English

English

Public and large private companies with international operations face a range of challenges regarding international tax planning and reporting. In our experience with advising CFOs and tax directors on valuation issues related to international tax initiatives, businesses are finding increasingly sophisticated ways to move capital across borders in the most tax-efficient manner in order to achieve a wide variety of business and tax objectives. Having business operations in different domiciles will inevitably generate various levels of cash flow and require different levels of investment. In many cases, companies transfer capital, cash or otherwise, between different international legal entities through the purchase or sale of securities. In particular, we have found that preferred stock is a useful tool for public and large private company tax planning initiatives given its inherent flexibility in structuring between debt- and equity-like features. Businesses seeking to facilitate the movement of assets between legal entities can use preferred stock as an adaptable tool to achieve a wide range of economic outcomes.

Representative Case Studies

The following case studies illustrate two examples of how we’ve helped our clients value preferred stock for international tax planning purposes, which can ultimately be used to set the transaction price and satisfy relevant regulatory requirements.

Case Study #1

- A $20B publicly traded manufacturer (“ABC Co.”) with global operations maintained an Asian legal entity that recently divested a non-core business unit.

- As a result, the Asian entity accumulated a cash balance of approximately $1B.

- At this time, ABC Co. was reducing its investment in Asia and increasing its investment in Europe.

- ABC Co. also maintained a European entity that owned an existing preferred stock interest in a North American entity.

- To facilitate the movement of the Asian entity’s cash balance to Europe where it could be deployed in accordance with ABC Co.’s investment strategy, ABC Co.’s tax team proposed a transaction in which the Asian entity would purchase the European entity’s preferred stock in the North American entity.

- The preferred stock in the North American entity was valued at $800M, allowing ABC Co.’s Asian entity to purchase the preferred stock and transfer its cash balance to a geography in which it intended to invest the capital.

Case Study #2

- A $5B publicly traded manufacturer (“XYZ Co.”) with global operations was seeking to ramp up investment in a new manufacturing facility in South America.

- The company’s North American operations held most of XYZ Co.’s excess cash available for investment.

- To fund the initial build-out of the facility, a North American entity of XYZ Co. purchased a new preferred stock instrument in the South American entity, which was structured to allow for additional follow-on issuances of preferred stock to facilitate further investment.

- Senior tax leadership at XYZ Co. structured a preferred stock instrument that achieved certain key economic objectives and we ultimately opined on the value of the preferred stock for tax reporting requirements.

The rest of this article explores (i) the various structural features of preferred stock that can be tailored to fit specific situations and (ii) some of the approaches taken in analyzing and valuing preferred stock.

Preferred Stock Features

Preferred stock is a class of ownership that is generally senior to common equity ownership and junior to senior and subordinated debt. Certain structural features associated with preferred stock are outlined in the following bullets. Each of these features can be included or excluded, adjusted, or modified to achieve the desired tax outcome.

- Liquidation Preference: If the business entity is liquidated or sold, the owners of preferred stock may receive a return of their capital contributions before the entity’s common stock owners receive any proceeds.

- Accrued Dividends: Dividends may accrue on preferred stock capital contributions at a pre-determined annual rate.

- Dividend Payment Flexibility: Dividends may be mandatorily payable in cash at a stated amount or may be payable based on a percentage of available cash flow.

- Cumulative vs. Non-cumulative: Stated dividends that are not paid on time or not paid at the stated rate may either accumulate or be permanently lost by shareholders.

- Participating Preferred: After receiving repayment of their capital contribution in accordance with the preferred liquidation preference, preferred stock owners are entitled to a pro rata portion of the residual equity of the business pari passu with the entity’s common stock owners.

- Convertible Preferred: Preferred stock owners may have the right to convert their shares into common stock at specified levels of value.

- Voting Rights: Preferred shares may be voting or non-voting.

- Callable vs. Putable: The issuer of preferred shares may call back the shares at specific prices or upon the occurrence of certain events; likewise, the owners of preferred shares may put their shares back to the company under various circumstances.

Although many of these features add to the complexity of preferred stock, the simplest form of preferred stock is a cumulative, dividend-paying instrument with no incremental common equity participation, conversion features, or other similar rights. In this instance, the risk and return characteristics of preferred stock are analogous to those of a bond. In assessing the value of this type of security, we would primarily rely on traditional fixed income pricing techniques, including procedures such as (i) analyzing the overall credit quality of the issuer, (ii) assigning an appropriate credit rating, (iii) determining a market yield applicable to the issuer and preferred stock, and (iv) discounting the future expected cash flows according to the calculated risk-adjusted rate of return to determine the value of the instrument. The following paragraphs outline our process in pricing the preferred stock in connection with corporate tax planning initiatives.

Analyzing Preferred Stock Yields

Analyzing the market yield applicable to preferred stock is the most critical component of the analysis described previously and is similar to the process for analyzing the market interest rate on a senior debt instrument. The first step is to evaluate the credit quality of the issuer and determine an appropriate credit rating. In general, preferred stock is rated two notches below a company’s investment-grade senior unsecured debt and three or more notches below non-investment grade senior unsecured debt. To determine an issuer’s credit rating, we generally apply the same techniques that global ratings agencies use in determining corporate credit ratings, which requires an analysis of a universe of public companies in the U.S. with rated debt.1

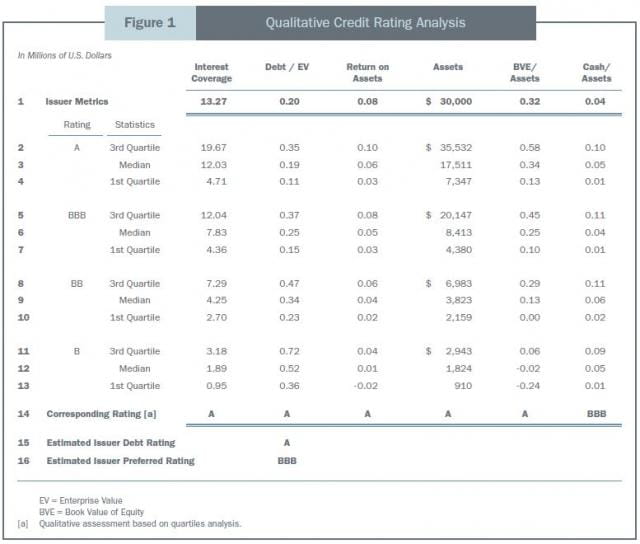

- The first approach is a qualitative analysis that compares certain credit metrics of the issuer with those of the public company universe and determines a credit rating for the issuer based on its relative credit profile.

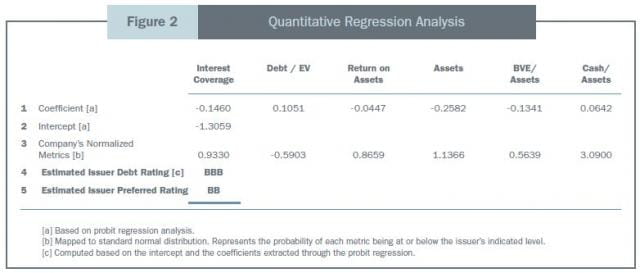

- The second approach is a quantitative analysis that uses probit regression analysis to construct a credit rating model, which is then applied to the issuer based on relevant credit metrics.

Qualitative Approach

We consider a variety of metrics when analyzing a company’s credit rating. Specifically, in order to determine which sample of financial metrics to include in our analysis, we consider using statistical techniques to test whether or not a wide range of financial indicators are significant. The following representative example in Figure 1 illustrates the credit metrics we’ve determined to be relevant for inclusion in this analysis: interest coverage (i.e., EBIT divided by interest expense), leverage (i.e., total debt divided by enterprise value), return on assets (i.e., net income divided by total assets), total assets, book value of equity divided by total assets, and cash and cash equivalents divided by total assets. First, we calculated these metrics for the public company universe, as well as for a hypothetical preferred stock issuer. We then selected credit ratings applicable to the issuer for each metric and qualitatively determined an overall rating based on the indicated results.

Quantitative Approach

We also implemented a probit regression analysis using the same set of metrics for the issuer and the public company universe. Specifically, we used the credit metrics as the dependent variables and the known ratings of the public companies (which are associated with an empirical probability of default) as the independent variables. In applying this model, we mapped the issuer’s credit metrics to the standard normal distribution of credit metrics for the public company universe, to analyze the probability of a given metric being at or below the issuer’s indicated levels, which resulted in the ‘normalized metrics’ in Figure 2. We then applied the resulting coefficients and intercept of the regression analysis to estimate a probability of default for the hypothetical issuer, which was used to conclude on the corresponding credit rating.

Analysis of Historical Preferred Stock Yields

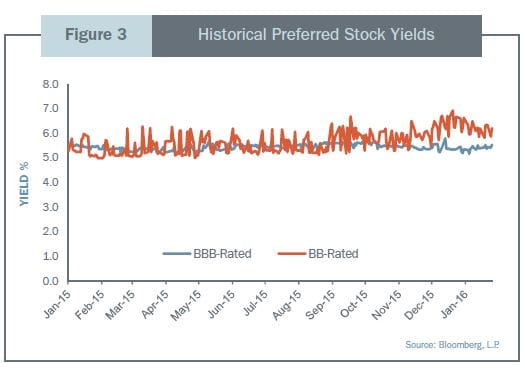

As Figure 3 shows, preferred stock yields have remained relatively flat at higher ratings levels (i.e., BBB and above), but have increased at lower ratings levels (i.e., BB and below) over the last year.

If we were to opine on a market yield applicable to the preferred stock of the hypothetical issuer, we would likely conclude on a range of 5.5% to 6.5% based on the yields on preferred securities with credit ratings of BB to BBB. As previously outlined, preferred stock may also maintain junior equity participation rights or conversion features that need to be considered in connection with valuing the fixed income component. Such cases often require a valuation of the business enterprise, in which we typically consider various closed form and flexible option pricing approaches in assessing the value associated with any derivatives on junior equity. A more in-depth discussion of this type of valuation is beyond the scope of this article.

Multi-national businesses are finding increasingly sophisticated ways to facilitate the movement of capital among different domiciles using a range of financial instruments. Preferred stock is a useful tool for public and large private company tax planning initiatives given its inherent flexibility in structuring between debt- and equity-like features. Businesses seeking to facilitate the movement of assets between legal entities can use preferred stock as an adaptable tool to achieve a wide range of economic outcomes.