English

English

Physician practices have been acquired in record numbers in recent years. Whether from a private equity sponsor, local health system, or another independent practice, most physician owners will receive offers to acquire their practice. Understanding the current M&A environment and how the value is determined will benefit these practice owners.

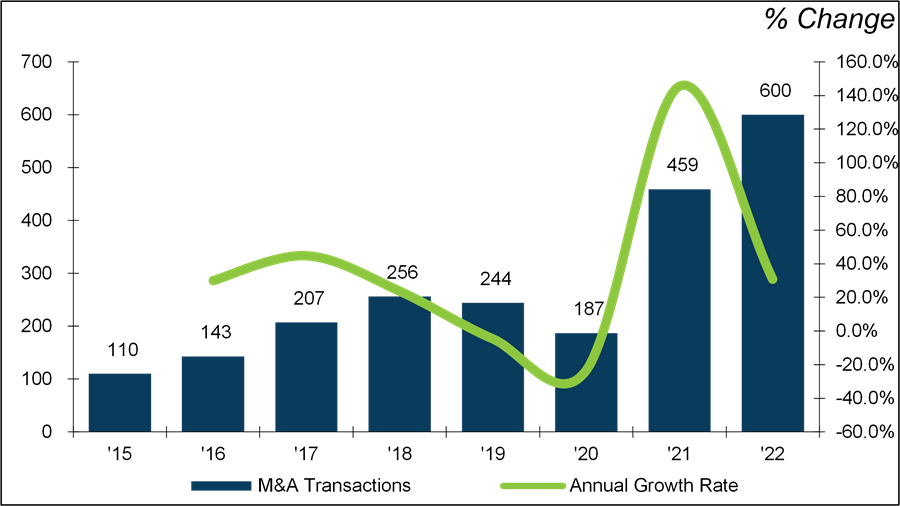

According to data from Irving Levin Associates, Inc. (“Irving Levin”), practice sales more than doubled between 2015 and 2019, increasing from 110 announced transactions in 2015 to 244 in 2019. While M&A activity was initially adversely impacted by the COVID-19 pandemic in 2020, total deal volume remained strong despite the prevailing economic uncertainty and negative operational and cash flow impacts caused by the pandemic. As restrictions eased and the economy reopened, deal volume rebounded in the second half of 2020, resulting in 187 total transactions for the year.1

Physician Medical Groups - M&A Transactions

M&A activity ramped up significantly to 459 transactions in 2021 and 600 in 2022.2 Transaction volumes in 2021 and 2022 benefited from the closing of deals that had been put on hold during the pandemic and from sellers motivated to close a deal ahead of a potential capital gains tax rate increase.3 Leading the acquisition charge are private equity sponsors looking to consolidate a fragmented market and strategic buyers such as health systems and large independent practices.

Strategic buyers, particularly health systems, are motivated to acquire practices to increase patient volumes and market share as well as to enhance negotiating power with payors. Private equity buyers often pursue a platform strategy – first acquiring a larger practice and growing it through a series of “bolt-on” acquisitions of smaller practices at favorable multiples. Practice platforms are able to improve profit margins by consolidating back-office functions (e.g., human resources, revenue cycle, accounting, and IT), streamlining operations, and negotiating improved reimbursement with payors as scale is achieved. Equity sponsors will typically hold a platform for three to seven years before exiting through a sale to a new buyer.

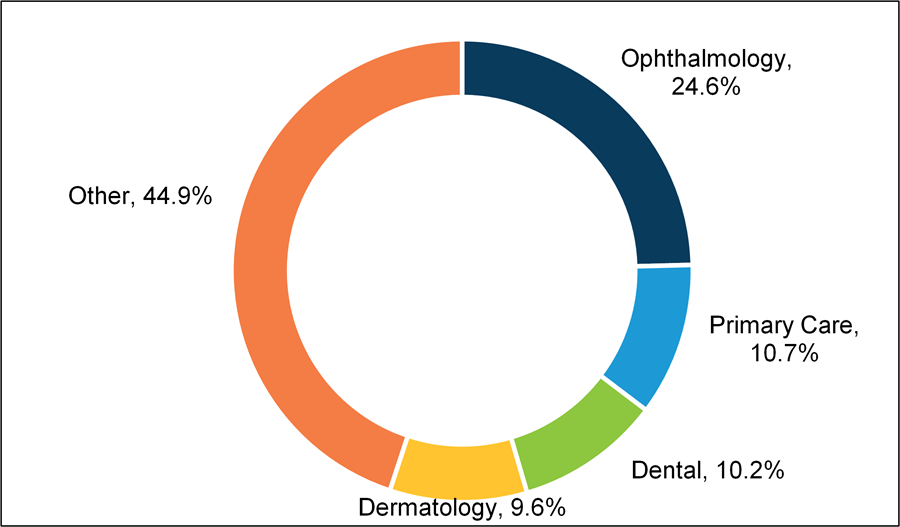

2020 M&A Transactions by Specialty

Private equity transactions dominated deal activity in recent years. Irving Levin Associates, Inc. reported that private equity buyers represented approximately 77% and 72% of total announced deals in 2019 and 2020, respectively, which represents a significant increase from 34% of announced deals in 2016. Ophthalmology practices were the most targeted specialty in 2020, followed by primary care groups, dental practices and support organizations, and dermatology practices.4 Another study that analyzed 355 physician practice acquisitions by private equity investors between 2013 and 2016 determined that the most popular specialties were anesthesiology (19.4%), multi-specialty (19.4%), emergency medicine (12.1%), family practice (11.1%), and dermatology (9.9%). Other attractive specialties include orthopedics, gastroenterology, urology, and ophthalmology practices, which are desirable due to their ancillary service revenue streams from ambulatory surgery centers, labs, and diagnostic imaging.5 The following table presents select notable M&A transactions involving physician groups in recent years.

Select Physician Practice M&A Transactions

Selling to either a strategic or financial buyer can be an attractive option for physicians. A sale allows a physician to focus on the practice of medicine while leaving the business operations to others. Sales to health systems are typically structured as an asset sale of 100% of the practice’s assets. Private equity transactions can be structured as stock or asset sales but usually involve the seller “rolling over” a portion (typically 10% to 40%) of their equity in the target practice into new equity in the acquiring entity. Rollover equity incentivizes the seller to remain focused on the continued success of the practice and allows the physician to participate in a subsequent sale when the sponsor ultimately exits the platform.

Practice acquisitions will continue for the foreseeable future. As physician owners contemplate their strategic options, it is useful for doctors to have a basic understanding of how potential buyers may assess the value of their practices.

Valuation Considerations

Practice valuations are typically performed under a Fair Market Value standard. Fair Market Value is commonly defined as the value in an arm’s-length transaction, consistent with the general market value of the subject transaction. General market value means the price that an asset would bring on the date of acquisition of the asset as the result of bona fide bargaining between a well-informed buyer and seller that are not otherwise in a position to generate business for each other.6 Acquirers may need to ensure that the price paid to acquire a physician practice is consistent with Fair Market Value to remain compliant with healthcare regulations such as the Stark Laws and the Anti-Kickback statute.

Fair Market Value differs from Investment Value. Investment Value contemplates a level of value that can only be achieved by strategic buyers and may take into account possible economic benefits from expense reductions or revenue/profit enhancements. Both Fair Market Value and Investment Value can consider “normalizing adjustments” (e.g., removal of one-time income / expense items, gains and losses, adjustments to compensation to a market level, etc.); however, Fair Market Value appraisals do not consider any buyer-specific or strategic control adjustments and enhancements.

Valuation theory includes three approaches or techniques for valuing a business like a physician practice: the Income Approach, the Market Approach, and the Asset Approach. The approach(es) used to value the practice will vary depending on whether or not the practice is expected to generate a positive economic return for its physician owners after paying all necessary operating expenses, including market compensation to the physicians. Practices expected to generate a positive economic return are typically valued under a combination of the Income and Market Approaches. Large practices with strong patient volumes and/or ancillary revenue streams (lab, diagnostic imaging, physical therapy, etc.) generally fall into this category. Practices that do not achieve patient volumes necessary to be profitable are commonly valued under an Asset Approach.

Income Approach

The Income Approach is based on the financial theory that the value of a physician practice is equal to the present value of its projected future free cash flows discounted at an appropriate risk-adjusted rate of return. Two common forms of the Income Approach are the Capitalized Cash Flow Method, a single-period capitalization methodology, and the Discounted Cash Flow (“DCF”) Method, a multiple-period discounting methodology. While both methodologies can be appropriate, buyers commonly rely on the DCF Method because it has the flexibility to explicitly incorporate anticipated changes in projected financial performance (e.g., changes in the number of providers, patient volume, reimbursement rates, etc.) over time.

The reliability of the DCF Method is dependent on the quality of the underlying assumptions in the projected cash flows. Key assumptions such as revenue growth and projected margins should be supportable in terms of the past performance as well as relevant market and industry data. Further, the forecasted cash flows should be adjusted to reflect any planned changes in the practice operations post-transaction, such as new compensation models that a buyer may put in place. Physician owners often structure their compensation in a manner designed to minimize taxable income by including any practice profits in owner’s compensation. To arrive at an accurate valuation, it may be necessary to restate owners’ compensation to a market level consistent with the buyer’s planned structure.

Private equity platforms commonly structure physician compensation as a certain percentage of collections, while hospitals may compensate physicians based on a production metric (e.g., wRVUs) or a fixed salary. Failing to align the projected compensation with the post-transaction structure could result in under-valuing (or over-valuing) the practice. For example, if a buyer plans to reduce physician compensation from historical levels, projected profits and cash flows will increase, which in turn raises the valuation. Similarly, normalization adjustments or “add-backs” should be made for any owner’s perquisites (e.g., personal car, country club dues, related-party rent) that may not continue post-transaction.

Market Approach

The Market Approach consists of two principal methodologies, the Guideline Public Company (“GPC”) Method and the Merger and Acquisition (“M&A”) Method. The GPC Method determines the value of a company based on a comparison to similar publicly traded companies (i.e., guideline companies). The M&A Method determines the value of a company based on a comparison to similar companies that have been the target of merger or acquisition transactions. After analyzing the risk and return characteristics of the comparable public companies and/or the target companies relative to the subject practice, appropriate valuation multiples are applied to the operating results (e.g., revenue, EBITDA, etc.) of the subject practice in order to develop indications of value.

The Market Approach is appealing due to its simplicity and because the valuation multiples used in this approach are based on observable, arm’s-length market transactions. A limitation of this approach is that it cannot explicitly reflect anticipated future operational changes in the same manner as a multi-period model (e.g., the DCF Method).

Many private equity buyers will express their purchase offers as a multiple of a practice’s adjusted EBITDA even if a more detailed analysis like the DCF Method was performed to support the valuation. While details of prior practice transactions can be difficult to obtain, understanding a range of reasonable multiples for differing practice specialties is beneficial in assessing the reasonableness of an offer.

Asset Approach

For physician practices that are not expected to generate positive cash flows, application of the Income Approach and Market Approach may result in a value below that of the market value of the practice’s net assets. A practice’s value cannot fall below this threshold, as its component assets could theoretically be sold off for their market value and the proceeds used to repay liabilities. In the Adjusted Book Value Method, a common form of the Asset Approach, the market value of each balance sheet asset is determined, including the value of any off-balance sheet assets (e.g., accounts receivable if cash basis accounting is used), and then netted against the market value of liabilities. It may be necessary to commission real and personal property appraisers if the practice has substantial tangible assets to ensure that the analysis reflects the market value of these assets.

Conclusion

Physician practice M&A activity should remain strong over the next several years. Understanding valuation concepts is important for physician owners evaluating a potential transaction, and engaging a valuation consultant to perform a current valuation of the practice can be a beneficial input for owners as they navigate the sale process.

- The Health Care Services Acquisition Report, 27th ed., Irving Levin Associates, Inc., 2021.

- The Health Care Services Acquisition Report, 27th ed., Irving Levin Associates, Inc., 2021 and various press releases.

- Calcagnini, John. Healthcare & Life Sciences Industry Update - Q4 2021. Stout.

- The Health Care Services Acquisition Report, 27th ed., Irving Levin Associates, Inc., 2021.

- Zhu, Jane M., MD, MPP, MSHP. Private Equity Acquisitions of Physician Medical Groups Across Specialties, 2013-2016. February 18, 2020.

- 42 CFR ß411.351 (2020)