English

English

J. Paul Getty, a renowned American industrialist, famously quoted “Formula for success: rise early, work hard, strike oil.” Numerous individuals and companies have followed Mr. Getty’s advice and have built substantial fortunes striking oil. The oil and gas industry, particularly in the U.S., has been one of the “shining stars” as the American and global economies recovered from the recession in late 2008. While oil prices dipped during the recession, the recovery in prices was relatively quick with the West Texas Intermediate (WTI) crude oil price averaging $96.45 per barrel between the start of 2011 through the first half of 2014. The second half of 2014 and the beginning of 2015 has been a completely different “story” as it relates to oil prices. Since reaching $107.62 per barrel on July 23, 2014, the WTI crude oil price has declined precipitously, reaching $53.27 per barrel at year-end 2014 and $48.66 per barrel at the end of March 2015. Similarly, the price of Brent crude oil has declined from $109.63 per barrel on July 1, 2014, to $58.21 per barrel at year-end 2014 and $54.36 per barrel at the end of March 2015. The following graphs present the WTI and Brent crude oil prices since the beginning of 2011 through March 2015.

The substantial decline in oil prices has resulted in significant implications for oil and gas companies and businesses tied to the commodity. Several “bell weather” companies in the oil and gas industry have cut capital expenditure budgets for 2015 and announced workforce reductions. Schlumberger Ltd., the world’s largest oilfield service company, announced on January 15, 2015 that it laid off 9,000 workers in late 2014 and took more than $1 billion in charges in the fourth quarter of 2014. According to a Wall Street Journal article on Schlumberger, “profits for the quarter fell sharply as a glut of oil and tepid demand for fuel drove down the price of crude and demand for Schlumberger’s services.”1 ConocoPhillips, the largest independent oil and gas company, slashed its 2015 capital expenditure budget, citing lower crude oil prices. Mr. Ryan Lance, ConocoPhillips’ chief executive officer, released a statement that “We are responding decisively to a weak price outlook in 2015 by exercising our capital and balance sheet flexibility.”2 According to an interview conducted by The Energy Report with Mr. Steven Salz, a special situations analyst at M Partners, falling oil prices are hurting oil field services companies in different measures depending on their specialties, but all are taking hits. Mr. Salz thinks “the Halliburton/Baker Hughes merger may be the first of a series of consolidations in the space.”3

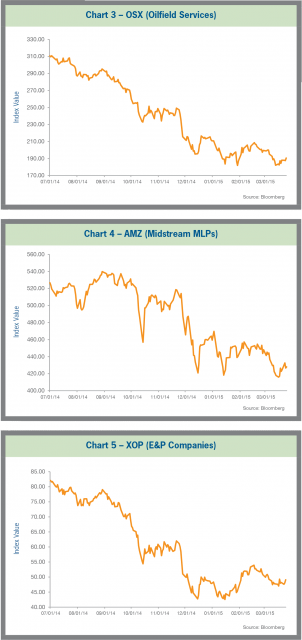

Publicly traded oil and gas companies have experienced a significant decline in their market capitalizations. The S&P Oil & Gas Exploration & Production Select Industry Index, an index of upstream exploration and production companies, has fallen by 40% since the second half of 2014. The PHLX Oil Sector Service Index, an index of oilfield services companies, has dropped by 39% over the same timeframe. Similarly, the Alerian MLP Index, an index of midstream companies, has declined by 19% over the same time period. Graphs 3-5 present these precipitous declines in these indices.

Impairments

In addition to modifying operational and growth strategies, the decline in oil prices has ramifications for companies’ financial statements and tax planning. An important consideration for companies is potential impairment of assets, including goodwill. Upon the occurrence of a business combination, goodwill is typically recorded on the balance sheet. Goodwill represents the excess of the purchase price of a business combination over the Fair Value of the net assets acquired. For publicly traded companies and private companies not planning to adopt guidelines recently issued by the Private Company Council, goodwill is an indefinite and long-lived asset and is not amortized. Rather, goodwill is tested for impairment, at least annually. Goodwill impairment testing standards are governed by ASC Topic 350-20-35, Goodwill—Subsequent Measurement, and ASC 820, Fair Value Measurement.

It is expected that there will be more incidences of impairments announced during 2015 than 2014. Such was the speed and unexpectedness of the decline in oil prices that even acquisitions made in 2014 can potentially see goodwill impairments. Given the volatility and uncertain environment in the oil and gas industry, there will be significant scrutiny of valuations performed during an impairment testing, and valuation experts will have to vigorously defend assumptions behind the projected financial performance. In addition, the use of “Step 0” (a qualitative impairment testing technique) is likely to reduce given the uncertainty in the current pricing environment and the decline in valuations.

In general, the Step 0 test allows an entity to first assess qualitative factors to determine whether it is more likely than not (i.e., more than 50%) that the Fair Value of a reporting unit is less than its carrying value. In order to make this evaluation, the FASB outlines relevant examples and circumstances to consider, including:

- General macroeconomic conditions such as a deterioration in general economic conditions, limitations on accessing capital, fluctuations in foreign exchange rates, or other developments in equity and credit markets

- Industry and market conditions such as a deterioration in the environment in which an entity operates, an increased competitive environment, a decline in market-dependent multiples or metrics (in both absolute terms and relative to peers), a change in the market for an entity’s products or services, or a regulatory or political development

- Changes in cost factors such as increases in raw materials, labor, or other costs that have a negative effect on earnings and cash flows

- Overall financial performance (for both actual and expected performance)

- Entity and reporting unit specific events such as changes in management, key personnel, strategy, or customers, contemplation of bankruptcy, litigation, or a change in the composition or carrying amount of net assets

- If applicable, a sustained decrease in share price (in both absolute terms and relative to peers)

Several factors previously outlined are particularly relevant in the current environment. The deterioration in the environment in which oil and gas companies are operating, the decrease in the market for such companies’ products and services, and the decline in the financial performance of oil and gas companies in the fourth quarter of 2014 and expected reductions in 2015, may all indicate potential impairment. As a result, it would be prudent for oil and gas companies and may be required by their auditors and advisors to perform Step One of the impairment test. This test involves determining the Fair Value of a group of assets (the company or reporting unit(s)) where goodwill is recorded and comparing the estimated Fair Value to the book-carrying value of this group of assets. If, under the Step One analysis, the Fair Value is greater than the carrying value, then no impairment is indicated. If the carrying value is greater than the Fair Value, then a Step Two analysis is conducted to quantify the level of impairment which is booked as a loss on the income statement. In addition, the precipitous decline in equity market capitalizations may further support the need for a detailed impairment analysis. In addition to goodwill, ASC 360-10 requires impairment testing of other long-lived assets like plant, machinery, and equipment. The oil and gas industry is highly capital-intensive and the reductions in capital expenditure budgets of upstream exploration and production companies will reduce the demand and market for equipment used in the industry.

Other Valuation Considerations

In addition to impairment considerations, there are other important valuation implications under the Fair Value reporting standard. For example, there have been recent instances where trading activity has “dried up” in high yield debt issued by oil and gas companies. In other words, there is an absence of an “orderly market.” As a result, to the extent that any quotes are available, these are likely not representative of pricing in an orderly market. Therefore, such securities may need to be valued using Level 3 inputs. Such inputs are not observable from objective sources. The most common Level 3 Fair Value measurement is an internally developed cash flow model. Investment companies, such as private equity firms and hedge funds, have invested substantial capital in high yield debt and equity securities of oil and gas companies. These funds are required to report their investments at Fair Value and, due to the absence of an orderly market, would need to reevaluate their valuation models.

During the recent oil and gas boom from 2010 through the first half of 2014, private equity funds invested a lot of “dry powder” in oil and gas companies. Funds backed seasoned and young oil and gas management teams and incentivized these teams by issuing options and other equity-linked securities. The expectation is that these options will be cashed out upon the occurrence of an exit event like a sale or an initial public offering. For options issued by companies in the oil and gas industry, it is highly likely that such options may be currently deeply out of the money because of the decline in valuations in the industry. To keep management teams motivated and incentivized, private equity funds and their portfolio companies may need to revalue their investments and issue new options at such revised valuations.

If oil prices continue to decline or stay at current levels, financial experts and industry participants are projecting an increase in the number of oil and gas companies in financial distress, leading to further consolidations in the industry. Cash-rich companies with strong balance sheets will be potential acquirers of assets and distressed companies at bargain prices. As discussed earlier, the Halliburton/Baker Hughes transaction may cause a domino effect in the oilfield services industry with companies looking to achieve cost reductions and adapting to significantly lower capital expenditure budgets of exploration and production companies. An important financial reporting and valuation consideration in such transactions would be the purchase price allocation exercise and the evaluation of bargain purchase considerations.

Summary

In summary, the precipitous decline in oil prices has resulted in oil and gas companies slashing capital expenditure budgets and reconfiguring their operating plans. Equity market capitalizations of oil and gas companies have followed the lower oil prices, further creating stress on business operations and balance sheets. The volatile and uncertain environment has enhanced the potential of impairment of assets and other valuation considerations.

Stout has significant expertise and experience in the oil and gas industry. Combined with its deep valuation resources, Stout has earned the trust of oil and gas companies in assisting them with complex valuation matters.

--

1 The Wall Street Journal, January 15, 2015.

2 Reuters, January 29, 2015.

3 The Energy Report, December 22, 2014.