pdf