English

English

Market Observations

The automotive industry, which was ramping up production to meet post-2020 pandemic demand, faced strong headwinds in the first half of 2021 due to various supply chain constraints, discussed later in this update. These supply issues hurt U.S. auto manufacturing, with GM, Ford, and other OEMs temporarily closing plants or reducing production. Consequently, auto parts manufacturers that feed their supplies to these plants also saw their order books being impacted in 2021. With new car output being hampered, inventories at dealerships have reached historic lows, and strong demand for new cars pushed prices to unprecedented levels.

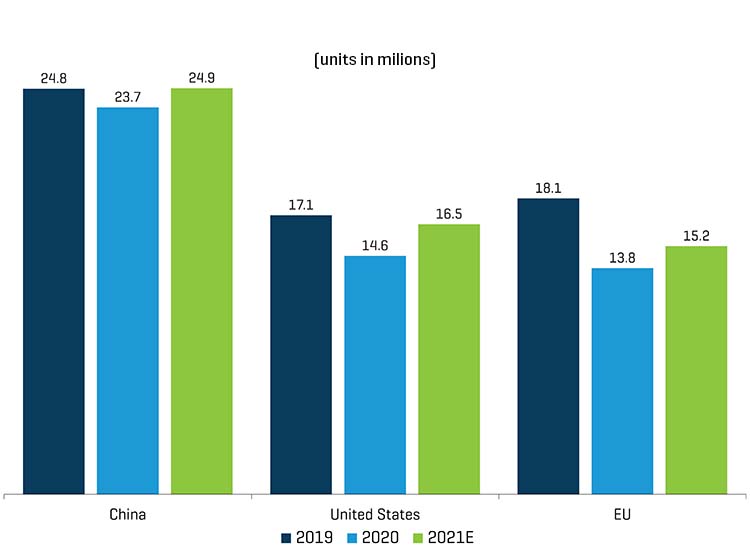

Global Light Vehicle Sales

GLOBAL PASSENGER CAR SALES PRE- AND POST- COVID 19

Source: IHS Markit

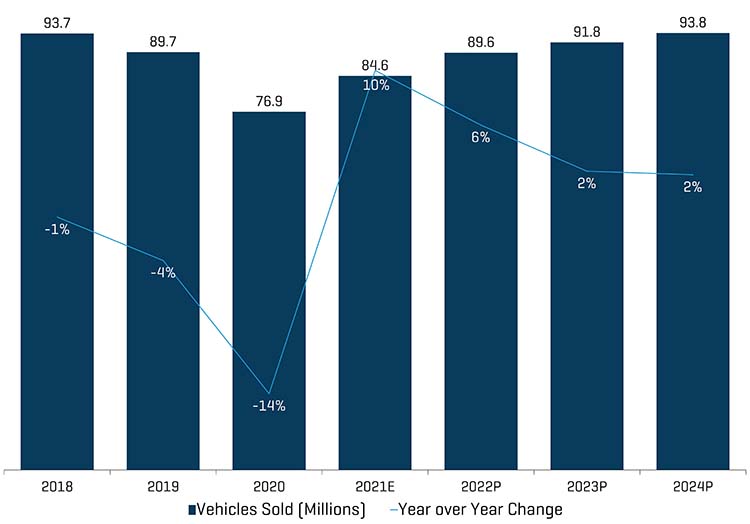

HISTORICAL AND PROJECTED GLOBAL LIGHT VEHICLE SALES

Source: IHS Markit

While demand for vehicles came roaring back in the second half of 2020, automotive suppliers in 2021 are confronted with many operational and supply-side challenges that negatively impact near-term revenue and profitability goals, including:

- Semiconductor Shortage: The automotive industry (accounting for ~10% of global semiconductor sales) was hit hardest by the semiconductor shortage. As auto manufacturers trimmed their orders for semiconductor chips ahead of the COVID-19 lockdowns, chipmakers allocated that capacity to verticals that benefit from the work-from-home environment (e.g., computer and smartphone industries). When auto sales began to rebound in the second half of 2020, supplies of automotive chips quickly began running low. The Taiwan drought, power failures in early 2021 following the Texas freeze, and a Japanese plant fire further exacerbated automotive chip shortages.

In the near term, semiconductor manufacturers are increasing capacity utilization, and automotive OEMs/suppliers are entering into long-term agreements and partnerships with chipmakers to improve order visibility and secure supply. In the medium term, semiconductor manufacturers are expanding global capacity with new plants announced and/or under construction.

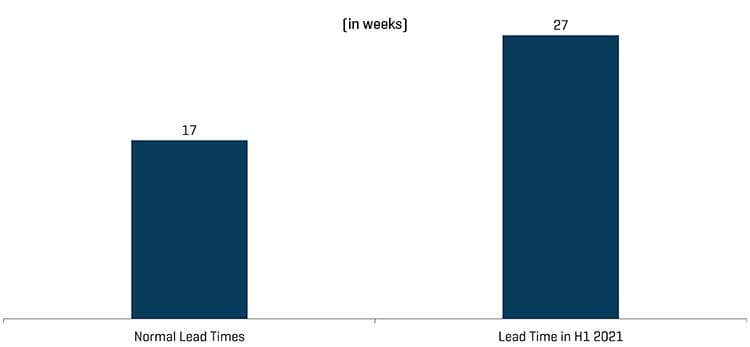

Automotive Semiconductor Trends

AUTOMOTIVE SEMICONDUCTOR LEAD TIMES

Source: IHS Markit

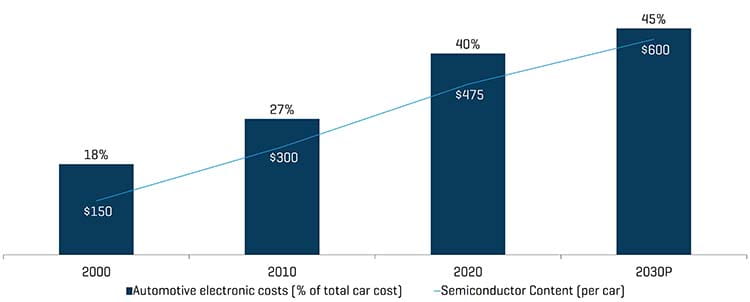

GROWING ELECTRONICS AND SEMICONDUCTOR CONTENT PER VEHICLE

Source: IHS Markit

- Soaring Steel Prices: Steel experienced a drastic resurgence in demand after COVID-19 lockdowns were lifted, with elevated prices reaching all-time highs in mid-2021. Rising domestic steel prices have pushed U.S. firms to import steel from overseas despite the 25%+ import tariffs and additional shipping costs. Industry experts expect the steel price rally to lose steam in late 2021 as steel mills add capacity and imports gradually reach U.S. shores.

- Container Shortage and Congested Ports: The increase in post-lockdown trade volumes choked up shipping terminals and led to congested sea routes, shipping delays, and stockpiling at ports. China, which recovered first from the COVID-19 impact, started opening trade routes but then faced challenges in bringing empty containers back from Western countries still under lockdowns. The auto industry continues to see delays sourcing raw materials and components, such as rubber, plastics, and seating foam, from Asian countries. The global pool of containers is forecasted to increase almost 6% in 2021, nearly double the projected annual increases from 2022 to 2025. Further, industry leaders expect added relief in 2022 as trade between countries normalizes.

Despite recent supply chain challenges temporarily impacting automotive sales and operational trends, the industry’s long-term demand profile remains intact. While supply-side challenges are likely to persist into 2022, IHS is forecasting sequential global production improvement starting in Q4’21 with year-over-year improvement starting modestly in Q2’22.

Automotive Production Trends

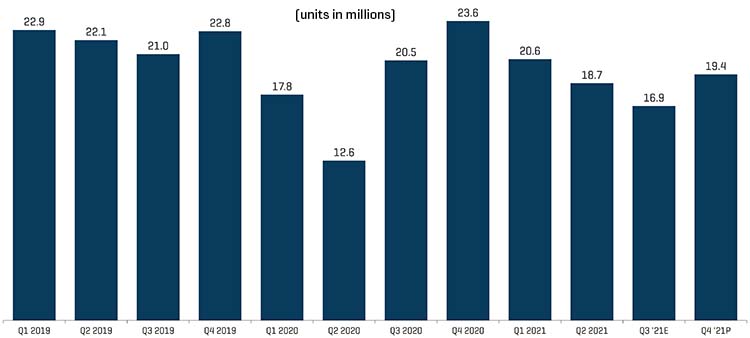

QUARTERLY GLOBAL LIGHT VEHICLE PRODUCTION

Source: IHS Markit

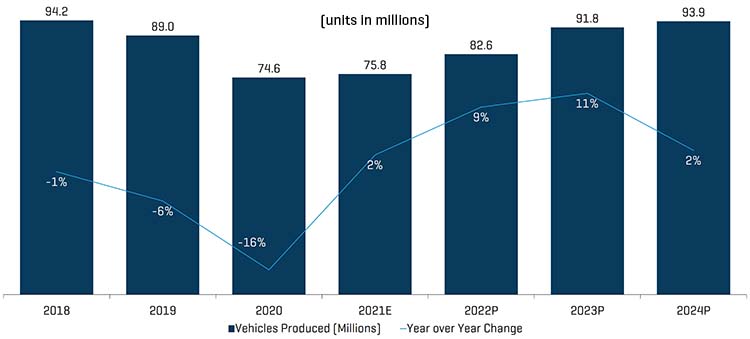

HISTORICAL AND PROJECTED GLOBAL LIGHT VEHICLE PRODUCTION

Source: IHS Markit

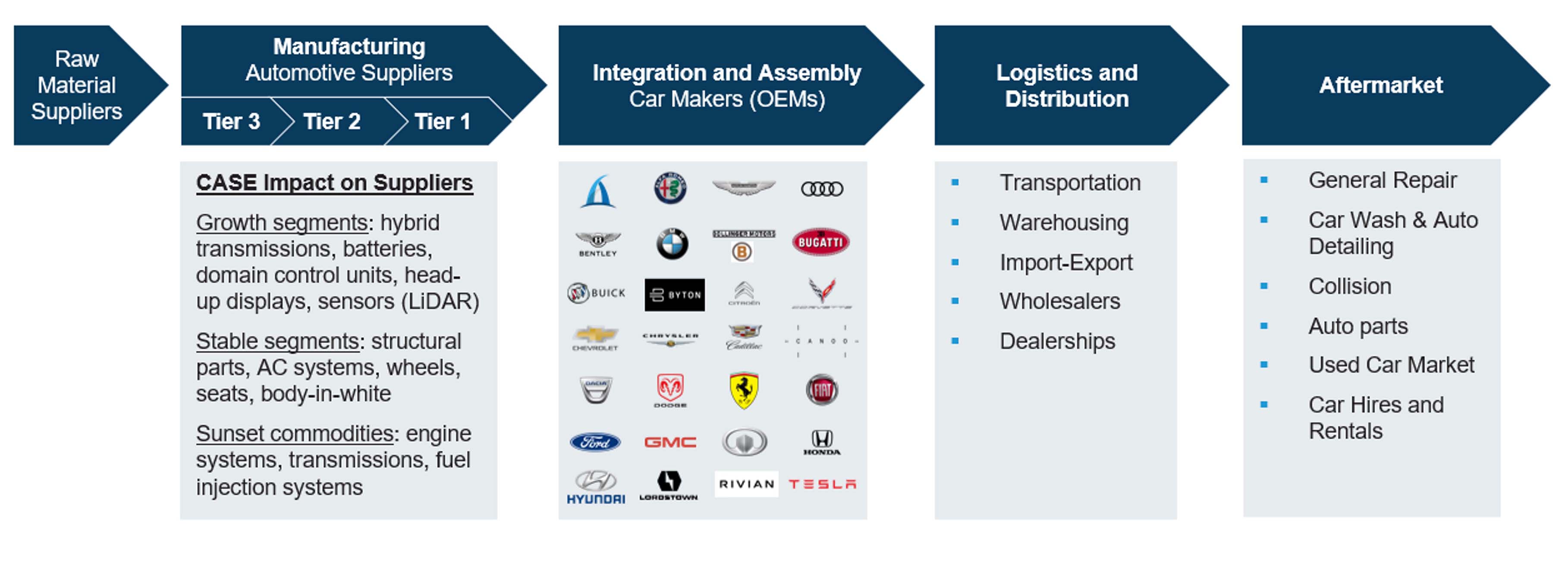

Automotive Supply Chain Evolution

Over the next decade, the automotive industry will face a magnitude of change driven primarily by four mutually reinforcing trends: Connected, Autonomous, Shared, and Electric (“CASE”). These trends are enabled by the advancement of technology in electronics and software and will result in different user behaviors and mobility preferences, shifting value pools across the supply chain, innovative business models, and new entrants into automotive. Neither OEMs nor traditional suppliers are fully positioned to define the software and technology requirements of these new systems. As such, increased collaboration between OEMs and suppliers is expected to become not just more prevalent but necessary. Auto OEMs and suppliers will see new business models and changing supply chain ecosystems with emerging competition from new entrants. M&A will become increasingly important to fill gaps in capabilities to allow suppliers to deliver complete and fully functional systems.

M&A Update

The challenges due to COVID-19 across the automotive sector caused softness in M&A during the second quarter of 2020 as OEMs, suppliers, and retailers adapted their businesses to the pandemic (e.g., temporary shutdowns, cost cutting, government programs, etc.). M&A quickly picked up in the second half of 2020; however, macroeconomic headwinds have plagued the industry in 2021 with increasing commodity costs and the supply chain disruptions discussed previously.

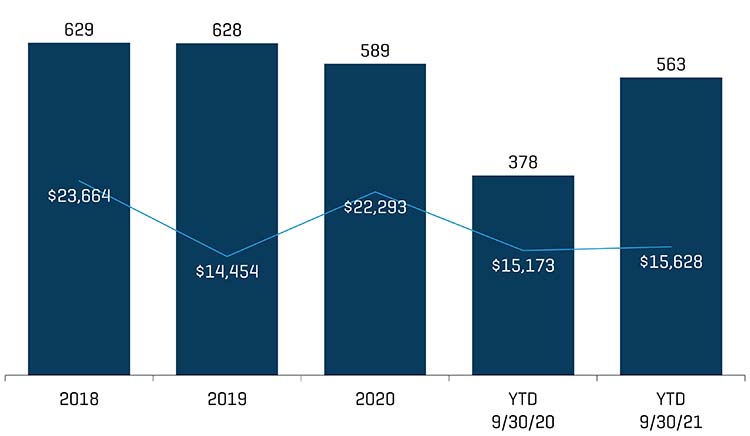

Automotive M&A Activity

AUTOMOTIVE DEALS (ANNUAL AND YTD)

Source: Capital IQ (represents announced and closed deals - excludes deals with EV below $50 million and above $1 billion)

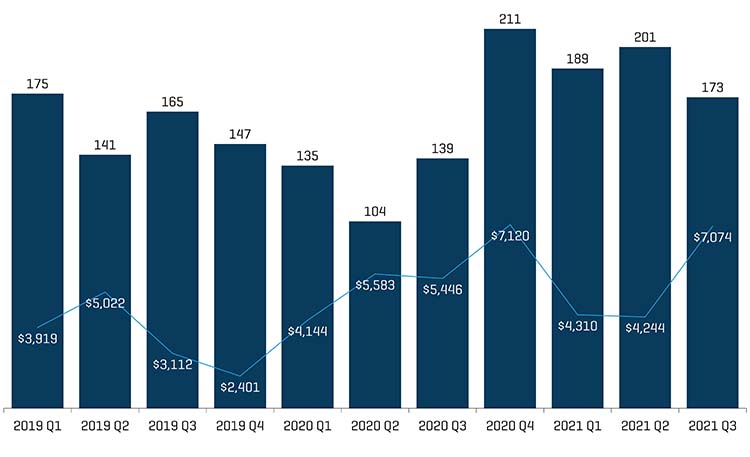

AUTOMOTIVE DEALS (QUARTERLY)

Source: Capital IQ (represents announced and closed deals - excludes deals with EV below $50 million and above $1 billion)

Whether an automotive supplier finds itself in a healthy or challenged post-COVID environment, M&A and restructuring activity over the next 24 months could be imperative in positioning suppliers for longer-term success. Innovative suppliers seeking growth in areas like electric vehicles (“EVs”) will need to continue to invest in forward-looking technologies. Such suppliers may supplement M&A activity with partnerships that accelerate technology development. Additionally, suppliers might need to divest certain growth areas that are difficult to fund, areas where they lack the current development capabilities, or areas that they no longer feel are the right long-term strategic fit as the vehicular landscape transforms.

Public Market Performance (market data as of September 30, 2021)

Public trading multiples have returned to more normalized levels after spiking in 2020 due to COVID-19 and supply-chain-related issues temporarily burdening profitability, with valuations at the time anticipating a market recovery.

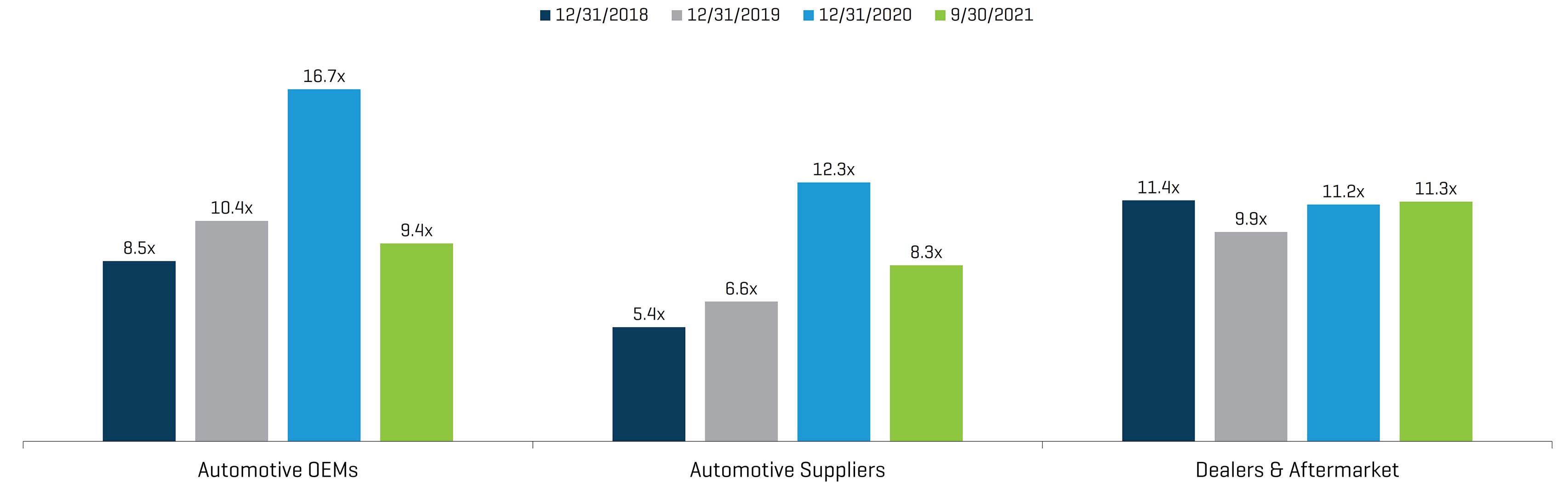

HISTORICAL TEV/ EBITDA BY SEGMENT

Source: Capital IQ

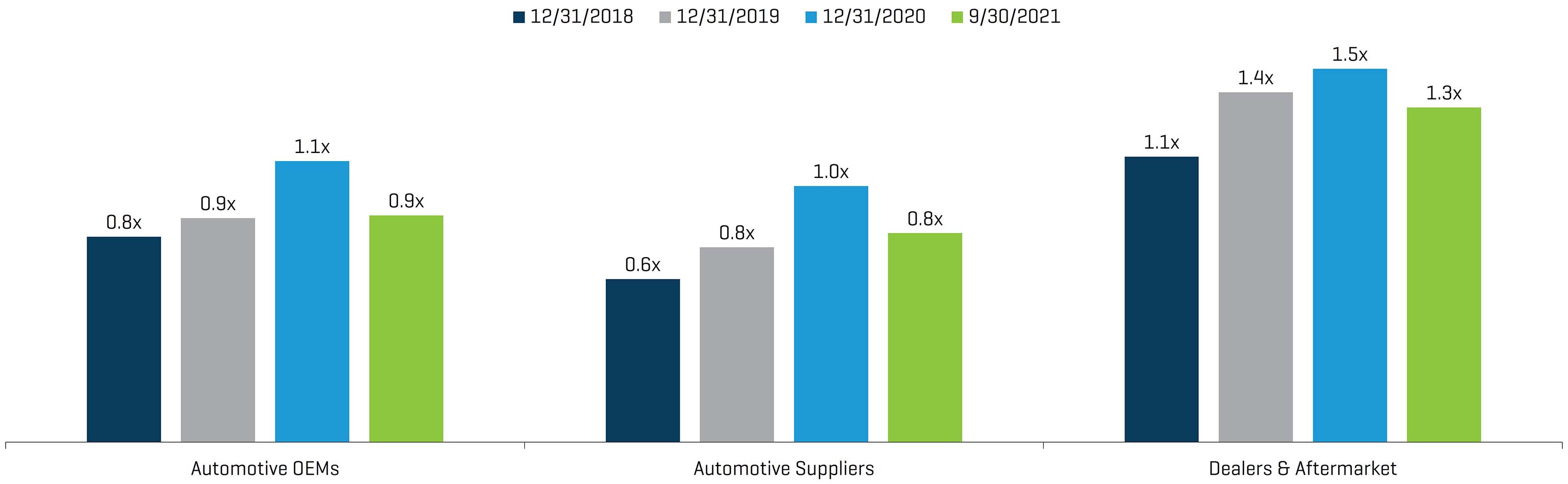

HISTORICAL TEV/ REVENUE BY SEGMENT

Source: Capital IQ

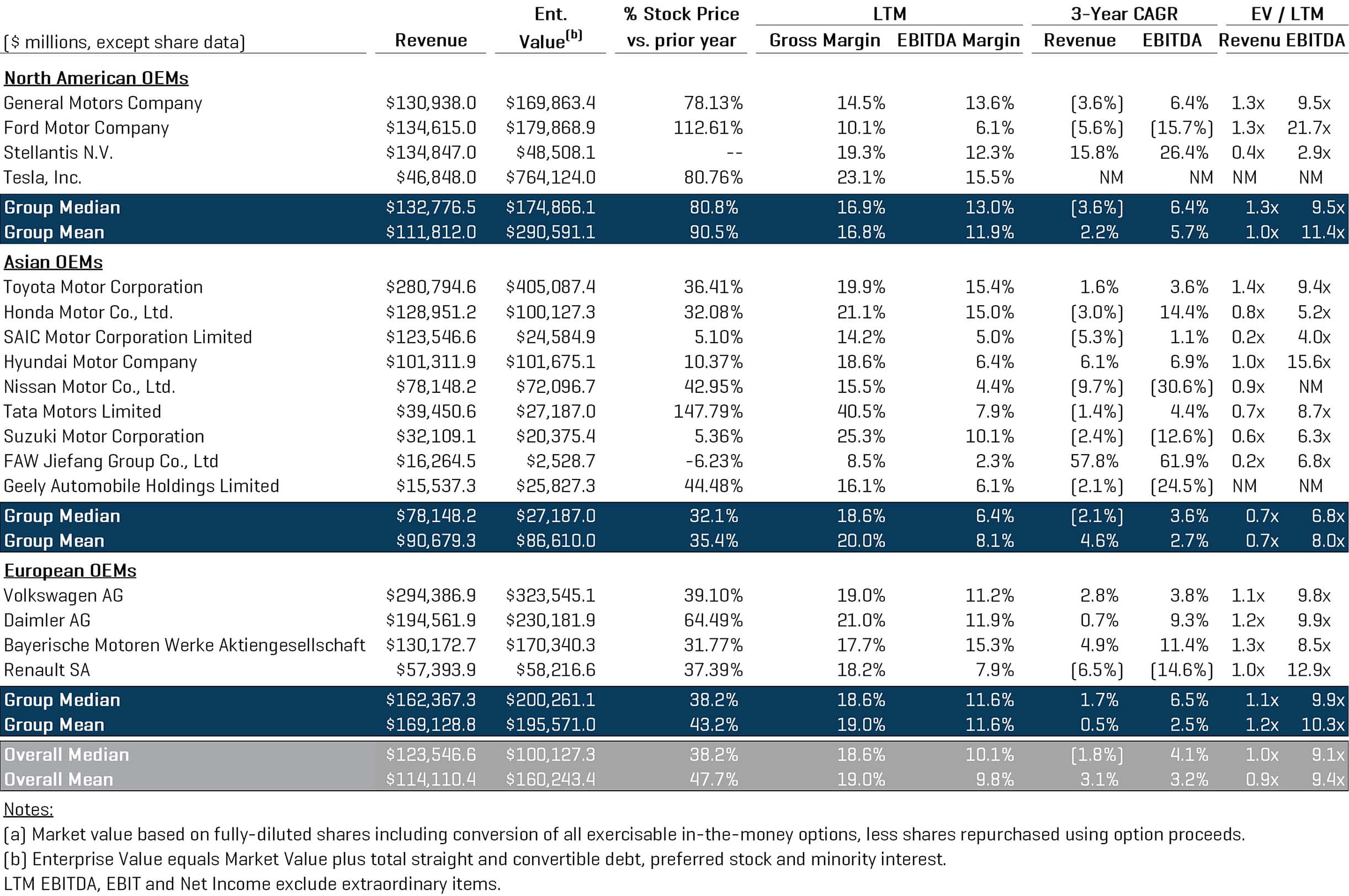

Automotive OEMs

Source: Capital IQ

Automotive Suppliers

Source: Capital IQ

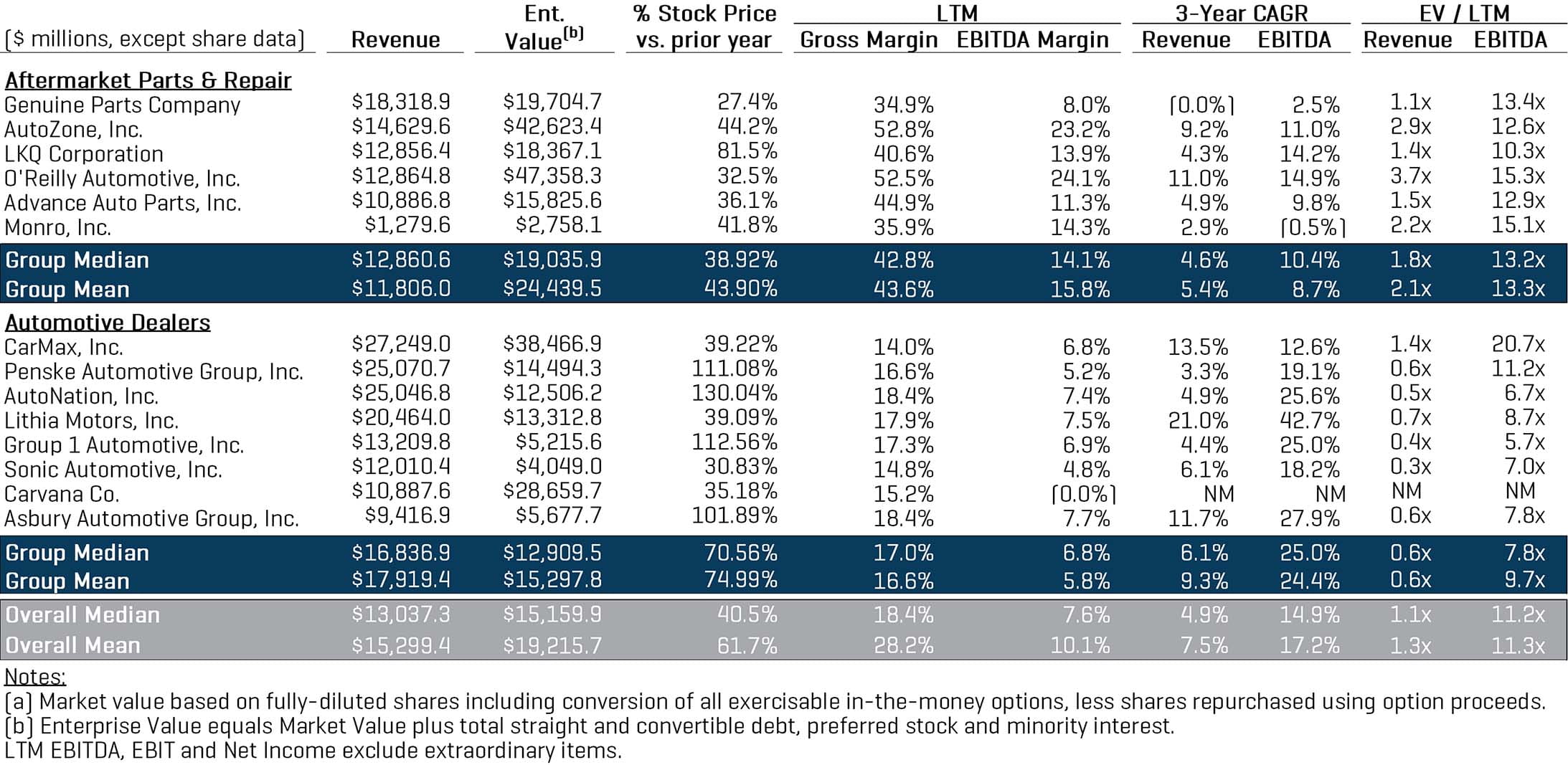

Automotive Dealers & Aftermarket

Source: Capital IQ

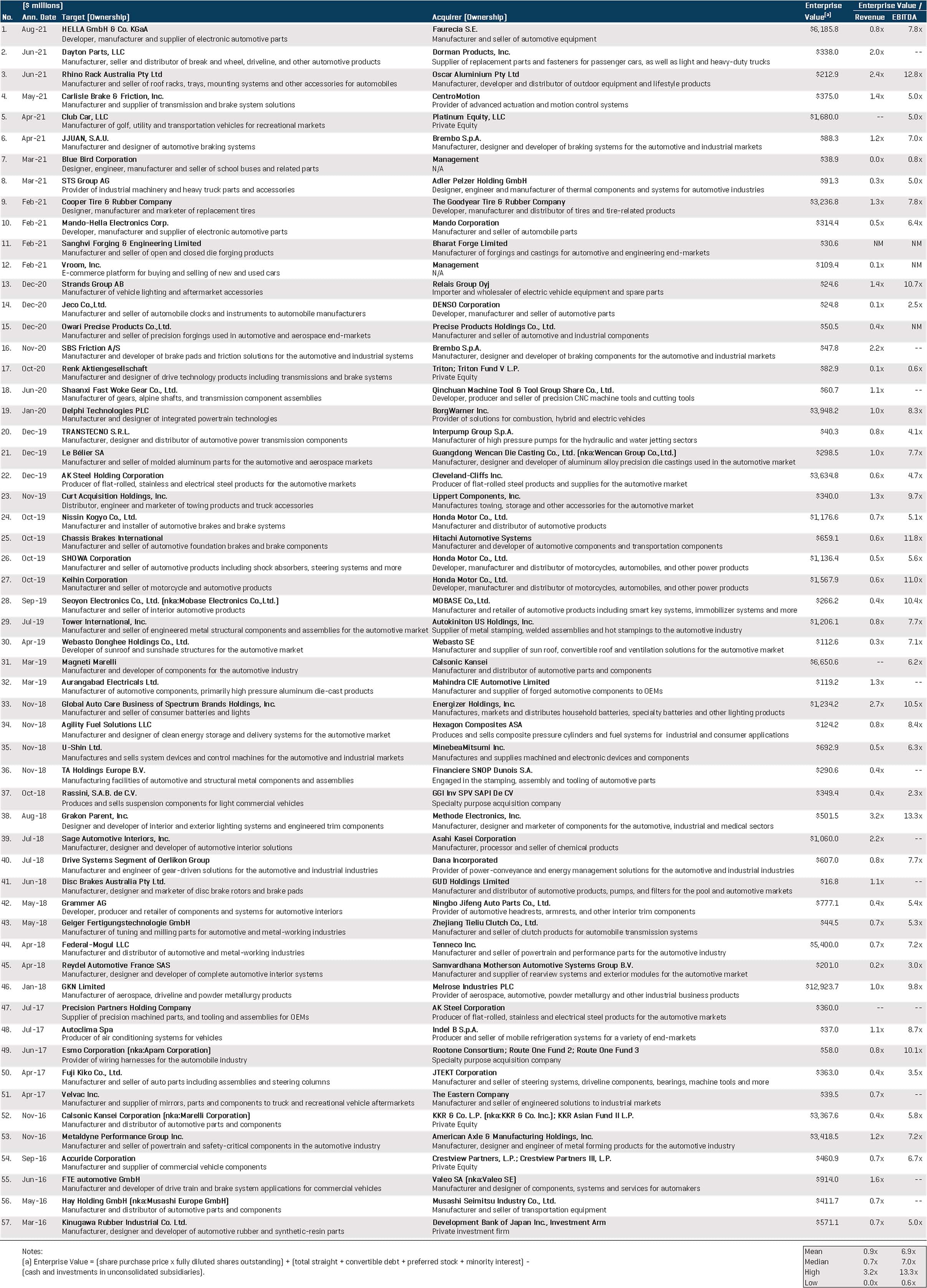

Recent Transaction Comparables