English

English

Introduction

Although the economy has recently exhibited some positive indicators, most asset classes have suffered significant declines in value during the previous 18 months. Luxury yachts, artwork, real property, aircraft, and businesses have all suffered significant declines in value. The commercial real estate market has been hit particularly hard with increased vacancies and declining lease rates impacting the ability of property owners to make mortgage payments. Combine these attributes with the current credit crunch and the near term outlook for commercial real estate market is not a positive picture.

Despite this bad news, there may be a silver lining. Currently, there is an opportunity to transfer assets to the next generation at discounted values through the use of an undivided interest ownership structure. An undivided interest is “An ownership right to use and possession of a property that is shared among co-owners, with no one co-owner having exclusive rights to any portion of the property.”1 For example, assume an asset is owned by four family members through a Tenancy in Common.2 Each member is a co-tenant and holds an undivided interest in the subject asset. The co-tenants collectively make all decisions as to the use and disposition of the asset. No one co-tenant may unilaterally mortgage, develop, or sell a portion of the asset. Consequently, the undivided interest suffers from a significant lack of control when compared to a fee-simple interest in that same asset. In addition, there is no liquid and efficient market that includes trading in undivided interests. Consequently, an undivided interest suffers from a lack of marketability.

The detrimental economic characteristics of undivided interests permit the application of valuation discounts when estimating their values. For example, if an asset is held through a Tenancy in Common and has a market value of $100 in fee-simple interest, it is unlikely that a 25% undivided interest would be worth $25. In fact, even in more normal and stable economic conditions than we are currently experiencing, the value of an undivided interest may be substantially less than a pro-rata share of a fee-simple interest. The current economic climate has contributed to a further negative impact on the estimated values of undivided interests.

Characteristics of Undivided Interests

- A fee-simple interest in an asset has the following unilateral rights, among others:

- Maintain exclusive use of the asset

- Lease the asset

- Sell or liquidate the asset

- Improve or maintain the asset

- Leverage the asset

In contrast, an owner of an undivided interest does not have the right to occupy or enjoy the use of the asset without permission from the other co-tenants. In addition, most decisions related to the management and liquidation of the asset requires unanimous consent among co-tenants. Consequently, an undivided interest suffers from a significant lack of control when compared to an asset that is owned in fee-simple interest.

Overall, the lack of control associated with an undivided interest leaves the unsatisfied investor with one of three options with respect to achieving liquidity: 1) sell the ownership interest to the other co-tenants; 2) attempt to locate another willing investor; or 3) if possible, conduct a potentially protracted and expensive partition lawsuit.

An undivided interest also suffers from a lack of marketability when compared to a fee-simple interest. This lack of marketability is primarily attributable to the following:

- No established market for undivided interests

- Obtaining financing for an undivided interest is more difficult than for a fee-simple interest

- Co-tenants may be jointly and severally liable for the debt obligations of the asset

- Negative consequences associated with suing for partition of the asset

- Creditors of individual co-tenants may be able to force the sale of the asset

An undivided interest shares similar economic characteristics as a minority equity position in a closely held company. The lack of control and lack of marketability of an undivided interest are mitigated by the fact that, in most states, an investor may file suit to have the asset partitioned by the court. If the court decides that the asset cannot be partitioned equitably, then it can order a forced sale of the asset and a division of the net proceeds after costs.

Despite the ability to achieve liquidity through a partition action, investors are typically wary of purchasing an asset that may require litigation to obtain liquidity. Consequently, the application of valuation discounts to the fee-simple interest value of the asset is typically appropriate.

Factors Affecting the Value of an Undivided Interest

In determining the Fair Market Value of an undivided interest, the following quantitative and qualitative factors should be considered:

- Value of the asset and size of the undivided interest

- Likelihood and ability to partition the asset

- Financial performance of the asset

- Debt obligations and access to additional financing

- Number of co-owners

- Prior transactions in the undivided interests

- Empirical studies of valuation discounts for lack of control and lack of marketability

Value of the Asset and Size of the Interest

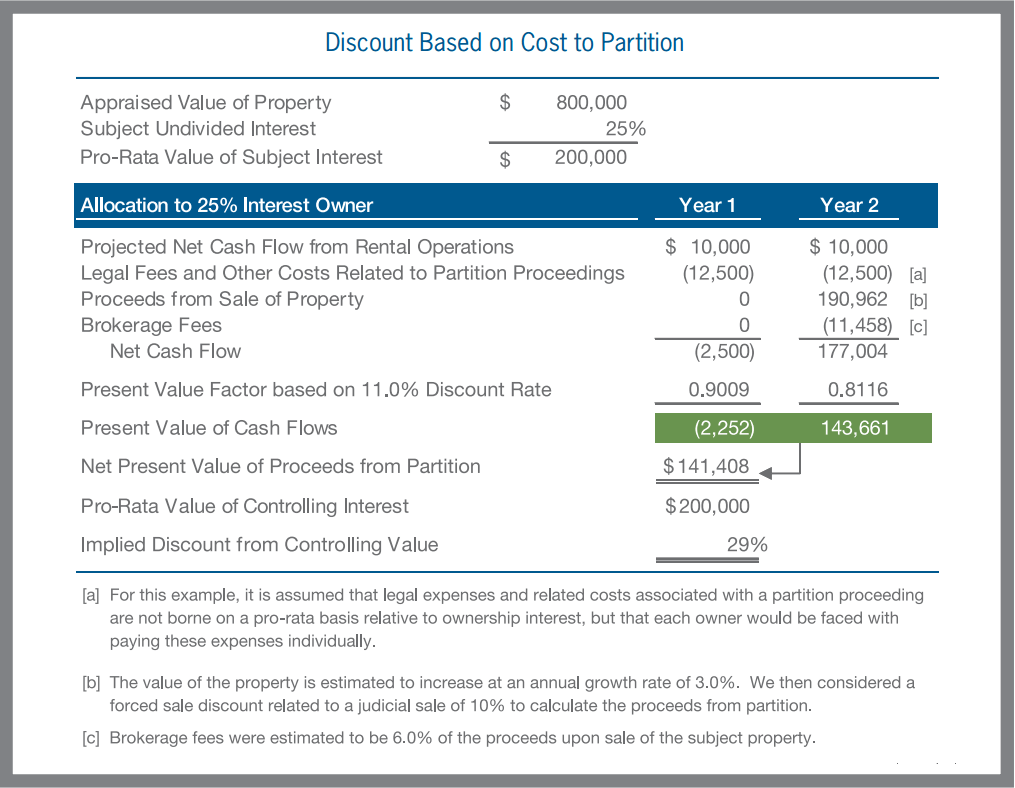

The first step in valuing an undivided interest is a determination of the Fair Market Value of the subject asset and the undivided interest in fee-simple interest. The value of the undivided interest may be affected by state laws related to the allocation of costs of a partition action among co-tenants. In the event the co-tenant bears the full costs of partition regardless of ownership percentage, size of the undivided interest may significantly impact the value of that interest. For example, if the subject interest is a 5% undivided interest in an asset worth $500,000 (i.e., a $25,000 pro-rata value) and the cost to partition the asset is $10,000, the partition costs represent a significant portion of the pro-rata value of the subject undivided interest. In this situation, the cost to partition would have a material impact on the Fair Market Value of the subject interest.

Likelihood and Ability to Partition the Asset

When conducting a partition analysis, an assessment of whether a partition action would result in the sale of the asset or merely a division of ownership should be considered. If the asset can be partitioned, it may be necessary to consider whether the division of ownership would change the underlying assumptions used in the appraisal of the interest. For instance, the shape or configuration of land may be an important characteristic of the appraisal value. If the asset is theoretically partitioned, the assumptions used in the appraisal may no longer be relevant. A partition analysis is primarily based on the following three factors:

- Quantification of the future proceeds and expenses

- Amount of time necessary to conduct a partition action

- Determination of the appropriate present value discount rate

Future Proceeds and Expenses of a Partition Action

The future value of the net proceeds available from the hypothetical sale of the asset should be considered in the analysis. The future value of the asset should be based on the projected price appreciation – or depreciation – of the asset, if any, during the partition period. Also, the expenses necessary to liquidate the asset should be considered in the determination of the future net proceeds. These expenses may include sales commissions, legal fees, survey fees, taxes, and so forth. The expenses associated with a partition action should also be estimated and included. If the asset is expected to produce income or incur expenses during the partition period, these expected revenues and expenses should be recognized and included in the analysis.

Partition Period

The amount of time necessary to conduct a partition varies by jurisdiction and by the characteristics of the subject asset. Generally, valuation professionals (and the courts) have considered two to four years to be reasonable. Under certain circumstances, the partition period may be longer. If the appraised value in fee-simple interest is estimated based on a highest-and-best-use assumption that is inconsistent with the current use of the subject asset, the assumed length of time associated with conversion and subsequent partition may be significantly greater than two to four years.

Present Value Discount Rate

Often, the courts will use capitalization rates derived from

appraisals of fee-simple interests to estimate the value of the economic returns associated with a partition action. While this may provide a useful starting point in assessing the appropriate discount rate, an upward adjustment is typically warranted. These rates of return are derived from transactions involving the sales of entire properties in fee-simple interest. Thus, the capitalization rates assume a controlling interest owner with the ability to liquidate the assets at will. A capitalization rate derived from the sales of properties in fee-simple interest may be understated when used to estimate the present value of proceeds attributable to an undivided interest. The calculation of a present value discount rate to use in a partition analysis should consider the following ownership characteristics of an undivided interest:

- Lack of control over the management and operations of the asset

- Likely holding period of two to four years

- Negative economic consequences resulting from actions of other co-tenants

- Expenses and hurdles associated with litigation in order to achieve liquidity

Overall, a cost to partition approach, when applied with meaningful assumptions, can provide a reasonable benchmark in establishing the Fair Market Value of an undivided interest. Following is a basic illustration outlining a valuation discount indicated by a cost to partition analysis.

Financial Performance of the Asset

Undivided interests are entitled to a pro-rata share of the revenues and expenses attributable to the asset. Consequently, an income-producing asset may be a more or less desirable investment depending on the expected financial performance. Obviously, properties that are expected to provide substantial cash distributions are more desirable than otherwise identical properties with little or no anticipated cash distributions. Also, the projected income and expenses associated with an asset during the time period necessary to conduct a partition action will likely be a consideration in the valuation of an undivided interest.

Debt Obligations and Access to Additional Financing

Typically, debt obligations attributable to an asset are subtracted from the appraised value in the process of valuing an undivided interest. In addition to this calculation, the following risk factors should be addressed:

- Whether co-tenants are jointly and severally liable for the debt obligations of the asset

- Whether partition and sale of the asset would result in the call of debt obligations

- Whether the debt obligations are assumable by the purchaser of an undivided interest

Depending on the answers to these questions, an upward or downward adjustment to the applicable valuation discount may be warranted. In addition, it should be noted that financial institutions are typically hesitant to lend against partial interests in assets.

Number of Co-tenants

Another qualitative factor to consider is the total number of co-tenants associated with the asset. The complexity of managing any asset increases with the number of co-tenants. Consequently, the relative lack of control increases as the number of co-tenants increases. However, even if the asset has only two co-tenants, valuation adjustments for lack of control and lack of marketability are typically justified.

Impact of Current Conditions

In assessing the primary assumptions involved in the assessment of the value of an undivided interest, the following points are noteworthy given the present economic environment, and suggest that higher discounts are warranted based on a cost-to-partition approach:

- Most asset values are depressed and may continue to decline

- Longer marketing periods may result in longer periods to complete a partition action

- Analysis of a partition action should consider the use of higher “forced sale” discounts given the lack of liquidity in the current market

- Higher discount rates used in a partition analysis may be warranted

- Declining financial performance of income-generating assets may result in lower cash flows during a partition proceeding

Empirical Data

Ideally, valuation discounts should be derived from empirical studies of market transactions involving undivided interests. Unfortunately, transactions in undivided interests typically are conducted between private parties, and the pertinent data are difficult or impossible to obtain. In most cases, historical transactions involving the subject interest do not exist. If transactions are present, often they were not on an arm’s-length basis. One of the reasons the courts have struggled with the conclusions presented by valuation experts in the courtroom setting pertains to the broad range of discounts indicated by the empirical data.

Given that undivided interests have some of the same economic characteristics as minority equity interests in closely held companies, comparisons can be drawn to valuation discounts obtained from empirical studies of transactions involving equity interests of closely held companies. Empirical studies of valuation discounts for lack of control and lack of marketability generally fall into one of the following categories:

- Private transactions in the common stock of companies prior to an initial public offering

- Price to net asset value of registered limited partnership interests

- Price to net asset value of closed-end mutual funds

- Private transactions of restricted stocks of publicly traded companies

- Acquisition premiums paid by acquirers of publicly traded companies

The valuation discounts provided by these studies are typically not directly comparable to an undivided interest. However, these studies provide insight into how the market discounts various assets for economic attributes related to control and marketability. Consequently, these studies should be considered in the valuation analysis of an undivided interest.

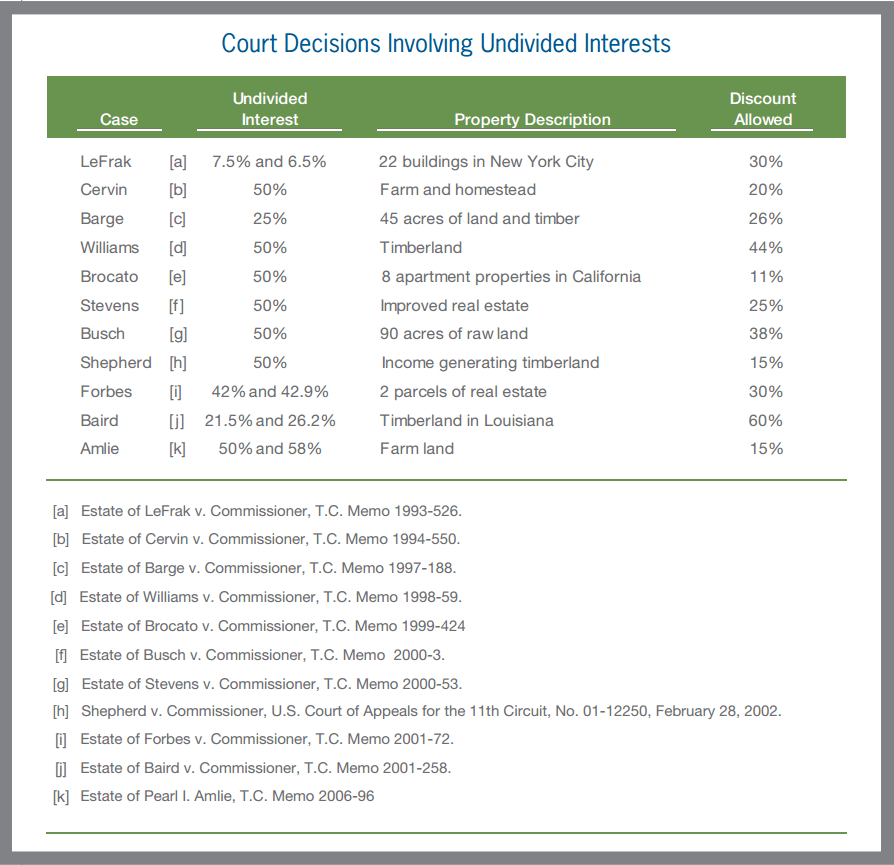

Court Decisions Related to Undivided Interest Discounts

The issue of estimating valuation discounts applicable to undivided interests has been the subject of much controversy inside the courts and among valuation professionals in the past. With that said, however, activity in the courts on this issue has certainly declined considerably relative to the number of cases in the late 1990s and early 2000s.

The courts consider a variety of quantitative and qualitative factors when determining the value of an undivided interest. Obviously, each decision is based on various facts and circumstances. In general, no valuation methodologies for undivided interests are universally accepted by the courts. As a result, analysts should be familiar with the factors that influence the relevant courts’ thinking regarding the valuation of undivided interests.

The courts have been somewhat fickle in their selection and application of valuation adjustments. Certain courts have allowed valuation adjustments of 60%. Other courts have selected valuation adjustments closer to 10%. Some courts have cited the relative lack of control and lack of marketability of an undivided interest when compared to a fee-simple interest. Other courts have solely focused on the out-of-pocket expenses associated with a partition action. Obviously, the facts and circumstances of each court case differ. Also, the quality and nature of the fee-simple interest appraisal report can have a substantial impact on the disposition of the court toward valuation adjustments. The following table references the indicated discounts determined in various court decisions since 1993.3

The valuation of an undivided interest requires knowledge and expertise from two valuation disciplines: asset appraisal and business valuation. The court decisions seem to indicate that litigants often rely on asset appraisal experts to value both the underlying assets and the undivided interest. The courts have historically expressed frustration with the lack of available evidence and supportable analysis when determining the value of an undivided interest. However, the dearth of market-based data on undivided interests is indicative of the limited and inefficient market for these ownership interests. It is important to point out that an undivided interest is a fractional equity ownership interest and not a pro-rata share of asset. An undivided interest may be much more comparable to a minority equity position in a closely held business than with a proportional ownership interest in an asset. Consequently, traditional asset appraisal techniques do not adequately address the economic issues of an undivided interest.

Conclusion

Undivided interests suffer from a variety of relatively unattractive economic and ownership characteristics. These characteristics contribute to the reduced desirability of these ownership interests when compared to fee-simple interests. The current economic situation has led to depressed asset values and longer market exposure periods, which leads to higher valuation discounts for undivided interests. These conditions may allow the gifting of undivided interests at values that are significantly lower than the value of the underlying assets in fee-simple interest.

Daniel R. Van Vleet

1 Dictionary of Real Estate Terms, 6th edition, by Jack P. Friedman, Jack C. Harris and J. Bruce Lindeman, published by Barron’s Educational Series, Inc.

2 A way for two or more people to have equal ownership interests in an asset. Each owner has the right to leave his or her share of the asset to any beneficiary upon the owner’s death. Each party (owner) in a tenancy-in-common agreement has the right to use the asset even if the physical size of the stake is different.

3 The list is not intended to be comprehensive.