English

English

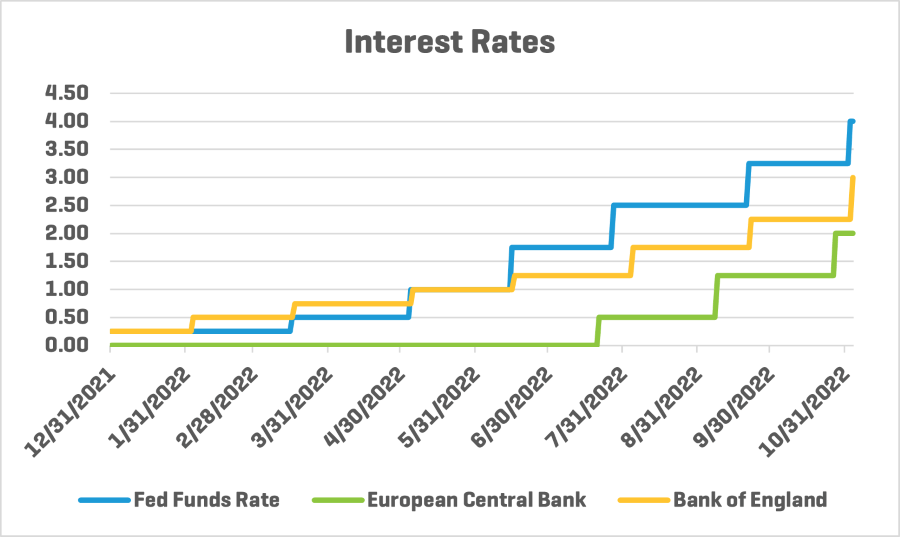

Central banks around the world have increased their prime rates significantly since January as they try to combat rising inflation. The U.S. Fed Funds Rate (“FFR”), the rate at which banks lend funds to one another (typically on an overnight basis), has increased from 0.25% as of January 1 to 4.00% as of the beginning of November. The London Inter-Bank Offer Rate (“LIBOR”, from 0.25% to 2.25%), and its successor the Secured Overnight Financing Rate (“SOFR”), as well as the European Central Bank (0.00% to 2.00%), have all increased since the beginning of the year. And there may be future interest rate hikes to come.

As companies think through the consequences of an increasing interest rate environment, one of the considerations for those companies that utilize International Financial Reporting Standards (“IFRS”) is around impairments of their non-financial assets. Under the guidance in IAS 36, market interest rates that are likely to affect the discount rate used to calculate an asset’s Value-in-Use (“VIU”) indications such that the assets recoverable amount decreases materially is considered to be an impairment indicator.

As companies are taking a closer look and assessing their non-financial assets, it is a good time for the companies to also perform the requirements under IAS 16. Under IAS 16, companies are required to review the remaining useful life, depreciation (amortization) method, and residual value of the corresponding assets at least annually. As a reminder, a change in the useful life, deprecation (amortization) method, and residual value are considered a change in accounting estimates under IAS 8. As such, any changes would only be treated prospectively.

Finally, companies will need to remain vigilant in their assessment of impairment indicators, as a decrease in interest rates could result in a reversal of the impairment that was recognized, as IFRS requires a company to assess whether the impairment should be reversed as well.