English

English

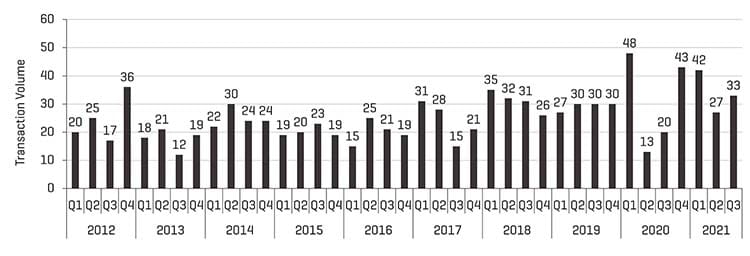

North American metal forming transaction volume is up 26% over the prior year through the first nine months of 2021. M&A activity is being driven by numerous factors, including anticipated tax rate increases for sellers and pandemic-delayed transactions coming to market this year. Outside of a handful of sectors (e.g., commercial aerospace or oil & gas), many metal forming businesses experienced a dramatic rebound in financial performance during the fourth quarter of 2020 that has continued into 2021. Traditional lenders aggressively reentered the market at the beginning of the year and record amounts of private equity capital are pursuing acquisitions. Combined with healthy strategic buyer balance sheets, these factors have strengthened the M&A and financing markets to pre-pandemic levels. Sellers that survived the depths of the pandemic found themselves faced with the near-term prospect of higher taxes and flooded the market with transactions over the past 12 months. There is now a large backlog of deals trying to close during the fourth quarter of 2021 and limited capacity for new deals until early next year.

Key Takeaways:

- Rebound in company performance and potential tax law changes driving sellers into the market

- Onset of pandemic last year created pent-up supply/demand of deals that started to loosen fourth quarter of 2020

- Financial buyers continue to have strong interest in metal forming businesses, accounting for over 70% of year-to-date transaction volume

- Aggressive lending environment supports M&A activity

- Buyers have limited bandwidth to evaluate transactions and have become increasingly selective about which deals to pursue

- Fourth quarter transaction launches pushed into early next year due to unprecedented number of deals trying to close by year-end

- Public company share prices and valuations driven higher by economic tailwinds, government stimulus, low interest rates and overall strong investor appetite for equities

Quarterly Metal Forming M&A Volume (through November 9th, 2021)

Source: CapIQ & Stout Capital, LLC

Stout Proprietary Metal Forming M&A Database Highlights

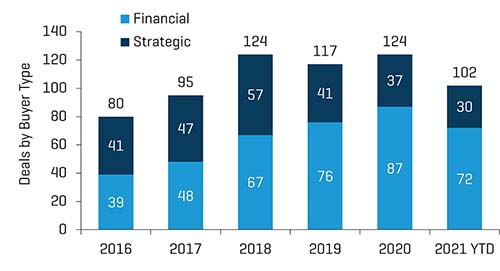

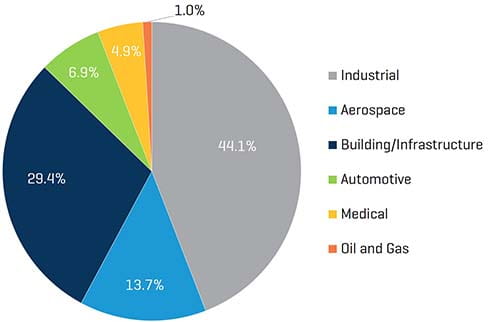

With record amounts of capital at their disposal and a robust lending environment, financial buyers accounted for over three-quarters of metal forming transaction volume year-to-date, continuing the trend seen over the past two years. This group includes “hybrid” buyers (strategic buyers owned by private equity firms) that can compete aggressively against pure play strategics in M&A sale processes. The relative share of Building / Infrastructure transactions grew for a second year in a row to 29.4% of total volume as sellers seek to capitalize on strength in the residential construction and remodeling market. Volumes in the remaining metal forming sectors were relatively flat versus the prior year.

Share of Transactions by Buyer Type (through November 9th, 2021)

Source:CapIQ & Stout Capital, LLC

2021 Transaction Volume by Sector (through November 9th, 2021)

Source:CapIQ & Stout Capital, LLC

Notable transactions announced during the first nine months of 2021 include:

- PCX Aerostructures, LLC’s acquisition of Senior Aerospace Connecticut for approximately $73 million

- DBM Global Inc.’s (OTCPK:DBMG) acquisition of Banker Steel Company, LLC, a portfolio company of Atlas Holdings LLC, for $145 million

- Nucor Corporation’s (NYSE:NUE) acquisition of the Insulated Metal Panels Business of Cornerstone Building Brands, Inc. for approximately $1.0 billion

- MiddleGround Capital portfolio company Shiloh Industries, Inc.’s divestiture of the Company’s U.S. BlankLight® business to TWB Company, LLC for a total consideration of $105 million

- Gibraltar Industries, Inc’s (Nasdaq: ROCK) acquisition of TerraSmart, LLC, for a total consideration of $220 million

- Dorman Products, Inc.’s (NasdaqGS:DORM) acquisition of Dayton Parts, LLC, a portfolio company of AEA Investors LP, for approximately $338 million

- Brookfield Business Partners L.P.’s (NYSE:BBU) acquisition of DexKo Global Inc., a portfolio company of KPS Capital Partners, LP, for $3.4 billion

- Nucor Corporation’s (NYSE:NUE) acquisition of Hannibal Industries, Inc. for $370 million

- Janus International Group, Inc.’s (NYSE:JBI) acquisition of Doors & Building Components Inc., a subsidiary of Cornerstone Building Brands, Inc., for a total consideration of $168 million

- Materion Corporation’s (NYSE:MTRN) acquisition of H.C. Starck’s Electronic Materials Portfolio for a total consideration of $380 million

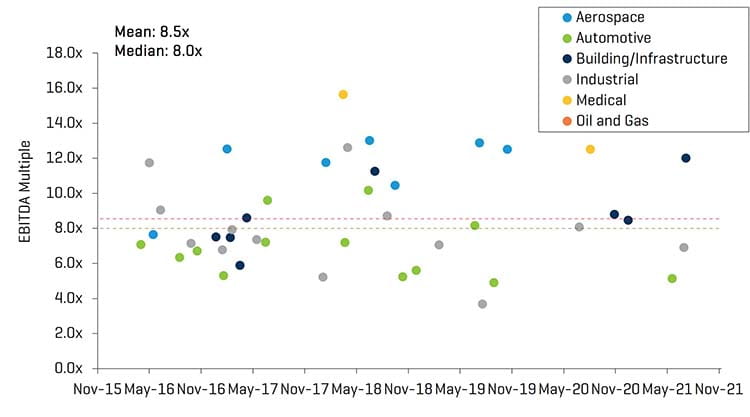

Select Transaction EV/EBITDA Multiples

Source:CapIQ & Stout Capital, LLC

Spotlight on Reshoring and Automation

North American metal formers are benefitting from COVID-related supply chain disruptions that have prompted customers to reevaluate sourcing decisions. According to a September report published by the Reshoring Initiative®, reshoring and foreign direct investment job announcements for 2021 are projected to increase 38% over the prior year and reach the highest annual total recorded to date. The report further notes that the rate of U.S. jobs coming from China is largely underreported in the data because factory announcements do not report the country whose imports are replaced. Nearshoring has also gained traction as Mexico and Canada provide logistical and cost advantages over Asian countries. The Reshoring Initiative® estimates that 40% of the value in product shipped from Mexico to the United States and 25% shipped from Canada contains U.S. content. In contrast, only 4% of the value of product shipping from China to the United States contains U.S. content.

Reshoring has created positive tailwinds for owners looking to sell businesses in 2021 and beyond. Anecdotally, many of Stout’s manufacturing clients have been quoting and winning programs that were previously sourced overseas. In some cases, the trend has resulted in meaningful increases in projected financial performance over the coming years. While accelerated growth is generally a positive for sellers, this dynamic has prompted questions from prospective buyers around companies’ ability to scale operations with scarce resources such as labor and raw materials. One obvious solution is growing investment in technology and automation. Results from McKinsey’s December 2020 Global Economic Conditions survey revealed that approximately 75% of respondents in North America and Europe said they expected investment in new technologies to accelerate in 2020–24, up from 55% who said they increased such investment in 2014–19. Accordingly, we’ve seen metal forming companies increasing capital expenditure budgets over the next 12-24 months to offset continued tightness in labor markets.

Public Company Performance

Equity markets have grown significantly over the past twelve months, fueled by economic recovery, government stimulus measures, and low interest rates. The Dow is up nearly 23% since November 2020 while the S&P 500 and NASDAQ are up approximately 35% and 34%, respectively, over the same period. Within the metal forming industry, current EV/EBITDA multiples for all sectors other than Aerospace and Building/Infrastructure were slightly below December 2020 trading multiples as earnings have caught up with share price growth.

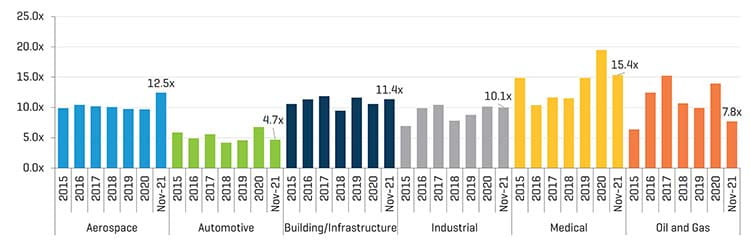

Public Companies: Last Twelve Months (“LTM”) EV/EBITDA Multiples (December 31, 2015 to November 9, 2021)

Source:S&P CapIQ

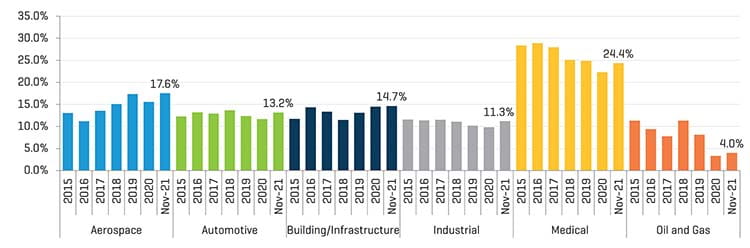

Public Companies: LTM EBITDA Margins (December 31, 2015 to November 9, 2021)

Source: S&P CapIQ

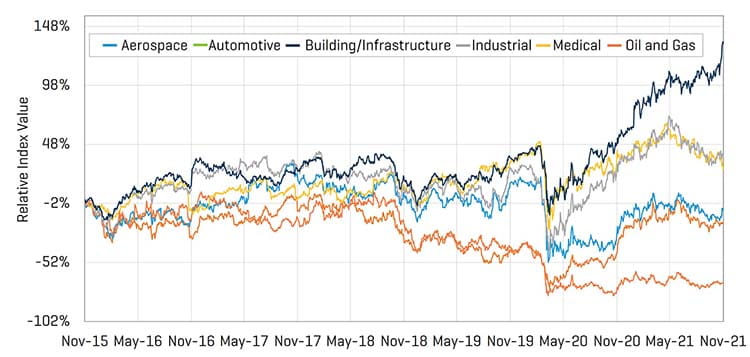

With the exception of Oil and Gas, all 2021 metal forming share price indices are trading above COVID lows. While Building/Infrastructure share prices have continued to soar, the other metal forming indices have retreated somewhat since mid-2021 as supply chain issues in key end markets and inflationary concerns weigh on share prices.

Public Companies: Relative Share Price Performance (November 9, 2015 to November 9, 2021)

Source: S&P CapIQ

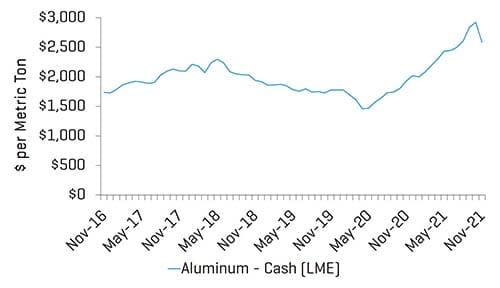

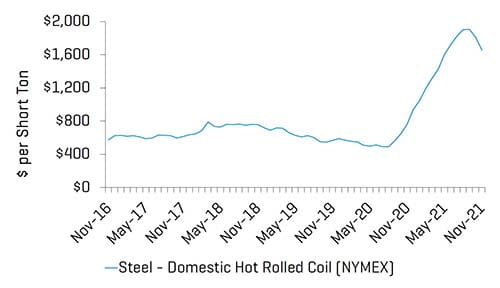

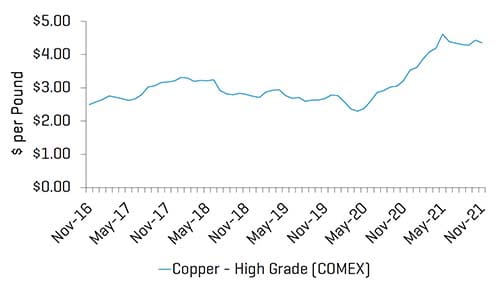

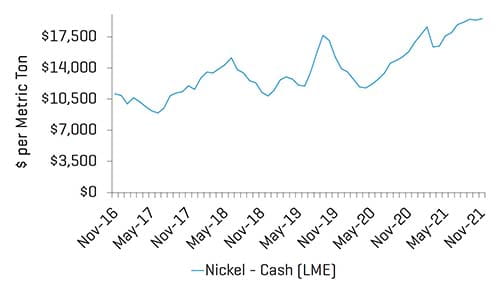

Metal Pricing

Domestic metals prices rose rapidly in 2021, reaching multiyear highs across various metals. While prices have dropped slightly from their peaks in Q2 and Q3 2021, they remain significantly above prior year levels due to strong end market demand, import restrictions and prolonged constraints throughout the metals supply chain.

Steel

Source:S&P CapIQ

Copper

Source:S&P CapIQ

Nickel

Source:S&P CapIQ

Aluminum