English

English

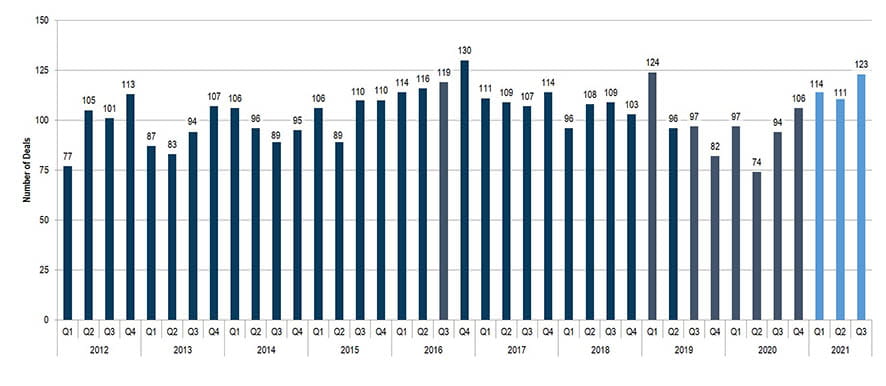

There were 348 plastics industry M&A transactions through the first nine months of 2021, a 31% year-over-year (YOY) increase. Plastics M&A has rebounded significantly since the Q2 2020 trough, with Q3 2021 achieving the highest level of quarterly deal activity since early 2019. M&A activity by private equity firms (both selling and buying) has increased significantly in 2021, accounting for most of the incremental volume for the year. Positive momentum is expected to continue for the rest of the year, with the full year 2021 on track to exceed the volumes achieved in 2016, the highest annual total in Stout’s proprietary database.

There are a number of factors contributing to the strong M&A market. From a buyer’s perspective, there continues to be strong demand from both strategic and financial buyers despite the unprecedented environment. There is significant equity capital available for the acquisition of good quality companies and a strong lending environment with financing sources that are ‘open for business’ throughout the capital structure. From a seller’s perspective, both macro and company-specific drivers have resulted in an increased supply of acquisition candidates in the market. Despite labor, material, chip shortages and other challenges, the financial performance of many companies within the plastics industry has improved, thus better aligning expectations with market valuations. The potential tax law changes introduced in 2021 have also increased the number of sellers in the market.

Key Q3 2021 Themes

- Near record-breaking M&A activity thus far in 2021, largely driven by private equity

- Continued interest in plastics companies across all processes and end markets, particularly in the U.S. market

- Significant pent-up demand from buyers stemming from lower, pandemic-related activity in 2020

- Potential tax law changes in 2022 driving significant M&A activity in 2021

- Overall increased supply of acquisition opportunities (companies going to market in 2021 that were slated to launch in 2020 or 2022)

- Positive momentum heading into Q4 2021 with strong buyer demand and access to capital

- Acquisition financing groups are ‘open for business’ and overall cost of capital continues to be low

- Strong company performance in many plastics sectors, despite labor, material, chip shortages and other challenges

- Continued improvement in key macroeconomic indicators

Stout Proprietary M&A Database Highlights

Buyer and Seller Trends

Hybrid buyer (private equity-owned strategic) activity increased 104% during the first three quarters of 2021, YoY, while financial and strategic buyer activity increased 47% and 2%, respectively. On the sell side, private equity and private seller activity increased 148% and 30%, respectively, YoY, while corporate seller (eg, corporate carveouts) transactions decreased 6%.

End Market Activity

M&A activity within the plastic packaging, medical, and industrial segments increased 105%, 42%, and 5% respectively, YoY, while automotive activity decreased 18%. Within the plastic packaging segment, extrusion and injection molding were particular bright spots, while injection molding saw the highest jump within medical. Medical continues to be one of the most sought-after segments within the plastics industry.

Activity by Process

M&A activity involving seven out of the 10 plastic processes tracked by Stout were flat or up during the first three quarters of 2021. Two of the largest process segments, extrusion and injection molding, both increased 43%, YoY, while thermoforming and distribution also saw significant increases.

Activity by Geography

U.S. domestic M&A activity led the charge during the first three quarters of 2021, increasing 50%, YoY. International M&A activity increased 28%, while cross-border activity decreased 11%, likely driven by Covid-related travel restrictions. Within the U.S. market, plastics M&A activity saw the biggest gains in the plastic packaging and medical end markets, as well as the injection molding, extrusion, thermoforming and rotational molding segments.

PLASTICS M&A VOLUME

QUARTERLY PLASTICS M&A VOLUME

Source: Stout and various sources

Market Trends

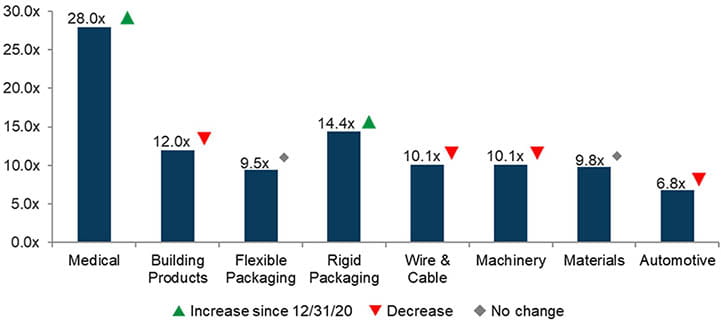

Plastics Industry Multiples

The U.S. stock market continues to perform well since the trough of March 2020, with the Dow, S&P 500 and Nasdaq up 10.6%, 14.7% and 12.1%, respectively, through the first three quarters of 2021. Within the plastics industry, four of eight plastics industry sectors that Stout tracks were up or flat for the first three quarters of 2021, although all segments are generally trading at or near all time highs. From a multiple perspective, Stout’s medical and rigid packaging indices saw the largest increase thus far in 2021.

Commodity Prices

Large price increases for crude oil and natural gas have occurred during the first three quarters of 2021, with crude oil up approximately 55% and natural gas up 136%. Overall, resin prices have generally trended up thus far in 2021, with certain commodity resins seeing the biggest increases, while pricing for engineering grade resins has been generally less volatile.

Macroeconomic Metrics

Key macroeconomic indicators such as GDP, consumer confidence, and unemployment also continue to trend positive, although access to labor and materials continue to be a major challenge for many companies.

EBITDA MULTIPLES (MEAN)

Source: Capital IQ and Proprietary Stout indices

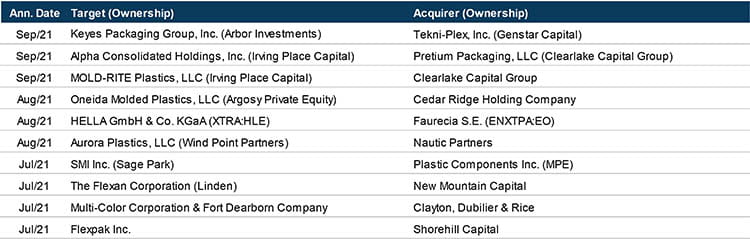

Q3 2021 PLASTICS INDUSTRY TRANSACTION HIGHLIGHTS