English

English

The life insurance industry provides protection against the premature death of policyholders over fixed, variable, and indefinite terms. In the event of a policyholder’s premature death, insurance companies guarantee a payout to a policyholder’s named beneficiaries. In exchange for taking on this risk, insurance companies charge policyholders premiums, which can be either one-time or recurring, over the insurance policy’s defined term.

Insurance providers generate income in two ways: 1) through the premiums charged to policyholders and 2) through investment income on the proceeds from premium payments. Given that a portion of insurance companies’ economic income is generated through returns on investment premiums, it is difficult to project the cash flows of insurance providers accurately, which limits the use of the discounted cash flow (DCF) method. Additionally, the DCF method is not typically applicable to insurance companies, as it is difficult to accurately project free cash flow as a result of the following:

- Insurance companies do not typically make material capital expenditures. They invest instead in human capital, marketing, and other operating expenses, which are included in their projected earnings.

- Insurance companies do not have what is normally defined as “net working capital”; their balance sheets include investments, which have no set collection date, and policy liabilities, which have various and unpredictable payment dates.

Instead, the discounted net income (DNI) method, another form of the Income Approach, is used to value insurance companies. While the DNI method provides an indication of the value of an insurance company, it is not typically applied in isolation, as the Market Approach also provides key indications of value for insurance companies. The Income Approach and Market Approach are used to determine the equity value of an insurance company, as enterprise value is not typically calculated.

Income Approach

While difficult to project, net income includes investment income, thereby including the impact of the returns on an insurance company’s invested premiums. Additionally, projected net income captures the economic impact of any capital expenditures, because the depreciation expense associated with any capital expenditures will be included in the firm’s projected net income. As a result, the DNI method is often used to value insurance companies. The DNI method involves projecting an insurance company’s net income and discounting the projected earnings to a present value amount using the required rate of return on the insurance company’s equity. The value of the discounted earnings stream reflects an estimate of the equity value of the insurance company.

Market Approach – Key Multiples

The Market Approach to valuing a company first involves calculating multiples of operational performance relative to indicators of value for comparable publicly traded companies and merger and acquisition (M&A) transactions. A statistical analysis of these calculated multiples is typically performed; after taking into consideration the subject company’s size, projected growth trends, profitability, and risk factors relative to the publicly traded companies and M&A transactions, a multiple or multiples is or are applied to the subject company’s projected or historical operating metrics.

A key multiple used in valuing insurance companies is the market value of equity (MVE) / book value (BV) multiple (MVE/BV). MVE is calculated as a company’s market price per share times its shares outstanding, whereas BV is an accounting construct defined as a company’s total assets less its total liabilities. Specifically, BV consists of a company’s retained earnings plus its net income for a given period minus any dividends paid to the company’s shareholders for a given period.

MVE/BV multiples serve as accurate indicators of value for insurance companies because substantially all of an insurance company’s assets and liabilities are financial in nature (i.e., investments and policy liabilities) and contribute to earnings (premium and investment income). It is important to note, however, that BV includes accumulated other comprehensive income (AOCI), which is composed of four items not included in a company’s net income for a given period:

- Unrealized holding gains or losses on investments that are classified as available for sale (AFS)

- Foreign currency translation gains or losses

- Pension plan gains or losses

- Pension prior service costs or credits

Once one of these four gains or losses is realized, it is shifted out of AOCI and included in net income, effectively shifting the gain or loss to the retained earnings account. Of particular importance in applying the MVE/BV multiple in the valuation of life insurance companies is the first component of AOCI.

As previously noted, a portion of a life insurance company’s economic income is realized through the gain or loss of invested premiums. The investments made on these premiums are typically classified as AFS and are marked to market on a company’s balance sheet.[1] Including AOCI in BV when calculating MVE/BV multiples for life insurance companies can distort the accuracy of a company’s true economic income and introduce volatility, as the inclusion of AOCI subjects the company’s multiple to the fluctuation in value of its AFS securities. Based thereon, AOCI is typically excluded from BV when calculating MVE/BV multiples for insurance companies; however, for comparative purposes, MVE/BV multiples including and excluding AOCI are typically evaluated in tandem.

Applying the selected MVE/BV multiples to a subject company’s recorded book value yields an indicated equity value for the company using the Market Approach. Notably, this approach ignores the fact that insurance companies’ BVs include information about a company’s future earning potential. To capture both the market value and earning potential of an insurance company using the Market Approach, multiples conditioned on (or implied from) a company’s return on average equity (ROAE) are used. In order to calculate these conditional multiples for a subject company, a regression analysis on the guideline companies’ MVE/BV multiples and their ROAE may be performed.

Regression Analysis

In determining conditional MVE/BV multiples, a regression analysis is performed in order to determine the relationship between i) the selected guideline companies’ MVE/BV (inclusive and exclusive of AOCI) multiples and ii) the selected guideline companies’ ROAE (inclusive and exclusive of AOCI). When performing a regression analysis, it is important to consider R2, a statistical measure of how well the regression line “fits” the data points. R2 ranges from zero to one, whereby one indicates a line of perfect fit and implies that the change in the independent variable entirely explains the change in the dependent variable. In this regression analysis, a higher R2 value would indicate better predictability of MVE/BV multiples based on ROAE.

The regression yields the formula y = mx + b, where “y” is the MVE/BV multiple and “x” is the ROAE. The formula is applied to the subject company in order to calculate an implied MVE/BV multiple.

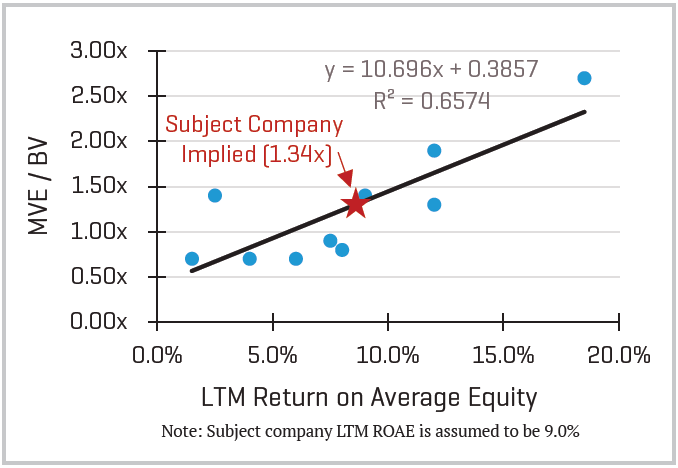

For example, a regression of the guideline companies’ MVE/BV to the selected guideline companies’ latest 12-month (LTM) ROAE yielded the formula y = 10.696x + 03857 (Figure 1). Assuming our subject company’s LTM ROAE is 9.0%, the implied multiple is calculated as follows.

1.34x = (10.696*9.0%) + 0.3857

Figure 1: MVE/BV vs. LTM ROAE

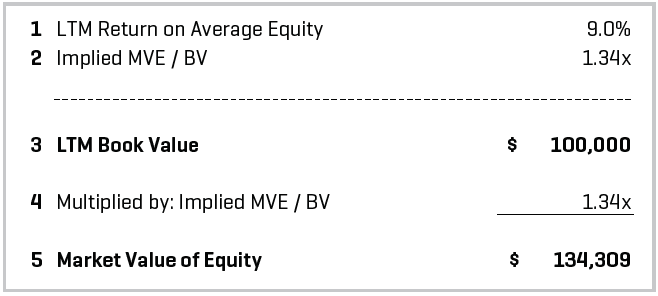

Applying the implied MVE/BV multiple to the subject company’s BV yields the indicated MVE for the subject company (Figure 2).

Figure 2: Indicated Market Value of Equity ($ in thousands)

A similar analysis can also be performed for the precedent M&A transactions to determine the relationship between i) the selected group of acquired companies’ MVE/BV (inclusive and exclusive of AOCI) multiples and ii) the selected group of acquired companies’ ROAE (inclusive and exclusive of AOCI).

Present Value of Future Market Value of Equity Analysis

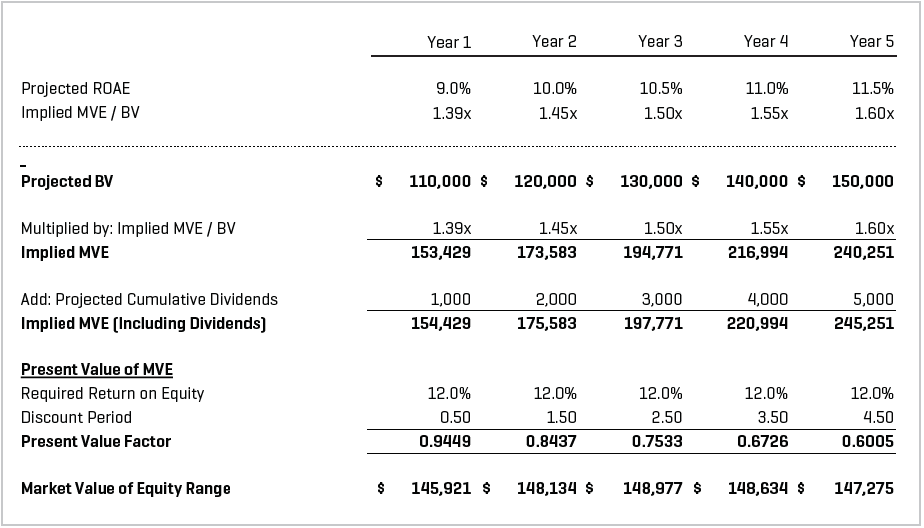

The regression of the selected guideline companies’ MVE/BV multiples to return on average equity can be further applied to calculate future implied MVE/BV multiples for the subject company. The regression formula is applied to the subject company’s projected ROAE to yield the future implied MVE/BV multiples.

Applying the implied MVE/BV future multiples to projected BV yields the undiscounted implied MVE range. After incorporating projected cumulative dividends, the future values are discounted to present value using the subject company’s calculated equity rate of return.

The analysis is performed inclusive and exclusive of AOCI (Figure 3).

Figure 3: Present Value of Future Market Value of Equity ($ in thousands)

Breaking With Tradition

A traditional Income Approach is not applicable to insurance companies, primarily because free cash flow is difficult to project. Additionally, a traditional Market Approach based on an insurance company’s historical BV fails to capture future earning potential. As a result, the less traditional methods described herein can be used to provide indications of an insurance company’s equity value.

The DNI method relies on the projections developed for a subject company, while the Market Approach and regression analyses rely more heavily on observable market data for comparable publicly traded companies and precedent M&A transactions. No single method is superior to another and therefore should not be employed in isolation. In practice, the application of each of these methods, along with an in-depth understanding of a subject company’s historical operational and financial performance, provides a supportable estimate of value for an insurance company.

- An AFS security is a debt or equity instrument that is a default classification for any investments that are not classified as trading securities or held-to-maturity securities. A trading security designation is assigned to investments where the intent is to sell them in the short term to earn a profit. A held-to-maturity security classification is assigned to investments where the intent is to hold them until the maturity date.