English

English

Economic Climate – Ripe for Bargain Purchases

Given the difficult macroeconomic environment and tight credit markets, a large number of companies in a broad spectrum of industries have encountered significant financial distress. Because of the recent pullback in spending, corporate revenues have declined dramatically and companies have struggled with respect to the realignment of expense structures. Without the ability to obtain financing through traditional means, many businesses have been forced to divest significant portions of their business, in part or in whole, or even enter into bankruptcy, in which assets may be sold through liquidation or the restructuring process. To further exacerbate the issue, the number of potential acquirers, both financial buyers and strategic acquirers, has decreased. The lack of liquidity options for the seller (and buyers) often yields a transaction value equivalent to “fire sale” prices.

As a result of the financial distress, there have been an inordinate number of recent transactions involving bargain purchase situations. The current accounting treatment under FASB ASC Topic 805, Business Combinations, is materially different as compared to the prior regulations, which called for a pro-rata reduction in the tangible and intangible assets until negative goodwill was eliminated. Based on our experience, the accounting and valuation treatment for a bargain purchase situation requires increased documentation and financial modeling support that incorporates compliance with the Fair Value definition in order to withstand regulatory scrutiny.

Bargain Purchase: Old Versus New Purchase Accounting Standards

Prior to the issuance of the requirements set forth in FASB ASC 805, purchase accounting standards promulgated that in the event that the total net assets acquired were greater than the purchase consideration, certain assets were written down pro-rata until the value of the assets acquired was equal to the purchase consideration. If, after reducing the value of any tangible and intangible assets acquired, the value of the net assets acquired was greater than the purchase consideration, the acquiring company would record an extraordinary gain as of the transaction date (i.e., purchase price is less than the net working capital amount).

One significant change in the new purchase accounting standards is that all the assets and liabilities of the acquired business must be valued and recorded on the balance sheet at Fair Value. That is, the actual transaction consideration paid is not relied upon exclusively. As part of this process, the business is typically valued independently and the results are compared to the transaction consideration. If it is deemed that the transaction consideration is lower than the Fair Value of the business, a gain is ultimately recorded from an accounting standpoint.

Establishing the Fair Value of the Business and the Correlation to the Value of Personal Property Assets

As a first step in this process, we typically perform an independent valuation of the business as a going concern, applying commonly accepted approaches such as an Income Approach (e.g., a discounted cash flow method) and a Market Approach (e.g., a guideline company method). If that analysis supports the value of the purchase consideration, and also exceeds the sum of the values of the underlying assets acquired (such as the net

working capital, real property and personal property), then the transaction price is relied upon with respect to the allocation of the asset values.

In order to conclude on the Fair Value of the business, it may also be required that the going concern value conclusion is compared to the value of the assets on a standalone basis. The critical portion of this exercise is the valuation of the tangible assets. As part of that process, we independently value the real and personal property assets under two premises of value: (i) Fair Value in continued use; and (ii) Fair Value in exchange. From a conceptual standpoint, the minimum value of a business is equal to the hypothetical liquidation value of the assets.

A unique nature of the value of personal property assets is that the value conclusion for a particular asset depends on its highest and best use by the company. In essence, a business valuation may impact the value of personal property. For instance, as indicated previously, two commonly accepted premises of value for personal property include:

- Fair Value In Continued Use: The highest and best use of the asset is “In-Use” if the asset would provide maximum value to market participants principally through its use in combination with other assets as a group (as installed or otherwise configured for use). When using an In-Use valuation premise, the Fair Value of the asset is determined based on the price that would be received in a current transaction to sell the asset, assuming that the asset would be used with other assets as a group and that those assets would be available to a market participant. The critical concept associated with this premise of value is that the earnings that are derived by the business support the assets in place. As a result, costs to install the equipment, such as labor, wiring and piping, and taxes, are typically included.

- Fair Value In Exchange: The highest and best use of the asset is “In-Exchange” if the asset would provide maximum value to market participants principally on a standalone basis. When using an In-Exchange valuation premise, the Fair Value of the asset is determinedbased on the price that would be received in a current transaction to sell the asset standalone. The critical concept associated with this premise of value is that a buyer of the assets would consider costs of removal. As such, costs associated with installation, wiring, and piping are excluded; and any demolition costs are included (as an economic detriment) to determine the value. Typically, Fair Value In-Exchange is viewed as the minimum value conclusion for financial reporting purposes.

Based on the results of a business valuation, it may be appropriate to conclude on a personal property value based on the value under the In-Use premise, the value under the In-Exchange premise, or some value in between. To further illustrate, consider the following transaction scenarios:

- The value of the business is equal to the transaction consideration and exceeds the sum of the value of the net working capital, real property, and personal property on a Fair Value In-Use basis. As such, there is intangible asset value derived by the business. In this instance, the value of the personal property is equal to Fair Value In-Use.

- The value of the business exceeds the transaction consideration and exceeds the sum of the value of the net working capital, real property, and personal property on a Fair Value In-Use basis. As such, there is intangible asset value derived by the business. In this instance, the value of the personal property is equal to Fair Value In-Use.

- The value of the business is in between the sum of the value of the net working capital, real property, and personal property on a Fair Value In-Use basis and the value of all of the assets on a Fair Value In-Exchange basis. In this circumstance, the business valuation quantifies the amount of economic obsolescence associated with the personal property assets since the business is not generating a sufficient return to support the In-Use asset values.

- The value of the business is equal to the transaction consideration, which is below or equal to the value of the net working capital, real property, and personal property on a Fair Value In-Exchange basis.

The following details the typical purchase accounting treatment in each of the scenarios above with comments as it pertains to the impact from a bargain purchase situation.

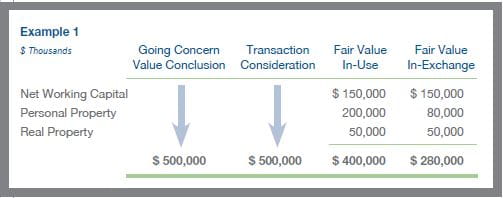

Going Concern Value = Transaction Consideration > Fair Value In-Use > Fair Value In-Exchange

In the following example, assume that the going concern value (or enterprise value “EV”), as determined by the Income Approach and Market Approach of the business, is equal to the total transaction consideration of $500 million. For this example, assume that the only tangible assets acquired are net working capital, personal property, and real property. The assets acquired are valued on both a Fair Value In-Use and Fair Value In-Exchange premise. Based on these Fair Value inputs, the total tangible asset value of the business can be calculated, as shown in the following table.

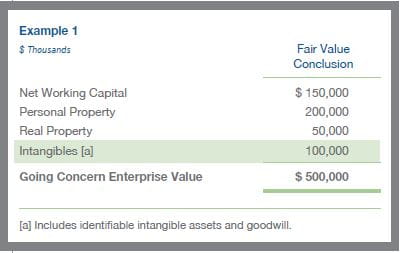

In this example, the going concern value conclusion of the business ($500 million) is greater than the implied asset values under a Fair Value In-Use and In-Exchange premise. Because the going concern value is greater than the asset value under a Fair Value In-Use premise, an “intangible gap” exists. The reconciliation of net assets acquired to going concern EV is shown in the following table.

This scenario is typical for a transaction whereby an operating company is generating a return greater than the return required on its tangible assets. In other words, there is intangible value generated when the identifiable assets are combined and employed in the company’s operations. Additionally, since the highest and best use of the assets is under a going concern basis and there is no indication of economic obsolescence, the personal property assets are valued under the In-Use premise. Furthermore, since the independent business valuation aligns with the consideration paid in the transaction, there is no evidence of a bargain purchase transaction.

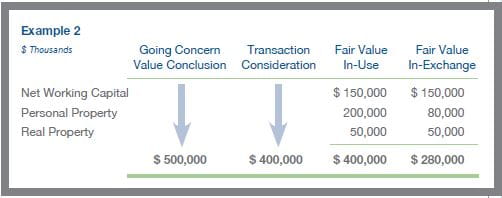

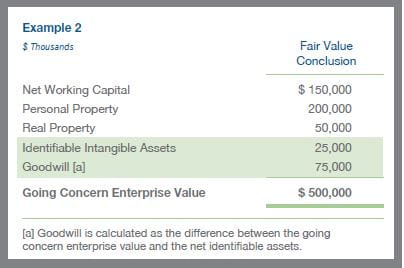

Going Concern Value > Transaction Consideration = Fair Value In-Use > Fair Value In-Exchange

In the following example, the same assumptions are considered as in the first example, except that total transaction consideration is $400 million. Additionally, the assets acquired are valued on both a Fair Value In-Use and Fair Value In-Exchange premise and compared with the going concern enterprise value and the transaction consideration, as shown in the following table.

As in the first example, the going concern value is greater than the asset values under a Fair Value In-Use premise; therefore, an “intangible gap” exists. Additionally, since the highest and best use of the assets is under a going concern basis and there is no indication of economic obsolescence, the personal property assets are valued under the In-Use premise. The reconciliation of net assets acquired to going concern EV is shown in the following table.

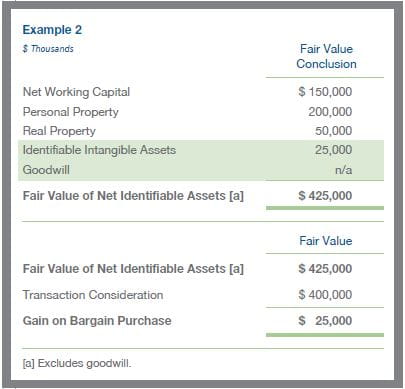

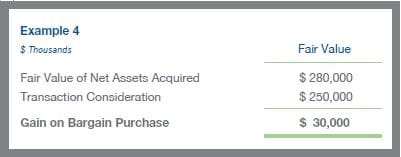

In this example, since the independent business valuation is greater than the consideration paid in the transaction (and there are market indications that the results are reasonable), there is an indication that a bargain purchase transaction has taken place. According to the current purchase accounting standards, the bargain purchase gain is calculated as the difference between the Fair Value of net identifiable assets acquired and the transaction consideration. In other words, goodwill is excluded in the bargain purchase calculation. The bargain purchase calculation is shown in the following table.

Fair Value In-Use > Going Concern Value = Transaction Consideration > Fair Value In-Exchange

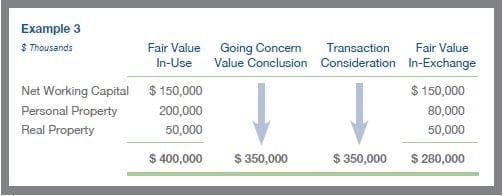

In the following example, assume that the going concern value as determined by the Income Approach and Market Approach of the business equals the total transaction consideration of $350 million. Again, assume that the only tangible assets acquired are net working capital, personal property, and real property. Based on the Fair Value inputs, the implied asset values of the business can be calculated, as shown in the following table.

While the Fair Value In-Use and In-Exchange are the same for net working capital and real property, the Fair Value of the personal property is considerably less under the In-Exchange premise as compared to the In-Use premise. In this example, the going concern value conclusion of the business is between the implied value under a Fair Value In-Use and In-Exchange premise.

Because the going concern value of the operations is less than the implied value under a Fair Value In-Use premise, the presence of economic obsolescence is indicated. Economic obsolescence is often due to underutilization of assets, whereby the owner of the assets cannot earn a rate of return sufficient to support a Fair Value In-Use conclusion. The Fair Value of the personal property assets can be calculated by subtracting the Fair Values of net working capital and real property from the concluded going concern EV, as shown in the following table.

According to the hierarchy of earnings concept, before value can be assigned to intangible assets, the fixed assets must be returning a required rate of return to the investors for these assets. In other words, in order to support any value to intangible assets, the business must be producing excess earnings over and above its fixed asset base. In this example, the business is not producing excess earnings, thus no intangible value would be ascribed. As in the first example, since the going concern value is the highest and best use of the assets and is equal to the transaction consideration, there is no bargain purchase gain.

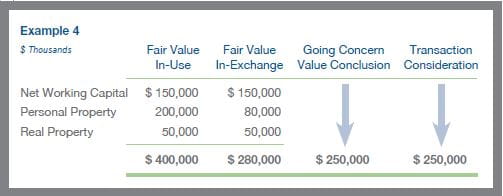

Fair Value In-Use > Fair Value In-Exchange > Going Concern = Transaction Consideration

As in previous examples, the acquired assets are valued under an In-Use and In-Exchange premise and the conclusions are compared to the transaction consideration. Presume within this context that the going concern value is equivalent to the transaction consideration. As shown in the table below, the asset values of the business under the Fair Value In-Use premise are greater than the Fair Value In-Exchange premise and going concern value conclusion (and thus the transaction consideration paid).

In this example, the business is not generating a return on its assets greater than the return required to support the assets valued under the In-Exchange premise. Additionally, the business is not generating excess earnings to support the value of intangible assets. (However, there may be unique circumstances in which intangible assets are recognized; such as a technology that is being licensed and generates royalty income.) Because Fair Value In-Exchange is an estimate of the value of the assets in an orderly liquidation, the fact that the purchase consideration is less than Fair Value In-Exchange indicates that the transaction likely involved a highly motivated seller who was in severe financial duress. As a result, the transaction was likely consummated on a “fire sale” basis (a forced liquidation). It has been generally interpreted that the minimum value conclusion for tangible assets for financial reporting purposes is equal to Fair Value In-Exchange. As a result, the gain on the bargain purchase is calculated by subtracting the assets on an In-Exchange basis from the price paid.

Conclusion

Because the existence of a bargain purchase is expected to be very rare, these types of scenarios typically require significantly more analytical due diligence. For instance, circumstances may arise by which the business may have loss contracts or unfavorable contracts as compared to market, thus negating the existence of a true bargain purchase. In any circumstance, these scenarios are highly complex from a financial reporting perspective. It is critical that these concepts are communicated among the appropriate parties (including the auditors) and debated at the outset of an engagement to ensure a smooth valuation process that results in an answer consistent with the accounting regulations.