English

English

Introduction

Stock options and other forms of stock-based compensation are frequently issued to company officers and key employees in start-up or early-stage companies in order to preserve cash and to align the incentives of key employees and investors. When reviewing Form S-1 registration statements for companies pursuing an initial public offering (“IPO”), the Securities and Exchange Commission (“SEC”) frequently targets stock-based compensation grants and the associated financial reporting requirements. Commonly referred to as “cheap stock” issues, the SEC is on the lookout for stock-based compensation grants that are substantially below Fair Value in the pre-IPO period, as well as inadequate disclosures of the grant-date Fair Values. SEC comment letters will cover all periods disclosed in the registration statement, including previous periods in which the company may have not yet pursued an IPO in earnest. Furthermore, the cheap stock issue may have significant tax consequences under Internal Revenue Code Section 409A (“IRC 409A”).

In an effort to provide best practices for the valuation of, and disclosures related to, the issuance of privately-held-company equity securities issued as compensation, the American Institute of Certified Public Accountants (“AICPA”) issued guidance in the form of a practice aid in 2004, which had become a critical resource for valuation experts, audit firms, and regulatory bodies.

In 2011, the AICPA issued a working draft of a replacement to the 2004 practice aid. After a period of public comment and subsequent edits, in 2013 the AICPA finalized the revised practice aid, Valuation of Privately-Held-Company Equity Securities Issued as Compensation (the “Practice Aid”).

The Practice Aid is available for purchase only in paperback, e-book, or online subscription from the AICPA website

Overview of Value Allocation Techniques

Common equity reflects a residual interest in a company’s value after considering senior securities such as debt and preferred stock. Typically, valuation analysts determine common equity value by first valuing the business as a whole, and then subtracting the senior securities in the capital structure. For example, debt and straight preferred stock are deducted from enterprise value (“EV”) to derive common equity value. This method of allocating EV is referred to as the Current Value Method (“CVM”).

By its very nature, the CVM assumes that the company is sold on the valuation date and the proceeds are distributed in accordance with investors’ liquidation rights. This approach may be appropriate in certain circumstances, but most companies operate as going concerns without an imminent liquidity event (e.g., a sale of the company, an IPO, or liquidation) and noncontrolling shareholders have no ability to unilaterally pursue a sale of the business.

Moreover, in situations where the subject company’s capital structure consists of complex securities (e.g., convertible preferred stock) or is highly leveraged, the valuation professional must take care to apportion EV or equity value to each security class based on their relative rights and preferences, considering that future increases (or decreases) in value may affect each security class differently.

To address these issues, the Practice Aid outlines two additional methods (plus a hybrid method) of allocating a company’s value to the various components of its capital structure. These methods are based on two key premises. First, the value of each class of securities should result from the security holders’ expectations about future economic events and the amounts, timing, and uncertainty of future cash flows. Second, at least some nominal value must be assigned to the common shares unless the enterprise is being liquidated and no cash is being distributed to the common shareholders (i.e., option value exists). These value allocation methods are the Probability-Weighted Expected Return Method (“PWERM”), the Option Pricing Method (“OPM”), and Hybrid Methods.

PWERM

The PWERM estimates the value of equity securities based on an analysis of various discrete future outcomes, such as an IPO, merger or sale, dissolution, or continued operation as a private enterprise until a later exit date. The equity value today is based on the probability-weighted present values of expected future investment returns, considering each of the possible outcomes available to the enterprise, as well as the rights of each security class. The following outlines the steps to perform a PWERM analysis.

- Determine the possible future outcomes available to the enterprise.

- Estimate the future equity value under each outcome.

- Allocate the estimated future equity value to each share class under each possible outcome according to the distribution or liquidation waterfall.

- Weight each possible future outcome by its respective probability to estimate the expected future probability-weighted cash flows to each share class.

- Discount the expected equity value allocated to each share class to a present value using a risk-adjusted discount rate. Note that each scenario may bear its own risk profile, and accordingly the discount rates used in each scenario may require different company-specific risk adjustments.

- Sum the probability-weighted present values allocated to each share class.

- Divide the present value allocated to each share class by the respective number of shares outstanding to calculate the value per share for each class.

- Consider additional adjustments, such as discounts, for lack of control or lack of marketability.

While the PWERM is intuitive, it requires significant and detailed assumptions regarding potential future outcomes. Estimating and supporting discrete event probabilities, and their associate timing, is inherently difficult and prone to optimism or conservatism. Because future outcomes must be explicitly modeled, the PWERM is generally more appropriate to use when the time to a liquidity event is short, making the range of possible future outcomes easier to predict. For example, a company may employ the OPM when the future liquidity events are uncertain, and begin to apply the PWERM (or Hybrid Methods) when its board of directors begins to evaluate exit opportunities in earnest by hiring investment bankers. In this regard, however, it is important to highlight that an IPO scenario is not a prerequisite in order to apply the PWERM. The PWERM may still be an acceptable approach in cases where the only two expected outcomes include (a) a sale or merger and (b) remaining private over a longer timeframe.

OPM

The OPM treats common stock or derivatives thereof as call options on the enterprise’s value or overall equity value. The value of a security is based on the optionality over and above the value securities that are senior in the capital structure (e.g., preferred stock), considering the dilutive effects of subordinate securities. In the OPM, the exercise price is based on a comparison with the overall equity value rather than per-share value. For example, common equity may be viewed as a call option on the total equity value with an exercise price equal to the liquidation preference of preferred stock. The OPM typically employs the Black-Scholes Option Pricing Model, although other option pricing models and techniques may be used depending on the complexity of the capital structure.

Unlike the PWERM, the OPM begins with the subject company’s current (rather than future) equity or enterprise value—representing the “asset price” in the option model—and incorporates a single expected term to a liquidity event rather than multiple potential exit dates. Similar to the PWERM, the OPM then estimates future potential outcomes of equity or enterprise value, although rather than just a few discrete outcomes, the OPM captures a lognormal distribution of potential outcomes around the current value.

The volatility factor selected in an OPM is a critical assumption that requires a significant degree of judgment. The Practice Aid outlines several key factors to consider when estimating volatility.

- For early stage companies, the selected volatility factor will often approach the upper end of the observed volatilities for the guideline public companies (especially for shorter timeframes), as the guideline public companies are likely larger, more profitable, and more diversified. Over the longer term, an appropriate volatility assumption may revert more toward the mean or median of the smaller guideline public companies.

- The effects of leverage can have a material impact on the selected volatility factor. As leverage increases, volatility increases. The Practice Aid provides examples whereby observed market volatilities are unlevered and relevered to better align with the subject company’s debt capitalization.

Debt may be incorporated in an OPM analysis by either (a) subtracting the Fair Value of debt from the company’s enterprise value to derive total equity, and then allocating that equity value between preferred and common stock via the OPM, or (b) building the OPM model on an enterprise basis whereby the zero-coupon bond equivalent of the debt over the assumed term is set as the first exercise price or breakpoint, and then allocating enterprise value between debt, preferred stock, and common stock via the OPM. If the OPM is performed on an enterprise value basis, the volatility measure should reflect unlevered (i.e., asset) volatility rather than equity volatility. In theory, both approaches should result in consistent value conclusions, although option (b)—building the OPM on an enterprise basis—may have the effect of shifting value away from the senior equity securities to the junior equity securities. For this reason, while the Practice Aid is clear that either method is acceptable, the task force believes that using the total equity value as the underlying asset, after deducting the Fair Value of the debt (option (a)), provides a better indication of the relative value of the junior and senior equity securities.

The Practice Aid also outlines circumstances in which it may be appropriate to consider more than one scenario, and then weighting each scenario according to the estimated probability. For example, if a class of convertible preferred stock has a forced conversion upon a qualifying IPO, but not in a sale of the company to a third party, the OPM can be performed under two scenarios. The sale scenario would assume the preferred stock has unlimited participation and the IPO scenario would assume forced conversion at the qualifying IPO threshold. As another example, the OPM may be performed in contemplation of a new financing round, although the pricing of the round may depend on whether certain milestones are achieved. One OPM scenario would assume the milestone is achieved and the other scenario would assume the milestone is not achieved.

The OPM is well-suited to many early-stage companies or later-stage companies with complex capital structures due to its ability to capture the option-like payoffs of various share classes based on today’s equity value, without discretely estimating specific future events or probabilities thereof. However, the OPM is highly sensitive to the inputs for volatility and expected term to a liquidity event, and can be complex to develop and calibrate appropriately.

Hybrid Method

Newly introduced in the 2013 Practice Aid is a Hybrid Method whereby the concepts of the PWERM and OPM are employed in a single framework. For example, suppose that the three scenarios considered in the PWERM were (a) an IPO, (b) a merger or sale of the business, or (c) remaining private. As previously described, the first two scenarios would be incorporated by (i) estimating the future equity value under each case, (ii) allocating the future value in each scenario according to the subject company’s capital structure, (iii) weighting each scenario, (iv) discounting the value to a present value equivalent using a risk-adjusted discount rate, and (v) considering discounts for lack of control or marketability, as appropriate. The third scenario, remaining private, is then modeled using the OPM over a reasonable timeframe until the senior securities (e.g., preferred stock) are redeemed or repurchased. The “stay private longer” scenario is then assigned its own weighting in relation to the IPO and merger or sale scenarios.

Backsolve Method

Also new to the 2013 Practice Aid is the “Backsolve Method.” The Backsolve Method, a form of the Market Approach to valuation, derives the implied equity value for one type of equity security (e.g., common equity) from a contemporaneous transaction involving another type of equity security (e.g., preferred stock).

- In a PWERM framework, the Backsolve Method involves selecting the future outcomes available to the enterprise, and then calibrating the future exit values, the probabilities for each scenario, and the discount rates for the various equity securities such that value for the most recent financing equals the amount paid for that security class.

- In an OPM framework, the Backsolve Method involves making assumptions regarding the time to liquidity, volatility, and risk-free rates, and then solving for the value of equity such that the value for the most recent financing equals the amount paid for that security class.

The resulting value from the analysis above may then require adjustment for any stated or unstated rights and privileges of the transacted security relative to the security being valued, including relative control and marketability attributes.1

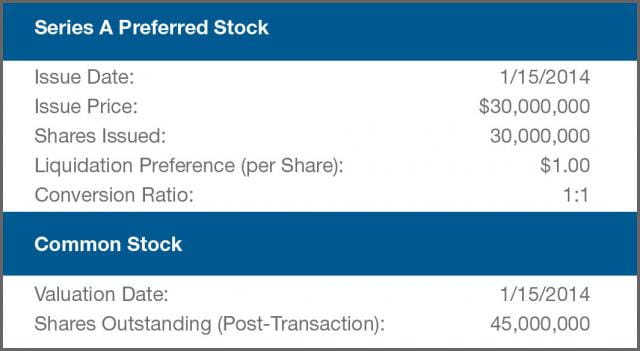

To illustrate the application of the Backsolve Method in an OPM framework, assume that ABC Company, Inc. (“ABC”) issued 30.0 million shares of Series A convertible preferred stock on January 15, 2014, with a liquidation preference of $1.00 per share (the “Preferred Stock”). The Preferred Stock has a conversion ratio of 1:1, is not entitled to dividends, and is voluntarily convertible into common stock. Prior to issuing the Preferred Stock, ABC had issued 42.0 million shares of common stock (the “Common Stock”) and the company issued an additional 3.0 million shares of Common Stock to its employees upon raising the new capital.

Table 1 - Assumptions

In order to comply with Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 718, Compensation—Stock Compensation (“FASB ASC 718”) and IRC 409A, ABC retained an independent valuation firm to determine the Fair Value and Fair Market Value of its Common Stock as of January 15, 2014.

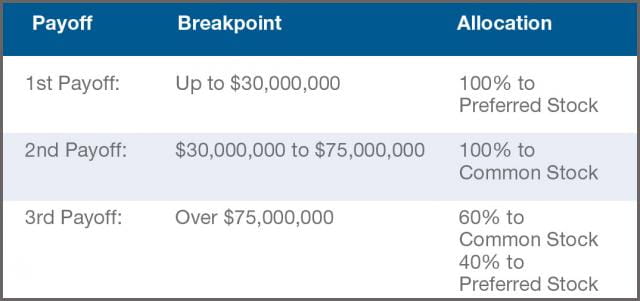

Table 2 - Payoff Breakpoints

After giving effect to the transactions previously described, ABC’s total equity value will first be allocated to the Preferred Stock up to $30.0 million, with no value being allocated to the Common Stock. The Common Stock holders are then allocated 100 percent of ABC’s incremental equity value, up to an additional $45.0 million ($75.0 million in aggregate). Above a total equity value of $75.0 million, it is economically advantageous for the Preferred Stock to convert into Common Stock; thus, holders of the Preferred Stock and Common Stock will share in any equity value above and beyond $75.0 million based on their relative ownership of ABC’s fully diluted shares.

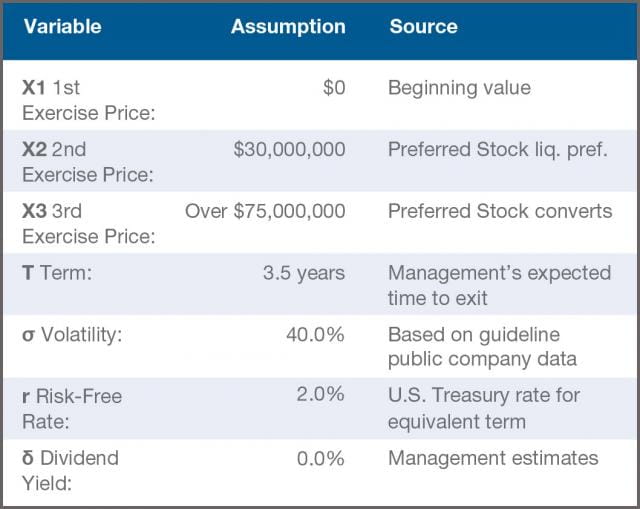

Table 3 - OPM Inputs

The OPM was selected to value the Common Stock via the Backsolve Method. To do so, the Black-Scholes Option Pricing Model is employed whereby the value of the Common Stock is based on the value of the optionality over and above the value of the Preferred Stock at each of the three breakpoints above. Table 3 outlines the key inputs to the OPM.

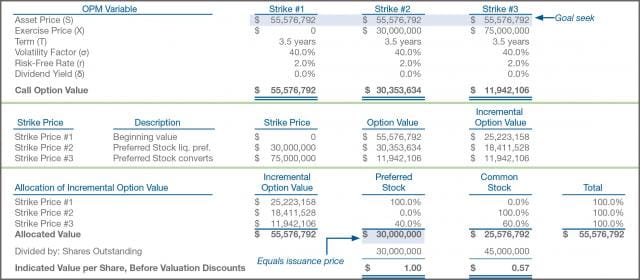

The results of the OPM are outlined in Table 4. The analysis is performed by way of solving for the total equity value that results in an allocated value to the Preferred Stock equal to $30.0 million (i.e., the issuance price). Based thereon, the total equity value is approximately $55.6 million and the value allocated to the Common Stock is approximately $25.6 million. Dividing by the number of shares outstanding results in an indicated value for the Common Stock of $0.57 per share.2

Table 4 - OPM: Backsolve Method

Different Purposes, Different Values?

We are often engaged by our clients to perform valuations for various purposes, users, and regulatory bodies, frequently as of the same valuation date, as it can be cost effective to complete the share-based payment valuation at the same time as the annual goodwill impairment analysis pursuant to FASB ASC Topic 350-20-35, Goodwill—Subsequent Measurement (“FASB ASC 350-20-35”). Moreover, the same valuation may be used by the company to determine the strike price for newly granted options to comply with IRC 409A. The following summarizes several key considerations when performing a valuation for multiple purposes.

Impairment Testing vs. Stock-Based Compensation

Goodwill impairment testing analyses are performed under the premise that the entire company or reporting unit is sold, whereas FASB ASC 718 is typically applied on a per-share (minority-interest) basis. Consequently, the inputs and assumptions should consider the most likely market participant for each respective unit of account. For impairment testing purposes, the market participant is a buyer for a controlling interest. For share-based payment purposes, the market participant is a buyer for a minority interest.

In a goodwill impairment setting, this may involve adjusting the subject company’s projected cash flows to correspond with market participant expectations (e.g., eliminating projected management fees to the private equity sponsor or incorporating market participant synergies) or deriving a discount rate that corresponds with the risk attributes of the most likely market participants (e.g., using a market participant capital structure or incorporating a risk premium for size based on the most likely market participants). Additionally, the goodwill impairment guidance requires that the tax attributes reflect the likely structure of a change of control transaction (i.e., stock vs. asset sale). To the extent not discretely incorporated in the cash flow projections, valuation analysts may also consider application of a market participant acquisition premium.

In a share-based payment setting, the equity valuation should consider the company’s operations under current ownership due to the inability of a minority shareholder to unilaterally alter the company’s cash flows or capital structure in the way that a controlling shareholder can. In contrast to the goodwill impairment analysis:

- The projected cash flows should include any projected management fees to the private equity sponsor

- Market participant synergies should not be considered

- The discount rate should consider the company’s existing capital structure, size-related risk, and cost of debt

- The tax attributes should not consider any potential changes arising from a change in control

- To the extent justified, valuation analysts may consider discounts for lack of control or marketability

It should be clarified that the recommendations above for a share-based payment valuation depend on the circumstances of the controlling owner. For example, although a minority shareholder cannot force a sale of the company, it is reasonable to assume that a venture capital or private equity-owned business will seek a liquidity event. In this case, it may be appropriate to use entity-specific assumptions until the expected liquidity event, and then consider market participant assumptions upon the liquidity event.

FASB ASC 718 vs. IRC 409A

The valuation of equity securities performed for financial reporting purposes may also differ from the value determined for tax-related purposes. The primary difference relates to valuation adjustments arising from restrictions that are a characteristic of the security (which would be transferred to market participants) versus the security holder (or the size of the security holder’s block of securities). For example, an equity security may not maintain any explicit restrictions on transferability. Still, the security holder has limited options to sell their securities due to a limited population of transferees, creating an implicit restriction. As provided in FASB ASC 718-10-30, the value of the security for financial reporting purposes would not be discounted due solely to the fact that the share could be transferred to a limited population of investors. However, these types of restrictions are often considered in estimating Fair Market Value for IRC 409A purposes. Similarly, “blockage” discounts are often considered in equity valuations for tax purposes to account for the difficulty associated with liquidating a large block of stock. Such discounts are not permitted for financial reporting purposes.

Other Highlights

Several other areas of the Practice Aid not highlighted in this article deserve review, including:

- A discussion surrounding adjustments for control and marketability

- An overview of the IPO process and the impact on value resulting from an IPO

- Inferring value from transactions in private company stock

- Recommended financial statement and pre-IPO disclosures

- Updated guidance for new financial reporting standards, including the relevance of FASB ASC Topic 820, Fair Value Measurement (“FASB ASC 820”) to FASB ASC 718

- Updates for AICPA valuation standards

Conclusion

Best practices for the valuation of privately held equity securities continue to evolve and the Practice Aid provides a comprehensive set of guidelines for boards of directors that issue these securities, valuation experts, auditors, and other interested parties (such as creditors). Still, the technical rigor and analytical proficiency required to meet these standards remain high. Private companies issuing stock-based compensation are well-served by coupling equity grants with a comprehensive valuation of the securities in order to meet financial reporting requirements, to avoid any unintended IRC 409A tax consequences, and to avoid delays in an IPO due to additional disclosures, restatements, and added professional fees.

1 The Backsolve Method indicates an equity value that is consistent with the private equity or venture capital investors’ expected rate of return, given the degree of control they have over the enterprise and the degree of marketability of their investment.

2 Before adjustments for differences between preferred and common shares in terms of control rights and liquidity.